- Executive Summary

- Global Diamond Core Drilling in Construction Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026 - 2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply-Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Construction Industry Overview

- Global Electrical Industry Overview

- Forecast Factors - Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 - 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Diamond Core Drilling in Construction Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Global Diamond Core Drilling in Construction Market Outlook: Operational Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Operational Type, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Operational Type, 2026-2033

- Hand Held

- Rig Operated

- Market Attractiveness Analysis: Operational Type

- Global Diamond Core Drilling in Construction Market Outlook: Drilling Technique

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Drilling Technique, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Drilling Technique, 2026-2033

- Stitch Drilling

- Underwater Diamond Drilling

- Surface Drilling

- Underground Drilling

- Market Attractiveness Analysis: Drilling Technique

- Global Diamond Core Drilling in Construction Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Diamond Core Drilling in Construction Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Operational Type, 2026-2033

- Hand Held

- Rig Operated

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Drilling Technique, 2026-2033

- Stitch Drilling

- Underwater Diamond Drilling

- Surface Drilling

- Underground Drilling

- Europe Diamond Core Drilling in Construction Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Operational Type, 2026-2033

- Hand Held

- Rig Operated

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Drilling Technique, 2026-2033

- Stitch Drilling

- Underwater Diamond Drilling

- Surface Drilling

- Underground Drilling

- East Asia Diamond Core Drilling in Construction Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Operational Type, 2026-2033

- Hand Held

- Rig Operated

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Drilling Technique, 2026-2033

- Stitch Drilling

- Underwater Diamond Drilling

- Surface Drilling

- Underground Drilling

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by , 2026-2033

- South Asia & Oceania Diamond Core Drilling in Construction Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Operational Type, 2026-2033

- Hand Held

- Rig Operated

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Drilling Technique, 2026-2033

- Stitch Drilling

- Underwater Diamond Drilling

- Surface Drilling

- Underground Drilling

- Latin America Diamond Core Drilling in Construction Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Operational Type, 2026-2033

- Hand Held

- Rig Operated

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Drilling Technique, 2026-2033

- Stitch Drilling

- Underwater Diamond Drilling

- Surface Drilling

- Underground Drilling

- Middle East & Africa Diamond Core Drilling in Construction Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Operational Type, 2026-2033

- Hand Held

- Rig Operated

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Drilling Technique, 2026-2033

- Stitch Drilling

- Underwater Diamond Drilling

- Surface Drilling

- Underground Drilling

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Albert Roller GmbH

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- APC Drilling & Constructions Pvt Ltd

- Atlas Copco AB

- Bauer AG

- Boart Longyear Ltd.

- Controls S.p.A.

- DUSS Maschinenfabrik GmbH & Co. KG

- Eibenstock Elektrowerkzeuge GmbH

- Epiroc AB

- Geomachine Oy

- Albert Roller GmbH

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Off-Road Equipment & Machinery

- Diamond Core Drilling in Construction Market

Diamond Core Drilling in Construction Market Size, Share, and Growth Forecast 2026 - 2033

Diamond Core Drilling in Construction Market by Operational Type (Handheld and Rig Operated), by Drilling Technique (Stitch Drilling, Underwater Diamond Drilling, Surface Drilling and Underground Drilling and Regional Analysis for 2026 - 2033

Key Industry Highlights:

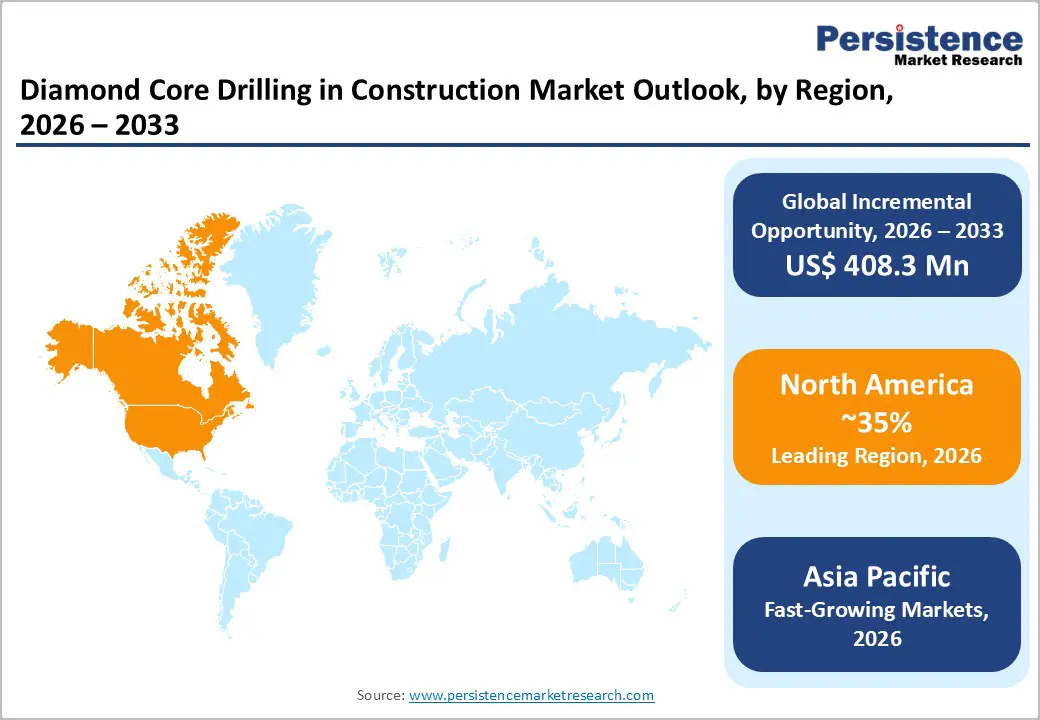

- Leading Region: North America dominates with 34% global market share United States infrastructure investment leadership reaches US$110 billion annually, bridge rehabilitation programs targeting 45,000 deficient bridges, and private commercial construction investment in high-rise development drive North American market dominance.

- Fastest-Growing: Asia Pacific is the fastest-growing region at 8.3% CAGR, the Chinese Belt and Road Initiative spanning 140+ countries, the Indian Prime Minister Gati Shakti infrastructure plan allocating US$ 1.3 trillion, and Southeast Asian urbanization acceleration establish Asia Pacific as the highest-expansion opportunity.

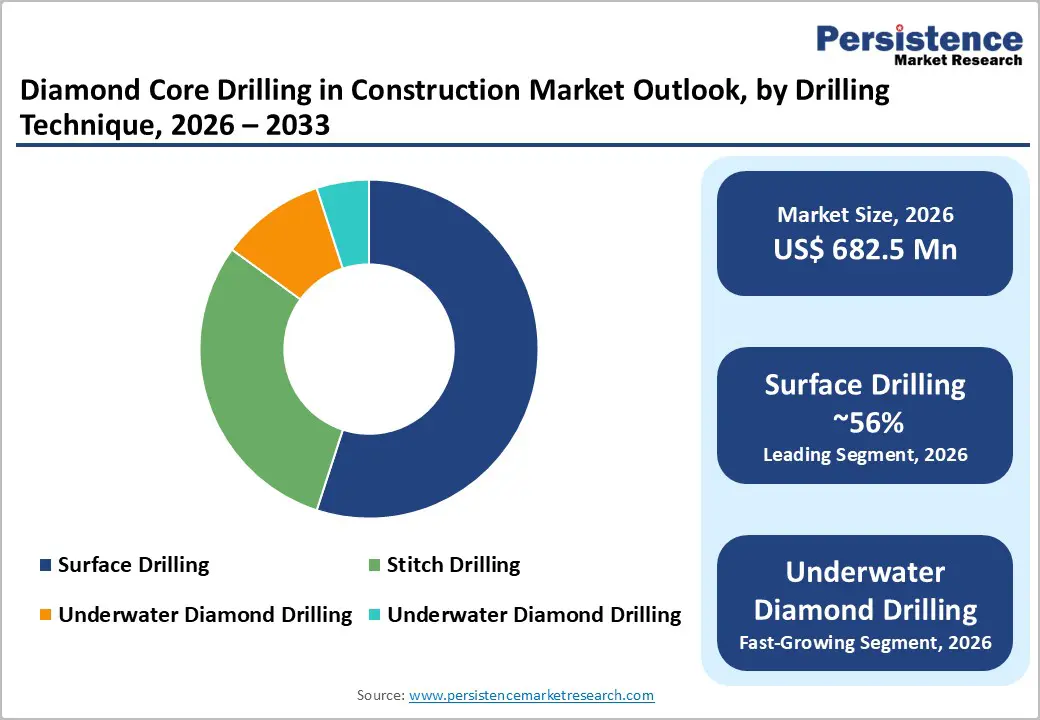

- Leading Segment: Rig-Operated systems dominate with 62% market share. Superior depth capability exceeding 500 meters, throughput rates supporting 50+ meters daily production, and robust infrastructure project performance maintain rig-mounted equipment dominance in construction drilling.

- Fastest-growing segment: Surface Drilling, with 7.8% annual growth. Residential construction expansion, utility installation prevalence, and foundation drilling applications drive surface drilling segment expansion across accessible job site applications.

- Opportunity: Automation and IoT Integration represent a major market opportunity. Smart controls enabling real-time monitoring, predictive maintenance optimization, and remote equipment operation drive emerging technology differentiation supporting competitive positioning.

| Key Insights | Details |

|---|---|

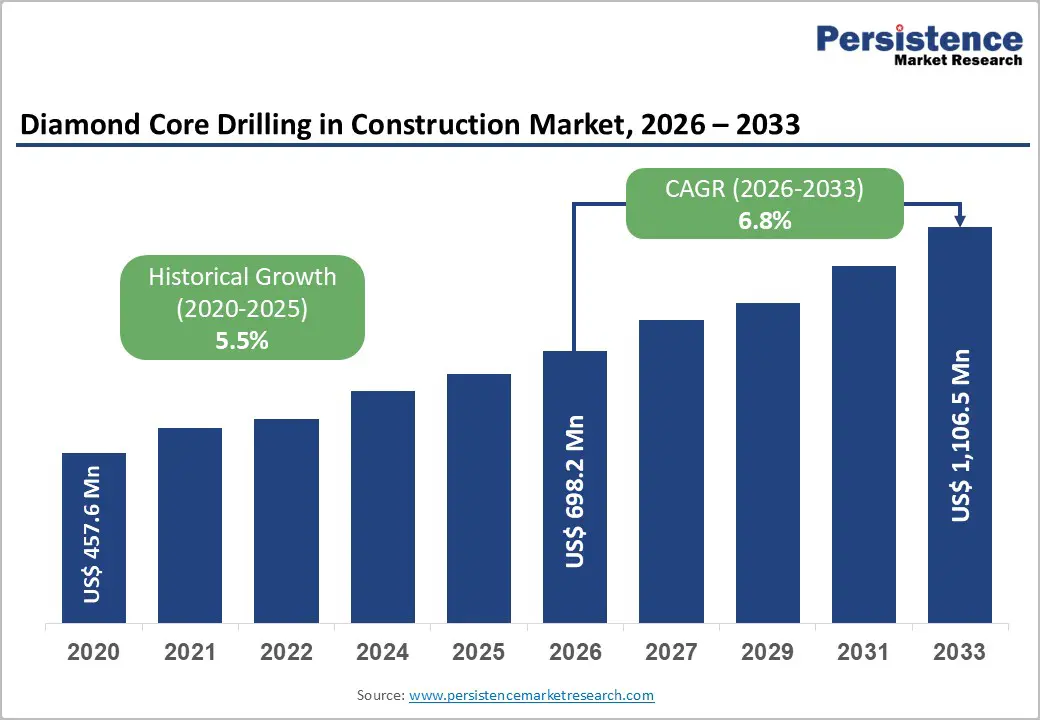

| Diamond Core Drilling in Construction Market Size (2026E) | US$ 698.2 Mn |

| Market Value Forecast (2033F) | US$ 1,106.6 Mn |

| Projected Growth (CAGR 2026 to 2033) | 6.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.5% |

Market Dynamics

Drivers - Accelerating Global Infrastructure Investment and Urban Development Projects

Sustained global infrastructure expansion and massive urban development initiatives are driving unprecedented demand for precision diamond core-drilling equipment capable of meeting complex construction requirements with minimal structural disruption. Global construction spending expanded at a 3.8% annual rate through 2024, reaching approximately US$17.2 trillion, with particular emphasis on infrastructure modernization, bridge replacement, tunnel development, and high-rise urban towers.

World Bank infrastructure financing reached US$440 billion in 2024, supporting road expansion, bridge modernization, railway development, and water management systems that require sophisticated diamond core-drilling capabilities. Urbanization acceleration across the Asia Pacific, Latin America, and the Middle East regions drives residential and commercial construction demand, with emerging markets adding approximately 1.8 billion urban residents through 2033, requiring expanded housing, commercial, and utility infrastructure.

Growing Emphasis on Green Building Standards and Non-Destructive Construction Methods

Rise in environmental sustainability requirements and green building certification mandates are establishing structural demand for low-vibration, low-dust drilling methods, preserving structural integrity while supporting Leadership in Energy and Environmental Design (LEED) and BREEAM compliance objectives. Green building construction expanded from 15% global market share in 2019 to 34% in 2024, with projections approaching 55% penetration by 2033, substantially amplifying demand for environmentally sensitive drilling technologies.

Occupational Safety and Health Administration (OSHA) regulations and International Organization for Standardization (ISO) standards impose stringent dust-suppression and vibration-control requirements during construction activities, particularly in occupied structures, where diamond core drilling is required to maintain operational viability that is unachievable with percussive alternatives. Wet core drilling expansion delivers superior dust suppression through water-cooled systems, enabling operations in environmentally sensitive areas and in occupied buildings with strict air quality requirements.

Restraints - High Capital Equipment Costs and Maintenance Complexity for Specialized Drilling Systems

Substantial capital investment requirements for advanced diamond core drilling equipment, specialized maintenance expertise demands, and limited equipment utilization across diverse project types create significant barriers constraining market expansion, particularly among small and medium-sized construction enterprises. Entry-level rig-mounted diamond core drilling systems require US$ 150,000-500,000 capital investment, with high-end automated platforms exceeding US$ 1.2 million, substantially limiting adoption among independent contractors and regional construction firms.

Handheld diamond core drills requiring US$ 5,000-25,000 investment demonstrate broader accessibility yet still represent meaningful capital barriers for small construction operations constrained by project-based revenue variability. Maintenance and calibration requirements for diamond drilling systems necessitate specialized technical expertise, calibrated equipment, and the availability of replacement components, creating operational complexity and unexpected cost escalations that undermine the accuracy of financial planning.

Material Supply Constraints and Volatility in Synthetic Diamond Element Supply

Supply chain vulnerabilities affecting synthetic diamond element availability and price volatility in specialized diamond powder and polycrystalline diamond (PCD) materials create cost unpredictability and equipment procurement delays substantially constraining market growth. Synthetic diamond production concentrated among limited global suppliers including De Beers Element Six, IIa Technologies, Henan Yuda Superhard Materials, and China-based producers creates supply concentration risk and limited competitive dynamics. Diamond powder market price escalation reflecting raw material constraints, energy price increases, and geopolitical supply disruptions elevates drilling equipment manufacturing costs by 8-12% annually, creating margin pressure and procurement hesitation among cost-sensitive customers. Lead times for specialized PCD cutting elements expanding to 16-24 weeks during supply constraints create project scheduling complications and inventory management challenges.

Opportunities - Integration of Automation and IoT Technologies in Precision Drilling Systems

Emerging automation technologies and Internet of Things (IoT) sensor integration, enabling real-time drilling condition monitoring, predictive maintenance optimization, and remote equipment management, represent transformative market opportunities for technology innovators. AI-driven drilling optimization platforms that analyze real-time sensor data automatically adjust torque, rotation speed, and penetration rate, improving drilling efficiency by 25-35% and extending diamond tool life through optimized operating parameters.

Smart controls integration, enabling remote equipment operation, automated core barrel changing, and depth tracking capabilities, reduces operator fatigue, enhances safety, and supports 24/7 operational scheduling on large infrastructure projects. Robotic drill stabilizers and automated core barrel changers deployed by Sino Gold Exploration and MECL (Mineral Exploration Corporation Limited) exemplify the adoption of emerging automation, with a 48% reduction in drilling time and improved core integrity, supporting expanded commercial viability.

Expansion of Directional Core Drilling and Complex Underground Excavation Applications

Accelerating the adoption of directional core-drilling technologies, which enable precise angled penetrations and complex underground tunnel development, represents a significant growth opportunity for equipment manufacturers and service providers. Underground infrastructure expansion, including subway systems, underground parking structures, geothermal heating systems, and utility tunnels, expanding at 7.2% annual rates across Asia Pacific, Europe, and North America, creates specialized demand for directional drilling capabilities. Master Drilling and Element Six's partnership in the development of synthetic-diamond-enabled tunnelling solutions achieved a 17% reduction in waste rock generation and substantially improved excavation speed, establishing technological differentiation and attracting premium customer valuations. Directional core drilling, enabling precise penetration control through complex geological formations, supports geotechnical exploration, foundation design validation, and subsurface resource assessment.

Category-wise Analysis

Operational Type Insights

Rig-Operated drilling systems maintain market dominance with approximately 62% market share, reflecting superior performance in large-scale infrastructure projects, deep drilling requirements, and continuous operational environments. Rig-mounted diamond core drilling platforms deliver exceptional depth capability exceeding 500 meters, throughput rates supporting 50+ meters of daily production on favorable geological formations, and robust architectures that withstand demanding job-site environments.

Rig-operated systems dominate infrastructure construction, bridge and tunnel development, utility installation, and large-scale commercial projects where project scope, drilling depth, and operational intensity justify substantial capital equipment investment. Handheld diamond core drills represent approximately 38% market share, expanding at an accelerating 7.4% annual growth rate driven by miniaturization, battery technology advancement, and application expansion in residential, small commercial, and retrofit project segments.

Drilling Technique Analysis

Surface drilling commands market dominance with approximately 56% market share, encompassing applications on accessible ground-level construction sites supporting foundation drilling, utility installation, and horizontal boring operations. Surface drilling versatility enables deployment across residential construction, commercial development, and infrastructure projects where ground accessibility and site conditions support standard drilling protocols. Stitch Drilling accounts for approximately 19% of the market, used in concrete cutting to create access openings through load-bearing walls, create elevator shafts, and perform structural modifications requiring precise hole placement without compromising the structure. Stitch drilling methodology enables controlled penetration through reinforced concrete by using sequential, precisely positioned holes, facilitating core removal and structural modification while maintaining surrounding structural integrity. Underground Drilling accounts for approximately 16% market share, expanding at an accelerating 8.1% annual growth rate driven by tunnel development, subway construction, geothermal system development, and underground utility installations.

Regional Insights

North America Diamond Core Drilling in Construction Market Trends

North America maintains established market leadership with approximately 34% global market share, anchored by the United States infrastructure investment leadership and technology innovation concentration. U.S. Department of Transportation infrastructure investment allocation of US$110 billion annually through 2033 drives sustained demand for precision drilling to support road reconstruction, bridge replacement, and tunnel modernization. Federal Highway Administration (FHWA) bridge rehabilitation programs targeting 45,000 deficient bridges require extensive diamond core drilling for structural assessment, core sampling, and foundation evaluation supporting maintenance decision-making.

The adoption of green building standards, including LEED certification, across commercial construction drives demand for non-vibration drilling methods, thereby preserving structural integrity and supporting occupancy compliance during active building use. Private construction investment in high-rise urban development, particularly in New York, Los Angeles, Chicago, and San Francisco, drives premium demand for advanced diamond core drilling equipment, enabling complex utility integration and precision opening creation.

Europe Diamond Core Drilling in Construction Market Trends

Europe represents approximately 25% global market share, characterized by stringent construction standards, aging infrastructure renovation emphasis, and advanced equipment technology adoption. European Union Cohesion Funds allocations exceeding US$ 380 billion support infrastructure modernization across Central European, Eastern European, and Mediterranean member states, thereby driving sustained procurement of drilling equipment. The German construction industry, emphasizing precision engineering and advanced methodologies, drives demand for sophisticated diamond core-drilling systems, with Eibenstock Elektrowerkzeuge GmbH and regional manufacturers establishing market leadership through technological innovation. United Kingdom post-Brexit infrastructure modernization and Midlands metropolitan development programs drive demand for advanced drilling capabilities supporting transportation infrastructure modernization. France, Spain, and Scandinavian nations, emphasizing sustainable construction and green building standards, are accelerating the adoption of non-destructive drilling methods, thereby supporting environmental compliance objectives.

Asia Pacific Diamond Core Drilling in Construction Market Trends

Asia-Pacific emerges as the fastest-growing region, with approximately 28% market share, expanding at an accelerating 8.3% annual growth rate, driven by extraordinary construction activity and accelerated infrastructure development. China dominates the regional market with 36% share, driven by the Belt and Road Initiative infrastructure development spanning 140+ countries, high-speed rail expansion totaling 40,000+ kilometers, and urban development accommodating 400+ million urban residents through 2033. Indian construction sector expansion at 9.2% annual growth rates, supported by Prime Minister Gati Shakti National Master Plan infrastructure investment totaling US$ 1.3 trillion, drives sustained equipment procurement for highway modernization, railway expansion, and urban development. Japan's infrastructure modernization programs, which emphasize earthquake-resistant construction and tsunami defense systems, drive demand for precision drilling to support structural assessment and seismic reinforcement.

Competitive Landscape

The diamond core drilling in construction market exhibits moderate consolidation among global tier-one manufacturers Atlas Copco AB, Epiroc AB, Hilti Corporation, Husqvarna, and Boart Longyear collectively commanding approximately 48% aggregated market share through comprehensive product portfolios, extensive distribution networks, and established relationships with major construction contractors. Market leaders pursue expansion through strategic acquisition of regional manufacturers, integration of automation and IoT technologies into equipment platforms, and research partnerships with construction technology innovators.

Regional manufacturer competition remains intense, with Chinese, Indian, and Southeast Asian manufacturers capturing 35% market share through cost-competitive offerings and application-specific product development. German manufacturers including Albert Roller GmbH, Eibenstock, and DUSS Maschinenfabrik maintain competitive positioning through precision engineering excellence and specialized industrial applications.

Key Market Developments

- In August 2025, Master Drilling and Element Six Complete Synthetic Diamond Tunnelling Solution Deployment Supporting 17% Waste Reduction Master Drilling and Element Six partnership deployment achieved exceptional 17% waste rock reduction and substantially improved excavation speed through synthetic diamond-enabled cutting tool integration, establishing technology differentiation attracting premium customer valuations for underground infrastructure projects.

- In November 2024, Hilti Launches Battery-Powered Core Drilling Line for Commercial Construction Applications Hilti Corporation introduced revolutionary battery-powered core drilling systems delivering corded-equivalent power with cordless operation convenience, substantially enhancing job site flexibility and operator mobility across commercial construction projects, exemplifying emerging equipment innovation trends.

Companies Covered in Diamond Core Drilling in Construction Market

- Albert Roller GmbH

- APC Drilling & Constructions Pvt Ltd

- Atlas Copco AB

- Bauer AG

- Boart Longyear Ltd.

- Controls S.p.A.

- DUSS Maschinenfabrik GmbH & Co. KG

- Eibenstock Elektrowerkzeuge GmbH

- Epiroc AB

- Geomachine Oy

- Other Key Players

Frequently Asked Questions

The global Diamond Core Drilling in Construction market was valued at US$ 698.2 million in 2026 and is projected to reach US$ 1,106.6 million by 2033, expanding at a 6.8% CAGR.

Primary growth drivers include accelerating global infrastructure investment totaling US$ 17.2 trillion in 2024, World Bank infrastructure financing reaching US$ 440 billion annually, expanding green building standards with LEED certification adoption at 34% market penetration and growing to 55% by 2033, and increasing emphasis on non-destructive construction methods preserving structural integrity during urban development.

Rig-Operated drilling systems dominate with approximately 62% market share, reflecting superior performance in large-scale infrastructure projects, deep drilling requirements exceeding 500 meters, and continuous operational environments supporting 50+ meters daily production.

North America maintains market leadership with approximately 34% global market share anchored by United States infrastructure investment leadership at US$ 110 billion annually.

Market leaders include Atlas Copco AB, Epiroc AB, Hilti Corporation, Husqvarna, Eibenstock and Elektrowerkzeuge GmbH.