- Medical Devices

- Dental Infection Prevention Market

Dental Infection Prevention Market Size, Share, and Growth Forecast 2026 - 2033

Dental Infection Prevention Market by Product Type (Disinfectants & Cleaning Solutions, Sterilization Products, Personal Protective Equipment (PPE), Cleaning & Sterilization Equipment, Others), Application (Preventive Dentistry, Oral Surgery, Periodontal Treatment, Restorative Dentistry, Others), End-user (Dental Clinics, Hospitals, Dental Laboratories, Academic & Research Institutes, Others), Regional Analysis, 2026 - 2033

Dental Infection Prevention Market Share and Trends Analysis

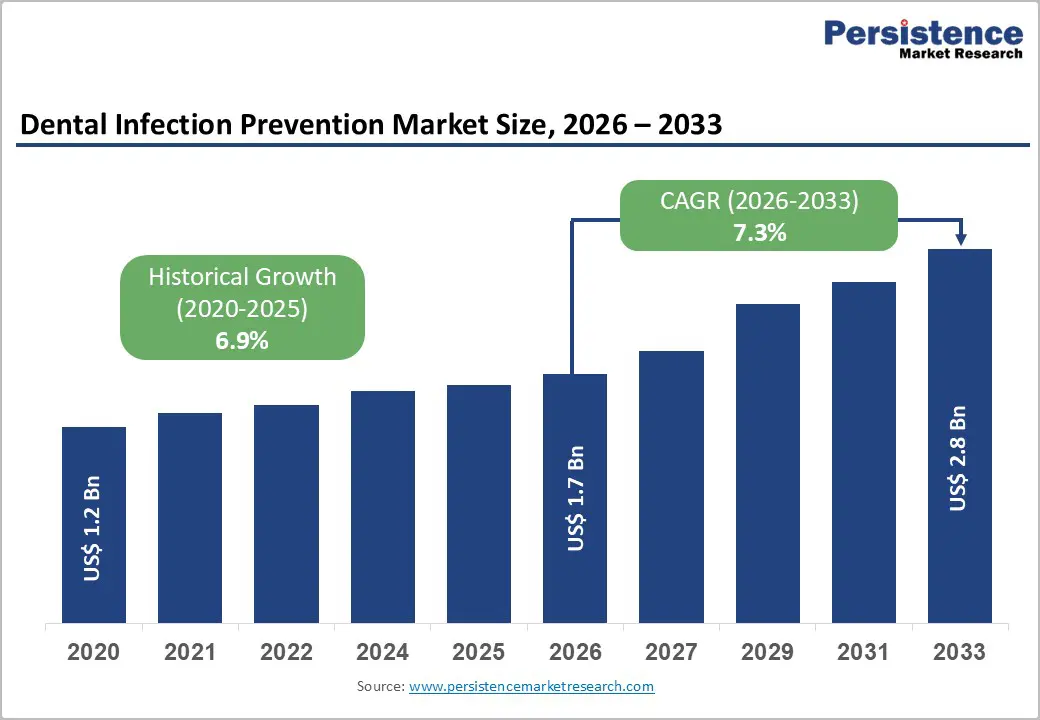

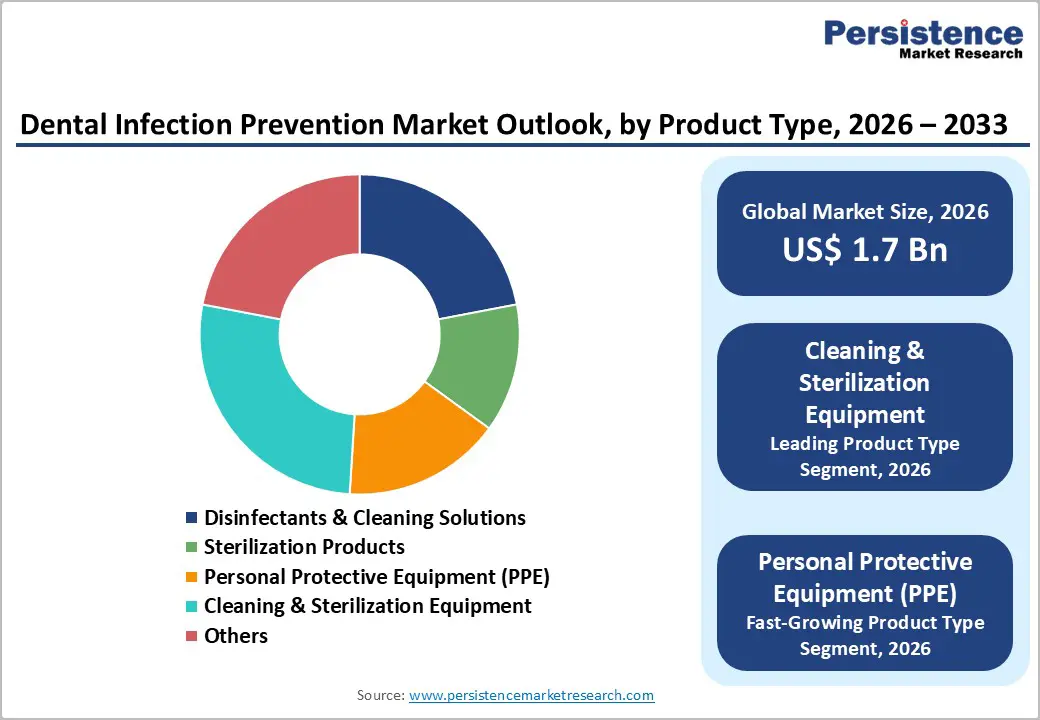

The global dental infection prevention market size is expected to be valued at US$ 1.7 billion in 2026 and projected to reach US$ 2.8 billion by 2033, growing at a CAGR of 7.3% between 2026 and 2033. The rising global burden of oral diseases, with nearly 3.5 billion people affected by caries and periodontal disease, is driving sustained investments in dental infection control solutions across care settings.

Strong regulatory emphasis from bodies such as the CDC and WHO on infection prevention in dental practices, including robust instrument sterilization workflows and disinfection protocols, further accelerates adoption of cleaning & sterilization equipment, PPE, and high-level disinfectants. Additionally, growing awareness of bloodborne infection risks among dental healthcare workers, especially related to HBV, HCV, and HIV, is encouraging clinics and hospitals to upgrade sterilization infrastructure and staff training, reinforcing long-term market expansion.

Key Market Highlights

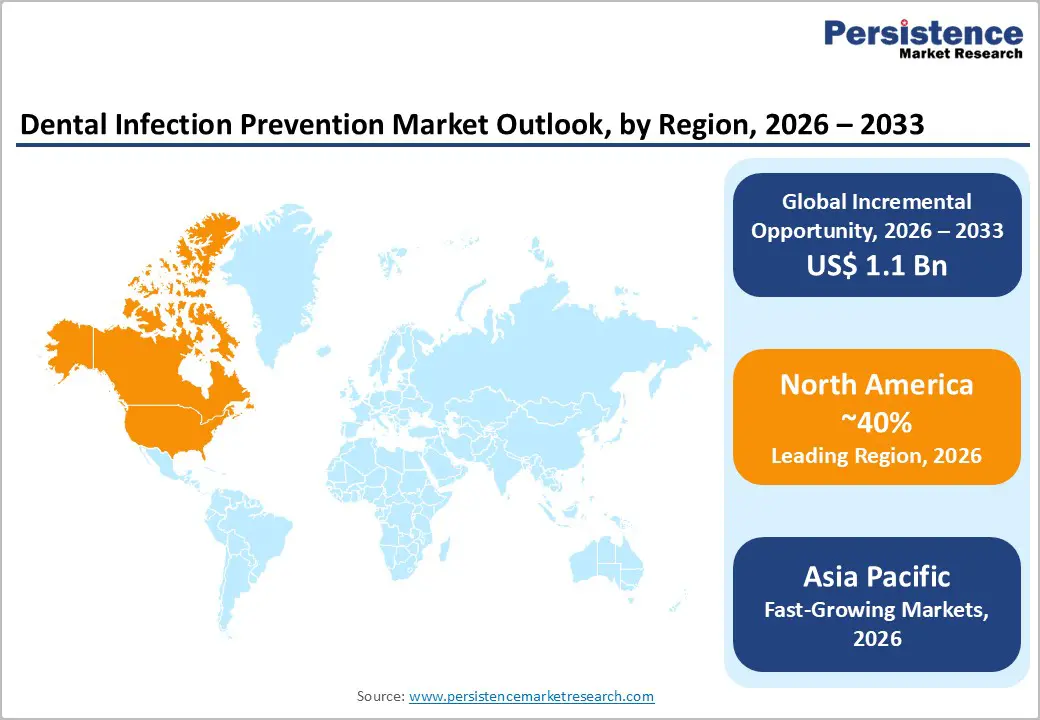

- North America remains the leading region in the dental infection prevention market, supported by 40% share in 2025, strong regulatory enforcement, high dental care utilization, and widespread adoption of advanced sterilization and disinfection technologies in clinics and hospitals.

- Asia-Pacific is the fastest-growing regional market, driven by expanding dental infrastructure in China, India, Japan, and ASEAN, rising oral health awareness, and competitive manufacturing capabilities that accelerate the adoption of infection-prevention products across care settings.

- Cleaning & sterilization equipment is the dominant product segment, contributing about 27% of global market value in 2025, as validated autoclaves, washer-disinfectors, and monitoring systems form the backbone of safe instrument reprocessing in dental practices.

- Personal protective equipment (PPE) is the fastest-growing product category, buoyed by post-pandemic norms around respirators, face shields, and protective gowns and by heightened focus on occupational safety for dental professionals exposed to bloodborne and aerosol-borne pathogens.

- A key market opportunity lies in integrated, high-throughput sterilization and digital monitoring solutions for DSOs and multi-chair clinics, enabling standardized infection control, efficient workflows, regulatory compliance, and long-term vendor partnerships across diversified dental networks.

| Key Insights | Details |

|---|---|

|

Dental Infection Prevention Market Size (2026E) |

US$ 1.7 billion |

|

Market Value Forecast (2033F) |

US$ 2.8 billion |

|

Projected Growth CAGR (2026–2033) |

7.3% |

|

Historical Market Growth (2020–2025) |

6.9% |

Market Dynamics

Drivers - Rise in Global Oral Disease Burden and Procedure Intensity

A key growth driver for the dental infection prevention market is the rising prevalence of dental caries and periodontal disease, which affects almost 50% of the world’s population, or about 3.5 billion people, according to the WHO Global Oral Health Status Report 2022. As more patients require restorative, periodontal, and oral surgical procedures, the volume of invasive dental interventions increases, raising the risk of cross-contamination and driving demand for high-performance sterilization products, disinfectants, and barrier PPE. Evidence from global burden of disease analyses indicates that oral disorders accounted for approximately 3.74 billion incident cases between 1990 and 2021, with caries of permanent teeth affecting 2.24 billion individuals, underscoring the need for robust infection prevention protocols at every stage of care. This intensifying clinical load compels dental clinics, hospitals, and laboratories to modernize their infection control workflows, from automated cleaning systems to validated autoclaves and monitoring indicators, positively impacting market growth.

Heightened focus on occupational safety and regulatory compliance

Another strong driver is the increased focus on protecting dental health-care personnel from bloodborne and aerosol-borne infections under stringent regulatory frameworks. Research indicates that dental professionals face an elevated risk of exposure to HBV, HCV, and HIV due to frequent use of sharp instruments and contact with blood and saliva during procedures, especially in oral surgery and periodontal interventions. Regulatory agencies and professional organizations, including the CDC, mandate comprehensive infection prevention strategies such as standard precautions, PPE, vaccination, and validated sterilization of heat-stable and heat-sensitive instruments. These requirements create consistent demand for sterilization products, PPE kits, and monitoring systems, while regular inspections and accreditation processes push practices to invest in state-of-the-art cleaning and sterilization equipment to maintain compliance and minimize occupational risk.

Restraints - High capital and operating costs for advanced sterilization infrastructure

A major restraint for the dental infection prevention market is the relatively high capital cost associated with purchasing advanced cleaning and sterilization equipment, including benchtop and large-capacity autoclaves, washer-disinfectors, and automated tracking systems. Small and solo dental practices, especially in low and middle-income regions, may struggle to justify investments in redundant sterilization lines, biological indicators, and high-level disinfectants when reimbursement levels are constrained, and patient volumes fluctuate. Additionally, ongoing operating expenses for consumables, maintenance, validation, and staff training increase the total cost of ownership, which can slow replacement cycles and limit the adoption of premium systems, particularly outside urban centers.

Compliance gaps and inadequate training in emerging markets

Another restraint is the persistent gap between recommended infection prevention guidelines and actual practice, especially in resource-constrained settings. Reports from various health authorities show that despite availability of CDC and national infection control standards, some dental facilities still exhibit inconsistent sterilization documentation, improper instrument reprocessing, or inadequate use of PPE, undermining patient and staff safety. Limited access to structured continuing education, language barriers in guideline dissemination, and competing operational priorities can delay the adoption of best practices, thereby dampening near-term demand for advanced infection prevention products that rely on trained personnel and standardized workflows.

Opportunity - Expansion of high-throughput cleaning & sterilization equipment in group practices and DSOs

One of the most attractive opportunities lies in expanding the use of high-throughput cleaning and sterilization equipment in large group practices and dental service organizations (DSOs), particularly in North America and Europe. As multi-chair clinics and corporate dental networks consolidate patient volumes, they require centralized instrument reprocessing facilities capable of handling high daily loads while ensuring full compliance with CDC and OSHA-aligned protocols, including mechanical, chemical, and biological indicators. This environment favors investment in integrated washer-disinfectors, advanced autoclaves, digital cycle tracking, and ergonomic layouts based on “dirty-to-clean” workflows, enabling vendors of cleaning & sterilization equipment to capture a larger share of capital budgets. Vendors that bundle equipment with training, validation services, and preventive maintenance can build long-term partnerships with DSOs, positioning themselves strongly in the fastest-growing equipment segment.

Innovation in PPE and single-use infection barriers for aerosol-generating procedures

Rapid innovation in personal protective equipment and single-use barriers presents another significant opportunity, particularly in the context of aerosol-generating procedures where infection risk is heightened. The heightened awareness generated during the COVID-19 pandemic has normalized the routine use of N95 or equivalent respirators, face shields, and fluid-resistant gowns in many dental settings, and this behavioral shift is expected to persist, thereby fueling demand for premium PPE lines with enhanced comfort and breathability. At the same time, new single-use barrier products, such as disposable chair covers, light-handle sleeves, and instrument wraps, complement conventional disinfectants and help practices reduce cross-contamination and turnaround time between patients. Manufacturers that can integrate regulatory compliance, fit-tested respiratory protection, and sustainable materials into PPE and barrier portfolios are well positioned to benefit from this opportunity, as the PPE segment remains the fastest-growing product category.

Category-wise Analysis

Product Type Insights

Cleaning & sterilization equipment is the leading product type, accounting for an estimated 27% market share in 2025, reflecting the central role of validated instrument reprocessing in dental infection prevention. Modern guidelines emphasize multi-step workflows that include pre-cleaning, ultrasonic or mechanical cleaning, rinsing, drying, packaging, sterilization, and storage, all of which depend on reliable equipment to ensure consistent outcomes. The CDC recommends using mechanical, chemical, and biological indicators to monitor sterilization cycles, which promotes continuous upgrades to autoclaves and monitoring systems in both dental clinics and hospitals. As the global oral disease burden rises and procedural volumes increase, practices prioritize investments in robust, high-capacity sterilization units and washer-disinfectors to manage throughput, making this category the structural backbone of the dental infection-prevention ecosystem.

Application Insights

Within dental applications, preventive dentistry is emerging as the leading segment by market share, accounting for an estimated 30–35% of dental infection-prevention spending in 2025, as health systems increasingly emphasize early intervention and routine care. Preventive visits, such as check-ups, cleanings, sealant placement, and fluoride treatments, constitute a high-volume, recurring workload that requires rigorous adherence to infection-control protocols for hand instruments, ultrasonic scalers, and prophylaxis equipment. Given that untreated caries in permanent teeth affects about 2.24 billion people worldwide, preventive care is expanding in both public and private settings, necessitating regular use of PPE, surface disinfectants, and standardized sterilization between patients. This consistent flow of low-acuity yet instrument-intensive procedures underpins stable demand for infection prevention consumables and equipment, solidifying preventive dentistry as the anchor application segment.

End-user Insights

Dental clinics constitute the leading end-user segment, accounting for an estimated 55–60% share of the dental infection prevention market in 2025, owing to their dominant role in delivering routine and specialized oral care services worldwide. Independent practices, group clinics, and DSOs collectively perform the majority of preventive, restorative, periodontal, and minor surgical procedures, all of which necessitate meticulous sterilization and disinfection processes. Professional bodies such as the American Dental Association (ADA) and national dental councils provide detailed guidance on infection control and sterilization for office-based settings, pushing clinics to invest in compliant sterilization products, PPE, and environmental disinfectants. As more countries expand dental insurance coverage and integrate oral health into universal health care frameworks, clinic patient volumes and procedure intensity increase, thereby reinforcing clinics’ position as the primary purchasers of infection-prevention solutions.

Regional Insights

North America Dental Infection Prevention Market Trends and Insights

North America holds the leading regional position, with an estimated 40% share of the dental infection prevention market in 2025, supported by high dental care utilization and strong regulatory frameworks. In the United States, agencies such as the CDC and OSHA enforce comprehensive standards covering instrument reprocessing, PPE use, and environmental disinfection in dental settings, prompting widespread adoption of advanced sterilization systems and high-performance disinfectants. The region benefits from a robust innovation ecosystem, with manufacturers and academic partners developing improved autoclaves, digital monitoring tools, and ergonomic reprocessing layouts that streamline workflows and enhance compliance.

Asia Pacific Dental Infection Prevention Market Trends and Insights

Asia Pacific is the fastest-growing regional market for dental infection prevention, driven by rapid urbanization, expanding middle-class populations, and rising awareness of oral health in China, India, Japan, and ASEAN economies. Large unmet need is evident as oral disorders show high incidence in Southeast Asia, yet dental infrastructure and infection control practices are still evolving, creating a substantial runway for equipment and consumables adoption. Governments in countries such as China and India are increasing investment in public oral health programs and dental education, while private chains and hospitals are expanding specialized dental centers, thereby boosting demand for autoclaves, chair-side disinfectants, and PPE.

Competitive Landscape

The dental infection prevention market features a moderately consolidated yet competitive environment, with multinational manufacturers and regional suppliers competing through broad product portfolios, regulatory compliance, and strong distribution networks. Companies focus on developing advanced sterilization systems, eco-friendly disinfectants, and high-performance protective consumables to meet stricter infection-control standards in dental clinics and hospitals. Strategic initiatives such as portfolio expansion, technology upgrades, acquisitions, and partnerships are commonly used to strengthen market presence and enter emerging regions. Growing awareness of cross-contamination risks and routine hygiene protocols continues to intensify competition, while service support and pricing strategies remain key differentiators among suppliers globally.

Key Developments:

- In January 2026, NewEra Hospitals launched a Dental Care Department at its Vashi facility in Navi Mumbai. The department was established to address dental and oral healthcare needs in the region by bringing advanced infrastructure, modern equipment, and specialist services under one roof. It was designed to offer a comprehensive range of dental treatments, from routine check-ups to complex oral and maxillofacial procedures.

Companies Covered in Dental Infection Prevention Market

- 3M Company

- Dentsply Sirona

- Henry Schein

- Kerr Corporation

- Hu-Friedy Mfg. Co.

- STERIS Corporation

- SciCan

- Crosstex International

- COLTENE Group

- Young Innovations

- GC Corporation

- A-dec Inc

- Midmark Corporation

- Cantel Medical

- Getinge AB

Frequently Asked Questions

The global dental infection prevention market size is projected to reach about US$ 1.7 billion in 2026, supported by growing dental procedure volumes, stringent infection control guidelines, and rising oral disease burden worldwide.

The primary demand driver is the combination of high global prevalence of dental caries and periodontal disease affecting nearly 3.5 billion people and strict regulatory requirements for sterilization, disinfection, and PPE use in dental settings.

North America leads the dental infection prevention market, with around 40% share in 2025, driven by high dental care utilization, strong CDC and OSHA-aligned regulations, and early adoption of advanced sterilization technologies.

A key opportunity lies in providing integrated cleaning & sterilization equipment, digital monitoring, and training services to group practices and DSOs, particularly in high-growth regions such as Asia Pacific and expanding corporate dental networks globally.

Major players include 3M Company, Dentsply Sirona, Henry Schein, Kerr Corporation, Hu‑Friedy Mfg. Co., STERIS Corporation, SciCan, Crosstex International, COLTENE Group, Young Innovations, GC Corporation, A‑dec Inc., and several other international and regional manufacturers.