- Executive Summary

- Europe Household Refrigerator Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Europe GDP Outlook

- Europe Consumer Appliances Market Growth Outlook

- Europe Consumer Goods Per Capita Spending by Country

- Forecast Factors – Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 – 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Europe Household Refrigerator Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Europe Household Refrigerator Market Outlook: Product Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Product Type, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- Single Door

- Double Door

- French Door

- Side by Side Door

- Market Attractiveness Analysis: Product Type

- Europe Household Refrigerator Market Outlook: Capacity

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Capacity, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Capacity, 2026-2033

- <200 Liters

- 200–400 Liters

- >400 Liters

- Market Attractiveness Analysis: Capacity

- Europe Household Refrigerator Market Outlook: Installation Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Installation Type, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Installation Type, 2026-2033

- Free-Standing Refrigerators

- Built-in / Integrated Refrigerators

- Market Attractiveness Analysis: Installation Type

- Europe Household Refrigerator Market Outlook: Sales Channel

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Sales Channel, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Sales Channel, 2026-2033

- Online

- Offline

- Market Attractiveness Analysis: Sales Channel

- Europe Household Refrigerator Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Region, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Market Attractiveness Analysis: Region

- Germany Household Refrigerator Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Germany Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- Single Door

- Double Door

- French Door

- Side by Side Door

- Germany Market Size (US$ Bn) and Volume (Units) Forecast, by Capacity, 2026-2033

- <200 Liters

- 200–400 Liters

- >400 Liters

- Germany Market Size (US$ Bn) and Volume (Units) Forecast, by Installation Type, 2026-2033

- Free-Standing Refrigerators

- Built-in / Integrated Refrigerators

- Germany Market Size (US$ Bn) and Volume (Units) Forecast, by Sales Channel, 2026-2033

- Online

- Offline

- Italy Household Refrigerator Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Italy Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- Single Door

- Double Door

- French Door

- Side by Side Door

- Italy Market Size (US$ Bn) and Volume (Units) Forecast, by Capacity, 2026-2033

- <200 Liters

- 200–400 Liters

- >400 Liters

- Italy Market Size (US$ Bn) and Volume (Units) Forecast, by Installation Type, 2026-2033

- Free-Standing Refrigerators

- Built-in / Integrated Refrigerators

- Italy Market Size (US$ Bn) and Volume (Units) Forecast, by Sales Channel, 2026-2033

- Online

- Offline

- France Household Refrigerator Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- France Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- Single Door

- Double Door

- French Door

- Side by Side Door

- France Market Size (US$ Bn) and Volume (Units) Forecast, by Capacity, 2026-2033

- <200 Liters

- 200–400 Liters

- >400 Liters

- France Market Size (US$ Bn) and Volume (Units) Forecast, by Installation Type, 2026-2033

- Free-Standing Refrigerators

- Built-in / Integrated Refrigerators

- France Market Size (US$ Bn) and Volume (Units) Forecast, by Sales Channel, 2026-2033

- Online

- Offline

- U.K. Household Refrigerator Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- U.K. Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- Single Door

- Double Door

- French Door

- Side by Side Door

- U.K. Market Size (US$ Bn) and Volume (Units) Forecast, by Capacity, 2026-2033

- <200 Liters

- 200–400 Liters

- >400 Liters

- U.K. Market Size (US$ Bn) and Volume (Units) Forecast, by Installation Type, 2026-2033

- Free-Standing Refrigerators

- Built-in / Integrated Refrigerators

- U.K. Market Size (US$ Bn) and Volume (Units) Forecast, by Sales Channel, 2026-2033

- Online

- Offline

- Spain Household Refrigerator Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Spain Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- Single Door

- Double Door

- French Door

- Side by Side Door

- Spain Market Size (US$ Bn) and Volume (Units) Forecast, by Capacity, 2026-2033

- <200 Liters

- 200–400 Liters

- >400 Liters

- Spain Market Size (US$ Bn) and Volume (Units) Forecast, by Installation Type, 2026-2033

- Free-Standing Refrigerators

- Built-in / Integrated Refrigerators

- Spain Market Size (US$ Bn) and Volume (Units) Forecast, by Sales Channel, 2026-2033

- Online

- Offline

- Russia Household Refrigerator Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Russia Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- Single Door

- Double Door

- French Door

- Side by Side Door

- Russia Market Size (US$ Bn) and Volume (Units) Forecast, by Capacity, 2026-2033

- <200 Liters

- 200–400 Liters

- >400 Liters

- Russia Market Size (US$ Bn) and Volume (Units) Forecast, by Installation Type, 2026-2033

- Free-Standing Refrigerators

- Built-in / Integrated Refrigerators

- Russia Market Size (US$ Bn) and Volume (Units) Forecast, by Sales Channel, 2026-2033

- Online

- Offline

- Russia Household Refrigerator Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Russia Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- Single Door

- Double Door

- French Door

- Side by Side Door

- Russia Market Size (US$ Bn) and Volume (Units) Forecast, by Capacity, 2026-2033

- <200 Liters

- 200–400 Liters

- >400 Liters

- Russia Market Size (US$ Bn) and Volume (Units) Forecast, by Installation Type, 2026-2033

- Free-Standing Refrigerators

- Built-in / Integrated Refrigerators

- Russia Market Size (US$ Bn) and Volume (Units) Forecast, by Sales Channel, 2026-2033

- Online

- Offline

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Liebherr

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Samsung

- Whirlpool

- LG

- Haier

- Bosch

- Midea

- Electrolux

- Miele

- Brandt

- Liebherr

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Home Appliances

- Europe Household Refrigerator Market

Europe Household Refrigerator Market Size, Share, and Growth Forecast 2026 - 2033

Europe Household Refrigerator Market by Product Type (Single Door, Double Door, French Door, Side-by-Side Door), Capacity (<200 Liters, 200–400 Liters, >400 Liters), Installation Type (Free-Standing Refrigerators, Built-in / Integrated Refrigerators), Sales Channel (Online, Offline), and Regional Analysis for 2026 - 2033

Europe Household Refrigerator Market Size and Trend Analysis

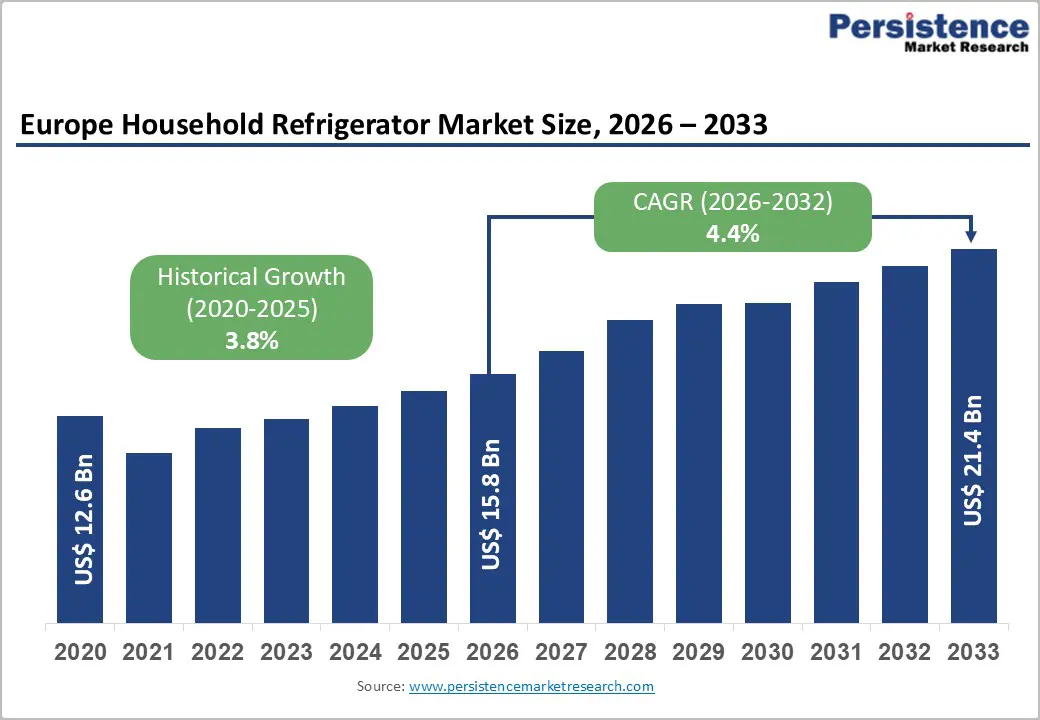

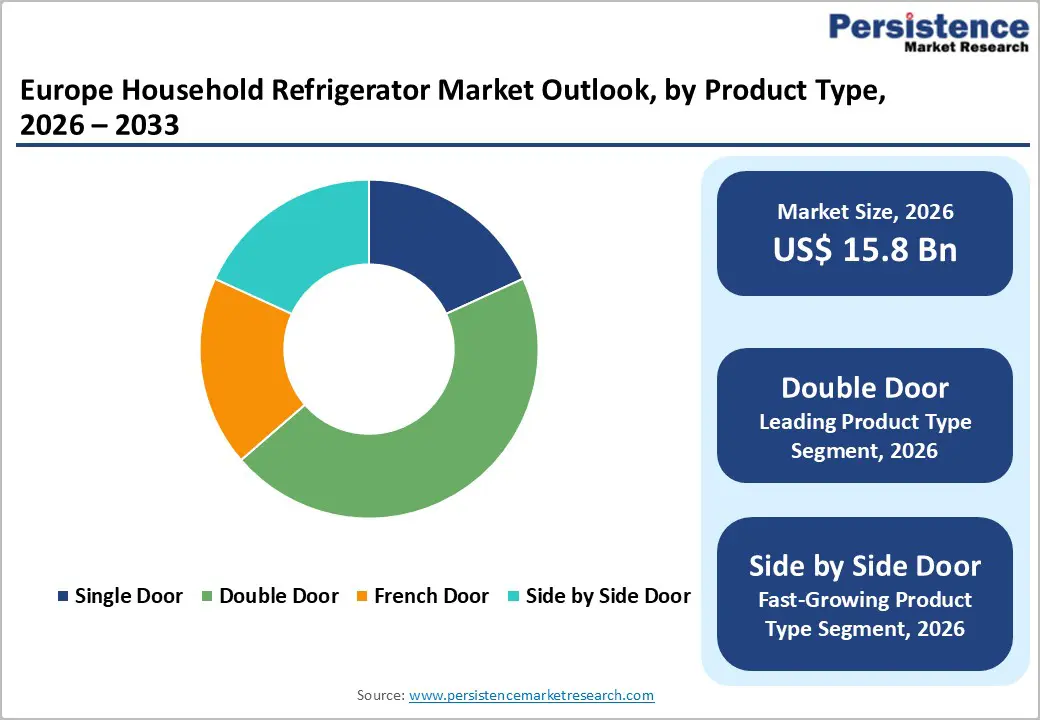

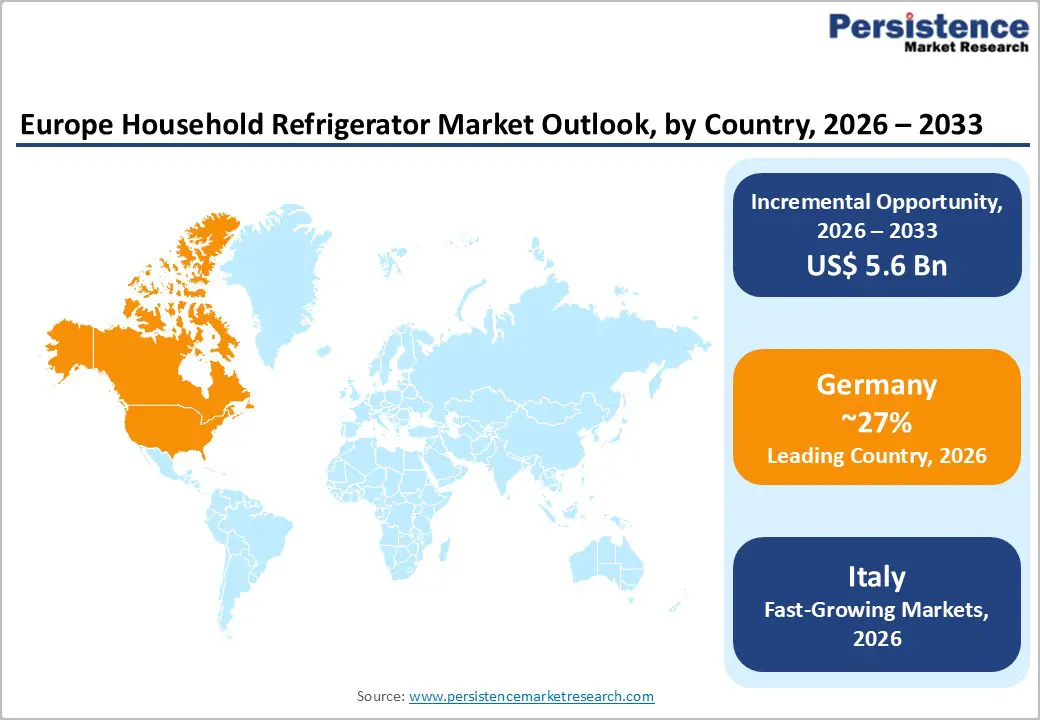

Europe Household Refrigerator market size is estimated to be valued at US$ 15.8 billion in 2026 and is projected to reach US$ 21.4 billion by 2033, growing at a CAGR of 4.4% between 2026 and 2033.

The market's consistent growth trajectory is principally driven by the European Union's aggressive energy efficiency mandates, rising consumer demand for smart and connected appliances, and the structural replacement cycle of aging refrigerator fleets across Western and Eastern European households. Growing middle-class purchasing power in Central and Eastern European (CEE) economies and the rising penetration of premium refrigerator categories, including French door and side-by-side models, are continuously elevating average selling prices and overall market value across the forecast horizon.

Key Industry Highlights:

- Dominant Country: Germany leads Europe Household Refrigerator market, driven by the continent's highest per-capita appliance spending, dominant domestic presence of BSH Hausgeräte GmbH, and accelerated replacement demand following the 2021 EU Energy Label rescaling that rendered millions of legacy appliances functionally inefficient.

- Emerging Country: Central and Eastern Europe (CEE) is the fastest-growing regional sub-market, propelled by rising household incomes, urbanization, and government-backed housing programs in Poland, Czech Republic, and Romania that are accelerating first-time and upgrade refrigerator purchases among an expanding middle-class consumer base.

- Dominant Product Type: Double Door refrigerators dominate the Product Type segment with approximately 41% revenue share, anchored by their optimal balance of refrigeration and freezer capacity within compact footprints suited to European kitchen dimensions and strong representation across all price tiers from entry-level to premium.

- Fastest Growing Installation Type: Built-in / Integrated Refrigerators are the fastest-growing Installation segment, driven by expanding premium kitchen renovation activity across Germany, Austria, and Scandinavia, where seamless fitted kitchen aesthetics and Ecodesign-compliant integrated appliances command 40–60% price premiums over equivalent free-standing models.

- Opportunity: Direct-to-consumer e-commerce expansion represents the key market opportunity, with online household appliance sales growing at over 14% CAGR across Europe through 2023, enabling manufacturers to capture higher margins, improve brand control, and deploy AR visualization and AI recommendation tools to reduce consumer hesitation in premium digital appliance purchases.

| Key Insights | Details |

|---|---|

|

Europe Household Refrigerator Market Size (2026E) |

US$ 15.8 Billion |

|

Market Value Forecast (2033F) |

US$ 21.4 Billion |

|

Projected Growth CAGR (2026–2033) |

4.4% |

|

Historical Market Growth (2020–2025) |

3.8% |

Market Dynamics

Drivers - EU Energy Efficiency Mandates and Ecodesign Regulations Accelerating Replacement Demand

The European Union's Ecodesign Regulation for household refrigerators, enforced under Commission Regulation (EU) 2019/2019, has established mandatory minimum energy performance standards that compelled manufacturers to phase out low-efficiency models from the European market by March 2021. The simultaneous introduction of the rescaled EU Energy Label, replacing the former A+++ system with a simplified A-to-G scale, has fundamentally shifted consumer perception, reclassifying most previously A-rated appliances to lower D or E bands.

According to Eurostat, approximately 38% of European households still operated refrigerators more than 10 years old as of 2023, representing a structurally large and price-sensitive replacement demand pipeline. The European Commission's Circular Economy Action Plan further incentivizes the uptake of longer-lasting, repairable, and energy-efficient appliances through mandatory repairability indices, driving manufacturers to invest in next-generation compressor technologies, including variable-speed inverter compressors, which are delivering measurable energy consumption reductions of up to 30–40% compared to conventional fixed-speed models.

Rising Smart Home Adoption and Connected Appliance Penetration

Europe's rapidly expanding smart home ecosystem is generating compelling demand for Wi-Fi and IoT-enabled household refrigerators equipped with touchscreen interfaces, remote temperature monitoring, inventory management systems, and integration with voice-activated assistants such as Amazon Alexa and Google Assistant. According to the European Consumer Organisation (BEUC), smart home device penetration across the EU-27 is projected to exceed 35% of households by 2027, significantly above 2022 levels of approximately 15%.

Countries including Germany, France, and the Netherlands are leading smart appliance adoption, driven by high broadband infrastructure density and strong consumer spending power. Major manufacturers including BSH Hausgeräte GmbH, LG Electronics, and Samsung Electronics have embedded proprietary smart platform ecosystems, Home Connect, ThinQ, and SmartThings respectively, directly into premium refrigerator product lines, creating powerful brand differentiation and recurring digital service revenue streams that are reshaping competitive dynamics across the European premium appliance segment.

Restraints - Prolonged Product Replacement Cycles Limiting New Unit Sales Growth

Household refrigerators are inherently long-life consumer durables, with average operational lifespans of 10 to 15 years widely reported across industry technical documentation and European Ecodesign preparatory study findings. This extended replacement cycle structurally constrains annual unit shipment volume, as a large proportion of European households with relatively newer appliances, particularly in Western Europe, defer replacement purchases until functional failure or a compelling energy savings argument materializes.

The Association of Home Appliance Manufacturers Europe (APPLiA) has reported that post-pandemic demand normalization from 2022 onward has led to volume softening in key markets including Germany and France, following an exceptional replacement surge driven by pandemic-era home renovation activity. These cyclical demand patterns limit the pace of new refrigerator sales, capping near-term market volume expansion despite positive long-run structural drivers.

Escalating Raw Material and Component Costs Compressing Manufacturer Margins

The European household refrigerator manufacturing sector faces significant cost-side pressures arising from elevated steel, aluminum, copper, and synthetic foam insulation prices, core input materials accounting for a substantial portion of total bill-of-materials costs. The European Steel Association (EUROFER) reported that hot-rolled coil steel prices in Europe remained elevated through 2023–2024 compared to pre-pandemic baselines, directly increasing manufacturing costs for appliance producers with European production footprints.

Compounding these pressures, the EU F-Gas Regulation (EU) 2024/573, which has tightened restrictions on high Global Warming Potential (GWP) hydrofluorocarbon refrigerants, requires manufacturers to accelerate their transition to alternative refrigerants such as isobutane (R-600a) and propane (R-290), entailing significant product reformulation, re-certification, and tooling costs that are difficult to fully pass through to price-sensitive retail consumers.

Opportunity - Built-in and Integrated Refrigerators Gaining Momentum in Premium Kitchen Design Segment

The Built-in / Integrated Refrigerator segment presents a high-margin and rapidly expanding opportunity for refrigerator manufacturers targeting Europe's premium kitchen and home renovation market. Driven by architectural trends favoring seamless kitchen aesthetics, Nordic and minimalist interior design movements, and the proliferation of bespoke fitted kitchen installations, demand for refrigerators that integrate invisibly behind cabinetry panels is growing substantially across Germany, Austria, Scandinavia, and the United Kingdom.

The European Kitchen Furniture Association (EFCI) has reported that fitted and semi-fitted kitchen installations account for over 70% of all new kitchen purchases across the EU's top-five consumer markets, creating a structurally embedded demand pipeline for built-in refrigeration solutions. Premium brands including Liebherr, Miele, and Neff (BSH) have positioned integrated refrigerator lines at price points 40–60% higher than comparable free-standing alternatives, offering meaningfully superior gross margin profiles. Manufacturers that develop modular built-in platforms with flexible capacity configurations and fast installation systems are positioned to unlock significant commercial opportunity across the premium European kitchen segment.

E-Commerce Channel Expansion Enabling Direct-to-Consumer Premium Appliance Sales

The accelerating shift of household appliance purchases toward online and direct-to-consumer e-commerce platforms represents a strategically significant growth opportunity for refrigerator manufacturers seeking to improve margin capture and brand control in Europe. According to the European E-Commerce Association, online sales of major household appliances in Europe grew at a CAGR exceeding 14% between 2019 and 2023, with Germany, France, and the United Kingdom accounting for the largest share of digital appliance transactions. The COVID-19 pandemic fundamentally recalibrated European consumer comfort with high-value appliance purchases through digital channels, a behavioral shift that has proven durable in post-pandemic purchasing patterns.

Leading brands including Samsung Electronics, LG Electronics, and Electrolux AB have invested heavily in direct-to-consumer digital storefronts, augmented reality (AR) visualization tools, and AI-powered product recommendation systems that reduce consumer hesitation in making large-ticket online appliance commitments. Manufacturers that strategically combine direct digital sales with efficient last-mile delivery and in-home installation service networks can achieve materially higher average transaction values and foster stronger customer lifetime relationships compared to traditional retail intermediaries.

Category-wise Insights

By Product Type

The double door refrigerator segment dominates by product type, commanding approximately 41% of total market revenue share in 2026. Double door refrigerators, featuring separate top-mounted freezer or bottom-mounted freezer configurations, deliver an optimal balance of usable refrigeration and freezer storage capacity within a compact footprint that is well-suited to the typical European apartment and house kitchen dimensions. Eurostat's household survey data indicates that combined refrigerator-freezer units represent the majority of European household appliance inventories, as European consumers predominantly prefer integrated refrigeration and freezing capability within a single appliance rather than separate dedicated units.

Leading manufacturers including BSH Hausgeräte GmbH (Bosch, Siemens), Electrolux AB, and Liebherr have concentrated their highest-volume product ranges within the double door category, supported by broad retail distribution across hypermarkets, specialist appliance retailers, and e-commerce platforms. Meanwhile, French Door refrigerators are the fastest-growing product type, gaining rapid traction in premium consumer segments as living standards and kitchen space availability improve across Western Europe.

By Capacity

The 200–400 Liters capacity segment leads the Europe Household Refrigerator market by capacity, representing approximately 55% of total market revenue share in 2026. This dominant capacity band directly corresponds to the storage requirements of the typical European household comprising 2.3 persons on average, as reported by Eurostat's household composition statistics for the EU-27. Refrigerators within the 200–400 Liter range offer sufficient total gross volume to meet the weekly grocery storage needs of a standard European family while remaining compliant with typical urban kitchen spatial constraints. The segment benefits from the broadest product variety across all major price tiers, from entry-level brands targeting Eastern European consumers to premium inverter models marketed in Germany, France, and Scandinavia.

Manufacturers have intensively focused their Ecodesign-compliant product development within this capacity band, rolling out next-generation models featuring No-Frost technology, dual-cooling systems, and precision humidity-controlled fresh zones that appeal to health-conscious and sustainability-aware European consumers.

Installation Type

Free-Standing Refrigerators maintain dominant leadership in the Europe Household Refrigerator market by installation type, accounting for approximately 73% of total installation segment revenue in 2026. The enduring dominance of free-standing refrigerators reflects their broad accessibility across all price segments, ease of installation, and compatibility with the diverse and non-standardized kitchen configurations prevalent across Europe's varied housing stock, including pre-war apartment buildings in France and Italy and terraced housing across the United Kingdom, where bespoke built-in cabinetry is not a structural feature.

The significantly lower total acquisition cost of free-standing models compared to built-in alternatives makes them the default choice for cost-conscious consumers, rental property landlords, and housing developers equipping new residential units at volume. However, Built-in / Integrated Refrigerators represent the fastest-growing installation sub-segment, driven by growing consumer investment in premium kitchen renovations and the proliferation of fitted kitchen installations, particularly across Germany, Austria, and the Nordic countries, where integrated appliance aesthetics are deeply embedded in kitchen design culture.

Sales Channel

The Offline sales channel retains leadership in the Europe Household Refrigerator market, representing approximately 62% of total market revenue in 2026. Offline retail channels, comprising large-format appliance specialist chains such as MediaMarkt, Darty (Fnac Darty), Currys, and Euronics, continue to dominate household refrigerator sales primarily because consumers prefer to physically inspect and compare large home appliances before purchase, particularly given the high unit price and long commitment horizon associated with refrigerator ownership. In-store demonstrations of features such as No-Frost performance, drawer ergonomics, LED lighting, and noise levels remain persuasive and difficult to replicate through digital channels alone.

The Online segment is the fastest-growing sales channel, consistently gaining share driven by the acceleration of e-commerce adoption for high-value goods across Germany, France, and the United Kingdom, where leading platforms including Amazon, Cdiscount, and manufacturer direct stores are capturing an expanding proportion of appliance purchase journeys initiated through digital product research and price comparison platforms.

Regional Insights

Germany Household Refrigerator Market Trends

Germany is Europe's largest household appliance market and the epicenter of premium refrigerator demand on the continent, driven by strong consumer purchasing power, a deeply embedded culture of quality-conscious home appliance investment, and a dense retail and e-commerce ecosystem for white goods. The GfK Consumer Appliance Tracking has consistently identified Germany as the highest per-capita spender on household appliances within the EU, with premium categories including built-in refrigerators and large-capacity French door models growing disproportionately. The Gesellschaft für Konsumforschung (GfK) has documented a sustained shift toward energy class A appliances following the 2021 EU Energy Label reform, as German consumers, highly attuned to energy costs, actively seek the lowest long-run operating cost appliances.

Germany's refrigerator market is also characterized by the dominant domestic presence of BSH Hausgeräte GmbH, owner of the Bosch, Siemens, Neff, and Gaggenau brands, which commands the highest single-brand market share in the country. German consumers' preference for made-in-Germany engineering quality sustains a meaningful premium positioning for domestic brands that outperforms most other European markets. The German Energy Agency (Deutsche Energie-Agentur / dena) has actively promoted appliance energy efficiency through consumer awareness programs, further accelerating the pace of low-efficiency refrigerator replacement and reinforcing demand for next-generation inverter and variable-cooling models.

France Household Refrigerator Market Trends

France is Europe's second-largest household refrigerator market, characterized by a balanced mix of mid-range and premium product demand, a well-established multi-format retail structure, and progressive policy measures targeting household energy efficiency. The French Environment and Energy Management Agency (ADEME) has been instrumental in shaping consumer and industry behavior through its Bonus-Réparation repair incentive scheme, part of France's Anti-Waste Law for a Circular Economy (AGEC), which financially subsidizes appliance repairs to extend product lifespans and reduce electronic waste. This policy framework, while moderating near-term replacement volumes among some consumer segments, simultaneously reinforces premium product positioning by highlighting the long-term cost-of-ownership advantages of high-durability appliances.

France's household refrigerator demand is further supported by significant urban housing construction activity driven by the Plan Logement national housing program and ongoing renovation of existing residential stock under the MaPrimeRénov' energy renovation subsidy scheme, both of which generate new appliance installation demand. French consumers demonstrate growing interest in connected refrigerators integrated with smart home platforms, supported by Orange and Bouygues Telecom's expanding smart home service offerings. Brands including Samsung, LG, and Electrolux (AEG) are actively gaining market share in France's urban premium segment, competing alongside traditional market leaders Bosch and Whirlpool through competitive digital direct-to-consumer strategies.

Italy Household Refrigerator Market Trends

Italy occupies a strategically distinctive position in Europe's household refrigerator landscape, functioning simultaneously as one of the continent's significant consumer markets and as a notable manufacturing base for white goods components and finished appliances. Italian consumers exhibit strong brand loyalty toward both domestic and well-established international appliance brands, with mid-range and premium double door and built-in refrigerators particularly popular in the country's design-conscious residential renovation segment. The Italian National Institute of Statistics (ISTAT) has documented sustained growth in household spending on durable goods, including appliances, supported by government incentive programs such as the Bonus Elettrodomestici and the broader Superbonus renovation tax credit scheme that has stimulated significant residential upgrade activity across the country.

Italy's industrial heartland, particularly the Veneto and Emilia-Romagna regions, hosts production facilities supplying components for major global appliance brands, establishing the country as an important node in Europe's white goods supply chain. The Italian Household Appliance Manufacturers Association (APPLiA Italia) has reported that domestic appliance production volumes have remained resilient, supported by both domestic demand and export competitiveness within the EU single market. Italy's growing adoption of energy-efficient inverter refrigerators and its expanding built-in kitchen segment, driven by Italy's globally influential furniture design sector including Scavolini, Snaidero, and Valcucine, are reinforcing demand for premium refrigeration solutions within the country's design-oriented consumer base.

Competitive Landscape

Europe household refrigerator market is moderately consolidated, with a group of large multinational and European heritage brands, BSH Hausgeräte GmbH, Electrolux AB, Whirlpool Corporation, LG Electronics, and Samsung Electronics, collectively commanding a substantial majority of regional revenue. Key competitive differentiators include Ecodesign regulatory compliance capability, smart connectivity ecosystem depth, design heritage, and service network reach. Liebherr and Miele anchor the ultra-premium tier through engineering quality and longevity positioning.

Emerging business model trends include appliance-as-a-service (AaaS) subscription pilots and digital aftersales platforms generating recurring service revenue. Asian manufacturers including Haier Group and Midea Group are systematically expanding European share through competitive pricing and targeted acquisition strategies, Haier notably completed its acquisition of Candy to strengthen European market presence.

Key Developments:

- In January 2025, LG Electronics launched its latest InstaView Door-in-Door refrigerator lineup in Europe, incorporating AI-powered ThinQ energy optimization and a Linear Inverter Compressor delivering up to 32% energy savings, targeting the growing A-rated premium refrigerator segment across Germany, France, and the United Kingdom.

- In September 2024, BSH Hausgeräte GmbH announced the expansion of its Home Connect smart appliance ecosystem to support Matter interoperability protocol, enabling seamless integration of Bosch and Siemens refrigerators with third-party smart home platforms and significantly enhancing its competitive positioning in Europe's connected appliance market.

- In March 2024, Electrolux AB unveiled its next-generation UltimateTaste 900 refrigerator series across European markets, featuring a dual MultiFlow air circulation system and TasteGuard freshness technology, reinforcing the company's strategic positioning at the premium fresh-food preservation segment ahead of the 2024 European Home Appliance Season.

Companies Covered in Europe Household Refrigerator Market

- BSH Hausgeräte GmbH (Bosch, Siemens, Neff, Gaggenau)

- Electrolux AB (Electrolux, AEG, Zanussi)

- Whirlpool Corporation (Whirlpool, Indesit, Hotpoint)

- LG Electronics Inc.

- Samsung Electronics Co., Ltd.

- Liebherr-Hausgeräte GmbH

- Miele & Cie. KG

- Haier Group (Candy, Hoover)

- Arçelik A.Ş. (Beko, Grundig)

- Panasonic Corporation

- Midea Group Co., Ltd.

- Sharp Corporation

- Hisense Group Co., Ltd.

- Gorenje Group (Hisense subsidiary)

- Vestfrost Solutions A/S

Frequently Asked Questions

The Europe Household Refrigerator market is estimated to be valued at US$ 15.8 billion in 2026 and is projected to reach US$ 21.4 billion by 2033, registering a forecast CAGR of 4.4% over the period 2026 to 2033. The market recorded a historical growth rate of 3.8% CAGR between 2020 and 2025.

The primary growth drivers are the European Commission's Ecodesign Regulation and the rescaled EU Energy Label (2021), which rendered a large proportion of legacy refrigerators obsolete and triggered accelerated replacement demand. Rising smart home adoption, with EU-27 smart device penetration projected to exceed 35% by 2027 per the European Consumer Organisation (BEUC), is further driving demand for connected and IoT-enabled premium refrigerators.

The Double Door refrigerator segment leads the product type category with approximately 41% market revenue share in 2026. Its dominance is driven by its alignment with the typical European household storage requirement for integrated refrigerator-freezer units, broad price tier availability, and strong manufacturer focus on Ecodesign-compliant double door models featuring No-Frost and inverter compressor technologies.

Germany leads the European Household Refrigerator market, recording the continent's highest per-capita appliance expenditure as tracked by GfK Consumer Appliance data. The country's strong demand for premium and energy-efficient refrigerators, combined with the dominant domestic presence of BSH Hausgeräte GmbH and accelerated replacement cycles driven by the 2021 EU Energy Label reform, collectively reinforce Germany's regional market leadership.

The most significant growth opportunity lies in Built-in / Integrated Refrigerators and direct-to-consumer e-commerce expansion. The European Kitchen Furniture Association (EFCI) reports that over 70% of new EU kitchen purchases are fitted installations, structurally driving built-in refrigerator demand. Simultaneously, online household appliance sales growing at over 14% CAGR offer manufacturers substantially higher margin capture compared to traditional retail intermediary channels.

The leading companies include BSH Hausgeräte GmbH (Bosch, Siemens, Neff), Electrolux AB (Electrolux, AEG, Zanussi), Whirlpool Corporation (Indesit, Hotpoint), LG Electronics Inc., Samsung Electronics Co., Ltd., Liebherr-Hausgeräte GmbH, Miele & Cie. KG, Haier Group (Candy, Hoover), Arçelik A.Ş. (Beko, Grundig), and Midea Group Co., Ltd., among other prominent players operating across Europe's premium, mid-range, and value refrigerator segments.