- Medical Devices

- Cancer Cryotherapy Market

Cancer Cryotherapy Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Cancer Cryotherapy Market by Product Type (Cryosurgery Systems, Cryoablation Systems, Localized Cryotherapy Devices, Cryotherapy Probes, Others), Disease Indication (Skin Cancer, Prostate Cancer, Cervical Cancer, Actinic Keratosis, Bone Cancer, Others) End-user (Hospitals, Specialty Cancer Centers, Ambulatory Surgical Centers (ASCs), Others), and Regional Analysis from 2026 to 2033

Cancer Cryotherapy Market Share and Trends Analysis

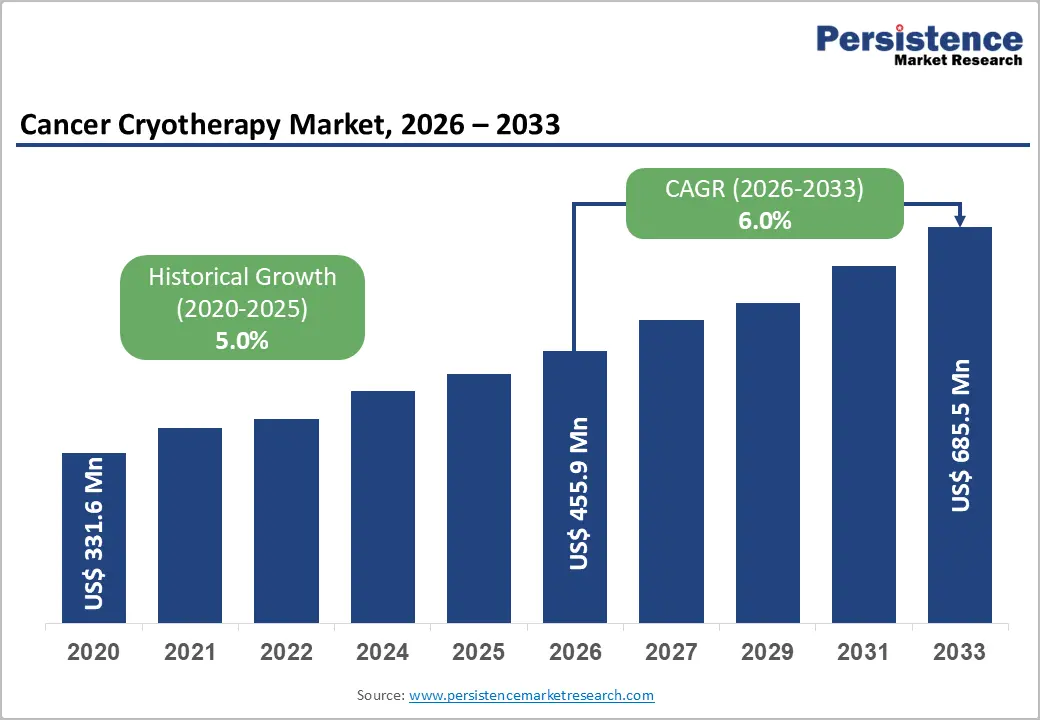

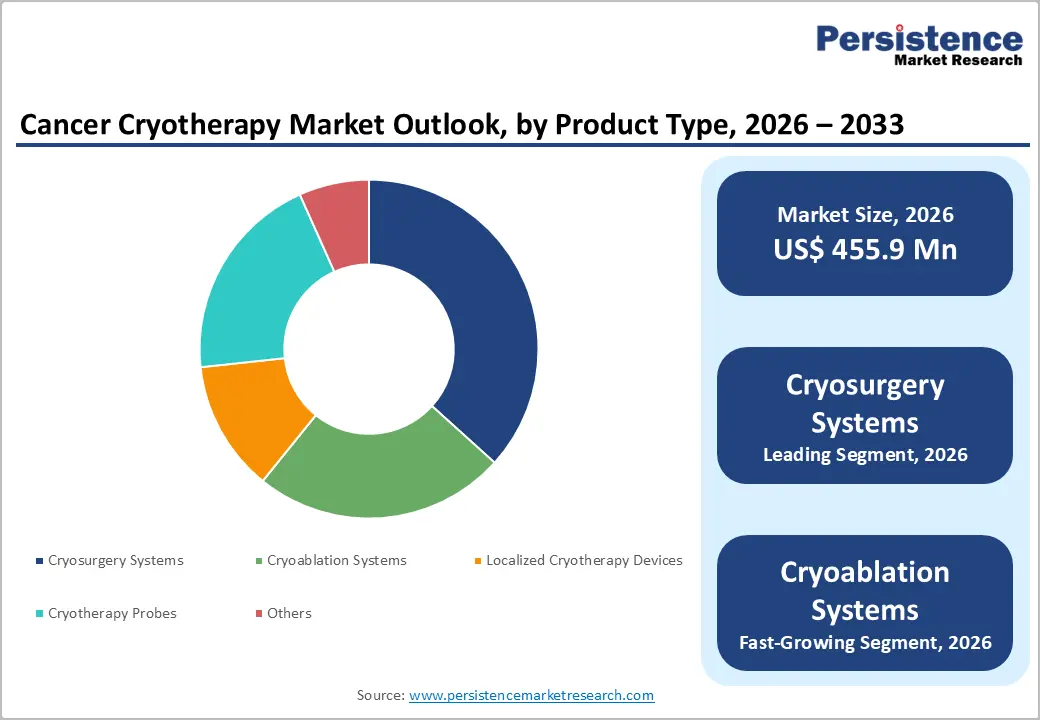

The global cancer cryotherapy market is estimated to grow from US$ 455.9 million in 2026 to US$ 685.5 million by 2033. The market is projected to record a CAGR of 6.0% during the forecast period from 2026 to 2033.

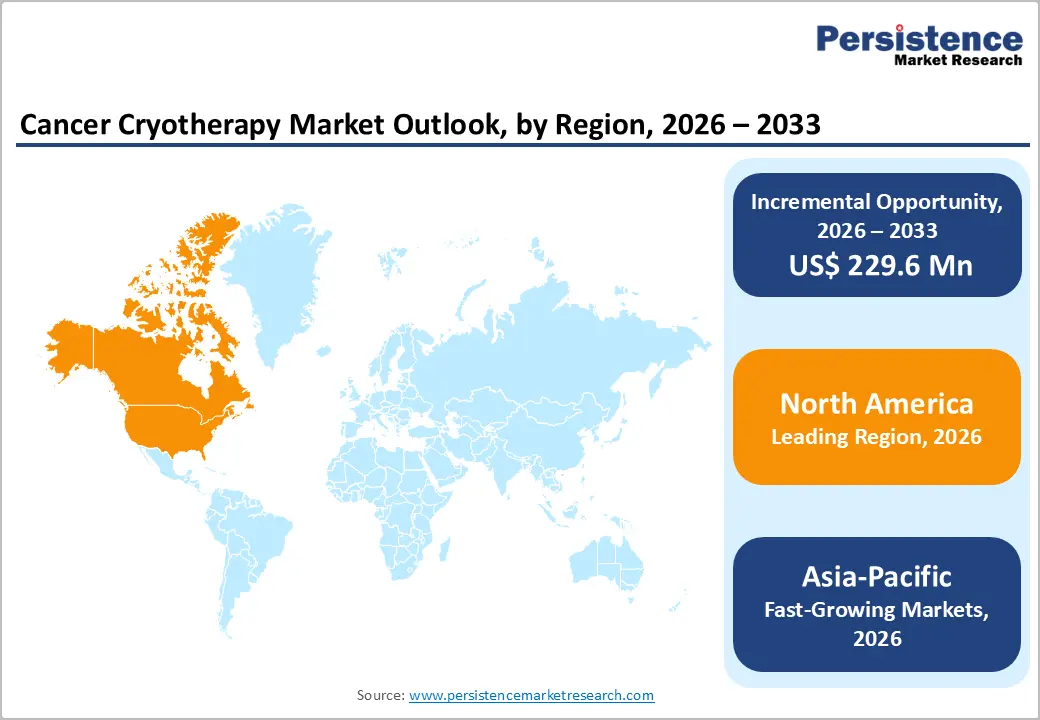

The global market is expanding steadily, driven by rising adoption of minimally invasive tumor ablation procedures and preference for targeted, tissue-sparing treatments. North America leads due to advanced oncology infrastructure and established device manufacturers, while Asia-Pacific is the fastest-growing region, supported by increasing cancer incidence, improving healthcare facilities, and growing awareness of cryoablation therapies.

Key Industry Highlights:

- Dominant Product Segment: Cryosurgery systems held 36.7% share in 2025, driven by strong adoption in minimally invasive tumor ablation, precision targeting, and growing preference for tissue-sparing procedures across prostate, liver, and kidney cancers.

- Dominant Region: North America is the leading region with 40.3% share in 2025, supported by advanced oncology infrastructure, high adoption of image-guided cryoablation, and presence of major device manufacturers.

- Growth Indicator: Growth is driven by increasing cancer incidence, rising preference for minimally invasive therapies, advancements in cryoablation technology, and expanding awareness among patients and physicians.

- Market Opportunity: Opportunities include expansion of image-guided cryoablation for additional cancer types, development of portable cryotherapy devices, adoption in emerging markets, and integration with multimodal cancer treatments.

| Key Insights | Details |

|---|---|

| Global Cancer Cryotherapy Market Size (2026E) | US$ 455.9 Mn |

| Market Value Forecast (2033F) | US$ 685.5 Mn |

| Projected Growth (CAGR 2026 to 2033) | 6.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.0% |

Market Dynamics

Driver: Growing preference for minimally invasive tumor ablation procedures

Minimally invasive tumor ablation techniques, including cryoablation, are increasingly preferred over traditional open surgery due to significantly lower patient morbidity and shorter recovery periods. In 2024, more than 62% of all minimally invasive tumor treatment procedures utilized ablation technologies in hospitals globally, driven by shorter hospital stays and reduced complication rates compared to open surgical resection. Clinical adoption reflects that cryoablation alone accounted for over 340,000 procedures worldwide in 2024, marking more than 15.5% growth versus 2023 for cryoablation specifically. Moreover, reductions in procedural trauma with percutaneous cryoablation have expanded indications, particularly in prostate and kidney cancers where preserving organ function is a priority. Government and healthcare data show that these techniques improve quality of life and decrease recovery times by up to 50% compared with conventional surgery, reinforcing clinical preference. Improved imaging guidance and precise thermal control further increase adoption among oncologists and interventional radiologists. This growing preference both expands the overall market and shifts treatment paradigms toward less invasive and more patient-centric oncology interventions.

Restraint: Need for specialized training and expertise for accurate tumor ablation

Cryoablation procedures require a higher degree of technical proficiency and clinical judgment than many conventional cancer treatments. Unlike standard surgical approaches, cryoablation demands precise control of probe placement, freeze-thaw cycles, and real-time imaging interpretation, and mastering these techniques typically requires extensive hands-on experience. Industry sources report that only a limited number of healthcare personnel worldwide have advanced cryoablation training, with procedure proficiency often achieved only after dozens of supervised cases. Specialized training centers and certified programs are scarce; for example, in parts of Southeast Asia, fewer than 20 cryoablation training facilities existed as recently as 2024. This limited availability of skilled practitioners constrains wider clinical adoption since many hospitals are reluctant to deploy cryotherapy programs without trained interventional oncologists and radiologists.

Furthermore, the technical complexity contributes to inconsistent patient outcomes in less experienced hands, which can increase procedural risk and reduce confidence among referring physicians. Because of these factors, many smaller hospitals prefer alternative ablation modalities that require less specialized training, restricting cryotherapy’s geographic and institutional penetration despite its clinical advantages.

Opportunity: Development of portable and cost-effective cryoablation devices

Technological innovation in cryotherapy is enabling smaller, more portable, and cost-effective cryoablation systems that expand access beyond large tertiary hospitals. In 2024, portable cryotherapy ablation devices accounted for nearly 29% of global device deployments, particularly in outpatient and ambulatory oncology settings, reflecting growing clinical preference for devices that reduce setup complexity and operational costs. These portable systems allow treatments to be performed outside of traditional operating rooms, lowering overhead and enabling broader utilization in specialty clinics and rural healthcare centers.

As cancer incidence rises globally, especially in emerging economies with constrained healthcare budgets, compact and affordable cryotherapy units create a strategic opportunity. They can reduce barriers to adoption, since smaller facilities are more likely to invest when capital expenditure and maintenance requirements are lower. Additionally, modular and handheld systems with advanced imaging integration facilitate same-day procedures, optimizing patient throughput and resource utilization.

The trend toward miniaturization and cost reduction aligns with broader health policy goals of expanding access to effective, minimally invasive cancer therapies, making portable cryoablation technology a compelling growth avenue.

Category-wise Analysis

By Product Type Insights

Cryosurgery systems dominate the cancer cryotherapy market with 36.7% share in 2025, because they are versatile, widely adopted, and clinically established across multiple tumor types. These systems enable precise freezing of tumor tissue while preserving surrounding healthy structures, reducing complications compared with open surgery. According to the American Cancer Society, minimally invasive procedures have grown substantially; for instance, percutaneous tumor ablations increased by over 20% between 2017 and 2023 as clinicians seek options with lower morbidity and faster recovery.† Because cryosurgery systems serve both superficial (skin) and deep tumors (prostate, kidney), their clinical use spans outpatient dermatology through interventional oncology.

Additionally, data from the National Cancer Institute (NCI) shows rising utilization: prostate and kidney cancer ablative procedures increased annually, with cryosurgery representing a significant proportion.‡ This broad applicability and strong clinical preference explain their market dominance.

By Disease Indication Insights

Skin cancer dominates the cancer cryotherapy market because it is one of the most prevalent forms of cancer globally, and cryotherapy is a frontline treatment for many superficial lesions. According to World Health Organization (WHO) estimates, non-melanoma skin cancers (basal and squamous cell carcinoma) exceed 5 million new cases annually worldwide, making it the most frequently diagnosed cancer category. Cryotherapy with liquid nitrogen is a standard treatment for actinic keratoses and early skin cancers due to its simplicity, low cost, and effectiveness in office settings without general anesthesia.

In the United States, dermatologic cryotherapy was among the top 5 ambulatory cancer procedures in 2023, reflecting its broad use across age groups. This high incidence of skin cancer, paired with the ready applicability of cryoablation, explains its dominant share in disease indication.

Regional Insights

North America Cancer Cryotherapy Market Trends

North America leads the cancer cryotherapy market because of its advanced healthcare systems, high cancer burden, and early adoption of minimally invasive therapies. The region accounts for the largest share of global ablation therapy usage, capturing 40.3% of the interventional oncology market in 2025, which includes cryoablation procedures. Additionally, the United States alone diagnoses millions of new cancer cases annually, nearly 2.7 million in North America in 2022, driving demand for diverse treatment options.

Favorable healthcare funding, extensive insurance coverage, and the presence of leading medical device manufacturers further accelerate cryotherapy adoption. Physicians and patients in North America increasingly opt for less invasive techniques like cryoablation due to shorter recovery times and reduced procedural risk compared with open surgery, reinforcing the region’s dominant position.

Europe Cancer Cryotherapy Market Trends

Europe is a key region in the cancer cryotherapy market due to its substantial cancer burden and well-established healthcare infrastructure. The region reported over 4.4 million new cancer cases in 2022, demonstrating a significant patient pool for oncology interventions, including cryoablation.European healthcare systems emphasize early detection and adoption of minimally invasive treatments, with national screening programs for breast, prostate, and colorectal cancers contributing to earlier diagnoses and treatment eligibility.

Government healthcare funding and universal coverage support access to advanced technologies, increasing cryotherapy utilization. Additionally, many European countries actively promote integration of interventional oncology within clinical practice, reinforcing Europe’s position as a major regional market second only to North America.

Asia-Pacific Cancer Cryotherapy Market Trends

Asia Pacific is the fastest-growing region in the cancer cryotherapy market due to its rapidly increasing cancer incidence and expanding healthcare access. This region recorded over 8.1 million new cancer cases annually, representing nearly half of the global burden, and signaling substantial demand for advanced treatment modalities like cryoablation. Investments in healthcare infrastructure, particularly in China, India, Japan, and other emerging economies, are increasing accessibility to minimally invasive cancer treatments.

Asia Pacific performs hundreds of thousands of ablation procedures annually, and portable, cost-effective technologies are lowering barriers in non-metropolitan areas. Government screening programs reaching hundreds of millions annually also expand early detection, making more patients eligible for cryotherapy. These factors collectively underpin the region’s robust growth trajectory.

Competitive Landscape

The cancer cryotherapy market is highly competitive, led by major medical device manufacturers such as Medtronic, CooperSurgical, and IceCure Medical. These companies focus on developing advanced cryoablation systems, expanding product portfolios, enhancing imaging-guided precision, and improving accessibility to minimally invasive cancer treatments to maintain market leadership and drive adoption.

Key Industry Developments:

- In November 2025, IceCure Medical Ltd. announced publication of an independent clinical study showing its cryoablation system, when combined with stereotactic body radiation therapy (SBRT), successfully treated stage I non-small cell lung cancer (NSCLC) with a 92% disease-specific five-year survival rate. The retrospective observational study, published in PLOS One, evaluated 64 patients with tumors ≥ 2 cm who received SBRT followed by cryoablation.

- In October 2025, The U.S. Food and Drug Administration granted marketing authorization to the ProSense® cryoablation system as the first cryotherapy treatment for breast cancer, marking a milestone in minimally invasive oncology care. The approval, announced in October 2025, allowed the device to be used for the local treatment of low-risk, early-stage breast tumors in women aged 70 and above who are not suitable for surgery.

Companies Covered in Cancer Cryotherapy Market

- Medtronic

- Boston Scientific Corporation

- Galil Medical

- IceCure Medical Ltd.

- Siemens Healthineers

- Brymill Cryogenic Systems

- CooperSurgical, Inc.

- Sanarus Medical

- CryoConcepts LP

- HealthTronics, Inc.

- Erbe Elektromedizin GmbH

- Zimmer MedizinSysteme GmbH

- AtriCure, Inc.

- Hygea Beijing

- Others

Frequently Asked Questions

The global cancer cryotherapy market is projected to be valued at US$ 455.9 Mn in 2026.

Rising cancer incidence, preference for minimally invasive treatments, technological advancements, and growing patient awareness drive growth.

The global cancer cryotherapy market is poised to witness a CAGR of 6.0% between 2026 and 2033.

Expansion in emerging markets, portable devices, integration with multimodal therapies, and adoption for additional cancer types.

Medtronic, Boston Scientific Corporation, Galil Medical, IceCure Medical Ltd., Siemens Healthineers, Brymill Cryogenic Systems.