- Medical Devices

- Balloon Infusers Market

Balloon Infusers Market Size, Share, and Growth Forecast, 2025 - 2032

Balloon Infusers Market By Material Type (Silicone, Latex), Product Type (Semi-compliant Balloons, Non-compliant Balloons), Application, and Regional Analysis for 2025 - 2032

Balloon Infusers Market Size and Trends Analysis

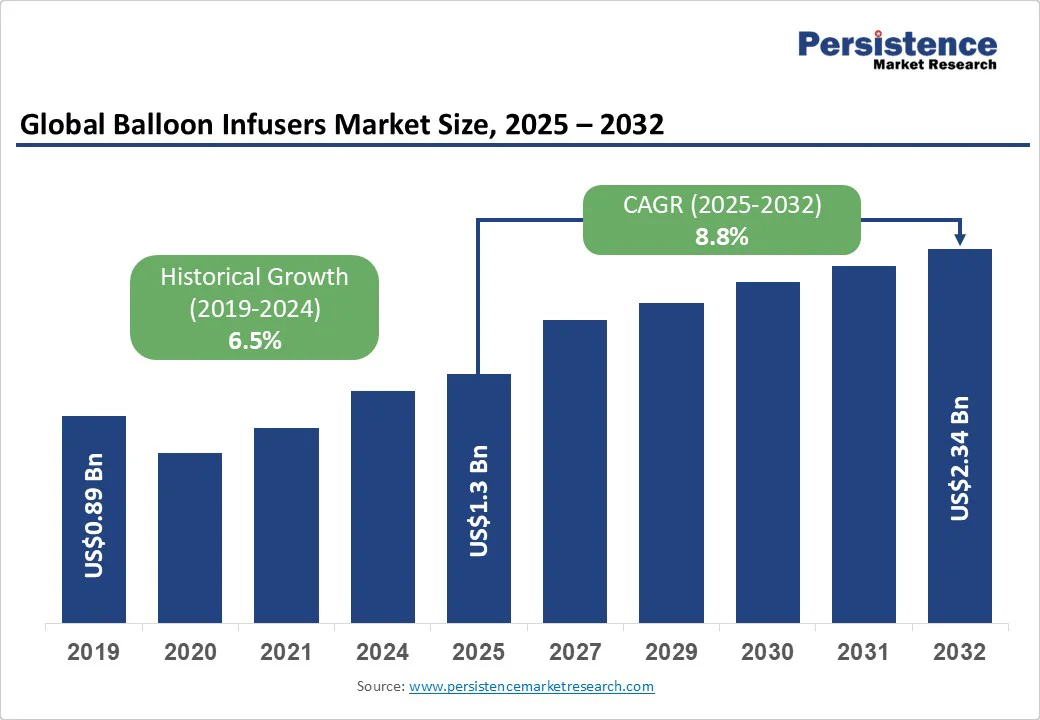

The global balloon infusers market size is likely to be valued at US$1.3 Bn in 2025 and is expected to reach US$2.3 Bn by 2032, growing at a CAGR of 8.8% during the forecast period from 2025 to 2032, due to the rising prevalence of cardiovascular diseases. The emphasis on minimally invasive interventions, coupled with the expansion of healthcare infrastructure in emerging economies, is driving procedural adoption. Increasing hospital budgets for interventional cardiology and the shift toward drug-coated balloon (DCB) compatibility are also contributing significantly to market growth.

Key Industry Highlights:

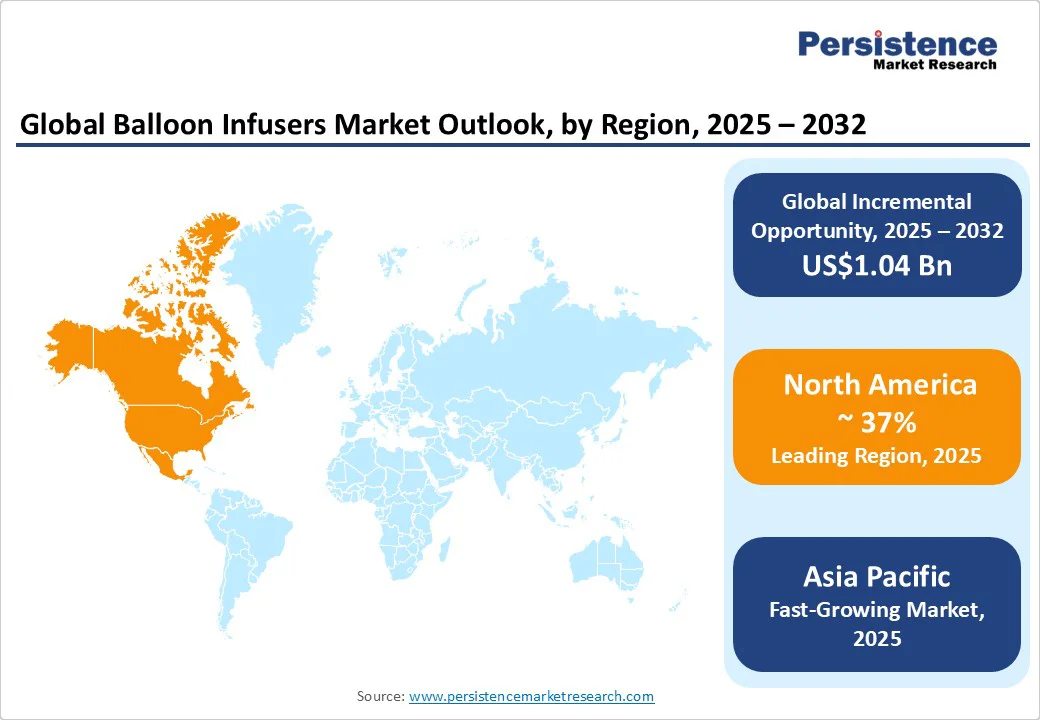

- Leading Region: North America is anticipated to account for 37% of the global market share in 2025, supported by advanced healthcare infrastructure and high adoption of interventional cardiology procedures.

- Fastest-growing Region: Asia Pacific is driven by rising cardiovascular cases in China and India, along with expanding healthcare access.

- Investment Plans: Key manufacturers are investing in polyurethane-based balloon technologies and geographic expansion into emerging Asian markets, particularly India, to capture rising demand for minimally invasive treatments.

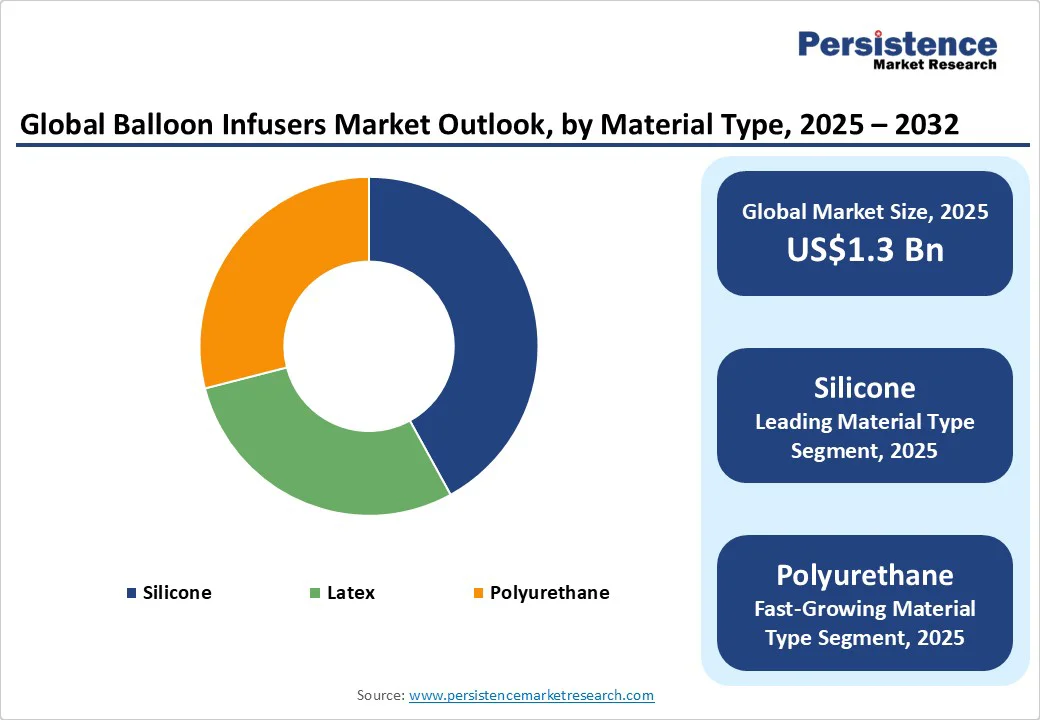

- Dominant Material Type: Silicone balloon infusers are anticipated to lead with a market share of approximately 42% in 2025, due to their flexibility, patient safety, and biocompatibility.

- Leading Product Type: Semi-compliant balloons are anticipated to dominate with 45% market share in 2025, widely used across standard interventional procedures due to their balance of flexibility and pressure control.

| Key Insights | Details |

|---|---|

|

Balloon Infusers Market Size (2025E) |

US$1.3 Bn |

|

Market Value Forecast (2032F) |

US$2.34 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

8.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Cardiovascular Disease and Shift Toward Minimally Invasive and Image-Guided Interventions

Cardiovascular diseases account for nearly one in three global deaths annually. Aging populations, rising incidence of diabetes and hypertension, and lifestyle-related risk factors such as obesity are leading to a steady increase in cardiovascular cases. This translates into higher procedural volumes for angioplasty, stent deployment, and related endovascular interventions where balloon infusers play a crucial role. Hospitals are also reporting higher repeat procedures due to restenosis and complex lesions, further increasing device consumption. The direct relationship between patient burden and procedural demand makes this a reliable growth driver for the balloon infusers market.

Healthcare systems continue to prioritize minimally invasive solutions that reduce hospital stays, improve patient outcomes, and lower overall healthcare costs. In cardiology and vascular surgery, balloons paired with infusion systems are becoming integral to angioplasty and drug delivery applications. This trend has encouraged manufacturers to invest heavily in semi-compliant and non-compliant balloon designs, drug-coated balloon compatibility, and precision infusion systems.

As healthcare access improves, procedure volumes are expected to grow significantly. Emerging markets also represent a price-sensitive customer base, which creates opportunities for mid-tier and low-cost balloon infuser systems that can meet demand while maintaining affordability. The rise of regional manufacturing hubs in Asia Pacific has further improved availability and reduced cost barriers, widening the patient access base.

Regulatory Oversight, Device Safety Concerns, and Cost Pressures

Stringent regulations governing medical devices, particularly in the U.S. and the European Union, present a challenge for manufacturers. Compliance with standards such as the U.S. FDA’s Quality System Regulations and the EU Medical Device Regulation (MDR) requires extensive testing, clinical trials, and documentation. High-profile recalls of balloon catheters and infusion systems have also raised safety concerns, leading hospitals to become more cautious in procurement decisions. This increases both cost and time-to-market for manufacturers, potentially slowing the pace of innovation.

In low- and middle-income countries, affordability remains a significant barrier. Advanced balloon infusers and drug-coated balloon-compatible systems are often priced at a premium, restricting their adoption in markets where government budgets are limited and patients pay a significant share out-of-pocket. Even in developed markets, reimbursement structures vary widely, leading to inconsistent adoption of premium-priced systems. These economic challenges encourage healthcare providers to prioritize cost over innovation, limiting the penetration of advanced solutions.

Growing Adoption of Drug-Coated Balloon (DCB) Procedures and Cost Optimization in Emerging Markets

Drug-coated balloon technology has gained traction in the treatment of restenosis and peripheral artery disease. As adoption of DCB procedures expands, there is a rising demand for balloons and infusion systems that are drug-compatible and provide precise inflation profiles. By 2032, if DCB adoption reaches 20–25% of relevant procedures, balloon infuser manufacturers could unlock incremental revenues worth several hundred million dollars globally.

Companies that align their product portfolios with DCB compatibility and secure strong clinical evidence will be best positioned to capture this growth. Localization of manufacturing in Asia Pacific and Latin America has already demonstrated the ability to reduce landed costs by 15–25%. This allows manufacturers to compete more effectively on price and helps navigate regional regulatory requirements more efficiently. By establishing partnerships with local distributors or contract manufacturers, global companies can scale faster in price-sensitive regions. Capturing this opportunity could increase unit sales by 20–40% in emerging markets, where patient volumes are high but budgets are constrained.

Next-generation balloon infusers are beginning to incorporate sensors and digital connectivity that provide data on pressure, inflation profiles, and real-time procedural performance. This integration allows hospitals to reduce procedure times, minimize complications, and improve training outcomes. Beyond the device itself, connected systems can open new service-based revenue streams through software subscriptions and data analytics. This opportunity could boost gross margins by 5–10% over the next decade, particularly for manufacturers that can combine hardware innovation with digital platforms.

Category-wise Analysis

Material Type Insights

Silicone balloons are expected to dominate the market with approximately 42% share in 2025, owing to their high biocompatibility, flexibility, and reduced risk of particulate shedding. Hospitals and clinicians widely prefer silicone-based products due to their predictable compliance and clinical safety profile. Manufacturers also favor silicone due to its ease of molding into consistent balloon geometries, supporting broad applicability in both coronary and peripheral procedures.

Polyurethane-based balloons are registering the fastest growth, with an estimated CAGR of around 10%. The material offers thinner walls, higher burst resistance, and superior drug-coating adhesion, making it particularly suited for drug-coated balloon applications. As demand for advanced interventions rises, polyurethane balloons are expected to capture a growing share of the market. Their combination of strength and flexibility also enables lower-profile designs, which are increasingly important for accessing smaller vessels in complex procedures.

Product Type Analysis

Semi-compliant balloons are projected to account for nearly 45% of the market, due to their versatility. They provide a balance between controlled expansion and adaptability across varying vessel diameters. Hospitals favor semi-compliant designs as they perform well in most standard angioplasty procedures, offering predictable results without excessive vessel trauma. Their compatibility with a wide range of infusion systems further cements their leadership.

Non-compliant balloons are projected to grow at a CAGR of 10%, fueled by their critical role in complex procedures requiring precise diameter control. These balloons are particularly valuable in stent placement and in treating calcified lesions where high-pressure dilation is essential. The growing global prevalence of complex coronary artery disease cases is expected to sustain this growth trend, making non-compliant balloons a strategic focus for premium product development.

Regional Market Insights

North America Balloon Infusers Market Trends - Innovation-Led Growth Anchored by Advanced Infrastructure

North America is anticipated to dominate, contributing around 37% of global revenues in 2025. Growth in North America is fueled by an innovation-driven ecosystem where leading companies such as Boston Scientific, Abbott Laboratories, and Medtronic consistently launch new and improved balloon infuser products that enhance safety, precision, and ease of use. Boston Scientific's recent launch of the INFLATE balloon infuser is a case in point, featuring smart sensor integration for better infusion control.

The U.S. leads this region due to its high procedural volumes in cardiovascular and other surgical interventions, supported by advanced hospital infrastructure and favorable reimbursement frameworks from Medicare and private insurers. For example, hospitals such as the Mayo Clinic and Cleveland Clinic often serve as early adopters of cutting-edge balloon infusion technologies.

In the U.S., balloon infusers and elastomeric pumps are FDA-regulated Class II medical devices. A 2023 update reclassified elastomeric pumps under Class II with special controls, aligning with ISO 28620:2021 (accuracy) and ISO 80369-7 (connector safety), streamlining the 510(k) process. Medicare Part B covers these pumps as DME for home infusion, with 20% coinsurance post-deductible. Starting January 2025, the NOPAIN Act expanded reimbursement for non-opioid pain management devices under select HCPCS codes.

Europe Balloon Infusers Market Trends - Value-Based Adoption and Localized Manufacturing

Europe stands as the second-largest market for balloon infusers, with key markets including Germany, the U.K., France, and Spain. The introduction of the EU Medical Device Regulation (MDR) in recent years has increased compliance costs and raised the bar for device safety and clinical evidence. While this has created a higher entry barrier for smaller firms, it has benefited established global players such as Siemens Healthineers, Smith & Nephew, and B. Braun Melsungen, who possess the resources to meet these stringent standards.

Growth in Western Europe is steady, supported by mature healthcare systems and well-established reimbursement policies. Central and Eastern European markets such as Poland, Hungary, and the Czech Republic are expanding more rapidly as healthcare infrastructure investments increase and access to advanced medical devices improves.

European buyers often prioritize clinical outcomes and cost-effectiveness, which influences procurement models heavily focused on evidence-based performance and long-term value. Hospitals in countries, including Germany and France, have adopted value-based purchasing frameworks that reward balloon infusers with demonstrated safety and efficacy.

Asia Pacific Balloon Infusers Market Trends - Infrastructure Expansion and Local Partnerships

Asia Pacific is the fastest-growing region in the balloon infusers market. This region is driven primarily by China and India, the two largest healthcare markets worldwide, buoyed by extensive government investments in healthcare infrastructure, expansion of cardiac care units, and a rapidly growing middle-class population demanding access to advanced treatment options.

China’s National Health Commission has rolled out initiatives such as the Healthy China 2030 plan, which supports the modernization of hospitals and the integration of advanced medical devices such as balloon infusers. In India, the expansion of private healthcare chains such as Apollo Hospitals and Fortis Healthcare is increasing the demand for sophisticated infusion systems.

Japan remains a mature but significant market, characterized by a well-established healthcare system and an aging population that drives demand for cardiac and vascular procedures. Meanwhile, ASEAN countries (including Indonesia, Malaysia, and Thailand) are emerging as important secondary demand centers as healthcare access and affordability improve.

International Original Equipment Manufacturers (OEMs) are focusing on local manufacturing facilities, leveraging government tenders, and forming partnerships with regional distributors. For example, Medtronic has set up manufacturing units in Malaysia to cater to regional demand efficiently. These strategies help reduce costs, ensure regulatory compliance, and build trust within local healthcare ecosystems.

Competitive Landscape

The global balloon infusers market is moderately consolidated, with global giants such as Medtronic, Boston Scientific, Abbott, and Teleflex dominating the premium segment. These companies hold a combined market share of over 50% in developed regions, supported by broad product portfolios and strong clinical validation. In contrast, emerging markets are more fragmented, with numerous local and regional manufacturers offering cost-effective alternatives. This dual structure creates a competitive environment where differentiation hinges on clinical evidence, regulatory compliance, and pricing strategies.

Leading OEMs launched next-generation balloon infusers with features such as improved compliance profiles, thinner balloon walls, and enhanced compatibility with drug-coated technologies. These launches strengthened clinical positioning and secured higher procurement rates. Several companies established contract manufacturing facilities and partnerships in Asia Pacific to lower costs and capture tenders. This localization strategy has proven critical for expanding into high-volume, price-sensitive markets.

Core strategies revolve around innovation, cost optimization, and market expansion. Leaders are differentiating through clinical evidence-backed products, robust after-sales support, and digital integration. Emerging models include subscription-based pricing for consumables and outcome-based procurement agreements.

Key Industry Developments

- In May 2025, C. R. Bard (BD) launched the Ranger Balloon Inflation Device, offering precise pressure control and enhanced visibility during angioplasty procedures.

- In February 2025, B. Braun Melsungen AG rolled out a smart elastomeric pump with customizable flow-rate settings, improving safety and therapy personalization.

Companies Covered in Balloon Infusers Market

- B. Braun Melsungen AG

- Baxter International Inc.

- Fresenius Kabi AG

- Terumo Corporation

- Nipro Corporation

- Smiths Medical

- Avanos Medical, Inc.

- Ambu A/S

- Pfm Medical AG

- Daiken Medical Co., Ltd.

- Palex Medical SA

- Canack Technology Ltd.

- PROMECON GmbH

- Halomedical Systems Ltd.

- ICU Medical, Inc.

- Becton, Dickinson and Company (BD)

- Pfizer Inc.

- Moog Inc.

- Medtronic plc

- Teleflex Incorporated

Frequently Asked Questions

The balloon infusers market size in 2025 is estimated at US$1.3 Bn.

By 2032, the balloon infusers market is projected to reach US$2.34 Bn, reflecting strong demand across medical applications.

Key trends include the rising adoption of elastomeric balloon pumps for outpatient care, increasing use of smart and sensor-integrated devices, and growing demand for disposable balloon infusers in oncology and pain management. Product innovations offering customizable flow rates and digital monitoring features are further shaping the market landscape.

The silicone balloon infusers segment holds the largest share, driven by its reliability and widespread use in post-operative pain management.

The balloon infusers market is expected to expand at a CAGR of 8.8% from 2025 to 2032.

The leading companies include B. Braun Melsungen AG, Baxter International Inc., Fresenius Kabi AG, Terumo Corporation, and Becton, Dickinson and Company (BD).