- Nutraceuticals & Functional Foods

- Chickpea Protein Market

Chickpea Protein Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Chickpea Protein Market by Product Type (Isolate, Concentrate, Hydrolyzed, Textured), Nature (Organic, Conventional), End-user (Functional Foods & Beverages, Sports Nutrition, Infant & Early Life Nutrition, Animal Nutrition, Others), and Regional Analysis, 2026 - 2033

Chickepea Protein Market Share and Trends Analysis

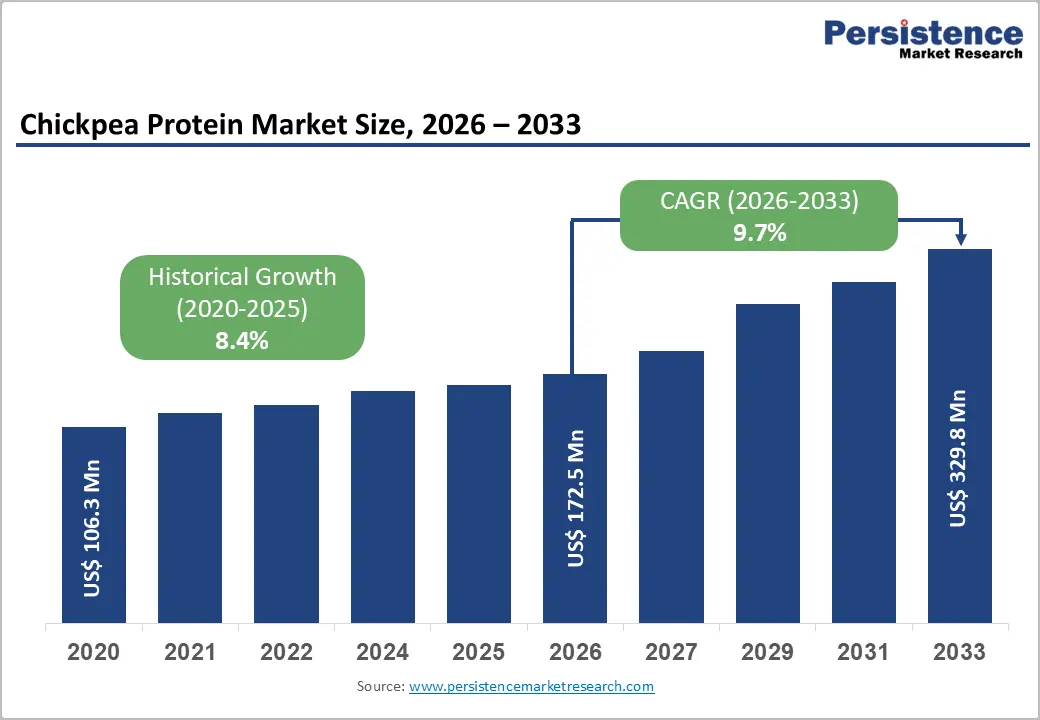

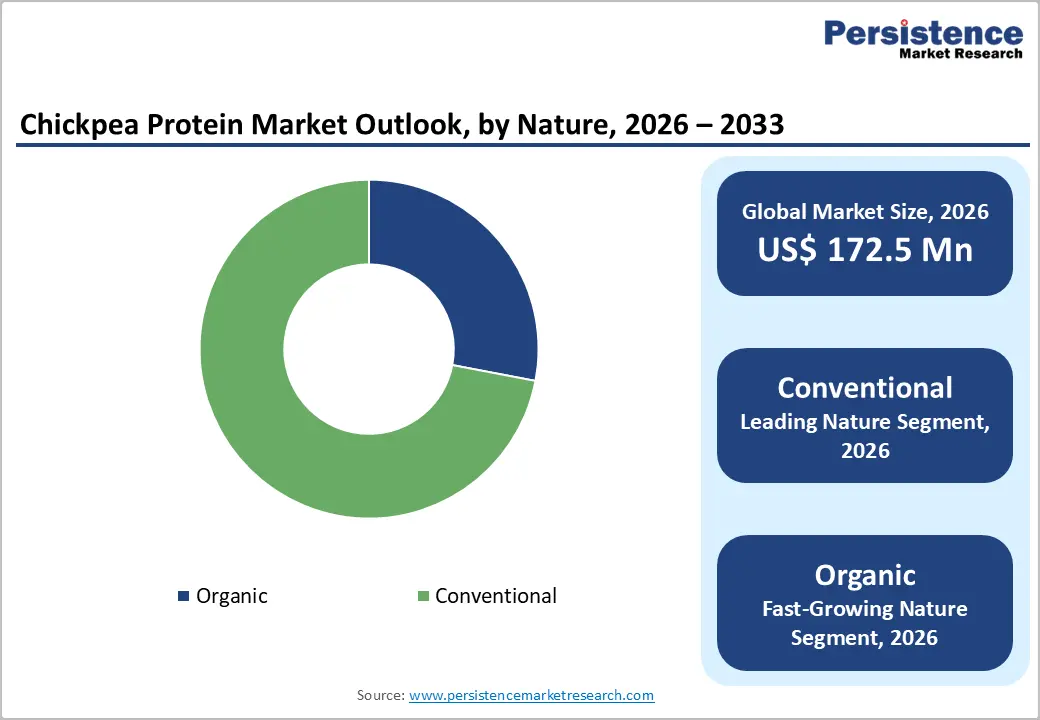

The global chickpea protein market size is expected to be valued at US$ 172.5 million in 2026 and projected to reach US$ 329.8 million by 2033, growing at a CAGR of 9.7% between 2026 and 2033.

The global market is transitioning rapidly from a niche plant ingredient space into a strategically important protein segment, driven by allergen-friendly positioning, clean-label demand, and expanding applications across functional nutrition and meat alternatives. While supply-side constraints persist, innovation, organic adoption, and regional diversification continue to reshape competitive dynamics.

Key Industry Highlights:

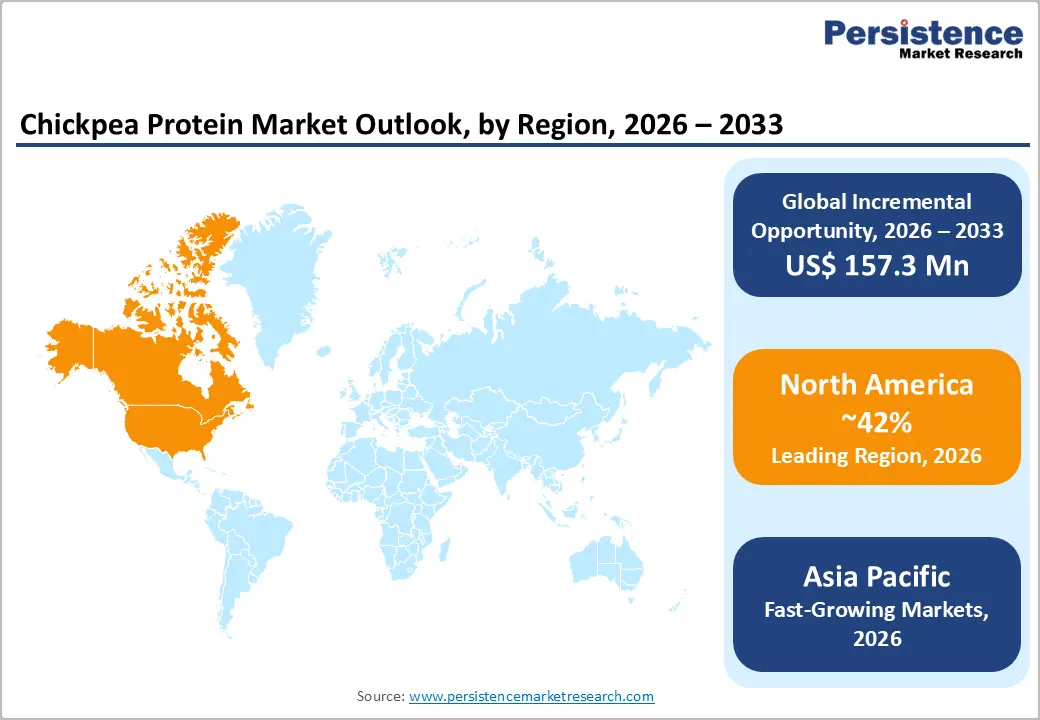

- Leading Region: North America, holding approximately 42% market share, supported by advanced food innovation ecosystems, strong plant-based adoption, and high demand for allergen-friendly, clean-label protein ingredients across functional foods, beverages, and meat alternatives

- Fastest-Growing Region: Asia Pacific, projected to grow at a CAGR of 10.3%, driven by rising protein awareness, cultural acceptance of pulses, urban dietary shifts, and expanding use of chickpea protein in fortified foods and modern plant-based formats across India, China, Japan, and South Korea

- Dominant End-Use Segment: Functional Foods & Beverages, accounting for around 38% market share as of 2025, fueled by demand for convenient nutrition, protein fortification, digestive health positioning, and stability in liquid and ready-to-consume applications

- Market Drivers: Rising consumer demand for allergen-friendly plant proteins, as chickpea protein’s soy-free, gluten-free, and dairy-free profile aligns with inclusive nutrition trends, food allergy awareness, and stricter labeling expectations worldwide

- Opportunities: Development of healthy and tasty textured chickpea protein for meat analogs, enabled by advances in extrusion and fermentation that improve texture, mouthfeel, and clean-label appeal while supporting high-protein claims

- Key Developments: In September 2025, Shandi Global launched Chanza, a whole chickpea-based plant protein, in India; in August 2025, NuCicer Inc. raised USD 11.5 million to expand production of hybrid high-protein chickpea varieties

| Key Insights | Details |

|---|---|

|

Global Chickpea Protein Market Size (2026E) |

US$ 172.5 Mn |

|

Market Value Forecast (2033F) |

US$ 329.8 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

9.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

8.4% |

Market Dynamics

Driver - Rising Consumer Demand for allergen-friendly plant proteins

A quiet shift in dietary priorities is reshaping protein sourcing worldwide, as consumers actively seek allergen-friendly nutrition solutions. Chickpea protein has emerged as a preferred option due to its natural absence of soy, gluten, and dairy, making it suitable for sensitive populations. Parents, athletes, and aging consumers increasingly favor chickpea-based proteins for daily nutrition, driven by clean ingredient lists and digestive comfort. Its mild taste and smooth texture further support incorporation into functional foods, beverages, and snacks without compromising sensory appeal.

This demand is amplified by rising food allergy awareness and stricter labeling expectations across retail and foodservice channels. Manufacturers view chickpea protein as a low-risk, high-acceptance ingredient that aligns with inclusive nutrition trends. As flexitarian and plant-forward diets expand, allergen-friendly proteins are transitioning from niche offerings into mainstream formulations, strengthening chickpea protein’s role as a core growth driver.

Restraints - Limited large-scale processing capacity constrains consistency in global supply

Behind growing interest in chickpea protein lies a structural bottleneck that continues to limit market expansion. Large-scale processing infrastructure for chickpea protein extraction remains unevenly distributed, restricting the ability to deliver consistent volumes across regions. Many producers rely on small or mid-sized facilities that struggle to meet rising demand from multinational food brands, leading to supply volatility and longer lead times.

This capacity gap also affects quality standardization, protein yield efficiency, and cost competitiveness. Inconsistent processing capabilities complicate long-term supply contracts, discouraging large buyers from adopting them fully. Capital-intensive equipment, technical expertise requirements, and regional crop variability further slow capacity expansion. Until investments accelerate in modern processing plants and scalable technologies, supply-side limitations will continue to restrain the global chickpea protein market despite strong downstream demand.

Opportunity - Development of healthy and tasty textured chickpea protein for meat analogs

Innovation at the intersection of taste, texture, and nutrition is unlocking new growth avenues for chickpea protein. Advances in extrusion and fermentation technologies now enable the creation of textured chickpea proteins that closely mimic the bite and juiciness of meat. This positions chickpea protein as a strong candidate for next-generation meat analogs targeting health-conscious consumers seeking clean-label, recognizable ingredients.

Startups and established players alike are leveraging chickpea protein’s neutral flavor and functional versatility to develop burgers, nuggets, and minced alternatives with improved mouthfeel. Its nutritional profile supports high-protein claims without relying on heavily processed inputs. As demand for healthier plant-based meats rises, textured chickpea protein offers a compelling opportunity for brands to differentiate through superior taste, nutrition, and simpler formulations.

Category-wise Analysis

By End-user, Functional foods & beverages dominate the global market

Functional Foods & Beverages holds approx. 38% market share as of 2025, reflecting strong consumer demand for nutrition that delivers measurable health benefits. Chickpea protein integrates seamlessly into protein shakes, nutrition bars, fortified snacks, and wellness beverages due to its smooth texture and balanced amino acid profile. Brands increasingly position these products around digestive health, sustained energy, and plant-based protein enrichment.

The dominance of this segment is reinforced by urban lifestyles favoring convenient, on-the-go nutrition formats. Chickpea protein supports clean-label positioning while enabling fortification without altering taste profiles. Food developers value its stability in liquid and semi-solid applications, expanding usage across ready-to-consume formats. As functional nutrition shifts from supplements toward everyday foods, this segment continues to anchor global chickpea protein demand.

Organic chickpea protein is anticipated to register strong growth during the forecast period

Organic Chickpea Protein is projected to grow at a CAGR of 11.6% during the forecast period as clean-label nutrition moves from preference to expectation. Consumers increasingly associate organic certification with transparency, chemical-free farming, and better long-term health outcomes. Chickpea protein benefits from this perception while offering allergen-friendly functionality and strong digestibility. Food and beverage brands use organic variants to strengthen trust, premium positioning, and label simplicity across sports nutrition, functional drinks, and fortified foods.

Growth is further supported by sustainability-driven purchasing and regulatory scrutiny on agricultural inputs. Organic chickpea protein aligns with regenerative farming, reduced pesticide exposure, and ethical sourcing narratives. Manufacturers value its versatility in powders, bars, and plant-based meals. As global organic food shelves expand, organic chickpea protein is transitioning from a niche ingredient to a mainstream protein solution for diverse consumer segments seeking trusted plant nutrition.

Regional Insights

North America Chickpea Protein Market Trends

North America holds approximately 42% market share in the global chickpea protein market, supported by advanced food innovation ecosystems and high plant-based adoption. In the U.S., chickpea protein is increasingly used in functional beverages, sports nutrition, and plant-based meat alternatives, driven by clean-label and allergen-aware consumers. Product launches emphasize minimal processing, protein density, and digestive comfort.

Canada complements this trend through strong availability of pulse crops and investment in value-added processing. Domestic food manufacturers are integrating chickpea protein into bakery products, snacks, and ready meals, targeting flexitarian diets. Supportive agricultural policies and export-oriented ingredient suppliers strengthen regional supply chains. Together, the U.S. and Canada continue to shape North America as a mature yet innovation-driven chickpea protein market.

Asia Pacific Chickpea Protein Market Trends

Asia Pacific chickpea protein market is expected to grow at a CAGR of 10.3%, fueled by dietary diversification and rising protein awareness. In India, chickpea protein benefits from cultural familiarity with pulses and growing demand for modern plant-based nutrition formats. Domestic brands increasingly incorporate it into fortified foods and beverages aimed at urban consumers.

China’s interests center on functional nutrition and alternative proteins that support wellness-driven lifestyles. Japan and South Korea emphasize precision nutrition, clean ingredients, and novel textures, encouraging use in beverages and meat alternatives. Regional manufacturers leverage chickpea protein for its balance of nutrition, taste adaptability, and compatibility with local cuisines. These dynamics position Asia Pacific as a high-growth, innovation-led market distinct from Western consumption patterns.

Competitive Landscape

The global chickpea protein market is moderately fragmented, with a mix of established ingredient suppliers and agile startups. Leading companies focus on clean-label formulations, improved protein functionality, and consistent quality to strengthen B2B relationships with food and beverage manufacturers. Certifications related to organic sourcing, food safety, and sustainability enhance credibility across global markets.

Competitive strategies increasingly emphasize product innovation for plant-based meat, functional foods, and beverages. Partnerships with food brands accelerate commercialization, while export opportunities in developing regions attract investment. Sustainability initiatives, aligned with evolving government regulations, influence sourcing and processing decisions. As competition intensifies, differentiation through technology, transparency, and application-specific solutions defines long-term success.

Key Developments:

- In September 2025, Singapore-based food-tech firm Shandi Global officially entered the Indian market with the launch of Chanza, a plant-based protein derived from whole chickpeas.

- In August 2025, Davis-based food technology company NuCicer Inc. raised USD 11.5 million to scale up the production of its hybrid high-protein chickpea varieties.

- In April 2025, at Vitafoods 2025, ATURA Proteins unveiled a new range of Organic Proteins from Chickpea (70%), Lentil (80%), and Fava Bean (85%), designed to support protein fortification and enhancement across food and beverage applications.

Companies Covered in Chickpea Protein Market

- Ingredion Incorporated

- The Scoular Company

- Cargill, Incorporated

- Glanbia plc

- ChickBumin

- NOW® Foods

- ADM

- Sun Nutrafoods

- Kerry Group plc

- AGT Food and Ingredients Inc.

- Daily Harvest

- Axiom Foods

- Atura

- Others

Frequently Asked Questions

The global chickpea protein market is projected to be valued at US$ 172.5 Mn in 2026.

Rising consumer demand for allergen-friendly plant proteins is a key driver for the global chickpea protein market.

The global chickpea protein market is poised to witness a CAGR of 9.7% between 2026 and 2033.

Development of healthy and tasty textured chickpea protein for meat analogs is key opportunity.

Major players in the global Chickpea Protein market include Ingredion Incorporated, The Scoular Company, Cargill, Incorporated, Glanbia plc, NOW® Foods, ADM, Kerry Group plc, Axiom Foods, and others.