- Food Ingredients & Additives

- Creamers Market

Creamers Market Size, Share, and Growth Forecast 2026 - 2033

Creamers Market by Product Type (Dairy-Based Creamers, Non-Dairy Creamers), by Nature (Powder, Liquid), by End Use (B2B, B2C), and by Regional Analysis, 2026-2033

Creamers Market Size and Trends Analysis

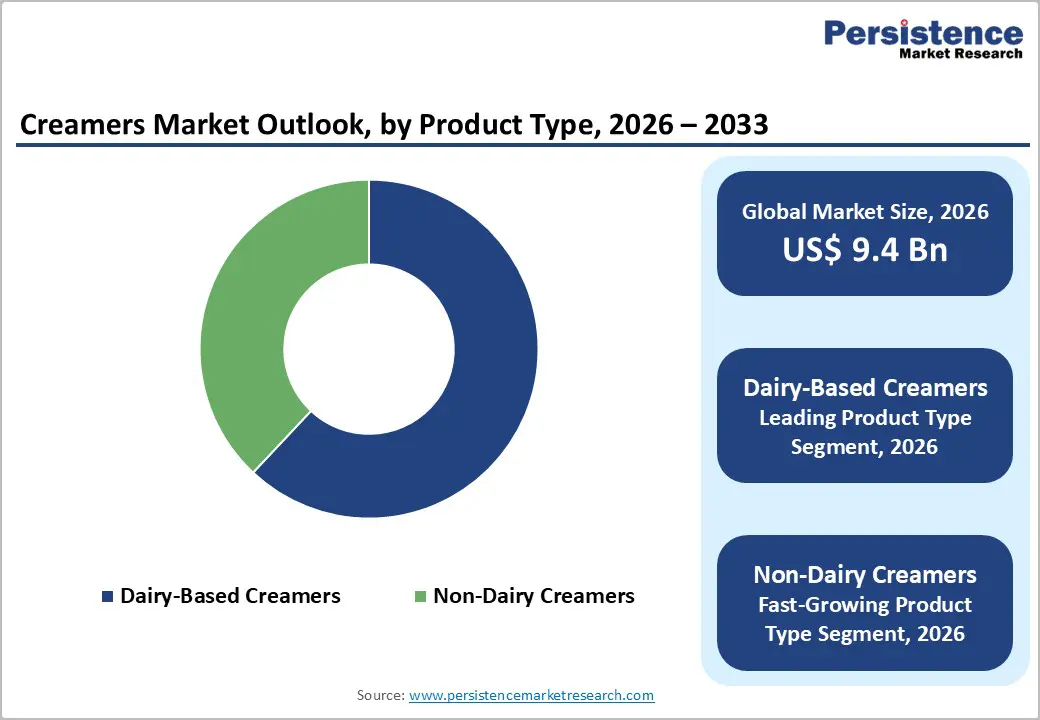

The global Creamers market size is expected to be valued at US$ 9.4 billion in 2026 and projected to reach US$ 13.5 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033.

The upward trajectory of the market is predominantly anchored in the global resurgence of coffee consumption and the intensifying demand for convenient, flavor-enhancing additives in beverage rituals. As urban populations expand and disposable incomes rise across emerging economies, the adoption of specialized creamers has evolved from a basic milk substitute to a premium sensory experience. According to data from the International Coffee Organization, world coffee consumption recently rebounded to over 177 million bags, creating a direct and proportional tailwind for the accompanying creamer industry across both household and commercial segments.

Key Industry Highlights

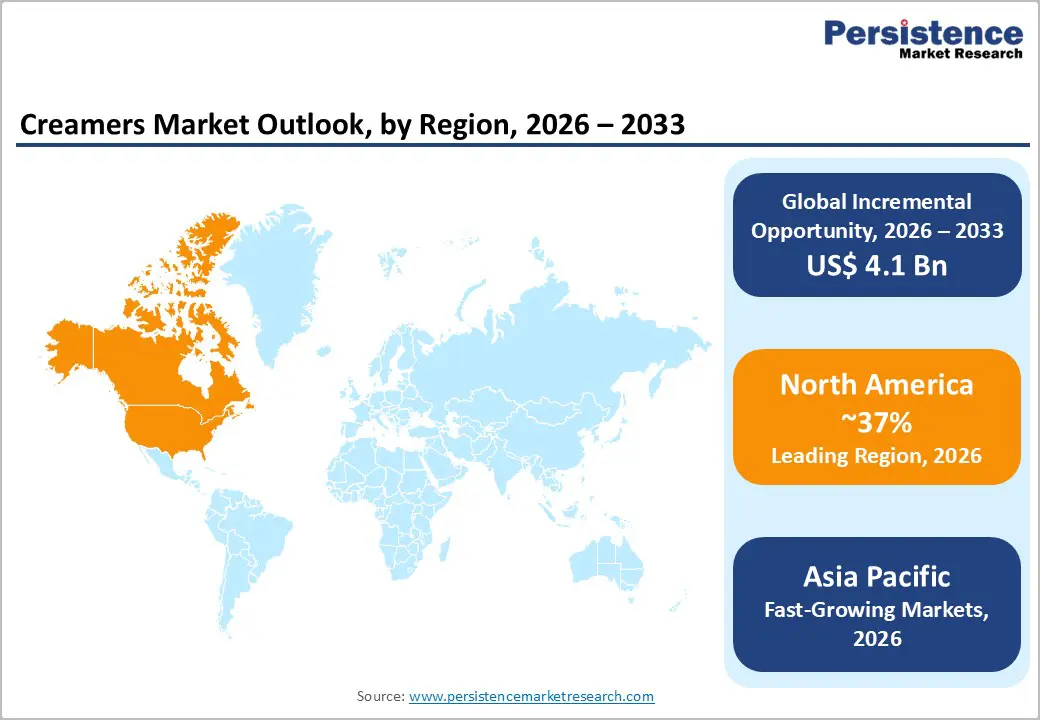

- Leading Region: North America, holding 37% market share, supported by strong coffee culture, premium flavor experimentation, clean-label innovation, and widespread availability across retail and e-commerce channels.

- Fastest-Growing Region: Asia Pacific, driven by rapid urbanization, Western-style coffee adoption, rising middle-class incomes, and expanding café culture across China, India, Japan, and Southeast Asia.

- Fastest-Growing Product Type Segment: Non-Dairy Creamers, fueled by rising lactose intolerance, vegan lifestyles, and innovation in oat-, almond-, coconut-, and soy-based formulations offering improved taste and functionality.

- Market Drivers: Rising demand for plant-based and lactose-free alternatives as consumers prioritize digestive health, sustainability, ethical sourcing, and clean-label ingredients in daily beverage consumption.

- Opportunities: Development of functional and clean-label creamers fortified with probiotics, vitamins, adaptogens, and natural sweeteners, positioning coffee as a daily wellness delivery platform.

- Key Developments: In November 2025, Danone’s Too Good & Co launched a new range of coffee creamers to expand beyond core dairy. In October 2025, Oatly introduced a plant-based creamer optimized for push-button coffee machines to strengthen foodservice penetration.

| Key Insights | Details |

|---|---|

| Global Creamers Market Size (2026E) | US$ 9.4 Bn |

| Market Value Forecast (2033F) | US$ 13.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.6% |

Market Dynamics

Driver – Rising Demand for Plant-Based and Lactose-Free Alternatives

A primary catalyst for the Creamers Market expansion is the accelerating global shift toward dairy alternatives, catalyzed by rising awareness of lactose intolerance and vegan lifestyles. According to data from the Plant-Based Foods Association, non-dairy creamer sales in mature markets like the United States have recently demonstrated growth rates as high as 24%, underscoring a significant transition in dietary priorities. Consumers are increasingly replacing traditional dairy with bases derived from Oats, Almonds, Soy, and Coconut, seeking "clean label" formulations that offer identical functionality without animal-derived allergens. This shift is particularly pronounced among Millennial and Gen Z demographics who prioritize digestive health, sustainability, and ethical sourcing, forcing market leaders like Danone and Nestle S.A. to diversify their product portfolios with innovative plant-based formulations.

Restraints – Health Concerns Regarding Saturated Fats and Artificial Additives

A notable barrier to market growth is the mounting scrutiny of ingredient labels by health-conscious consumers concerned about the high sugar and saturated fat content in conventional creamers. Many traditional non-dairy creamers utilize Hydrogenated Oils, which can contribute to heart health issues if consumed in excess. Regulatory bodies such as the U.S. Food and Drug Administration (FDA) and the European Food Safety Authority (EFSA) have intensified guidelines on Trans-Fats and artificial sweeteners, compelling manufacturers to undertake costly reformulations. This scrutiny often leads to a negative consumer perception of highly processed creamers, potentially driving a segment of the market back toward fresh milk or minimally processed additives, thereby slowing the adoption rate of standard shelf-stable products.

Opportunity – Innovation in Functional and Clean-Label Creamer Formulations

Manufacturers have a significant opportunity to capitalize on the "Health and Wellness" trend by integrating functional ingredients such as Probiotics, Vitamins, and Adaptogens into their creamer formulations. Consumers are increasingly viewing their morning coffee as an delivery vehicle for holistic nutrition, creating a market for "superfood" creamers that offer more than just flavor. According to recent news from the Plant-Based Foods Association, the demand for low-sugar and allergen-friendly options is evolving into a preference for fortification. By achieving Organic Certification and utilizing natural sweeteners like Stevia or Monk Fruit, brands can distinguish themselves in a crowded marketplace. This strategic focus on health-centric innovation allows companies to align with global movements toward transparency and better-for-you food products, ensuring sustained engagement with the health-conscious consumer.

Category-wise Analysis

Product Type Analysis

The Dairy-Based Creamers segment held the leading market share, accounting for 62% of the total revenue in 2025. This dominance is attributed to the traditional taste preference of classic coffee drinkers who prioritize the rich, creamy mouthfeel and familiar flavor profile that only animal-derived fats can provide. Industry giants like Saputo Inc. and Arla Foods maintain a strong presence in this category by leveraging robust dairy supply chains and introducing lactose-free variants that cater to health-conscious users without sacrificing authentic flavor. However, Non-Dairy Creamers represent the fastest-growing segment through the forecast period. Driven by a surge in veganism and a rise in lactose intolerance globally, this segment is benefiting from a wave of innovation in Almond, Oat, and Coconut bases that appeal to a wide consumer base seeking digestive health and sustainability.

Distribution Channel Analysis

The B2C (Business-to-Consumer) segment represents the largest end-use category in the Creamers Market, driven by the high volume of daily household coffee consumption. As at-home brewing technologies improve, consumers are increasingly willing to invest in premium creamers to enhance their domestic beverage experience. Retail giants like Nestle S.A. have successfully utilized their Coffee-Mate brand to capture this household demand through innovative packaging and seasonal flavor launches. Conversely, the B2B (Business-to-Business) segment, primarily comprising Foodservice & HoReCa, is the fastest-growing end-use area. This growth is fueled by the rapid expansion of international coffee chains and the rising demand for "on-the-go" beverage solutions. Cafés and restaurants are increasingly requiring large-format, high-stability creamers to manage high-volume service while maintaining the consistency that global specialty brands demand.

Region-wise Insights

North America Creamers Market Trends and Insights

North America remains the dominant region in the global landscape, holding a 37% market share in 2025. The region's leadership is anchored in the United States, which possesses a deeply ingrained coffee culture and high per-capita consumption rates. A key trend in this region is the aggressive shift toward premiumization and "flavor-exploration," where consumers frequently rotate between seasonal limited editions and permanent artisanal flavors.

The regulatory environment in North America, governed by the FDA, has recently focused on transparency in labeling, which has spurred an innovation ecosystem centered on "clean-label" and non-GMO products. Furthermore, the robust retail infrastructure and the rapid expansion of e-commerce channels have made a diverse array of both dairy and plant-based creamers highly accessible. Major domestic players like Califia Farms, LLC and Danone have established significant manufacturing advantages here, utilizing advanced aseptic packaging technology to extend shelf life without the use of artificial preservatives, thereby aligning with the health-conscious values of the modern American consumer.

Asia Pacific Creamers Market Trends and Insights

The Asia Pacific region is the fastest-growing market for creamers globally, projected to record a high CAGR through 2032. This rapid expansion is primarily driven by the "Westernization" of food habits and a burgeoning middle-class population in countries like China, India, and Japan. Urbanization has led to a significant increase in coffee consumption among younger demographics, who view specialty coffee as a status symbol and a daily convenience.

According to reports from the International Coffee Organization, Vietnam and Indonesia are not only major producers but are also becoming significant consumers of processed coffee additives. The region's growth dynamics are unique due to the dual demand for affordable Powder creamers in traditional retail and premium Non-Dairy alternatives in modern café chains. Manufacturing advantages in the region are attracting global players who are setting up localized production facilities to cater to regional taste profiles, such as Coconut and Soy-based options that align with traditional Asian dietary staples. The rise of online grocery platforms in Southeast Asia is also facilitating the rapid penetration of diverse creamer brands into previously untapped rural and semi-urban markets.

Market Competitive Landscape

The Creamers Market is characterized by a moderate degree of consolidation, with a handful of global conglomerates like Nestle S.A. and Danone holding significant market power through their flagship brands and extensive distribution networks. However, the market remains highly competitive due to the rapid emergence of agile, plant-based specialists such as Califia Farms, LLC and Oatly, who have disrupted the traditional dairy hierarchy with their focused brand identities and innovation-led strategies. Leading players are increasingly adopting multi-channel approaches, leveraging both B2B partnerships with global coffee chains and B2C e-commerce platforms. Emerging business model trends show a pivot toward "Direct-to-Consumer" (DTC) subscription models and sustainable sourcing as key differentiators. Market leaders are also investing in R&D for weight-loss-friendly and high-protein formulations to align with evolving health trends and maintain brand loyalty in a crowded retail landscape.

Key Developments:

- In November 2025, Danone’s Too Good & Co unveiled a new range of coffee creamers, expanding its portfolio beyond core dairy offerings.

- In October 2025, Oatly introduced a new plant-based milk formulated specifically for push-button coffee machines. The launch reinforces its strategy to boost foodservice penetration by offering barista-friendly oat solutions for high-traffic beverage environments.

- In August 2025, Califia Farms expanded its Simple & Organic range with three new seasonal creamers designed for autumn and winter preferences. The company also introduced a creamy horchata beverage, strengthening its position in the dairy-alternative creamer category.

Companies Covered in Creamers Market

- Nestle S.A.

- Danone

- Organic Valley

- Royal FrieslandCampina N.V.

- PT. Santos Premium Krimer

- Califia Farms, LLC

- Oatly

- Chobani

- Lactalis Group

- Arla Foods

- Saputo Inc.

- Others

Frequently Asked Questions

The global Creamers Market is expected to be valued at approximately US$ 9.4 billion in 2026, growing steadily at a CAGR of 5.3% from its historical base.

The demand is primarily driven by the rising global Coffee Consumption, a surge in Lactose-Free and plant-based dietary preferences, and the expansion of the professional Café Culture across emerging economies.

North America is the leading regional market, holding a 37% share in 2025, supported by a mature retail infrastructure and continuous innovation in indulgent and health-focused formulations.

Significant opportunities lie in the development of Barista-Grade non-dairy formulations and the integration of Functional Ingredients such as probiotics and protein to cater to health-conscious consumers.

Key players include Fonterra Co-Operative Group Limited, Arla Food Ingredients Group, Glanbia Plc, Lactalis Group, FrieslandCampina, Saputo Inc., Idaho Milk Products, Nestle S.A., Danone, Nestle S.A., Lactalis Group, Arla Foods, Saputo Inc., and others