- Beverages

- Beauty Drinks Market

Beauty Drinks Market Size, Share, and Growth Forecast, 2026 – 2033

Beauty Drinks Market by Ingredients Type (Vitamins & Minerals, Others), Functional Benefits (Anti-Aging, Detoxification, Others), Distribution Channel (Specialty Stores, Drug Stores and Pharmacies, Online Retail Stores, Others), and Regional Analysis for 2026 – 2033

Beauty Drinks Market Size and Trends Analysis

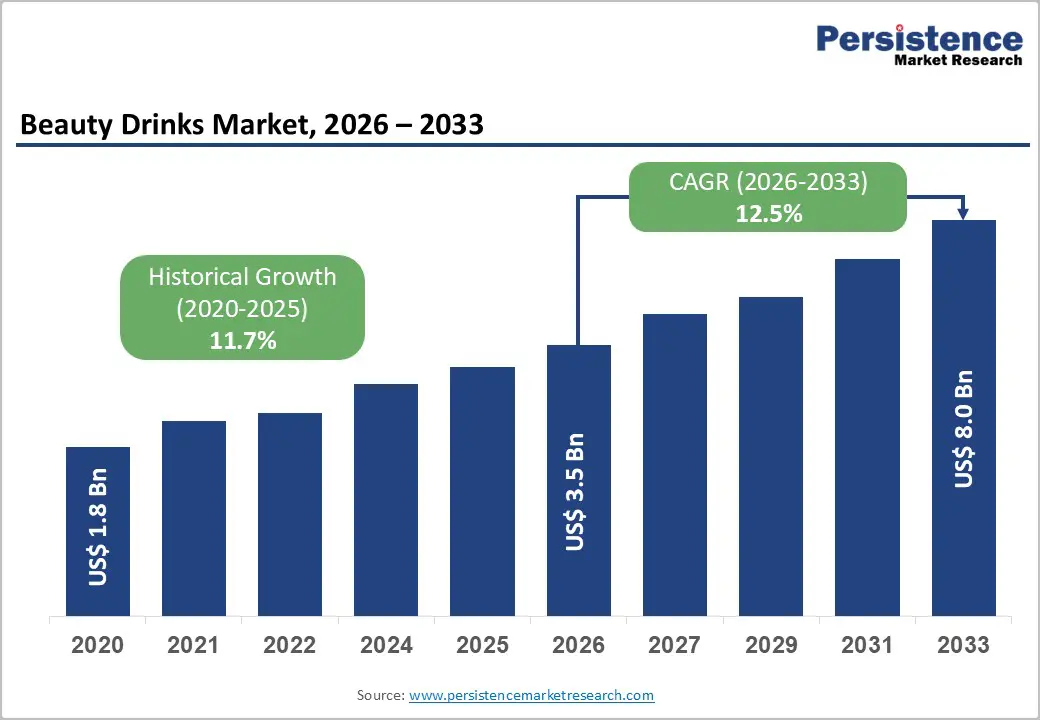

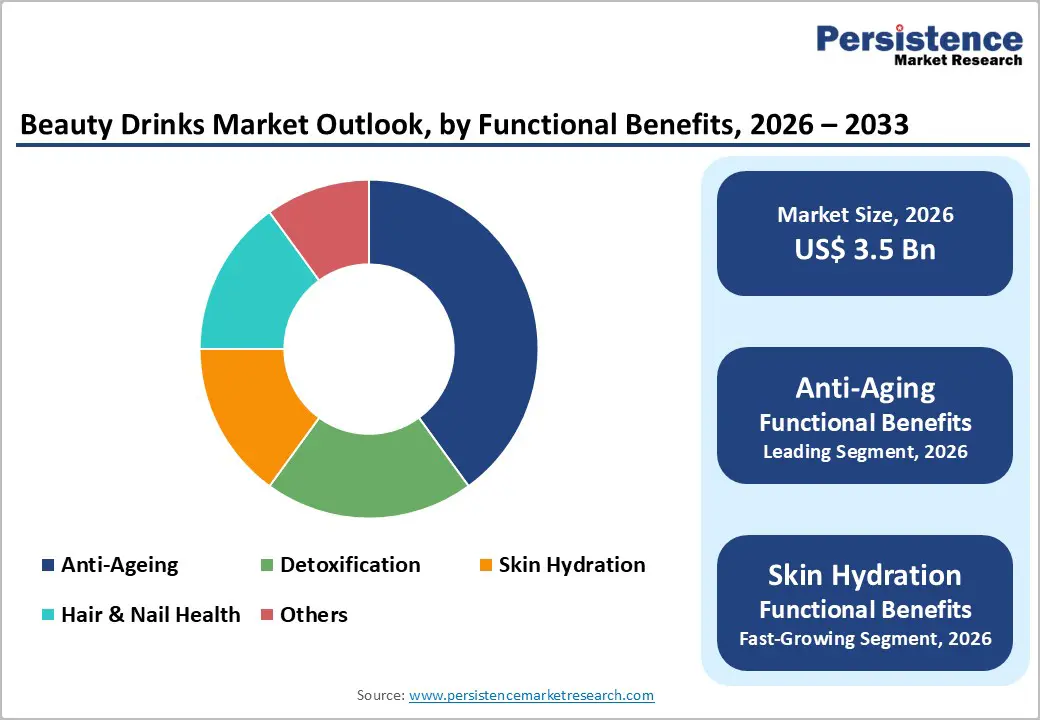

The global beauty drinks market size is likely to be valued at US$3.5 billion in 2026, and is expected to reach US$8.0 billion by 2033, growing at a CAGR of 12.5% during the forecast period from 2026 to 2033, driven by the increasing prevalence of beauty-from-within trends, rising consumer preference for ingestible skincare and haircare solutions, and growing demand for convenient, functional beverages with proven anti-aging and skin-hydration benefits.

Growing demand for collagen-based and glutathione-enriched beauty drinks, especially through online retail and specialty stores, is accelerating adoption across distribution channels. Advances in low-sugar, clean-label formulations and clinically backed ingredient synergies are further boosting uptake by offering better taste, efficacy, and regulatory acceptance. Increasing recognition of beauty drinks as a critical daily ritual for proactive skin, hair, and nail health in emerging wellness and nutricosmetics markets remains a major driver of market growth.

Key Industry Highlights:

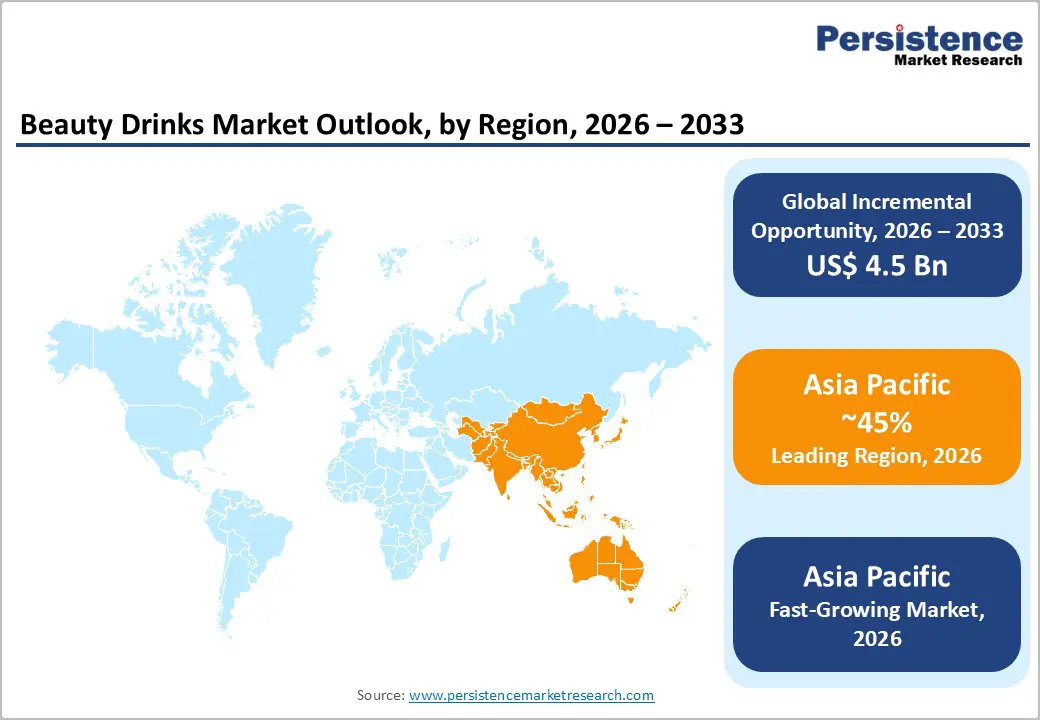

- Leading Region: Asia Pacific, expected to account for 45% market share in 2026, driven by high beauty consciousness, strong K-beauty/J-beauty influence, and strong demand in Japan, South Korea, and China.

- Fastest-growing Region: Asia Pacific, fueled by rapid middle-class expansion, explosive e-commerce growth, and increasing acceptance of ingestible beauty in India and Southeast Asia.

- Dominant Ingredients Type: Collagen, to hold approximately 52% of the market share, as it remains the most clinically validated and widely marketed beauty-from-within ingredient.

- Leading Functional Benefits: Anti-aging, contributing nearly 42% of the market revenue, due to the strongest consumer association with visible youth benefits.

| Report Attribute | Details |

|---|---|

|

Beauty Drinks Market Size (2026E) |

US$3.5 Bn |

|

Market Value Forecast (2033F) |

US$8.0 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

12.5 |

|

Historical Market Growth (CAGR 2020 to 2025) |

11.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis: Rising Consumer Shift toward Ingestible Beauty

The rising consumer shift toward ingestible beauty reflects a deeper evolution in how people think about health and appearance. Rather than relying solely on topical products such as creams or serums, today’s consumers increasingly seek beauty solutions from within via supplements, powders, and functional foods that promise benefits for skin, hair, and nails. This trend is driven by a desire for holistic wellness, where beauty is an outcome of overall health rather than an isolated goal.

People are becoming more ingredient-savvy and expect transparency, science-backed claims, and multitasking benefits (e.g., combining hydration, antioxidant support, and gut health). Social influence and self-care culture also play big roles: ingestible beauty fits into daily routines and aligns with the broader personalization of wellness. As lifestyles get busier, convenience matters, and ingestibles offer an easy way to support beauty goals. This shift highlights a deeper consumer belief that internal nourishment can enhance external radiance.

Proactive Skin-Health Routines

Proactive skin-health routines are about anticipating needs rather than reacting to visible issues. Instead of waiting for breakouts, dryness, or irritation to surface, people are now building daily habits that preserve and strengthen skin over time. This mindset treats the skin as a living ecosystem, something to nurture consistently through targeted habits, mindful lifestyle choices, and informed product use.

These routines focus on understanding individual skin characteristics such as sensitivity, barrier strength, and environmental exposure. They combine foundational care, gentle cleansing, hydration, and sun protection with periodic actions such as exfoliation, antioxidant support, and barrier-repair treatments. Nutrition, sleep quality, and stress management are increasingly recognized as essential contributors to skin health, not merely as factors that influence the efficacy of topical creams. This shift reflects a deeper desire for long-term skin resilience rather than quick fixes. People want routines that feel personalized and predictive, helping them maintain a healthy, balanced complexion every day.

Barrier Analysis - High Raw Material Costs

High raw material costs are increasingly shaping production decisions across industries. When the price of essential inputs such as specialized actives in cosmetics, key ingredients in food and beverages, or metals in manufacturing rises, businesses face direct pressure on their profit margins. These costs often climb due to factors such as supply chain disruptions, scarcity of specific natural resources, increased environmental regulations, or higher energy prices that affect extraction and processing.

Producers must then make tough choices: absorb the added expense and reduce profitability, increase prices for customers, reformulate products with cheaper alternatives, or invest in more efficient sourcing strategies. For smaller companies, especially, spikes in raw material costs can strain budgets and slow innovation. This ripple effect can also influence market dynamics, forcing companies to rethink product portfolios, negotiate long-term supply contracts, or explore sustainable substitutes.

Supply-Chain Volatility for Premium Bioactive Ingredients

Supply-chain volatility for premium bioactive ingredients arises when the flow of highly sought-after, performance-driven components becomes unpredictable. These ingredients, often derived from rare botanicals, fermentation processes, or biotech synthesis, depend on complex networks of growers, processors, and specialized manufacturers. Weather extremes, geopolitical tensions, regulatory shifts, and transportation bottlenecks can all disrupt this network, making availability inconsistent and lead times longer.

For brands that position products around efficacy and innovation, unstable access to these bioactives creates planning headaches. They may delay product launches, reformulate on short notice, or pay premiums to secure limited supplies. Smaller suppliers, in particular, struggle to absorb these fluctuations, which can hamper scaling or investment in quality improvements. Consumers expect transparency and efficacy; therefore, substitutions without clear communication can erode trust. In essence, supply-chain volatility for premium bioactive ingredients forces companies to be more agile, strategic, and resilient, building stronger relationships, diversifying sources, and forecasting demand more accurately to maintain performance and brand promise.

Opportunity Analysis - Clinically Backed Combination Formulas

Clinically backed combination formulas represent a shift from single-ingredient products to thoughtfully blended solutions supported by scientific evidence. Instead of offering a single active ingredient at a time, these formulas integrate multiple ingredients that work together to target multiple aspects of a concern, such as hydration, barrier repair, and skin inflammation, while enhancing each other’s effectiveness. What makes them “clinically backed” is that their performance is not just assumed; it is demonstrated through structured testing, such as controlled trials, user studies, or measurable biomarker improvements.

Consumers value these formulas because they want confidence that products will deliver meaningful results without guesswork. When brands invest in solid clinical validation, it reduces trial and error for users, strengthens trust, and differentiates offerings in a crowded market. The combinations are designed to balance potency with safety, minimizing irritation while maximizing benefit.

Subscription-Based DTC Models

Subscription-based direct-to-consumer (DTC) models change how people buy products by turning one-off purchases into ongoing relationships. Instead of shopping each time they run out, customers sign up to receive products automatically at regular intervals—whether monthly skincare sets, health supplements, or household essentials. This model gives consumers convenience and predictability; they do not have to remember to reorder, and they often benefit from perks such as discounts, personalization, or exclusive access.

For brands, subscriptions unlock more stable revenue and deeper customer insight. With recurring orders, companies can forecast demand more accurately, tailor offerings based on usage patterns, and build long-term loyalty rather than constantly chasing new buyers. It also shifts the focus from transactional marketing to ongoing engagement, brands invest more in communication, customization, and value over time.

Category-wise Analysis

Ingredients Type Insights

Collagen is expected to lead the market, holding 52% of the share in 2026, reflecting its broad appeal and versatile benefits. As a structural protein vital for skin elasticity, joint function, and connective tissue strength, collagen resonates with consumers seeking visible results in beauty and overall wellness. Its popularity is boosted by diverse formats, powders, capsules, drinks, and the perception that ingesting collagen supports internal and external health. Brands also highlight sustainability and bioavailability, strengthening consumer trust. Vital Proteins, a widely recognized collagen supplement brand acquired by Nestlé Health Science, has become a market leader with strong consumer demand for its collagen peptides and beauty-from-within products. Its broad product range, powders, capsules, and gummies target skin, hair, nail, and joint health, helping the brand secure a significant share of the global collagen supplement category.

Glutathione is likely to be the fastest-growing ingredient category, as consumers increasingly prioritize internal wellness and visible skin benefits. Its strong antioxidant properties make it appealing for detoxification, immune support, and skin brightness, which drives demand across nutraceuticals, beauty supplements, and cosmeceuticals. Globally, product launches featuring glutathione, especially reduced forms and advanced delivery systems such as liposomal formulations, have surged, reflecting broad market interest and innovation in this space. More than 30% growth in new glutathione products in recent years highlights how quickly it is being adopted compared with traditional antioxidants. Kyowa Hakko Bio Co., Ltd. is a major global producer of premium glutathione, known for its branded Setria® Glutathione ingredient used in supplements and beauty-from-within products. Setria has undergone clinical studies and is widely included in formulations supporting antioxidant protection, skin health, and detoxification, helping drive demand across the nutraceutical and cosmetic segments.

Functional Benefits Insights

Anti-aging is expected to dominate the market, contributing nearly 42% of revenue in 2026, due to an increasing priority on solutions that target visible signs of aging, such as wrinkles, loss of elasticity, and skin texture concerns. This category spans high-demand products from topical serums and creams to ingestible beauty supplements and advanced dermatological treatments, making it one of the largest revenue drivers across both cosmetic and wellness spaces. Growing awareness of preventive self-care, expanding across older and younger demographics focused on long-term skin health, and cross-category innovation all help anti-aging capture a larger share of consumer spending than other segments. The Procter & Gamble Company (P&G), through its Olay Regenerist anti-aging range, remains a top seller in many markets due to its science-driven formulations targeting wrinkles, texture, and elasticity.

Skin hydration is emerging as one of the fastest-growing functional benefits in skincare, as consumers increasingly recognize moisture balance as fundamental to healthy, resilient skin. Modern formulations—particularly lightweight serums, gels, and barrier-strengthening moisturizers—are engineered to deliver deep, long-lasting hydration while seamlessly fitting into daily routines, fueling broad adoption across age groups and skin types. Globally, hyaluronic acid and key humectants such as glycerin and ceramides have become core actives in hydration-focused products, reflecting strong consumer demand for solutions that enhance moisture retention and support the skin’s protective barrier. Neutrogena’s Hydro Boost line (under Kenvue) exemplifies this trend. Products such as the Hydro Boost Hyaluronic Acid Water Gel rank among the world’s top-selling hydration-focused skincare items, consistently driving strong sales in the hydration segment and reinforcing Neutrogena’s leadership in this category.

Regional Insights

North America Beauty Drinks Market Trends

Growth in North America is fueled by the region’s high per-capita spending on nutricosmetics, strong influencer-led product discovery, and widespread awareness of beauty-from-within benefits. Well-established distribution networks in the U.S. and Canada provide robust support for beauty drink programs, ensuring broad accessibility across key segments, including collagen, glutathione, and anti-aging. Rising demand for subscription-based models and convenient, easy-to-integrate formats is further accelerating adoption, as these offerings enhance consumer compliance and reduce reliance on topical-only routines.

Ongoing innovation in beauty drinks, ranging from stable low-sugar formulations and enhanced functional fortification to targeted skin-hydration benefits, is attracting substantial public and private investments. In parallel, government initiatives and consumer education campaigns are encouraging adoption by addressing concerns around synthetic ingredients, aging, and emerging wellness risks, supporting sustained market growth. The increasing emphasis on skin-hydration grading and specialized applications, particularly within anti-aging and related segments, is broadening the scope and applications of beauty drinks.

Europe Beauty Drinks Market Trends

Europe shows significant growth, driven by increasing awareness of the benefits of ingestible beauty, robust regulatory systems, and government-led health & wellness programs. Countries such as Germany, France, the U.K., and Italy have well-established nutraceutical frameworks that support routine consumption of beauty drinks and encourage the adoption of innovative beverage delivery methods. These functional formulations are particularly appealing to anti-aging populations, regulation-conscious consumers, and skin-hydration users, improving outcomes and coverage.

Technological advancements in the development of beauty drinks, such as enhanced fortification, application-specific delivery, and improved clean-label grades, are further enhancing market potential. European authorities are increasingly supporting research and trials for drinks against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, low-sugar options is aligned with the region’s focus on preventive beauty and reducing topical dependency. Public awareness campaigns and promotion drives are expanding reach in both urban and rural areas, while brands are investing in ingredients and novel variants to increase adoption.

Asia Pacific Beauty Drinks Market Trends

Asia-Pacific is projected to dominate and be the fastest-growing market, accounting for 45% of revenue in 2026, driven by rising beauty awareness, expanding government initiatives, and expanding application programs across the region. Countries such as Japan, South Korea, China, and India are actively promoting drinks campaigns to address skin-health growth and emerging ingestible beauty needs. Beauty drinks are particularly attractive in these regions due to their scalable administration, ease of adoption, and suitability for large-scale retail and e-commerce drives in both urban and rural populations.

Technological advancements are enabling the development of stable, effective, and enjoyable beauty drinks that withstand challenging distribution conditions and minimize taste dependence. These innovations are critical for reaching domestic consumers and improving overall category coverage. Growing demand for collagen, glutathione, and anti-aging applications is contributing to market expansion. Public-private partnerships, increased wellness expenditure, and rising investment in research and production capacity for beauty drinks are further accelerating growth. The convenience of drinks delivery, combined with improved efficacy and reduced risk of rejection, positions beauty drinks as a preferred choice.

Competitive Landscape

The global beauty drinks market features competition between established multinational CPG players and emerging premium & regional specialists. In North America and Europe, Nestlé SA (via brands such as Natra) and Vital Proteins LLC lead through strong R&D, distribution networks, and retail partnerships, bolstered by innovative collagen and functional-fortification programs. In Asia Pacific, Shiseido Co. Ltd (The Collagen) and Kinohimitsu advance with localized flavors and high-efficacy claims, enhancing accessibility. Functional fortification delivery boosts visible results, cuts skepticism risks, and enables mass integrations across channels. Strategic partnerships, collaborations, and acquisitions merge expertise, expand portfolios, and speed market penetration. Clean-label formulations solve trust issues, aiding penetration in mainstream wellness areas.

Key Industry Developments

- In May 2025, the MAR Advantage team launched its ready-to-drink (RTD) Athena's Glow Drink, which blends natural ingredients with real benefits for women aged 45+. MAR Advantage had one major goal in mind when creating Athena's Glow Drink: to meet the unique wellness needs of women in their prime who are thriving, health-conscious, and ready for a product that speaks to their lifestyle in a way the industry often overlooks.

- In April 2024, Bizzi launched ready-to-drink coffee-plus-collagen blends in three flavor variants. Health-conscious consumers seeking convenient wellness options are the target audience for three new blends: Coffee + Collagen Signature Blend, Matcha + Collagen Signature Blend, and Coffee + Collagen Vanilla & Turmeric.

Companies Covered in Beauty Drinks Market

- Nestlé SA

- Shiseido Co. Ltd (The Collagen)

- Sappe Public Company Ltd

- Kinohimitsu

- Lacka Foods Ltd

- Hangzhou Nutrition Biotechnology Co., Ltd

- AmorePacific Corp

- Asterism Healthcare

- Revive Collagen

- Bella Berry

- My Beauty & GO

- Rejuvenated Ltd

- Molecule Beverages

- Big Quark

- On-Group Ltd

- Vital Proteins LLC

- DyDo Drin Co.

- Fine Japan Co., Ltd.

Frequently Asked Questions

The global beauty drinks market is projected to reach US$3.5 billion in 2026.

Beauty-from-within trends and demand for ingestible skincare and haircare solutions are key drivers.

The beauty drinks market is poised to witness a CAGR of 12.5% from 2026 to 2033.

Clinically backed combination formulas and subscription-based DTC models are key opportunities.

Nestlé SA, Shiseido Co. Ltd (The Collagen), Vital Proteins LLC, Kinohimitsu, and Revive Collagen are the key players.