- Executive Summary

- Global Automotive Venting Membrane Market Snapshot, 2026 and 2033

- Market Opportunity Assessment, 2026 - 2033, US$ Bn

- Key Market Trends

- Future Market Projections

- Specialty Clinics Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Key Trends

- Macro-Economic Factors

- Global Sectorial Outlook

- Global GDP Growth Outlook

- COVID-19 Impact Analysis

- Forecast Factors - Relevance and Impact

- Value Added Insights

- Treatment Type Adoption Analysis

- Regulatory Landscape

- Value Chain Analysis

- Key Deals and Mergers

- PESTLE Analysis

- Porter’s Five Force Analysis

- Global Automotive Venting Membrane Market Outlook:

- Key Highlights

- Market Size (US$ Bn) and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Bn) Analysis and Forecast

- Historical Market Size (US$ Bn) Analysis, 2020-2025

- Market Size (US$ Bn) Analysis and Forecast, 2025-2033

- Global Automotive Venting Membrane Market Outlook: By Product Type

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Product Type,2020-2025

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026-2033

- ePTFE Membranes

- PU Membranes

- Others

- Market Attractiveness Analysis: By Product Type

- Global Automotive Venting Membrane Market Outlook: By Application Type

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Application Type,2020-2025

- Market Size (US$ Bn) Analysis and Forecast, By Application Type, 2026- 2033

- Engine Systems

- Electrical Components

- Lighting Systems

- Powertrain

- Others

- Market Attractiveness Analysis: Indication

- Key Highlights

- Global Automotive Venting Membrane Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Region,2020-2025

- Market Size (US$ Bn) Analysis and Forecast, By Region, 2026- 2033

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Automotive Venting Membrane Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market,2020-2025

- By Country

- By Product Type

- By Application Type

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026- 2033

- U.S.

- Canada

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026- 2033

- ePTFE Membranes

- PU Membranes

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Application Type, 2026- 2033

- Engine Systems

- Electrical Components

- Lighting Systems

- Powertrain

- Others

- Europe Automotive Venting Membrane Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market,2020-2025

- By Country

- By Product Type

- By Application Type

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026- 2033

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Türkiye

- Rest of Europe

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026- 2033

- ePTFE Membranes

- PU Membranes

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Application Type, 2026- 2033

- Engine Systems

- Electrical Components

- Lighting Systems

- Powertrain

- Others

- East Asia Automotive Venting Membrane Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market,2020-2025

- By Country

- By Product Type

- By Application Type

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026- 2033

- China

- Japan

- South Korea

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026- 2033

- ePTFE Membranes

- PU Membranes

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Application Type, 2026- 2033

- Engine Systems

- Electrical Components

- Lighting Systems

- Powertrain

- Others

- South Asia & Oceania Automotive Venting Membrane Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market,2020-2025

- By Country

- By Product Type

- By Application Type

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026- 2033

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026- 2033

- ePTFE Membranes

- PU Membranes

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Application Type, 2026- 2033

- Engine Systems

- Electrical Components

- Lighting Systems

- Powertrain

- Others

- Latin America Automotive Venting Membrane Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market,2020-2025

- By Country

- By Product Type

- By Application Type

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026- 2033

- Brazil

- Mexico

- Rest of Latin America

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026- 2033

- ePTFE Membranes

- PU Membranes

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Application Type, 2026- 2033

- Engine Systems

- Electrical Components

- Lighting Systems

- Powertrain

- Others

- Middle East & Africa Automotive Venting Membrane Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market,2020-2025

- By Country

- By Product Type

- By Application Type

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026- 2033

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026- 2033

- ePTFE Membranes

- PU Membranes

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Application Type, 2026- 2033

- Engine Systems

- Electrical Components

- Lighting Systems

- Powertrain

- Others

- Competition Landscape

- Market Share Analysis, 2024

- Market Structure

- Competition Intensity Mapping by Market

- Competition Dashboard

- Company Profiles (Details - Overview, Financials, Strategy, Recent Developments)

- GORE® Automotive

- Overview

- Segments and Treatment Types

- Key Financials

- Market Developments

- Market Strategy

- Donaldson Company, Inc.

- Saint-Gobain Performance Plastics

- Freudenberg Group

- Porex Corporation

- W. L. Gore & Associates, Inc.

- Nitto Denko Corporation

- Zeus Industrial Products, Inc.

- Sumitomo Electric Industries, Ltd.

- Clarcor Inc.

- Parker Hannifin Corporation

- MicroVent

- APTIV PLC

- MANN+HUMMEL Group

- GORE® Automotive

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Automotive Components & Materials

- Automotive Venting Membrane Market

Automotive Venting Membrane Market Size, Share, and Growth Forecast, 2026 - 2033

Automotive Venting Membrane Market by Product Type (ePTFE Membranes, PU Membranes, Others), Application Type (Engine Systems, Electrical Components, Lighting Systems, Powertrain, Others), and Regional Analysis for 2026 - 2033

Automotive Venting Membrane Market Size and Trends Analysis

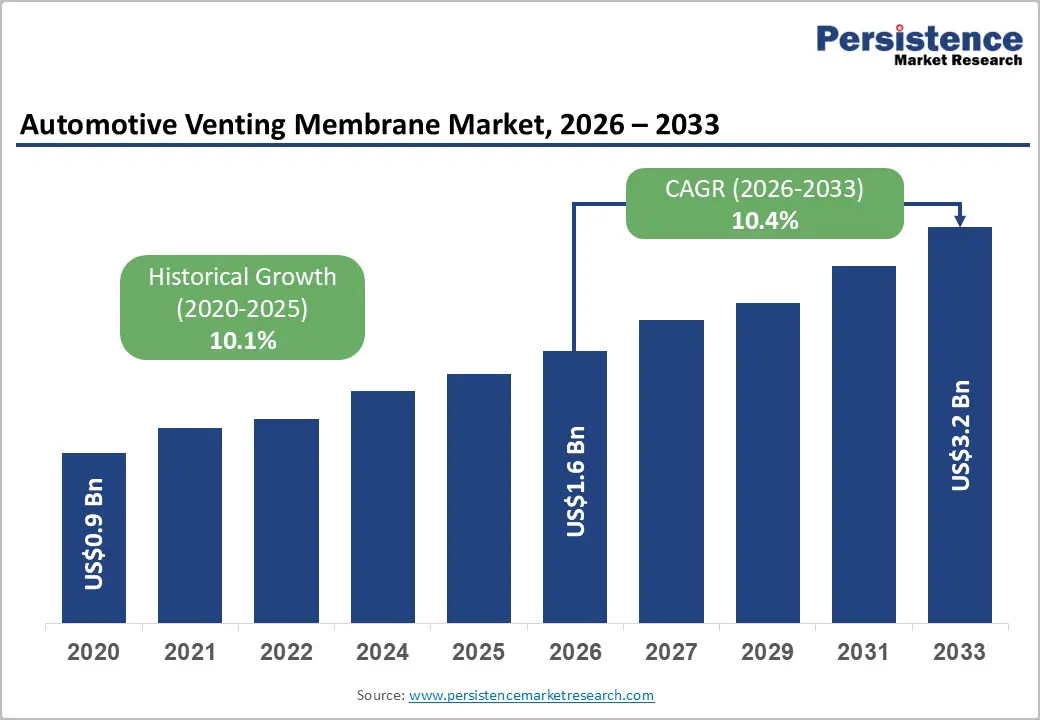

The global automotive venting membrane market size is likely to be valued at US$1.6 billion in 2026 and is expected to reach US$3.2 billion by 2033, growing at a CAGR of 10.4% during the forecast period from 2026 to 2033, driven by rising vehicle production, increasing integration of electronic and electrical components, and the growing need for effective pressure equalization and moisture protection in sealed automotive systems.

The shift toward electric vehicles (EVs) is driving demand for venting membranes, which protect batteries, electronics, and sensors from heat, moisture, and contaminants. Strict emission, safety, and durability standards are prompting OEMs to adopt advanced venting solutions across engines, lighting, powertrains, and electronic housings.

Key Industry Highlights:

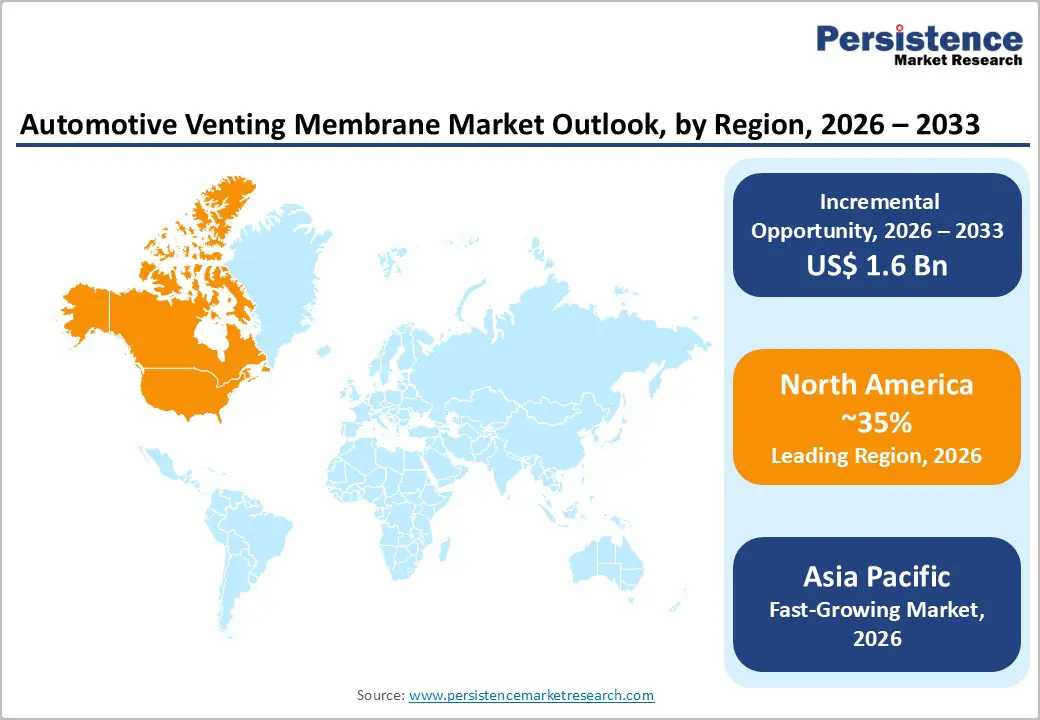

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 35% in 2026, driven by strong EV adoption, stringent emission regulations, advanced automotive electronics, and robust OEM investments.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, driven by rapid EV adoption, large-scale vehicle production, cost-efficient manufacturing, and rising demand for battery and powertrain venting solutions.

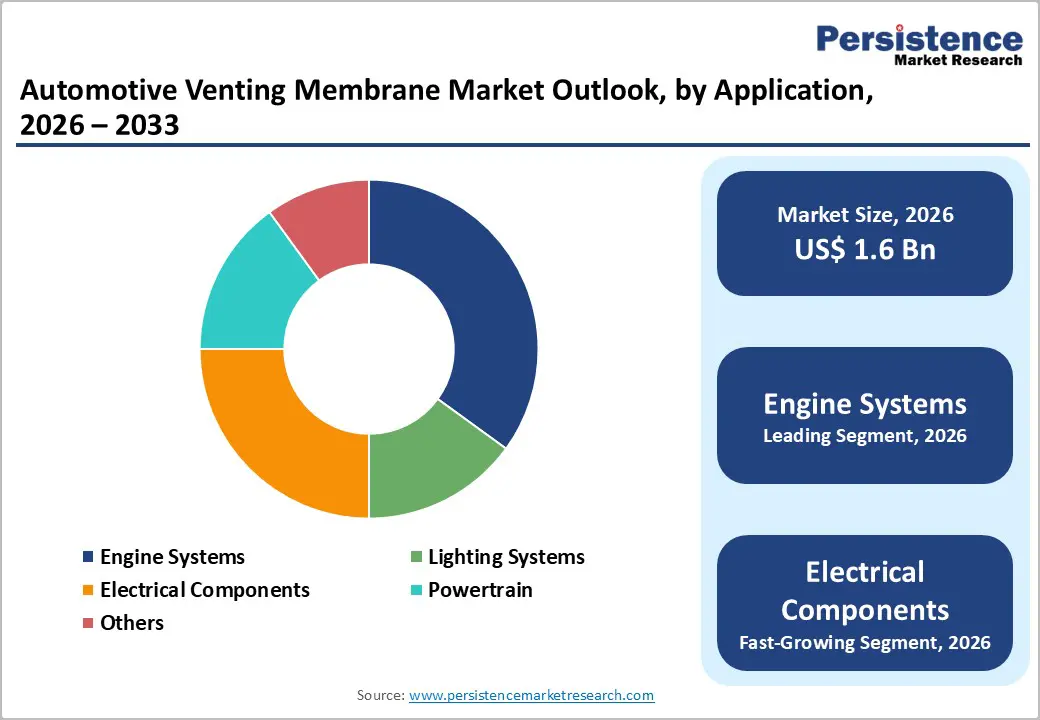

- Leading Product Type: ePTFE membranes are projected to be the leading product type in 2026, accounting for 45% of revenue share, owing to their superior breathability, chemical resistance, and reliability in demanding automotive environments.

- Leading Application: Engine systems are anticipated to be the leading application type, accounting for over 40% of the revenue share in 2026, supported by their extensive use in core propulsion and pressure-sensitive automotive components.

| Key Insights | Details |

|---|---|

| Automotive Venting Membrane Market Size (2026E) | US$1.6 Bn |

| Market Value Forecast (2033F) | US$3.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 10.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 10.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Increasing Demand for Electronic Component Protection in Vehicles

Modern electric and hybrid vehicles increasingly rely on sensitive electronic modules, including battery management systems, power control units, sensors, infotainment systems, and advanced driver-assistance systems (ADAS). These components need robust protection against moisture, dust, temperature changes, and chemical exposure. Automotive venting membranes are essential for ensuring reliability and longevity by equalizing pressure while preventing the ingress of liquids and particulates. The use of high-performance membranes, particularly ePTFE and polyurethane (PU)-based solutions, has grown as manufacturers prioritize electronic durability and performance.

The transition to electric vehicles (EVs) has further heightened demand, as battery packs and associated electronics require specialized venting to manage thermal and pressure fluctuations while safeguarding against water, dust, and corrosive substances. Regulatory standards emphasizing the safety, performance, and durability of automotive electronics are also driving OEM adoption. The market for automotive venting membranes is expanding rapidly, with manufacturers investing in advanced membrane technologies to protect electronic components in both passenger and commercial vehicles.

Volatility in Raw Material Prices

Venting membranes are primarily manufactured using specialized materials such as ePTFE, PU, and other high-performance polymers. These materials are heavily influenced by fluctuations in the global chemical and polymer markets, which, in turn, are affected by factors such as changes in crude oil prices, geopolitical tensions, supply chain disruptions, and regional production limitations. Such volatility introduces uncertainty for manufacturers, making it challenging to maintain consistent pricing and plan long-term contracts with automotive OEMs.

Rising raw material costs can constrain the adoption of premium venting membranes in cost-sensitive vehicle segments, as manufacturers may seek more economical alternatives that compromise on performance. This is particularly critical for applications requiring high durability, chemical resistance, and reliable moisture and pressure management, such as EV battery packs and electronic housings. Companies must adopt strategic sourcing, efficient supply chain management, and cost-optimization strategies to mitigate the impact of price fluctuations.

Venting Membranes Supporting Next-Generation Automotive Technologies

The growth of autonomous and connected vehicles offers a significant opportunity for the automotive venting membrane market. These vehicles rely on advanced electronic systems, such as ADAS, LiDAR, radar modules, cameras, and infotainment networks that require robust protection from environmental contaminants. Venting membranes ensure reliability and longevity by enabling pressure equalization, managing moisture, and preventing the ingress of dust, water, and other particulates.

Rising demand for specialized membranes for EV batteries, sensor housings, and electronic control units is driving innovation in materials such as ePTFE and PU, which provide superior breathability, chemical resistance, and durability. Regulatory standards focused on electronic safety and reliability further support adoption. Autonomous and connected vehicles are thereby creating strong growth prospects for manufacturers, spurring investments in high-performance venting solutions for the next generation of smart and electrified automotive technologies.

Category-wise Analysis

Product Type Insights

The ePTFE membranes segment is expected to lead the automotive venting membrane market, accounting for approximately 45% of total revenue in 2026, driven by their exceptional performance in demanding automotive applications. These membranes are highly valued for their superior breathability, chemical resistance, and durability under extreme conditions, including high temperatures, moisture exposure, and pressure variations. ePTFE membranes are widely adopted in premium applications, including EV battery packs, engine housings, and advanced electronic modules, where long-term reliability is critical. For example, Gore® Automotive uses ePTFE membranes in battery venting systems for EVs, ensuring safe pressure equalization while preventing water and particulate ingress.

PU membranes are likely to represent the fastest-growing segment in 2026, driven by their cost-effectiveness and flexibility across a broad range of automotive venting applications. For example, Freudenberg Group develops customized PU and hybrid membrane solutions, alongside traditional ePTFE products, catering to varied venting needs, including electronic housings and standard engine ventilation systems, at competitive costs compared with high-end PTFE options. These membranes offer adequate breathability, sealant compatibility, and mechanical strength, making them suitable for mass-market vehicles and standard automotive modules where premium ePTFE performance may exceed requirements.

Application Insights

Engine systems are projected to lead the market, capturing around 40% of the total revenue share in 2026, due to the widespread necessity of pressure equalization in core automotive systems. These applications require venting membranes to manage pressure fluctuations, prevent contaminant ingress, and ensure durability in combustion and propulsion-related components. Membranes are integrated into fuel tanks, transmission housings, and engine enclosures to maintain operational efficiency and meet regulatory standards. For example, Freudenberg Group supplies venting membranes for engine air intake and transmission systems, enhancing component protection and performance reliability.

Electrical components are likely to be the fastest-growing, driven by the rapid integration of electronics, sensors, and connected vehicle technologies. These systems demand advanced venting membranes for moisture management, dust filtration, and thermal stability, ensuring the reliability of sensitive modules such as ADAS, infotainment, and lighting controls. For example, MANN+HUMMEL provides membranes for electric vehicle battery enclosures and electronic control units, safeguarding electronics against environmental stressors. The growth in this segment is propelled by the global shift toward EVs, autonomous vehicles, and highly connected cars, which significantly increase the number and complexity of electronic components.

Regional Insights

North America Automotive Venting Membrane Market Trends

North America is expected to lead the market in 2026, capturing a 35% share, driven by the region’s advanced automotive industry and rapid adoption of electric and autonomous vehicles. The increasing use of venting membranes in battery packs, power electronics, and control modules ensures reliable pressure equalization and protection against environmental factors, particularly as EV production grows in the U.S. and Canada. Rising demand for high IP-rated components to safeguard sensors, lighting systems, and electronic housings is further boosting membrane adoption across modern vehicle architectures.

The region is also seeing a shift toward sustainable, eco-friendly membrane materials, driven by regulations on environmental compliance and a reduction in the use of fluorinated compounds. Manufacturers are exploring recyclable and PFAS-free alternatives to meet evolving standards and support circular economy initiatives. Localized production and smart manufacturing are strengthening domestic supply chains, reducing dependence on imports, and enabling tailored solutions for regional OEMs. For example, MicroVent has developed specialized venting membranes for hybrid and electric vehicles, improving filtration and temperature regulation in battery systems.

Europe Automotive Venting Membrane Market Trends

Europe is expected to be a key market for automotive venting membranes in 2026, driven by stringent regulations aimed at reducing emissions, improving safety, and advancing sustainability. Policies such as the EU’s Fit for 55 initiative and tightening CO2 standards are accelerating the adoption of electric and hybrid vehicles, increasing demand for high-performance venting membranes to protect battery packs, power electronics, and control modules from moisture, dust, and pressure fluctuations. Germany, France, the U.K., and Italy are leading markets due to their advanced automotive sectors and early adoption of electrified mobility.

The rapid deployment of connected and autonomous vehicle technologies further drives membrane usage across ADAS sensors, ECUs, and lighting systems, all of which require robust environmental protection. In response, companies such as Freudenberg Group have expanded European operations to supply advanced venting solutions for EV battery housings and electronic modules. Strategic partnerships and investments in localized R&D and production infrastructure are reinforcing the region’s competitive position and supporting OEMs in meeting performance and regulatory requirements.

Asia Pacific Automotive Venting Membrane Market Trends

The Asia Pacific region is expected to be the fastest-growing market for automotive venting membranes in 2026, driven by high vehicle production volumes and rapid adoption of electric and hybrid vehicles. China, Japan, South Korea, and India are key contributors, with China leading due to its dominant global vehicle output and ambitious EV policy targets, which increase demand for advanced venting solutions for battery packs and electronic components. Government incentives and subsidies promoting clean mobility are further supporting regional membrane adoption.

The region is also seeing a shift toward sustainable, next-generation venting materials, including recyclable and PFAS-free options, in response to stricter environmental regulations and OEM sustainability objectives. Manufacturers are developing lightweight, high-temperature-resistant, and eco-friendly membrane solutions to meet evolving standards. For example, Saint-Gobain Performance Plastics has expanded its operations in China to supply advanced ePTFE and hybrid venting membranes for EV battery housings and electronic modules, strengthening its position in the region’s growing automotive sector.

Competitive Landscape

The global automotive venting membrane market exhibits a moderately fragmented structure, driven by numerous established material and component manufacturers competing across regions, technologies, and application areas. While a few large players hold significant shares in advanced membrane technologies such as ePTFE and specialty materials, the overall market also includes a wide range of regional and niche suppliers offering polyurethane and hybrid solutions for standard automotive venting needs. This diversity reflects varying OEM requirements for cost, performance, and application-specific features, from battery pack venting to electronics enclosures and fluid reservoirs.

With key leaders including Gore & Associates, Donaldson Company, Inc., Freudenberg Group, Saint-Gobain Performance Plastics, Porex Corporation, Parker Hannifin Corporation, and Sumitomo Electric Industries, Ltd., the competitive landscape is focused on innovation and market expansion. These players leverage their R&D capabilities, patented materials, and strong OEM relationships to maintain leadership positions and secure long-term supply contracts. For example, Gore has launched an advanced ePTFE membrane series tailored for EV battery applications, enhancing pressure resistance and contaminant protection for next-generation electric vehicles.

Key Industry Developments:

- In August 2025, ANTA Group, in partnership with Donghua University, launched AEROVENT ZERO, a high-performance, PFAS-free waterproof-breathable membrane developed in China. As the country’s first independently developed and commercially scaled PFAS-free membrane, AEROVENT ZERO represents a major advancement in sustainable technical textiles and strengthens China’s position in a market traditionally dominated by international players.

- In May 2024, KACO GmbH + Co KG, a subsidiary of the Zhongding Group, introduced a next-generation battery venting system for electric vehicles. Designed to enhance EV battery safety, reliability, and performance, the system addresses challenges from higher battery energy densities and extreme operating conditions. Key features include water resistance above 250 mbar, adjustable opening pressure, and stable operation across a temperature range of -40°C to +80°C.

Companies Covered in Automotive Venting Membrane Market

- GORE® Automotive

- Donaldson Company, Inc.

- Saint-Gobain Performance Plastics

- Freudenberg Group

- Porex Corporation

- W. L. Gore & Associates, Inc.

- Nitto Denko Corporation

- Zeus Industrial Products, Inc.

- Sumitomo Electric Industries, Ltd.

- Clarcor Inc.

- Parker Hannifin Corporation

- MicroVent

- APTIV PLC

- MANN+HUMMEL Group

Frequently Asked Questions

The global automotive venting membrane market is projected to reach US$1.6 billion in 2026.

Rising vehicle production, increasing integration of electronic and EV components, and the need for effective pressure equalization and protection against moisture and contaminants.

The automotive venting membrane market is expected to grow at a CAGR of 10.4% from 2026 to 2033.

The rapid growth of electric, autonomous, and connected vehicles, increasing demand for battery and electronics venting solutions, and the development of sustainable, PFAS-free, and high-performance membrane materials.

GORE® Automotive, Donaldson Company, Inc., and Saint-Gobain Performance Plastics are some of the leading players.