- Executive Summary

- Global BOPP Films Packaging Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Tobacco Industry Overview

- Global Food and Beverage Industry Overview

- Forecast Factors – Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 – 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

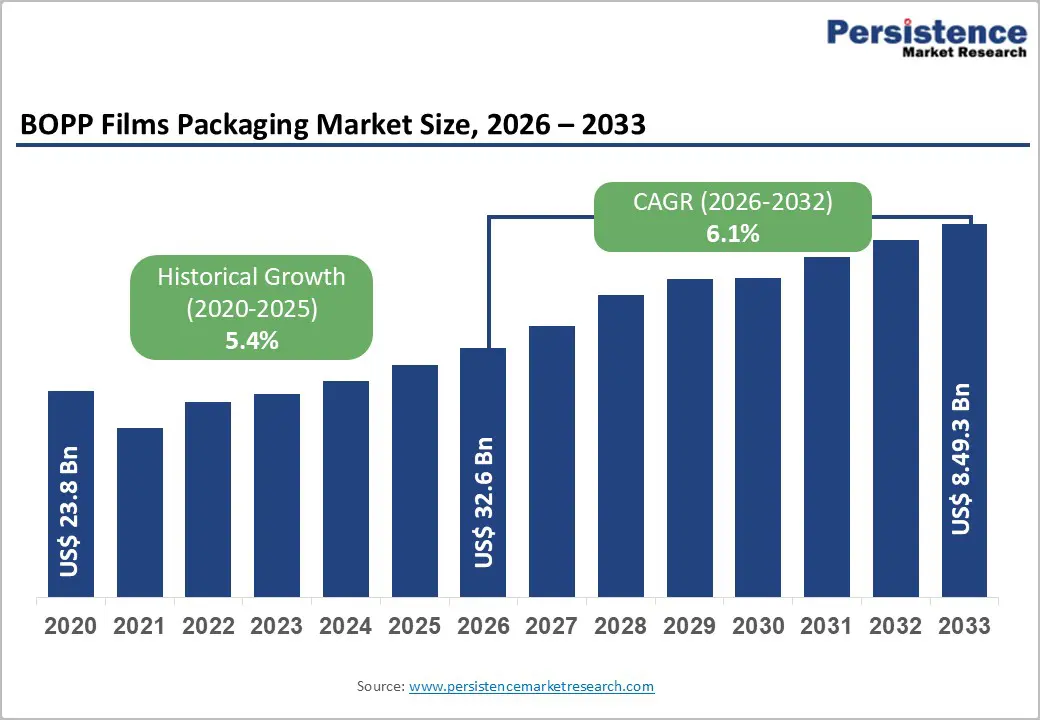

- Global BOPP Films Packaging Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

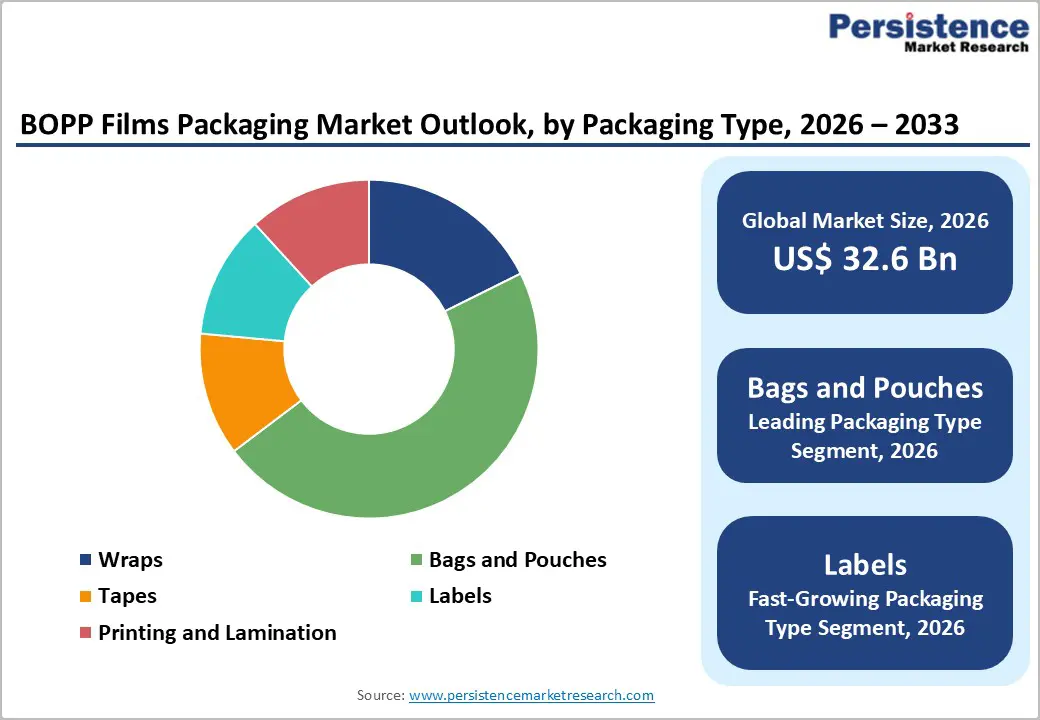

- Global BOPP Films Packaging Market Outlook: Packaging Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Packaging Type, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Packaging Type, 2026-2033

- Wraps

- Bags and Pouches

- Tapes

- Labels

- Printing and Lamination

- Market Attractiveness Analysis: Packaging Type

- Global BOPP Films Packaging Market Outlook: End Use

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by End Use, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by End Use, 2026-2033

- Food

- Meat

- Fresh Produce

- Confectionery

- Beverage

- Personal Care & Cosmetics

- Pharmaceuticals

- Others

- Coffee & Tea

- Tobacco Packaging

- Electrical & Electronics

- Industrial

- Other foods (chips, biscuits, & cereals)

- Food

- Market Attractiveness Analysis: End Use

- Global BOPP Films Packaging Market Outlook: Thickness

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Thickness, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Thickness, 2026-2033

- Below 15 micron

- 15 to 30 micron

- 30 to 45 micron

- Above 45 micron

- Others

- Market Attractiveness Analysis: Thickness

- Global BOPP Films Packaging Market Outlook: Production Process

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Production Process, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Production Process, 2026-2033

- Tenter

- Tubular

- Market Attractiveness Analysis: Production Process

- Global BOPP Films Packaging Market Outlook: Industry

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Industry, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Industry, 2026-2033

- I1

- I2

- Market Attractiveness Analysis: Industry

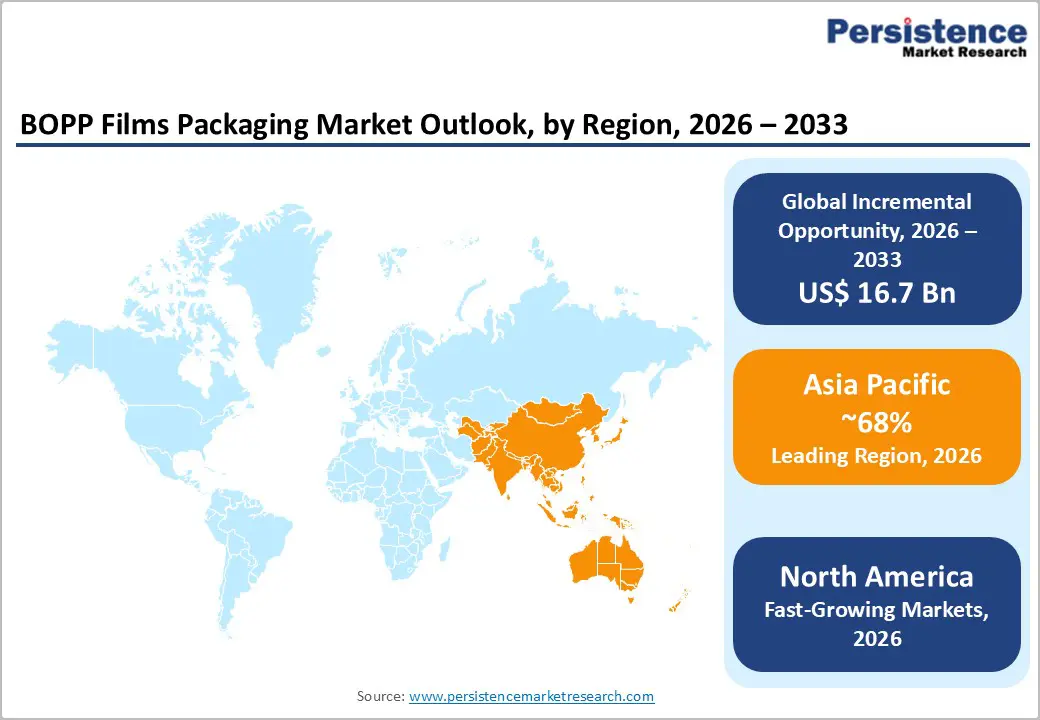

- Global BOPP Films Packaging Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America BOPP Films Packaging Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Packaging Type, 2026-2033

- Wraps

- Bags and Pouches

- Tapes

- Labels

- Printing and Lamination

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by End Use, 2026-2033

- Food

- Meat

- Fresh Produce

- Confectionery

- Beverage

- Personal Care & Cosmetics

- Pharmaceuticals

- Others

- Coffee & Tea

- Tobacco Packaging

- Electrical & Electronics

- Industrial

- Other foods (chips, biscuits, & cereals)

- Food

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Thickness, 2026-2033

- Below 15 micron

- 15 to 30 micron

- 30 to 45 micron

- Above 45 micron

- Others

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Production Process, 2026-2033

- Tenter

- Tubular

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Industry, 2026-2033

- I1

- I2

- Europe BOPP Films Packaging Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Packaging Type, 2026-2033

- Wraps

- Bags and Pouches

- Tapes

- Labels

- Printing and Lamination

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by End Use, 2026-2033

- Food

- Meat

- Fresh Produce

- Confectionery

- Beverage

- Personal Care & Cosmetics

- Pharmaceuticals

- Others

- Coffee & Tea

- Tobacco Packaging

- Electrical & Electronics

- Industrial

- Other foods (chips, biscuits, & cereals)

- Food

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Thickness, 2026-2033

- Below 15 micron

- 15 to 30 micron

- 30 to 45 micron

- Above 45 micron

- Others

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Production Process, 2026-2033

- Tenter

- Tubular

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Industry, 2026-2033

- I1

- I2

- East Asia BOPP Films Packaging Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Packaging Type, 2026-2033

- Wraps

- Bags and Pouches

- Tapes

- Labels

- Printing and Lamination

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by End Use, 2026-2033

- Food

- Meat

- Fresh Produce

- Confectionery

- Beverage

- Personal Care & Cosmetics

- Pharmaceuticals

- Others

- Coffee & Tea

- Tobacco Packaging

- Electrical & Electronics

- Industrial

- Other foods (chips, biscuits, & cereals)

- Food

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Thickness, 2026-2033

- Below 15 micron

- 15 to 30 micron

- 30 to 45 micron

- Above 45 micron

- Others

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Production Process, 2026-2033

- Tenter

- Tubular

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Industry, 2026-2033

- I1

- I2

- South Asia & Oceania BOPP Films Packaging Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Packaging Type, 2026-2033

- Wraps

- Bags and Pouches

- Tapes

- Labels

- Printing and Lamination

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by End Use, 2026-2033

- Food

- Meat

- Fresh Produce

- Confectionery

- Beverage

- Personal Care & Cosmetics

- Pharmaceuticals

- Others

- Coffee & Tea

- Tobacco Packaging

- Electrical & Electronics

- Industrial

- Other foods (chips, biscuits, & cereals)

- Food

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Thickness, 2026-2033

- Below 15 micron

- 15 to 30 micron

- 30 to 45 micron

- Above 45 micron

- Others

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Production Process, 2026-2033

- Tenter

- Tubular

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Industry, 2026-2033

- I1

- I2

- Latin America BOPP Films Packaging Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Packaging Type, 2026-2033

- Wraps

- Bags and Pouches

- Tapes

- Labels

- Printing and Lamination

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by End Use, 2026-2033

- Food

- Meat

- Fresh Produce

- Confectionery

- Beverage

- Personal Care & Cosmetics

- Pharmaceuticals

- Others

- Coffee & Tea

- Tobacco Packaging

- Electrical & Electronics

- Industrial

- Other foods (chips, biscuits, & cereals)

- Food

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Thickness, 2026-2033

- Below 15 micron

- 15 to 30 micron

- 30 to 45 micron

- Above 45 micron

- Others

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Production Process, 2026-2033

- Tenter

- Tubular

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Industry, 2026-2033

- I1

- I2

- Middle East & Africa BOPP Films Packaging Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Packaging Type, 2026-2033

- Wraps

- Bags and Pouches

- Tapes

- Labels

- Printing and Lamination

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by End Use, 2026-2033

- Food

- Meat

- Fresh Produce

- Confectionery

- Beverage

- Personal Care & Cosmetics

- Pharmaceuticals

- Others

- Coffee & Tea

- Tobacco Packaging

- Electrical & Electronics

- Industrial

- Other foods (chips, biscuits, & cereals)

- Food

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Thickness, 2026-2033

- Below 15 micron

- 15 to 30 micron

- 30 to 45 micron

- Above 45 micron

- Others

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Production Process, 2026-2033

- Tenter

- Tubular

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Industry, 2026-2033

- I1

- I2

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Uflex Ltd.

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Cosmo Films Ltd.

- Ampacet Corporation

- Polyplex Corporation Ltd.

- Toray Plastics (America), Inc.

- Manucor S.p.A.

- SRF Limited

- Innovia Films Limited

- Mitsui Chemicals Tohcello, Inc.

- LC Packaging International BV

- Futamura Chemical Co. Ltd.

- Inteplast Group

- Jindal Poly Films Limited

- Chiripal Poly Films Ltd.

- Poligal S.A.

- Uflex Ltd.

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Non-food Packaging

- BOPP Films Packaging Market

BOPP Films Packaging Market Size, Share, and Growth Forecast 2026 – 2033

BOPP Films Packaging Market by Packaging Type (Wraps, Bags and Pouches, Tapes, Labels, and Printing and Lamination), Thickness (Below 15 micron, 15 to 30 micron, 30 to 45 micron, and Above 45 micron), Production Process (Tenter and Tubular), End-user (Food, Coffee & Tea, Beverage, Tobacco Packaging, and Others), and Regional Analysis, 2026-2033

Key Industry Highlights:

- Leading Region: Asia-Pacific dominates the global BOPP Film Packaging market, accounting for over 68% of global production, driven by China's 2.9 million metric tons and India's 1.3 million metric tons in consumption, supported by integrated manufacturing infrastructure, cost competitiveness, and proximity to high-growth consumer markets.

- Fastest Growing Country: India exhibits the fastest growth trajectory at 8.4% CAGR through 2033, propelled by rapid urbanization, expanding middle-class populations, robust FMCG penetration in tier-2 cities, and substantial e-commerce expansion requiring protective flexible packaging solutions.

- Dominant Packaging Type: Bags and Pouches account for approximately 54% of the market share and are favored for food, beverage, and consumer goods applications due to their lightweight construction, superior printability, excellent barrier properties, cost-effectiveness, and 100% recyclability, thereby supporting sustainability objectives.

- Growing Segment: Pharmaceutical packaging is the fastest-growing end-use application, with an approximately 6.8% CAGR through 2033, driven by stringent regulatory requirements for tamper-proof, moisture-resistant packaging that preserves drug efficacy and by the expansion of the healthcare sector globally.

- Key Market Opportunity: The implementation of the EU's Packaging and Packaging Waste Regulation, mandating 100% recyclable packaging by 2030 and requiring a minimum 30% recycled content, catalyzes global brand owners toward mono-material BOPP structures, creating substantial growth opportunities for manufacturers offering certified sustainable solutions.

| Report Attribute | Details |

|---|---|

|

Global BOPP Films Packaging Market Size (2026E) |

US$ 32.6 Bn |

|

Market Value Forecast (2033F) |

US$ 49.3 Bn |

|

Projected Growth CAGR (2026-2033) |

6.1% |

|

Historical Market Growth (2020-2025) |

5.4% |

Market Dynamics

Drivers - Rising Demand for Flexible and Sustainable Packaging

The accelerating shift toward flexible and sustainable packaging formats is a fundamental driver of growth for the BOPP Films Packaging Market, as brand owners and regulators increasingly prioritize material efficiency, recyclability, and carbon footprint reduction. BOPP films offer a superior strength-to-weight ratio, enabling downgauging while maintaining mechanical performance, which directly reduces plastic consumption per unit of packaging. According to UNEP data, flexible packaging solutions can reduce material use by more than 30% relative to rigid alternatives, resulting in lower transportation emissions and improved life-cycle efficiency.

Global regulatory frameworks such as Extended Producer Responsibility (EPR) policies implemented across the EU, U.S., and parts of Asia Pacific are compelling manufacturers to transition toward mono-material packaging structures that are compatible with existing recycling streams. BOPP films, being polypropylene-based, are widely accepted in mechanical recycling systems, making them a preferred solution over complex multi-layer laminates. As sustainability commitments become embedded in FMCG procurement strategies, demand for recyclable BOPP films continues to strengthen across food, beverage, and personal care applications.

Aerospace and Defense Sector Advancement and High-Performance Material Requirements

The sustained global expansion of packaged food and fast-moving consumer goods (FMCG) consumption is another critical driver of demand for BOPP film packaging. Urbanization, rising disposable incomes, and changing dietary habits are increasing reliance on packaged and convenience foods, particularly in emerging economies. According to the FAO, global packaged food production volumes increased by more than 18% between 2018 and 2023, with the Asia-Pacific region accounting for a significant share of the increase in consumption.

BOPP films are extensively used in snack foods, bakery products, confectionery, fresh produce, and frozen foods due to their excellent moisture barrier, optical clarity, and printability. These properties help preserve product freshness, extend shelf life, and enhance shelf appeal in highly competitive retail environments. The rise of private labels and premium food branding has increased demand for high-gloss, high-definition printed films, reinforcing the structural importance of BOPP films within the global FMCG packaging ecosystem.

Restraints - Volatility in Polypropylene Raw Material Prices

Volatility in polypropylene resin prices constitutes a significant restraint on the BOPP film packaging market, directly affecting production costs and profit margins. Polypropylene pricing is closely linked to crude oil and natural gas markets, making it vulnerable to geopolitical tensions, supply disruptions, and energy price fluctuations. According to IEA data, petrochemical feedstock prices experienced volatility exceeding 25% during 2021–2023, creating uncertainty for film producers and converters.

This cost volatility complicates long-term pricing agreements with brand owners and limits manufacturers' ability to pass on cost increases, particularly in price-sensitive food packaging segments. Smaller and mid-sized players are disproportionately impacted, as they lack backward integration or hedging capabilities. As a result, raw material volatility continues to constrain profitability and investment planning, especially in emerging markets where price sensitivity is high.

Increasing Regulatory Scrutiny on Plastic Packaging

Despite being recyclable, BOPP films remain subject to broader regulatory scrutiny targeting plastic packaging waste reduction. Governments across Europe, North America, and Asia are introducing stringent plastic waste management regulations, restrictions on single-use plastics, and mandatory recycling targets. Policies such as the EU Single-Use Plastics Directive and plastic waste regulations enforced by the Government of India have increased compliance requirements for packaging manufacturers.

While these regulations promote recyclability and circular-economy principles, they also increase operational costs associated with labeling, reporting, and waste-recovery obligations. Manufacturers must invest in compliance systems, certification processes, and sustainable material innovation, which can delay product launches and increase capital expenditure. In the short term, regulatory uncertainty and compliance complexity act as a restraining force on market expansion, particularly for exporters operating across multiple jurisdictions.

Opportunities - Technological Advancements in High-Barrier and Specialty Films

Innovation in BOPP film manufacturing processes enables access to premium market segments that require superior performance characteristics. Advanced production technologies, including sequential and simultaneous stretching, enhance clarity, barrier properties, and printability to meet evolving application demands. The development of outstanding barrier metallized BOPP films specifically engineered for snack foods, confectionery, and beverage packaging addresses market requirements for extended shelf life.

Uflex Limited recently launched the 'B-UUB-M' Outstanding Barrier Metallized BOPP Film targeting dry fruits, chips, snacks, biscuits, cookies, and confectionery applications. Industry initiatives by companies like PureCycle Technologies, advancing industrial BOPP film trials using recycled resin, demonstrate a commitment to circular economy principles. The successful commissioning of Cosmo First's new BOPP line in Aurangabad, Maharashtra with capital expenditure exceeding US$ 46.76 million and an annual capacity of 81,200 MT, exemplifies ongoing capacity expansion responding to robust demand fundamentals.

Rapid Growth of E-commerce and Secondary Packaging

The rapid expansion of global e-commerce and direct-to-consumer retail models is creating new demand avenues for BOPP films, particularly in secondary and protective packaging applications. According to UNCTAD, global e-commerce shipments increased by more than 70% between 2019 and 2024, driven by digital retail penetration and shifting consumer purchasing behavior. BOPP films are increasingly used in protective wraps, tamper-evident packaging, and branded shipping solutions due to their puncture resistance, flexibility, and print quality.

As brands seek lightweight, durable, and cost-effective packaging solutions for logistics-intensive operations, BOPP films offer a compelling value proposition. The rise of subscription-based food and personal care services is reinforcing demand for consistent, high-performance packaging materials that ensure product integrity during transit. This structural shift toward e-commerce-led distribution is expected to sustain long-term demand growth for BOPP films.

Category-wise Insights

Product Type Analysis

Bags and Pouches dominate the BOPP films packaging market, commanding approximately 54% market share due to their exceptional versatility across food, beverage, and consumer goods applications. This segment's leadership reflects fundamental advantages, including lightweight construction that reduces transportation costs, superior printability that enables premium brand presentation, and excellent barrier properties that extend product shelf life. According to industry data, bags and pouches made from BOPP film are experiencing accelerated adoption in ready-to-eat snack, confectionery, and fresh produce packaging.

The Flexible Packaging Association reports that food packaging accounts for 50% of flexible packaging shipments, with BOPP bags offering cost-effectiveness and 100% recyclability. Technical innovations, including resealable zippers, tamper-evident features, and breathable valve technologies, enhance functionality. The segment benefits from growing consumer preference for convenient, portion-controlled packaging aligned with on-the-go consumption patterns. Manufacturing efficiency on modern form-fill-seal equipment further drives economic attractiveness for brand owners seeking to optimize packaging procurement costs while maintaining product integrity.

Thickness Insights

The 15-to-30-micron thickness segment represents the market's largest category, capturing approximately 36% of global consumption due to an optimal balance between performance and cost-efficiency. Films within this thick range deliver excellent stiffness for machinability on high-speed packaging lines while maintaining sufficient flexibility for pouch and wrapper applications. This segment dominates food packaging applications, including snack food pouches, bakery wrapping, and lamination structures. Industry data indicate that more than 5.7 million metric tons of BOPP films in the 15–30-micron range were used in 2024, with demand driven by China, India, and Brazil.

The segment's popularity reflects manufacturers' preference for films offering reliable seal integrity, consistent processing characteristics, and economical material usage. Advanced production technologies enable precise thickness control, ensuring uniform optical properties and barrier performance. The range accommodates both transparent and metallized variants suitable for diverse packaging requirements from fresh produce with anti-fog properties to high-barrier chocolate wrappers requiring oxygen protection.

Production Process Insights

The Tenter process dominates BOPP film production, accounting for approximately 85% of global manufacturing capacity due to its superior quality and operational flexibility. This sequential stretching method involves machine direction orientation followed by transverse direction stretching in a tenter frame, enabling precise control over film properties, including thickness, uniformity, optical clarity, and mechanical strength. The tenter process accommodates wider film widths exceeding 10 meters, maximizing production efficiency and material yield. Major capacity expansions globally employ tenter technology, including Oben Holding Group's order for a Brückner 10.4 m BOPP film line in Monterrey, Mexico adding 60,000 tpa capacity upon completion in 2026.

The process facilitates coextrusion of multiple layers, enabling tailored barrier properties, heat-seal characteristics, and optical effects. Leading equipment supplier Brückner Maschinenbau pioneered advancements, including production speeds exceeding 550 m/min achieved on Uflex's Poland facility. The dominance of the tenter process reflects its ability to produce films that meet stringent specifications for food-contact applications while maintaining economic competitiveness across commodity and specialty grades.

End-user Insights

Food packaging is the largest end-use segment, accounting for approximately 63% of global BOPP film consumption. This dominant position stems from BOPP films' superior characteristics, including high transparency allowing product visibility, excellent moisture and oxygen barrier properties preserving freshness, and exceptional clarity enhancing shelf appeal. The segment encompasses diverse applications, including meat packaging, fresh produce wrapping, confectionery pouches, and dry food products such as chips, biscuits, and cereals. Industry statistics indicate that approximately 58% of BOPP films are used in food packaging applications.

The food segment's growth is amplified by urbanization, the expansion of the middle class in Asia-Pacific nations, and rising consumption of packaged convenience foods. Indian snack producers like Haldiram's leverage transparent BOPP films to extend shelf life by up to 20% while boosting product visibility in modern retail displays. The COVID-19 pandemic accelerated demand for hygienic, sealed packaging solutions, further reinforcing BOPP films' position in food applications requiring contamination-free, tamper-evident sealing capabilities.

Regional Insights

North America BOPP Films Packaging Market Trends

The United States maintains market leadership in North America, driven by sophisticated consumer preferences and robust regulatory frameworks governing food-contact materials. The US flexible packaging industry generated US$ 41.5 billion in sales in 2022, according to the flexible packaging association, with food packaging representing 50% of shipments. The market benefits from established recycling infrastructure and corporate sustainability commitments by major brands pursuing recyclable packaging targets. However, polypropylene resin price volatility creates operational challenges, with prices increasing 4-5 cents per pound in early 2025, compelling converters toward vertical integration and sophisticated procurement strategies.

E-commerce growth substantially influences North American demand patterns, with online retail expanding rural delivery networks requiring lightweight, protective mailer films. Innovation ecosystems centered on advanced barrier technologies and recycled content integration characterize the region's competitive landscape. Companies including Inteplast Group operate dedicated BOPP film production lines for fresh-cut produce markets, offering specialized anti-fog properties and controlled oxygen transmission rates. The regulatory environment emphasizes FDA compliance for food-contact applications while encouraging the development of mono-material structures, facilitating mechanical recycling. North America's mature market status drives focus on value-added specialty grades, including matte, pearlized, and high-barrier metallized films.

Europe BOPP Films Packaging Market Trends

European markets are fundamentally shaped by the Packaging and Packaging Waste Regulation (PPWR) effective February 2025, which mandates all packaging achieve recyclability by 2030. This regulatory framework catalyzes substantial investments in mono-material BOPP structures and design-for-recycling innovations across Germany, UK, France, and Spain. The regulation establishes recyclability performance grades A, B, and C, with packaging below 70% recyclability prohibited from 2030, escalating to 80% threshold by 2038. European brand owners accelerate adoption of BOPP films by meeting stringent environmental criteria while maintaining barrier performance for premium food products.

Germany's position as a leading tobacco-consuming nation supports continued BOPP films demand for cigarette packaging applications requiring specialized barrier properties. The region witnessed strategic capacity additions including Innovia Films' installation of an 8.8-meter-wide multilayer co-extrusion line near Leipzig with 36,000 tons annual capacity producing thin-gauge label films responding to sustainable product demands. The PPWR mandates minimum recycled content of 30% for PET contact-sensitive packaging and 10% for other plastic packaging by 2030, driving development of certified recycled BOPP films. European manufacturers pursue ISCC Plus certification validating sustainable sourcing. In May 2024, Plastchim-T's acquisition of Manucor boosted combined BOPP capacity to 200,000 tpa, strengthening competitive positioning across European markets.

Asia Pacific BOPP Films Packaging Market Trends

Asia Pacific dominates global BOPP films production and consumption, accounting for over 68% of worldwide output led by China and India's expansive manufacturing infrastructure. China operates more than 90 operational BOPP lines with consumption exceeding 2.9 million metric tons in 2024, while India follows with 1.3 million metric tons fueled by rising FMCG penetration in tier-2 cities. The region's competitive advantages include integrated polypropylene resin production, low labor costs, and proximity to high-growth consumer markets. Regional manufacturers leverage economies of scale enabling aggressive export strategies, with Chinese BOPP films exports surpassing 980,000 metric tons in 2024.

Rapid urbanization and expanding middle-class populations across China, Japan, India, and ASEAN nations drive packaged food consumption, supporting BOPP films demand. India's polymer consumption growth of 8.5% in FY 2024-25 underscores robust market fundamentals. Strategic capacity expansions characterize regional dynamics, including JPFL Films Private Limited's announcement of a new 60,000 tons per annum BOPP film production unit in India with US$ 30 million investment. Jindal Poly Films' Maharashtra facility maintains capacities of 294,000 t/y BOPP, 170,000 t/y BOPET, and 33,000 t/y CPP. Regional manufacturers increasingly focus on specialty grades including anti-fog films for fresh produce and high-barrier metallized variants for confectionery applications. Southeast Asian markets, including Vietnam, Indonesia, and Bangladesh, witness continued capacity additions responding to food processing industry expansion and e-commerce proliferation.

Competitive Landscape

The BOPP films packaging market exhibits moderate consolidation with the top 10 companies commanding approximately 40% of global capacity, while numerous regional players compete across commodity and specialty segments. Industry structure reflects a balance between large multinational corporations operating integrated production facilities across multiple continents and specialized converters focusing on value-added grades serving niche applications. Competitive strategies emphasize capacity expansion in high-growth regions, vertical integration securing polypropylene feedstock supply, and research and development investments advancing sustainable materials and enhanced barrier technologies.

Key differentiators include production capabilities spanning diverse film widths and thick ranges, technical expertise in coextrusion and metallization processes, and established customer relationships with major food and consumer goods brands. Market leaders pursue geographic diversification mitigating regional demand fluctuations while smaller players differentiate through rapid response times, customization capabilities, and localized technical support. The competitive environment intensifies as overcapacity in certain regions, particularly legacy Chinese assets operating below optimal utilization, creates pricing pressures compelling operational efficiency improvements and consolidation activities.

Key Developments:

- In June 2025, Cosmo First (Cosmo Films Ltd.) commissioned a new BOPP film line at its Aurangabad, Maharashtra facility with capital expenditure exceeding US$ 46.76 million. The line features cutting-edge technology with annual rated capacity of 81,200 MT, boosting the company's yearly BOPP capacity by approximately 40% to 2,77,000 MT.

- In February 2025, Oben Holding Group ordered a Brückner 10.4 m BOPP film line for a new plant in Monterrey, Mexico, a project that will add 60,000 tpa of capacity upon start-up in 2026, strengthening regional production capabilities.

- In April 2024, South Mill Champs and Sprouts Farmers Market introduced bamboo tills flow-wrapped with perforated BOPP film for fresh mushrooms, improving shelf life while supporting sustainability goals for recyclable, fiber-based packaging aligned with consumer preferences.

Companies Covered in BOPP Films Packaging Market

- Uflex Ltd.

- Cosmo Films Ltd.

- Ampacet Corporation

- Polyplex Corporation Ltd.

- Toray Plastics (America), Inc.

- Manucor S.p.A.

- SRF Limited

- Innovia Films Limited

- Mitsui Chemicals Tohcello, Inc.

- LC Packaging International BV

- Futamura Chemical Co. Ltd.

- Inteplast Group

- Jindal Poly Films Limited

- Chiripal Poly Films Ltd.

- Poligal S.A.