- Medical Devices

- Electrosurgical Cautery Market

Electrosurgical Cautery Market Size, Share, and Growth Forecast, 2026 - 2033

Electrosurgical Cautery Market by Product Type (Monopolar, Others), Electrosurgical Unit (ESU) Type (Cutting Electrosurgical Units, Others), Application (General Surgery, Others), End-user (Hospitals, Others), and Regional Analysis for 2026 – 2033

Electrosurgical Cautery Market Size and Trends Analysis

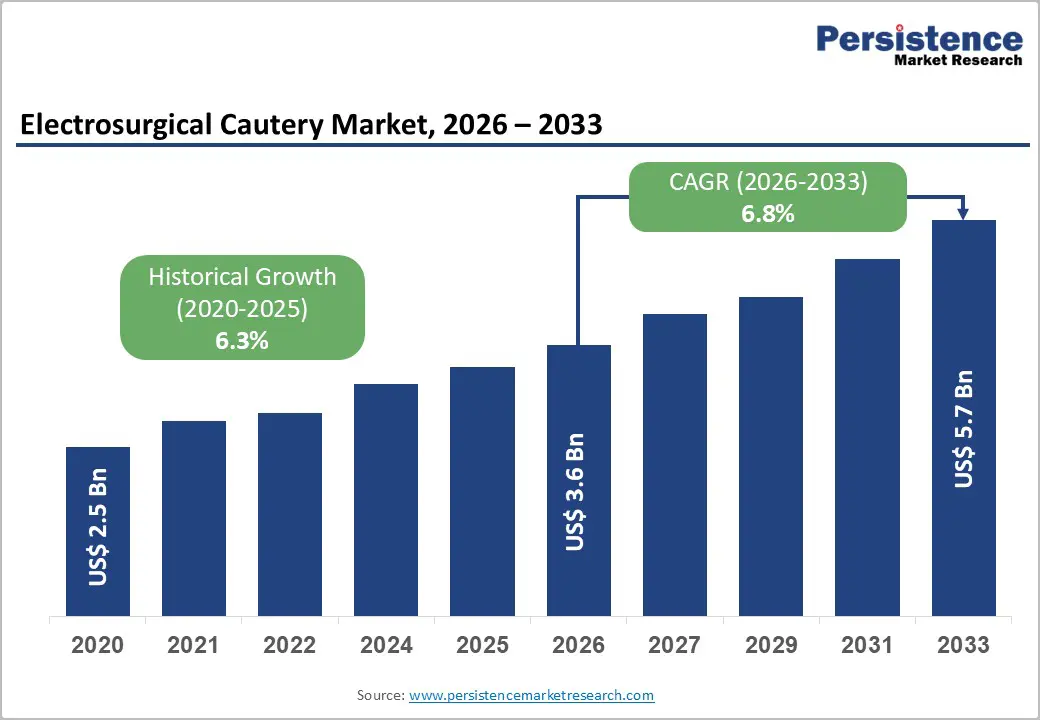

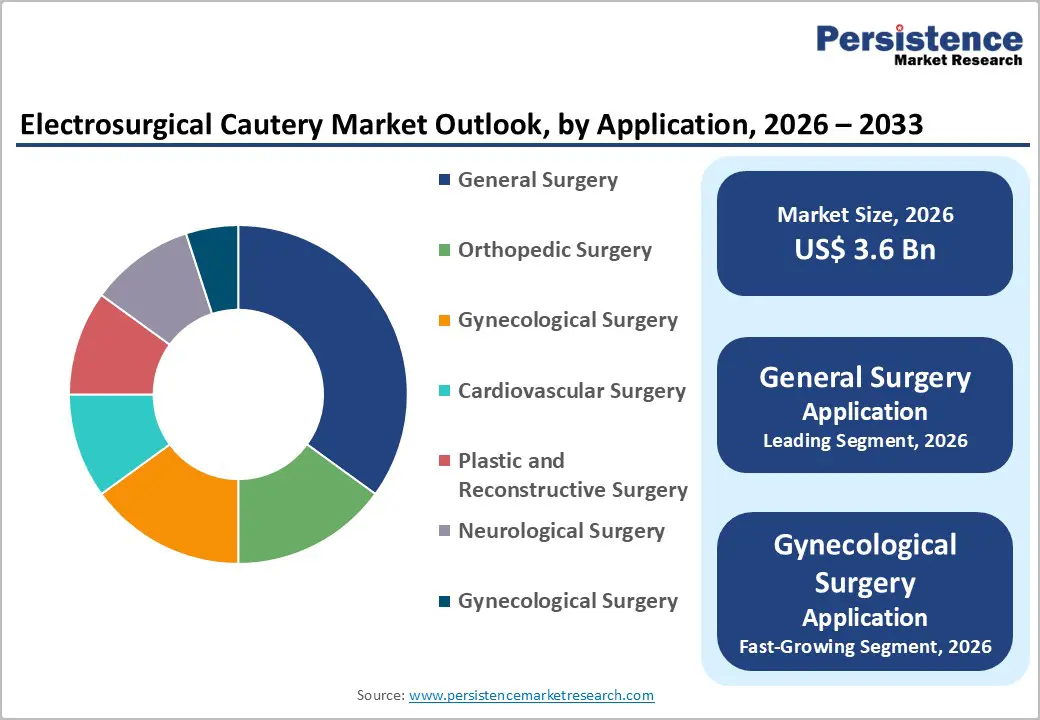

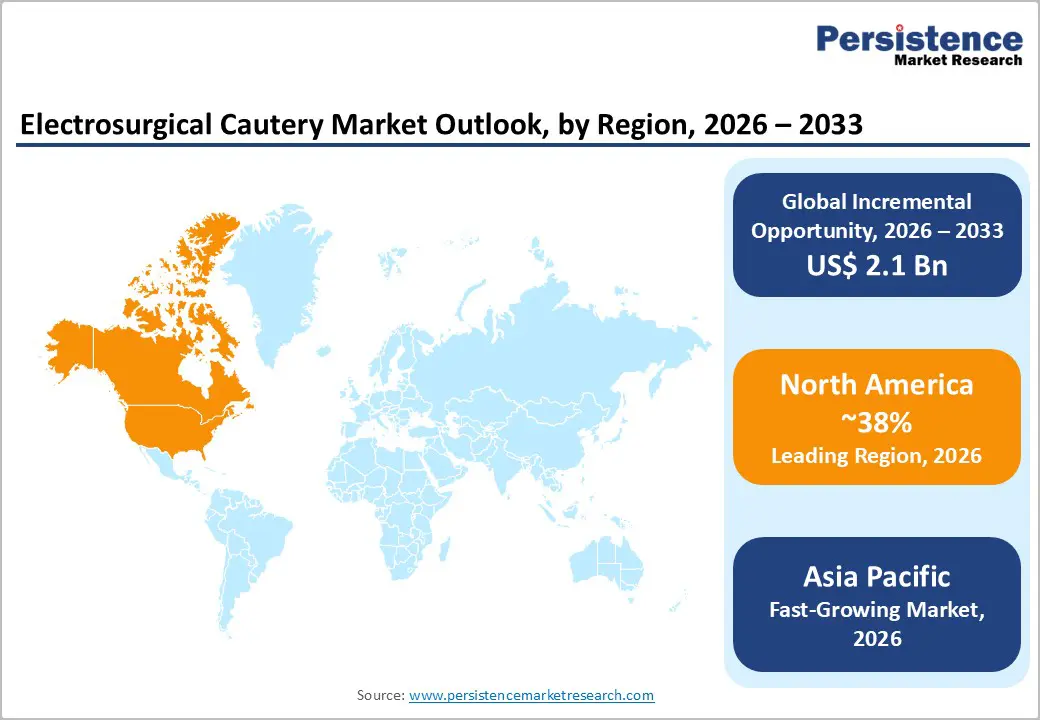

The global electrosurgical cautery market size is likely to be valued at US$3.6 billion in 2026, and is expected to reach US$5.7 billion by 2033, growing at a CAGR of 6.8% during the forecast period from 2026 to 2033, driven by the increasing prevalence of minimally invasive surgical procedures, rising geriatric population requiring surgical interventions, and growing adoption of advanced electrosurgical devices in hospitals and ambulatory surgical centers. Growing demand for precise, safe electrosurgical cautery instruments, especially bipolar and combination ESUs for general and gynecological surgery, is accelerating adoption across end-user settings.

Advances in vessel-sealing technology and smoke-evacuation integration are further boosting uptake by offering better hemostasis and reduced surgical smoke hazards. Increasing recognition of electrosurgical cautery as critical for efficient tissue cutting, coagulation, and reduced blood loss in high-volume surgical specialties remains a major driver of market growth.

Key Industry Highlights:

- Leading Region: North America, anticipated to account for a 38% market share in 2026, driven by high procedural volumes, advanced ASC infrastructure, and strong demand in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by a rapid increase in surgical procedures, expanding healthcare infrastructure, and rising adoption of minimally invasive techniques in China and India.

- Dominant Product Type: Bipolar, to hold approximately 48% of the market share, as it remains the preferred choice for precision and safety.

- Leading Application Type: General surgery is expected to dominate the market, contributing nearly 48% of revenue in 2026, due to its broad scope and high procedure volume across healthcare systems.

- In 2025, Surgeons at Rajasthan Hospital (RHL) in Jaipur, led by Dr. Ravindra Singh Rao, performed a minimally invasive electrosurgical valve-in-valve mitral procedure on a 74-year-old high-risk patient, implanting a new valve without open-heart surgery.

| Global Market Attributes | Key Insights |

|---|---|

| Electrosurgical Cautery Market Size (2026E) | US$3.6 Bn |

| Market Value Forecast (2033F) | US$5.7 Bn |

| Projected Growth CAGR (2026-2033) | 6.8% |

| Historical Market Growth (2020-2025) | 6.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Growth of Minimally Invasive Surgical Procedures and Geriatric Population

The rise in minimally invasive surgical (MIS) procedures, combined with the rapid growth of the geriatric population, is reshaping surgical care delivery worldwide. Minimally invasive techniques, such as laparoscopic, endoscopic, and catheter-based procedures, are increasingly preferred because they reduce tissue trauma, shorten hospital stays, and lower postoperative complication rates. These benefits are especially critical for elderly patients, who often present with multiple comorbidities and reduced physiological resilience. Smaller incisions and faster recovery times help minimize surgical stress, enabling quicker mobilization and lowering the risk of infections or prolonged hospitalization.

The global geriatric population is expanding due to increased life expectancy and improved management of chronic diseases. Older adults are more susceptible to conditions such as cardiovascular disorders, osteoarthritis, gastrointestinal diseases, and cancers, many of which require surgical intervention. Minimally invasive approaches allow surgeons to address these conditions more safely and efficiently, even in high-risk patients. Procedures that were once delayed or avoided in elderly individuals are now being performed with greater confidence.

Increasing Adoption of Advanced Vessel-Sealing and Smoke-Evacuation Systems

The increasing adoption of advanced vessel-sealing and smoke-evacuation systems reflects a broader shift toward enhancing surgical precision, safety, and efficiency. Vessel-sealing devices use energy (such as advanced radiofrequency or ultrasonic technology) to permanently fuse blood vessels and tissue bundles during surgery. This reduces intraoperative bleeding, lowers the need for sutures or clips, and shortens procedural time. For surgeons, reliable vessel sealing means clearer views of the operative field and reduced physiological stress on patients, which can translate into fewer complications, less postoperative pain, and faster recovery.

The use of energy-based surgical tools inevitably generates surgical smoke, a complex mixture of gases and particulates that can compromise visibility and pose health risks to operating room staff. Smoke-evacuation systems are designed to capture and filter this smoke at the source, improving air quality and maintaining a clearer surgical field. Improved visibility reduces procedural errors, supports more accurate tissue dissection, and enhances the overall workflow for surgical teams. The synergy of these technologies is reshaping modern operating rooms.

Barrier Analysis – High Cost of Advanced Electrosurgical Systems

The high cost of advanced electrosurgical systems represents a significant barrier to broader adoption and equitable access in healthcare settings. These systems, which include sophisticated energy-based devices capable of cutting, coagulating, and sealing tissue, combine precision engineering, advanced software, and safety features that drive up their manufacturing costs. For hospitals and surgical centers operating under tight budgetary constraints, the upfront price of acquiring this technology can be daunting, especially when balanced against other pressing needs such as staffing, facility upgrades, or essential imaging equipment.

Beyond the initial purchase price, ongoing expenses contribute to the overall financial burden. Many advanced electrosurgical platforms require proprietary accessories, maintenance agreements, and periodic software updates, all of which add recurring costs. Smaller hospitals and outpatient facilities may struggle to justify these investments when patient volumes or procedure complexity do not guarantee a swift return on investment. In resource-limited regions or public health systems with fixed funding, the challenge is even greater, potentially widening disparities in the quality of surgical care available to different populations.

Stringent Regulatory Approval and Reimbursement Challenges

Stringent regulatory approval and reimbursement challenges significantly influence the development and adoption of medical technologies. Advanced surgical devices and systems must undergo rigorous evaluation by regulatory authorities to ensure safety and effectiveness before they can be marketed. This process often involves extensive preclinical testing, clinical trials, and detailed documentation, a timeline that can span several years. For manufacturers, navigating complex regulatory frameworks across different regions adds layers of cost and uncertainty. Each jurisdiction may have its own standards, submission requirements, and review cycles, making global product launches resource-intensive and technically demanding.

Even after regulatory clearance, securing favorable reimbursement remains a separate hurdle. Healthcare payers, whether government programs or private insurers, must decide whether and how much they will cover for new devices and procedures. If reimbursement codes are unclear, inadequate, or absent, hospitals and providers may be reluctant to adopt innovations that patients must pay for out of pocket. This is especially true in markets where cost containment is a priority and where payers require robust evidence of long-term clinical and economic benefit before approving coverage.

Opportunity Analysis – Growing Surgical Procedure Volumes

Growing surgical procedure volumes are a key factor driving expansion across the global healthcare and medical device landscape. This growth is largely influenced by demographic shifts, particularly population growth and aging, along with a rising prevalence of chronic and lifestyle-related diseases. Conditions such as cardiovascular disorders, cancers, orthopedic problems, and gastrointestinal diseases increasingly require surgical intervention, leading to a steady rise in both elective and emergency procedures. Improved diagnostic capabilities are also enabling earlier detection of medical conditions, which often results in timely surgical treatment rather than prolonged medical management.

Advances in surgical techniques have further contributed to higher procedure volumes. Minimally invasive and day-care surgeries have reduced recovery times, shortened hospital stays, and lowered complication risks, making surgery a more acceptable option for patients and physicians alike. Procedures that were once deferred due to high risk or long recovery periods are now being performed more frequently. The expansion of ambulatory surgical centers has also played a major role by increasing capacity, improving operational efficiency, and reducing overall treatment costs.

Technological Innovation

Technological innovation is a central force shaping the evolution of modern electrosurgical and surgical device markets. Continuous advances in energy-delivery technologies have enabled greater precision, allowing surgeons to cut, coagulate, and seal tissue with improved control and consistency. Enhanced feedback mechanisms, such as real-time tissue sensing and adaptive power modulation, help optimize energy output based on tissue type, reducing unintended thermal damage and improving patient safety. These innovations support more predictable surgical outcomes and increase clinician confidence during complex procedures.

Innovation lies in system integration and usability. Newer platforms are designed with intuitive interfaces, ergonomic handpieces, and programmable settings that simplify operation and reduce the learning curve for surgical teams. Compact designs and modular components also make advanced systems easier to deploy across different operating rooms and care settings, including ambulatory surgical centers. The incorporation of built-in safety features such as automatic shutoff, insulation monitoring, and enhanced grounding technologies helps minimize procedural risks.

Category-wise Analysis

Product Type Insights

Bipolar is anticipated to dominate the market, accounting for approximately 48% of the market share in 2026. Its dominance is driven by strong safety and performance advantages. In bipolar systems, electrical energy is confined between two electrodes on the instrument tip, minimizing unintended current flow through the patient’s body. This localized energy delivery minimizes the risk of thermal injury and enhances precision, making bipolar devices ideal for delicate and minimally invasive procedures. Medtronic's HET™ bipolar system, used for precise tissue coagulation in general surgery such as treating symptomatic hemorrhoids, showcases the focused energy delivery and clinical effectiveness of bipolar devices.

Hybrid is likely to be the fastest-growing product type, due to combining the strengths of both monopolar and bipolar technologies in a single platform. This versatility allows surgeons to switch between energy modes during complex procedures without changing instruments, improving workflow efficiency, and reducing operative time. Hybrid systems also support a broader range of surgical applications, from open to minimally invasive techniques, making them attractive to hospitals seeking flexible solutions. Thunderbeat™ system from Olympus Corporation, Thunderbeat™ combines bipolar energy for effective vessel sealing with ultrasonic energy for rapid cutting, allowing surgeons to perform both functions with one instrument rather than switching between tools. This hybrid approach enhances procedural efficiency and precision, particularly in minimally invasive procedures such as laparoscopic colorectal or gynecologic surgeries.

Application Insights

General surgery is expected to dominate the market, contributing nearly 48% of revenue in 2026, due to its broad scope and high procedure volume across healthcare systems. General surgeons routinely perform a wide range of procedures, including gastrointestinal, colorectal, hernia, and abdominal surgeries, all of which heavily rely on electrosurgical technologies for cutting and hemostasis. The growing preference for minimally invasive techniques in general surgery further increases the use of advanced energy-based devices. Medtronic’s Aquamantys™ System and PlasmaBlade™ are actively used in general surgical procedures such as laparoscopic cholecystectomy, hernia repair, and soft tissue dissection. These electrosurgical instruments provide precise cutting and hemostatic sealing, helping surgeons manage bleeding and tissue dissection efficiently during high-volume general surgeries.

Gynecological surgery represents the fastest-growing application, driven by the increasing incorporation of advanced energy devices to improve precision, reduce blood loss, and shorten recovery times. Procedures such as hysterectomies, myomectomies, endometriosis treatment, and laparoscopic pelvic surgeries benefit from electrosurgical tools that enable efficient cutting and controlled hemostasis in delicate anatomical regions. The shift toward minimally invasive gynecologic techniques has accelerated this trend, with surgeons preferring energy devices that support both dissection and vessel sealing. Medtronic’s Valleylab™ electrosurgical platforms, which power advanced bipolar and vessel-sealing instruments used in procedures such as laparoscopic hysterectomy and myomectomy. These devices are designed to provide reliable cutting and hemostasis in delicate gynecologic tissues, helping reduce blood loss and operative time. Surgeons frequently use Valleylab-driven tools in minimally invasive gynecologic procedures due to their precision and safety features, supporting growing adoption in this application area.

Regional Insights

North America Respiratory Anesthesia Consumables Market Trends

North America is projected to dominate, accounting for nearly 38% of the share in 2026, driven by the region’s high surgical volumes, advanced ASC penetration, and high public awareness of precision surgery benefits. Distribution systems in the U.S. and Canada provide extensive support for electrosurgical cautery programs, ensuring wide accessibility across bipolar, general surgery, and hospital populations. Increasing demand for advanced, convenient, and easy-to-use forms is further accelerating adoption, as these formats improve hemostasis and reduce barriers associated with traditional cautery.

Innovation in electrosurgical cautery technology, including stable hybrid, improved vessel-sealing delivery, and targeted ASC enhancement, is attracting significant investment from both public and private sectors. Government initiatives and CMS campaigns continue to promote use against blood-loss risks, procedural efficiency concerns, and emerging outpatient threats, creating sustained market demand. The growing focus on gynecological grades and specialty uses, particularly for general surgery and others, is expanding the target applications for electrosurgical cautery.

Europe Electrosurgical Cautery Market Trends

Europe is supported by increasing awareness of precision surgery benefits, strong regulatory systems, and government-led minimally invasive surgery programs. Countries such as Germany, France, the U.K., and Spain have well-established healthcare frameworks that support routine electrosurgical cautery use and encourage adoption of innovative energy delivery methods, including bipolar and hybrid platforms. These high-precision formulations are particularly appealing for general surgery populations, regulation-conscious hospitals, and ASC users, improving outcomes and coverage rates.

Technological advancements in electrosurgical cautery development, such as enhanced vessel-sealing, application-targeted delivery, and improved combination ESU grades, are further boosting market potential. European authorities are increasingly supporting research and trials for cautery against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, low-blood-loss options is aligned with the region’s focus on preventive complication reduction and day-surgery expansion. Public awareness campaigns and promotion drives are expanding reach in both hospital and ASC segments, while suppliers are investing in production and novel variants to increase efficacy.

Asia Pacific Electrosurgical Cautery Market Trends

Asia Pacific is likely to be the fastest-growing market for electrosurgical cautery in 2026, driven by rising surgical awareness, increasing government initiatives, and expanding application programs across the region. Countries such as China, India, Japan, and South Korea are actively promoting cautery campaigns to address surgical growth and emerging precision needs. Electrosurgical cautery is particularly attractive in these regions due to its scalable administration, ease of adoption, and suitability for large-scale hospital and ASC drives in both urban and rural populations.

Technological advancements are supporting the development of stable, effective, and easy-to-deploy electrosurgical cautery, which can withstand challenging OR conditions and minimize blood-loss dependence. These innovations are critical for reaching domestic hospitals and improving overall surgical coverage. Growing demand for bipolar, general surgery, and hospital applications is contributing to market expansion. Public-private partnerships, increased healthcare expenditure, and rising investment in cautery research and production capacity are further accelerating growth. The convenience of cautery delivery, combined with improved precision and reduced risk of complications, positions it as a preferred choice.

Competitive Landscape

The global electrosurgical cautery market features competition between established medical device leaders and emerging energy-specialists. In North America and Europe, Medtronic and Olympus Corporation lead through strong R&D, distribution networks, and hospital ties, bolstered by innovative bipolar and vessel-sealing programs. In Asia Pacific, local players advance with cost-competitive solutions, enhancing accessibility. Bipolar delivery boosts precision, cuts thermal risks, and enables mass integrations across ORs. Strategic partnerships, collaborations, and acquisitions merge expertise, expand portfolios, and speed commercialization. Hybrid formulations solve versatility issues, aiding penetration in complex procedures.

Key Industry Developments:

- In October 2025, Medtronic, a leading medical device company, announced the launch of two advanced electrosurgical devices in India: the Valleylab FT10 Electrosurgical Generator (VLFT10FXGEN) and the Valleylab FT10 Vessel Sealing Generator (VLFT10LSGEN). These new systems are equipped with TissueFect sensing technology, which automatically adjusts the energy delivered based on the type of tissue being treated.

- In March 2025, Johnson & Johnson MedTech, a global leader in surgical technologies, introduced the DUALTO™ Energy System. This integrated surgical platform combines multiple energy modalities for use in both open and minimally invasive surgeries. It is designed to work alongside Service Solutions for device uptime and can be paired with the Polyphonic™ Fleet software application for efficient device management. Additionally, DUALTO™ is built for future compatibility with the company's OTTAVA™ Robotic Surgical System.

Companies Covered in Electrosurgical Cautery Market

- Medtronic

- Boston Scientific Corporation

- Olympus Corporation

- B.Bran Melsungen

- Bovie Medical Corporation

- KLS Martin

- Symmetry Surgical

- Conmed Corporation

- Ebre Elektromedizin GmbH

Frequently Asked Questions

The global electrosurgical cautery market is projected to reach US$3.6 billion in 2026.

Advancements in electrosurgical technologies enable greater precision, controlled energy delivery, and safer outcomes across a wide range of surgical applications.

The electrosurgical cautery market is poised to witness a CAGR of 6.8% from 2026 to 2033.

Adoption of advanced and hybrid energy devices, offering manufacturers opportunities to differentiate through multifunctionality, improved safety, and workflow efficiency.

Medtronic, Olympus Corporation, B.Braun Melsungen, Conmed Corporation, and Erbe Elektromedizin GmbH are the key players.