- Executive Summary

- Global Cable Modem Termination System Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply-Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Construction Industry Overview

- Global Electric Industry Overview

- Forecast Factors – Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 – 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Cable Modem Termination System Market Outlook: Historical (2020 – 2024) and Forecast (2026 – 2033)

- Key Highlights

- Global Cable Modem Termination System Market Outlook: DOCSIS Standard

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by DOCSIS Standard, 2020-2024

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by DOCSIS Standard, 2026-2033

- DOCSIS 3.0 and Below System Standard

- DOCSIS 3.1 System Standard

- Below System Standard

- Market Attractiveness Analysis: DOCSIS Standard

- Global Cable Modem Termination System Market Outlook: CMTS Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by CMTS Type, 2020-2024

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by CMTS Type, 2026-2033

- Integrated CMTS

- Modular CMTS

- Market Attractiveness Analysis: CMTS Type

- Global Cable Modem Termination System Market Outlook: Application

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Application, 2020-2024

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Business

- Consumer

- Market Attractiveness Analysis: Application

- Global Cable Modem Termination System Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Region, 2020-2024

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Cable Modem Termination System Market Outlook: Historical (2020 – 2024) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by DOCSIS Standard, 2026-2033

- DOCSIS 3.0 and Below System Standard

- DOCSIS 3.1 System Standard

- Below System Standard

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by CMTS Type, 2026-2033

- Integrated CMTS

- Modular CMTS

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Business

- Consumer

- Europe Cable Modem Termination System Market Outlook: Historical (2020 – 2024) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by DOCSIS Standard, 2026-2033

- DOCSIS 3.0 and Below System Standard

- DOCSIS 3.1 System Standard

- Below System Standard

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by CMTS Type, 2026-2033

- Integrated CMTS

- Modular CMTS

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Business

- Consumer

- East Asia Cable Modem Termination System Market Outlook: Historical (2020 – 2024) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by DOCSIS Standard, 2026-2033

- DOCSIS 3.0 and Below System Standard

- DOCSIS 3.1 System Standard

- Below System Standard

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by CMTS Type, 2026-2033

- Integrated CMTS

- Modular CMTS

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Business

- Consumer

- South Asia & Oceania Cable Modem Termination System Market Outlook: Historical (2020 – 2024) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by DOCSIS Standard, 2026-2033

- DOCSIS 3.0 and Below System Standard

- DOCSIS 3.1 System Standard

- Below System Standard

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by CMTS Type, 2026-2033

- Integrated CMTS

- Modular CMTS

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Business

- Consumer

- Latin America Cable Modem Termination System Market Outlook: Historical (2020 – 2024) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by DOCSIS Standard, 2026-2033

- DOCSIS 3.0 and Below System Standard

- DOCSIS 3.1 System Standard

- Below System Standard

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by CMTS Type, 2026-2033

- Integrated CMTS

- Modular CMTS

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Business

- Consumer

- Middle East & Africa Cable Modem Termination System Market Outlook: Historical (2020 – 2024) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by DOCSIS Standard, 2026-2033

- DOCSIS 3.0 and Below System Standard

- DOCSIS 3.1 System Standard

- Below System Standard

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by CMTS Type, 2026-2033

- Integrated CMTS

- Modular CMTS

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Business

- Consumer

- Competition Landscape

- Market Share Analysis, 2024

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Casa Systems

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Arris International Limited

- Cisco System Inc.

- Nokia Corporation

- Harmonic Inc.

- Broadcom Inc.

- Huawei Technologies Co. Ltd

- Chongqing Jinghong Hi-tech Co. Ltd

- Juniper Networks Inc.

- Blonder Tongue Laboratories Inc.

- Casa Systems

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Semiconductor Materials & Components

- Cable Modem Termination System Market

Cable Modem Termination System Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Cable Modem Termination System Market by DOCSIS Standard (DOCSIS 3.0 and Below System Standard, DOCSIS 3.1 System Standard and Below System Standard), By Modem Type (Integrated CMTS and Modular CMTS), Application (Business and Consumer) and Regional Analysis for 2026 - 2033

Cable Modem Termination System Market Size and Trends Analysis

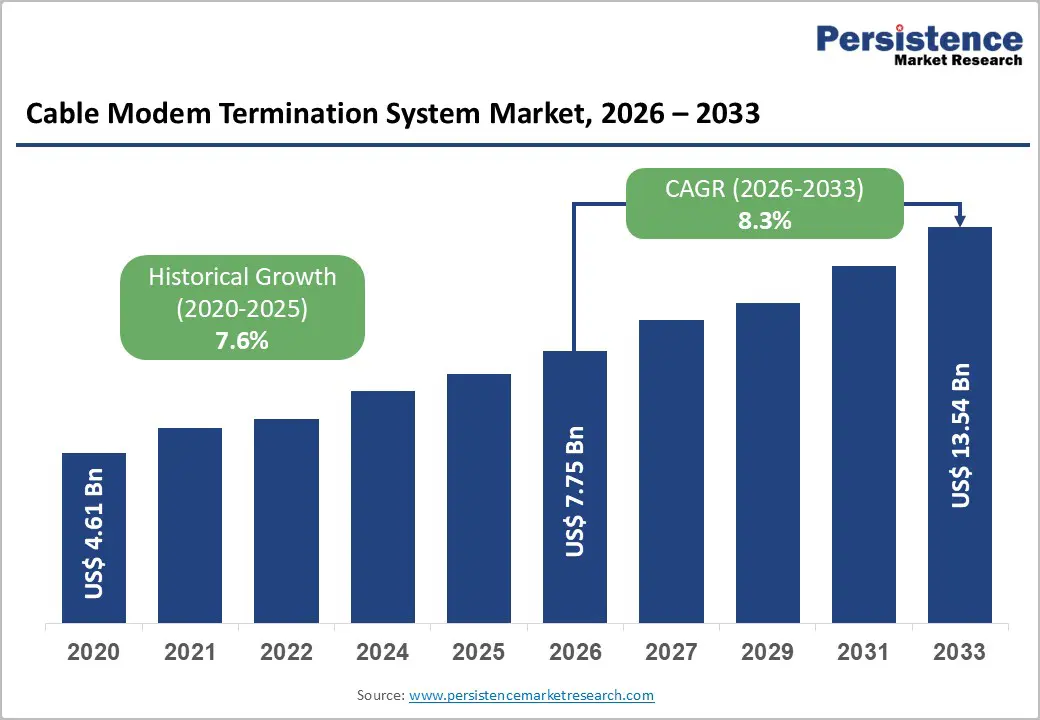

The global Cable Modem Termination System (CMTS) Market size is likely to be valued at US$ 7.75 billion in 2026 and is projected to reach US$ 13.54 billion by 2033, growing at a CAGR of 8.3% between 2026 and 2033. The market is driven by capital equipment replacement cycles for end-of-life legacy systems, competitive pressure from fiber and 5G deployments necessitating cable network optimization, and regulatory support for broadband infrastructure investment.

Key Industry Highlights:

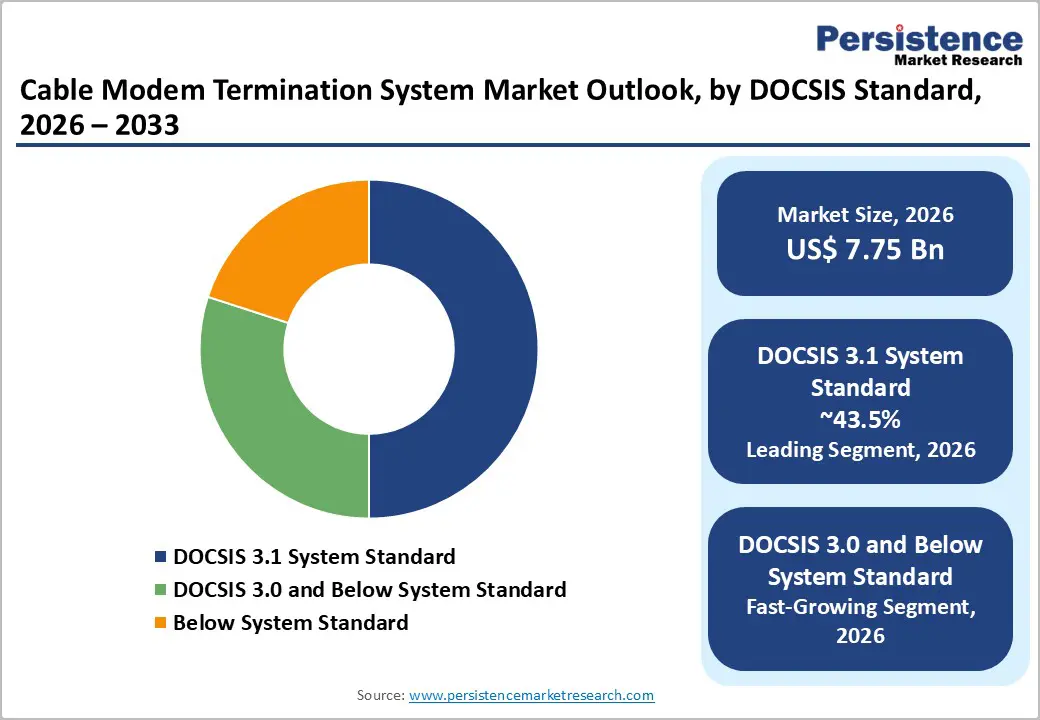

- Leading Technology Standard: DOCSIS 3.1 dominates with 43.5% market share delivering 5-10 Gbps downstream performance, while DOCSIS 3.0 and below represents fastest-growing segment at 6.8% CAGR, driven by legacy equipment refresh cycles across regional operators.

- Dominant CMTS Architecture: Integrated CMTS systems command 62.1% market share through established operational deployment, while Modular CMTS represents the fastest growing at 12% CAGR, driven by Distributed Access Architecture (DAA) adoption and virtualization migration.

- Primary Application Segment: Consumer broadband establishes 64.3% market share with 500+ million global subscribers; Business broadband represents the fastest-growing segment at 14% CAGR, driven by SLA-backed service demand and premium pricing opportunities.

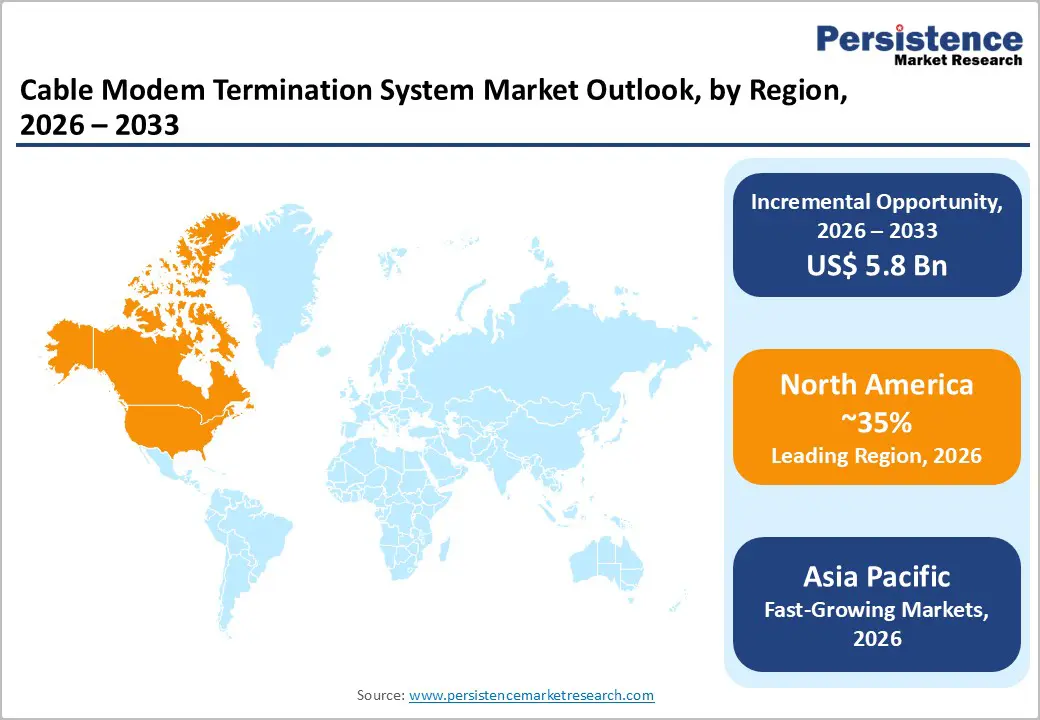

- Regional Market Leadership: North America maintains 35% global market share driven by Comcast, Charter, Cox modernization initiatives; Europe commands 25% share with competitive fiber pressure; Asia Pacific demonstrates fastest regional growth at 13% CAGR, expanding from 20% current share to 28% by 2033.

- Infrastructure Modernization Driver: Major cable operators budgeting US$ 5-10 billion annually for network modernization; 40% of operators planning Remote-PHY/Remote-MACPHY architectures driving virtualized CMTS solution adoption; Virtual CMTS deployment growth 18% annually.

| Key Insights | Details |

|---|---|

|

Cable Modem Termination System Market Size (2026E) |

US$ 7.75 Bn |

|

Market Value Forecast (2033F) |

US$ 13.54 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.3% |

|

Historical Market Growth (CAGR 2020 to 2024) |

7.6% |

Market Dynamics

Drivers - Accelerating Broadband Infrastructure Modernization and DOCSIS Technology Migration

Cable operators globally manage approximately 500+ million subscriber connections with growing demand for multi-gigabit symmetrical broadband services, driving sustained CMTS equipment refresh cycles. DOCSIS 3.1 technology deployment, delivering downstream speeds of 5-10 Gbps versus DOCSIS 3.0 maximum of 1 Gbps, establishes compelling performance justification for capital infrastructure replacement. Legacy CMTS system end-of-life cycles, with original deployments from 2005-2015 reaching 15–20-year operational limits, necessitate replacement equipment procurement across major cable operators, including Comcast, Charter Communications, and Cox Communications.

Vendor migration pressures, with original CMTS suppliers such as Scientific Atlanta and Motorola operating or consolidating, force operators to select new platform providers, including Cisco, Casa Systems, and Harmonic. Investment capital allocation, with major cable operators budgeting US$ 5-10 billion annually for network modernization, establishes a sustained market demand driver.

Consumer Demand for Gigabit-Class Broadband and Competitive Pressure from Alternative Providers

Consumer broadband consumption patterns, with average household data consumption exceeding 300 GB monthly and peak demand reaching 500+ GB during peak hours, necessitate network infrastructure capable of delivering consistent multi-gigabit performance. Streaming video services, including Netflix 4K (25 Mbps), Disney+ (15 Mbps), and emerging 8K offerings (50+ Mbps), drive household speed requirements that exceed 300 Mbps for concurrent streaming. Fiber overbuilds by competitors, with AT&T, Verizon, and Google Fiber deploying fiber-to-home across 15-20 million premises annually, create a competitive imperative for cable operators to maintain service speed parity.

5G wireless competition, with fixed wireless access (FWA) providers deploying gigabit-class residential broadband at aggressive pricing, compels cable network optimization to preserve market share. Work-from-home persistence, with 35% of the workforce operating remotely 2-3 days weekly, establishes sustained demand for reliable high-speed home connectivity.

Restraints - High Capital Equipment Costs and Complex Network Migration Requirements

CMTS platform acquisition costs, ranging from US$ 500,000 to US$5,000,000+ per system, depending on subscriber capacity (100K-1M subscribers), pose significant capital barriers for independent and smaller cable operators. Network migration complexity, requiring service interruption minimization while transitioning subscriber connections across legacy and new infrastructure, extends implementation timelines to 12-24 months. Redundancy requirements, necessitating dual CMTS deployment for fault tolerance and service continuity, effectively double per-location capital expenditure.

Legacy infrastructure dependencies, with operators managing heterogeneous equipment ecosystems spanning 15+ years of technology evolution, create integration complexity, increasing deployment costs 20%. Technical skills requirements, necessitating specialized DOCSIS/network engineering expertise increasingly scarce in the labor market, increase implementation and operational costs. Competitive pricing pressure, with CMTS solution providers competing aggressively on price while maintaining service quality, constrains vendor profitability and R&D investment.

Regulatory Uncertainty and Cybersecurity Compliance Burden

FCC network modernization regulations, including potential requirements for IPv6 adoption and increased security standards, establish uncertain compliance timelines that affect deployment planning. Cybersecurity threat landscape, with cable infrastructure representing critical national infrastructure attracting increasing malicious attention, necessitates sophisticated security architecture, adding 15-20% to implementation costs. Data privacy regulations, including GDPR and state-level broadband privacy requirements, establish compliance obligations affecting system design and operational procedures.

Supply chain concentration risks, with limited suppliers controlling the CMTS platform market and critical components, create vulnerability to supply disruptions. Intellectual property complexity, with DOCSIS standards requiring licensing arrangements with CableLabs and technology providers, increases operational costs and legal complexity. Legacy technology support requirements, with operators needing to maintain aging DOCSIS 3.0 and earlier infrastructure supporting subscriber populations while deploying DOCSIS 3.1, create operational overhead.

Opportunity - Distributed Access Architecture (DAA) and Remote PHY Deployment Expansion

Distributed Access Architecture deployment, including Remote-PHY and Remote-MACPHY architectures, represents a distinct market opportunity addressing cable operators' desires to modernize aging HFC network infrastructure. Remote-PHY node deployment, enabling distributed PHY processing at network edge rather than centralized headend, supports fiber-deep architectures reducing coaxial cable reliance. Market opportunity estimates suggest DAA-compatible CMTS solutions will expand from US$ 2-3 billion (2026) to US$ 5 billion (2033), representing 12% CAGR substantially exceeding overall market growth.

Service group density improvements, with distributed architectures supporting 3-4x greater subscriber density versus legacy centralized models, enable spectrum efficiency, maximizing existing cable plant investment. Fiber integration advantages, enabling seamless evolution toward all-fiber architectures through incremental fiber deployment rather than complete network overbuilding, establish compelling business case.

Edge Computing and Network Slicing for Business Services

Network slicing capabilities, enabling segregated virtual networks that support differentiated service levels for business customers, represent an emerging market opportunity that addresses enterprise broadband demand. Business-class broadband deployments, with SLA-backed service commitments requiring 99.99% availability and sub-10ms latency, enable premium pricing of 3-5x consumer broadband rates.

A multi-tenant network architecture, supporting multiple business customers on a shared infrastructure with security isolation, improves operator asset utilization and profitability. Market opportunity estimates suggest business broadband segment expansion from US$ 1.5-2 billion (2026) to US$ 4-5 billion (2033), representing 15% CAGR substantially exceeding consumer segment growth. Edge computing integration, enabling content delivery network (CDN) edge node placement at network access points, creates new revenue opportunities.

Category-wise Analysis

DOCSIS Standard Technology Analysis

DOCSIS 3.1 holds 43.5% market share in the CMTS technology segment, driven by widespread adoption among major cable operators and new network deployments. Its performance advantages supporting 5–10 Gbps downstream and 1.7–2 Gbps upstream—provide a strong case for migration from earlier standards. The integration of OFDM improves spectrum efficiency and noise immunity, delivering up to 50% higher capacity than DOCSIS 3.0. Global deployment across 400+ million subscribers, along with strong vendor support from Cisco, Casa Systems, and Harmonic, reinforces ecosystem maturity. Enhanced DOCSIS 3.1 Plus capabilities further extend the technology roadmap.

DOCSIS 3.0 and earlier technologies are the fastest-growing segment at 6% CAGR, driven by legacy system refresh cycles. Aging infrastructure and retrofit upgrades generate sustained demand for replacement hardware, components, and support services ahead of full DOCSIS 3.1 migration.

CMTS Type/Architecture Insights

Integrated CMTS systems hold 62.1% market share, driven by the dominance of traditional single-chassis architectures in established cable networks. By combining DOCSIS processing, video QAM, and Ethernet routing into one platform, integrated CMTS solutions simplify operations and reduce system complexity. A large installed base—accounting for 60–70% of active deployments reflects operator familiarity, proven reliability, and commercial maturity. Strong vendor support and competitive offerings ensure continued availability, while capital efficiency is improved as a single integrated system can replace multiple standalone platforms, lowering upfront deployment costs.

Modular CMTS systems are the fastest-growing segment, expanding at 12% CAGR through 2033. Their ability to independently scale capacity, support distributed deployments, and enable incremental investment improves ROI. Compatibility with virtualization, Remote-PHY, and distributed access architectures positions modular CMTS as a preferred solution for next-generation, cloud-native network upgrades.

Application Insights

Consumer broadband applications account for 64.3% of CMTS demand, driven by the sheer scale of residential subscribers and continuous bandwidth consumption. Over 95% of cable customers rely on broadband services, providing operators with a stable, recurring revenue base. Ongoing household upgrades from 300 Mbps plans to 1 Gbps+ tiers, along with broadband expansion into previously underserved areas, sustain infrastructure investment. Rising data intensity from streaming platforms, where households often run two to three concurrent video services, significantly increases downstream traffic. Online gaming and cloud-based computing further elevate performance requirements, reinforcing CMTS capacity upgrades.

Business broadband is the fastest-growing segment, expanding at 14% CAGR through 2033. Strong SMB presence in cable-served regions, persistent work-from-home trends, and demand for SLA-backed, premium services drive adoption. Advanced business features require enhanced CMTS functionality, supporting differentiated and higher-margin offerings.

Regional market insights

North America Cable Modem Termination System Market Insights

North America commands approximately 35% of the global CMTS market share, valued at approximately US$ 3.7 billion in 2026, with projections approaching US$ 6.5 billion by 2033. The United States represents the dominant regional market contributor, accounting for 80% of the North American market value, driven by Comcast, Charter Communications, and Cox Communications' network modernization initiatives.

Capital infrastructure modernization, with major cable operators budgeting US$ 5-10 billion annually for network upgrades, represents the primary market driver. Subscriber broadband speed demand, with consumer expectations advancing from 300 Mbps to 1+ Gbps, drives CMTS equipment upgrade requirements. Competitive fiber and 5G deployment responses, with operators modernizing networks to maintain service speed parity, establish sustained procurement drivers.

Europe Cable Modem Termination System Market Insights

Europe represents approximately 25% of global CMTS market share, valued at approximately US$ 1.9 billion in 2026. Germany, United Kingdom, France, and Spain collectively represent 75% of European market value, reflecting established cable operator infrastructure and broadband market maturity.

DOCSIS 3.1 technology migration, with European cable operators modernizing legacy infrastructure to compete with fiber deployments, represents the primary market driver. Fiber competition intensity, with Telecom Italia, Orange, and Deutsche Telekom fiber deployments accelerating, creates network modernization imperative. Government broadband targets, including EU connectivity goals requiring 1 Gbps availability in all populated areas, drive cable operator infrastructure investment.

Asia Pacific Cable Modem Termination System Market Trends

Asia Pacific demonstrates robust growth dynamics, commanding approximately 20% market share with projections increasing to 28% by 2033. The region valued at approximately US$ 1.2 billion in 2026 is anticipated to reach US$ 3-4 billion by 2033, representing the fastest-growing regional market with an estimated CAGR of 13%.

Cable broadband network expansion, driven by operators establishing or expanding footprints in tier-2/tier-3 cities across India, the Philippines, and Southeast Asia, represents the primary regional differentiator. Consumer broadband demand growth, with middle-class digital adoption exceeding 30% annually in emerging markets, establishes rapid subscriber and bandwidth growth.

Competitive Landscape

The global CMTS market demonstrates moderate consolidation with major telecommunications equipment manufacturers and specialized cable access solution providers maintaining dominant competitive positions. The top 6 suppliers, including Cisco Systems, Casa Systems, Harmonic, CommScope, Huawei Technologies, and ARRIS Group, collectively control approximately 55% of global market share, reflecting incumbent advantages, technology differentiation, and established operator relationships.

Market structure reflects bifurcation between diversified telecom equipment vendors (Cisco) leveraging broad infrastructure relationships and specialized cable broadband solution providers (Casa Systems, Harmonic) emphasizing focused technology expertise.

Key Developments

- In July 2024, Commscope signed an agreement to sell its Outdoor Wireless Network (OWN) unit and its Distributed Antenna System (DAS) business to Amphenol Corp. for USD 2.1 billion. This transaction offers the business an increased focus and further fortifies its CommScope NEXT significance with its enduring segments and business units.

- In May 2024, Vecima Networks Inc. acquired AXING AG to provide Entra DAA solutions to cable operatives in Germany. The partnership will significantly improve the offering of state-of-the-art broadband HFC access systems, and clients will benefit from leading products and strong support.

- In May 2024, Comcast announced that it has reduced the electricity to distribute information across its network by 40% over the last few years. Thus, these cloud-based technologies drive efficiency via real-time performance visibility and provide a service that is better for both customers and the planet.

Companies Covered in Cable Modem Termination System Market

- Casa Systems

- Arris International Limited

- Cisco System Inc.

- Nokia Corporation

- Harmonic Inc.

- Broadcom Inc.

- Huawei Technologies Co. Ltd

- Chongqing Jinghong Hi-tech Co. Ltd

- Juniper Networks Inc.

- Blonder Tongue Laboratories Inc.

- Others Key Players

Frequently Asked Questions

The Cable Modem Termination System market is estimated to be valued at US$ 7.75 Bn in 2026.

The key demand driver for the Cable Modem Termination System (CMTS) market is the surging demand for high-speed broadband and multi-gigabit data traffic over cable networks.

In 2026, the North America region will dominate the market with an exceeding 35% revenue share in the global Cable Modem Termination System market.

Among the DOCSIS Standard, DOCSIS 3.1 System Standard holds the highest preference, capturing beyond 43.5% of the market revenue share in 2026, surpassing other DOCSIS Standard.

The key players in Cable Modem Termination System are Casa Systems, Arris International Limited, Cisco System Inc., Nokia Corporation and Harmonic Inc.