- Automotive Components & Materials

- Automotive Engine Cradle Market

Automotive Engine Cradle Market Size, Share and Growth Forecast, 2026-2033

Automotive Engine Cradle Market by Material Type (Metallic, Non-Metallic), Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicle (HCVs)), Sales Channel (Original Equipment Manufacturers (OEMs), Aftermarket), Regional Forecast for 2026-2033

Automotive Engine Cradle Market Share and Trends Analysis

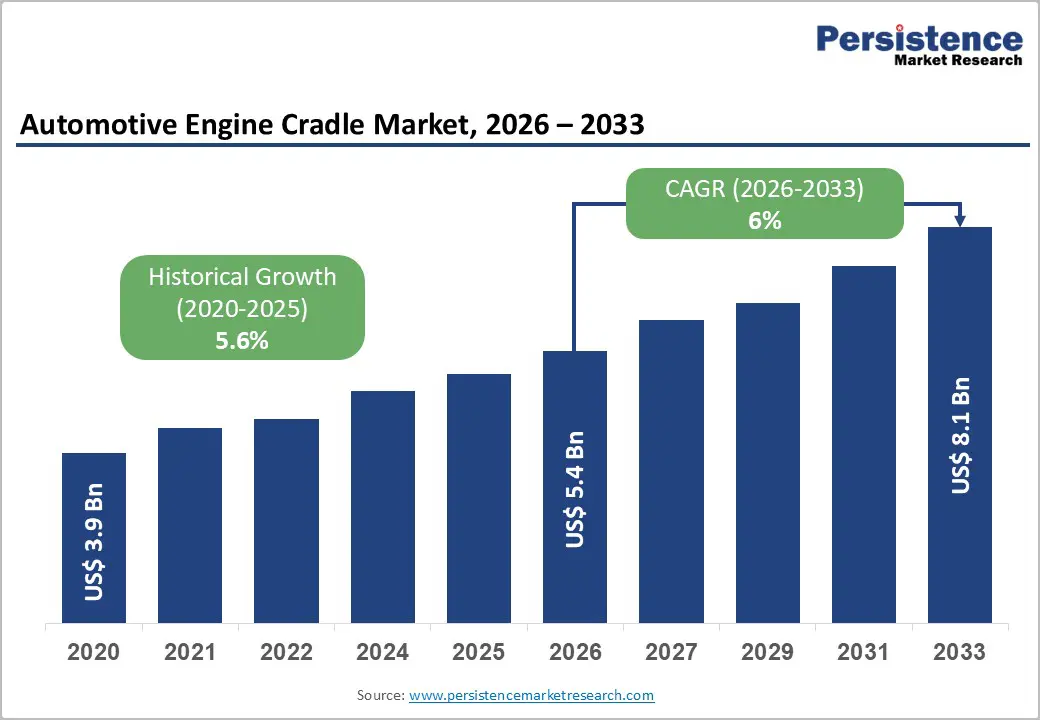

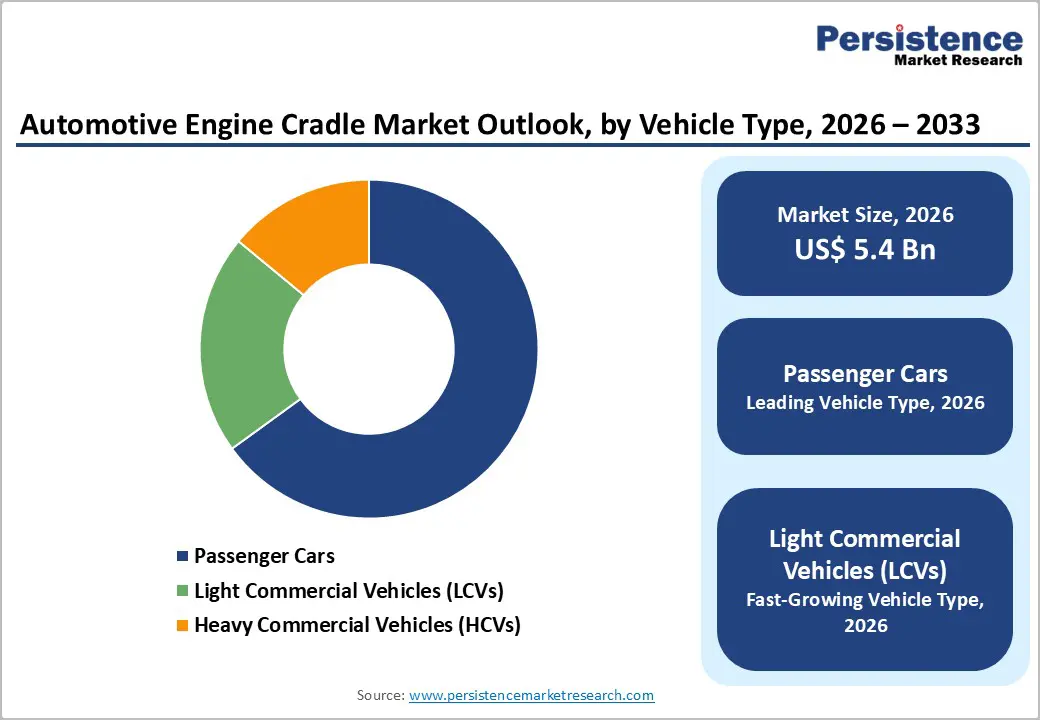

The global automotive engine cradle market size is likely to be valued at US$ 5.4 billion in 2026, and is projected to reach US$ 8.1 billion by 2033, growing at a CAGR of 6.0% during the forecast period of 2026–2033.

The market is evolving steadily as vehicle manufacturers are responding to changing platform architectures and stricter performance expectations. Growth is being supported by rising vehicle production and by the increasing use of lightweight structural components that are improving fuel efficiency and overall vehicle dynamics. Automotive original equipment manufacturers (OEMs) are actively redesigning engine cradle systems to support modular vehicle platforms and electrified powertrains, which are becoming central to long-term product strategies. Engine cradles are continuing to play a critical role in load distribution, vibration control, and powertrain integration across passenger and commercial vehicle segments. Regulatory pressure is also shaping market direction as safety and emissions standards are becoming more stringent across global markets. Manufacturers are investing in advanced materials and optimized designs to enhance crash performance while reducing overall vehicle weight.

Key Industry Highlights

- Dominant Material Type: Metallic engine cradles are expected to account for approximately 78% of global revenue in 2026, driven by their structural strength and cost efficiency.

- Leading Vehicle Type: Passenger cars are expected to hold around 65% revenue share in 2026, supported by high production volumes and safety-driven structural integration.

- Fastest-growing Vehicle Type: Light commercial vehicles (LCVs) are projected to be the fastest-growing sat a CAGR of about 6.8% through 2033, driven by e-commerce logistics growth and fleet electrification.

- Dominant Sales Channel: OEMs are projected to command 82% of the market revenue in 2026, reflecting engine cradle integration at the vehicle assembly stag.

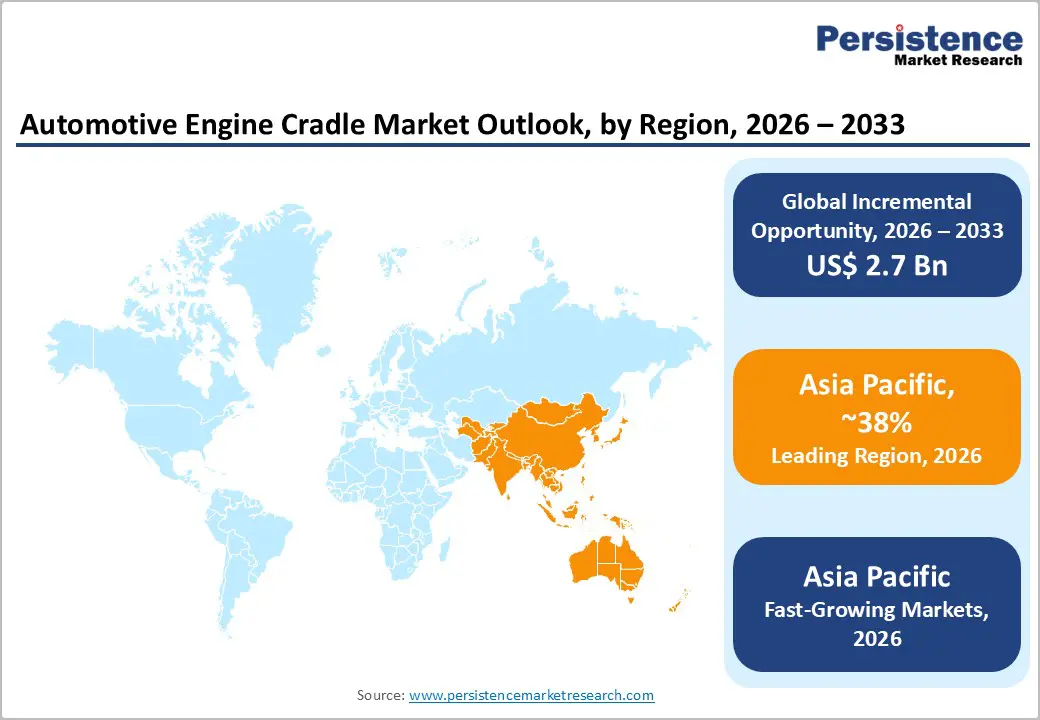

- Regional Leadership: Asia Pacific is expected to dominate with a share of approximately 38% in 2026, and is projected to grow at a CAGR of around 6.9% through 2033, supported by large-scale vehicle manufacturing and cost-efficient supply chains.

- Core Growth Themes: Electrification and lightweighting are the most critical long-term growth drivers, as OEMs redesign engine cradle systems to support electric powertrains, improve efficiency, and meet tightening emission and safety regulations.

| Key Insights | Details |

|---|---|

| Automotive Engine Cradle Market Size (2026E) | US$ 5.4 Bn |

| Market Value Forecast (2033F) | US$ 8.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Vehicle Production Growth and Regulatory-Led Platform Transformation

Global vehicle production has entered a structurally stronger phase following post-pandemic supply chain normalization, with total output exceeding 93 million units in 2024, and passenger cars contributing nearly 75% of production. As engine cradles serve as core structural elements supporting the powertrain, suspension, and steering systems, higher vehicle output directly translates into proportional demand growth. At the same time, OEMs are accelerating the transition toward modular vehicle platforms, enabling multiple models to share standardized underbody architectures. This shift improves manufacturing scalability, reduces component complexity, and increases repeat demand for uniform engine cradle designs across regions and vehicle classes.

Regulatory pressure is reinforcing this structural transition. Emission and fuel-efficiency mandates under the European Union (EU) Fit for 55 framework and U.S. CAFE standards are pushing OEMs to reduce vehicle weight, as a 10% reduction in mass can improve fuel efficiency by 6–8%. In response, leading automakers intensified investment in lightweight chassis and subframe systems. For instance, Volkswagen Group expanded its modular platform investments across Europe in 2025, prioritizing high-strength steel and aluminum-intensive underbody structures to meet emission targets while preserving crash performance and NVH standards. These combined production, regulatory, and platform trends are structurally increasing the strategic importance and value contribution of advanced automotive engine cradle systems.

Cost Pressure and Supply Chain Localization Challenges

The manufacturing of automotive engine cradles is inherently capital-intensive, involving complex forming, welding, and precision machining processes, particularly for aluminum and hybrid material variants. According to World Steel Association and International Aluminium Institute data, raw material price volatility remained elevated due to energy cost inflation and geopolitical disruptions, increasing input cost uncertainty for component suppliers. These pressures raise production costs and constrain pricing flexibility, especially for OEM programs targeting cost-sensitive passenger and commercial vehicle segments, slowing the adoption of advanced engine cradle designs.

Supply chain reliability further compounds these challenges, as engine cradles must be delivered in tight synchronization with vehicle assembly operations. During 2024–2025, logistics bottlenecks and regional trade uncertainties exposed vulnerabilities in cross-border sourcing for large structural components. In response, OEMs intensified localization requirements, compelling suppliers to establish regional manufacturing footprints. For example, in 2025, several global automakers expanded localized sourcing mandates across North America and Asia, prompting Tier-1 suppliers to announce new capacity investments, while smaller Tier-2 players faced consolidation pressure due to limited capital access. This uneven ability to localize production continues to restrain short-term market expansion.

Electrification and Logistics-Led Structural Evolution

The accelerating shift toward electric mobility is creating a significant opportunity for the redesign of automotive engine cradle systems. According to the International Energy Agency (IEA), global electric vehicle (EV) sales surpassed 17 million units in 2024, accounting for nearly 20% of total vehicle sales, fundamentally altering vehicle underbody and load-distribution requirements. Electric platforms require modified subframes to support battery packs, electric motors, and enhanced crash protection, increasing demand for lightweight yet structurally robust engine cradle designs. OEMs are therefore prioritizing modular and EV-optimized cradle architectures across new vehicle programs.

This opportunity is further strengthened by the rapid expansion of urban logistics and advanced manufacturing adoption. The World Bank reported a 7% annual increase in urban freight movement across developing economies in 2025, driving higher utilization of light commercial vehicles that require engine cradles capable of sustaining higher load cycles and improved fatigue resistance. In parallel, governments in Germany, Japan, and China introduced incentives in 2025 to accelerate smart manufacturing adoption, supporting the use of hydroforming, robotic welding, and digital simulation. These developments enable suppliers to improve production efficiency, enhance structural consistency, and align with OEM investment plans focused on electrified and high-duty-cycle vehicle platforms.

Category-wise Insights

Material Type Insights

Metallic cradles are expected to remain the dominant material segment, accounting for approximately 78% of global revenues in 2026, due to their proven structural strength, cost efficiency, and recyclability. Steel and aluminum cradles are preferred in mass-market passenger cars and commercial vehicles, where crash performance and durability are critical. Volkswagen Group expanded metallic subframe production at its Emden facility in Germany, supporting modular platform integration for high-volume passenger cars while maintaining safety and cost-efficiency standards. Government-backed recycling mandates in the EU further reinforced continued reliance on metallic structures.

Non-metallic automotive engine cradles are projected to be the fastest-growing material segment, expanding at a CAGR of 7.2% through 2033, driven by EV adoption and premium vehicle demand. Composites provide corrosion resistance and significant weight reduction, enhancing vehicle efficiency. Toyota incorporated composite engine cradles in its limited-production bZ4X electric SUV in Japan, validating durability and NVH performance. This milestone encouraged suppliers to scale production capabilities and invest in lightweight composite technologies for future EV platforms.

Vehicle Type Insights

Passenger cars are likely to lead the market, holding nearly 65% of the automotive engine cradle market revenue share in 2026, driven by high production volumes and stringent safety regulations. Engine cradles enhance noise, vibration, & harshness (NVH) control and crash energy absorption, improving vehicle performance and occupant safety. Stellantis standardized metallic cradles across Jeep and Peugeot modular platforms in Europe, optimizing production and structural reliability. Regulatory emphasis on crash testing in Europe reinforced demand. Consumer preference for quieter, smoother rides further increased adoption. Modular cradle designs enabled deployment across multiple models, improving efficiency. Passenger cars remain the backbone of global engine cradle demand.

LCVs are expected to be the fastest-growing segment, projected to showcase a CAGR of 6.8% during the 2026-2033 forecast period, fueled by last-mile delivery and fleet electrification. Cradles must withstand higher loads and frequent use. Ford launched localized production of the e-Transit van in Kansas City, integrating high-strength metallic cradles for urban logistics. Public incentives for electric freight in North America boosted adoption. OEM modular platforms improved reliability across internal combustion engine (ICE) and EV variants. Increasing e-commerce and fleet electrification support long-term growth. LCVs are now a key growth driver for engine cradle suppliers.

Sales Channel Insights

OEM channels are projected to dominate with over 82% of market revenues in 2026, as cradles are integrated during the vehicle assembly stage. Long-term platform agreements and synchronized production planning are providing supply continuity and quality consistency for manufacturers. OEMs are increasingly adopting modular cradle architectures to simplify assembly across multiple vehicle models and powertrain configurations. Capacity expansions by tier-one suppliers are aligning with localization requirements and regulatory expectations, particularly for passenger vehicles and LCVs. Over time, OEM-led sourcing will have reinforced reliability, compliance, and scale efficiency, sustaining this channel as the core revenue foundation for engine cradle suppliers.

The aftermarket segment is expanding steadily as vehicle fleets are aging and replacement cycles are increasing, particularly in collision repair and high-usage commercial applications. Regulatory tightening around vehicle roadworthiness is encouraging more frequent inspections and component replacements, supporting sustained aftermarket activity. Policy actions by authorities such as Japan’s Ministry of Land, Infrastructure, Transport and Tourism (MLIT) are strengthening compliance standards, which is increasing demand for certified replacement parts. Suppliers are broadening distribution networks to improve reach across passenger and commercial fleets. As 2033 draws closer, aftermarket demand will have evolved into a stable complementary channel, delivering recurring revenue while supporting long-term vehicle maintenance and operational safety.

Regional Insights

North America Automotive Engine Cradle Market Trends

North America, led by the United States, remains a key market for automotive engine cradles due to the strong production of light trucks and SUVs. U.S. Department of Transportation (DOT) mandates on crash performance and fuel efficiency directly influence subframe and cradle design standards. OEMs and Tier-1 suppliers invest heavily in lightweight steel, aluminum, and EV-compatible architectures to comply with regulations. For instance, General Motors expanded EV platform production in Michigan, integrating modular subframe and cradle systems for electric trucks and SUVs. Consumer demand for safer and quieter rides further supports the adoption of engineered cradles. Modular cradle standardization across models improves assembly efficiency and reduces costs. North America continues to be a high-value market with stable demand driven by regulation and production scale.

Reshoring initiatives and incentives under the Inflation Reduction Act (IRA) encourage local manufacturing of structural components, creating investment opportunities for suppliers. Tier-1 and Tier-2 companies are establishing new regional facilities and upgrading technology to meet OEM requirements. Advanced joining techniques, robotics, and digital simulation are increasingly used to reduce weight and improve durability. OEMs prioritize cradle standardization across modular platforms to optimize production efficiency. Investments in EV-specific cradles further strengthen supplier competitiveness. Collaborative initiatives between manufacturers and government programs support supply chain resilience. Thus, North America maintains a strong market position through regulation-driven innovation and production capacity.

Europe Automotive Engine Cradle Market Trends

Europe is a key regional market for automotive engine cradles, led by Germany, the U.K., France, and Spain, with Germany serving as the engineering and R&D hub. Premium OEMs focus on advanced chassis systems and aluminum or composite cradles to reduce weight and enhance efficiency. Harmonized Euro 7 emission and safety regulations drive the adoption of efficient engine mounting solutions. BMW expanded lightweight subframe production in Leipzig, integrating composite cradles for EV and hybrid vehicles, reinforcing Europe’s leadership in engineering-intensive structural components. Consumer demand for high NVH performance and sustainable materials supports cradle adoption. Standardization across modular platforms improves production efficiency and cost control. Europe remains a critical market for high-value engine cradle solutions, combining innovation with regulatory compliance.

Energy cost pressures and environmental compliance requirements continue to shape supplier investment strategies, encouraging automation and resource-efficient production. OEMs are standardizing metallic and composite cradles across modular vehicle lines to optimize efficiency. Strong R&D funding supports the development of crash-optimized and lightweight designs. Government EV incentives and infrastructure expansion indirectly boost demand for EV-compatible engine cradles. Suppliers balance technological innovation with regulatory requirements to maintain competitiveness. European OEMs continue to prioritize cradle performance, sustainability, and cost-effectiveness. This positions Europe as a strategic market for advanced engine cradle solutions.

Asia Pacific Automotive Engine Cradle Market Trends

Asia Pacific is expected to be the largest and fastest-growing regional market for automotive engine cradles, accounting for nearly 38% of global revenues in 2026, led by China, followed by Japan and India. High domestic production volumes, cost-efficient manufacturing, and growing vehicle demand drive cradle adoption. Government-led EV incentives in China and India and expanding urban logistics fleets accelerate demand for metallic and non-metal cradles. BYD, for example, expanded its EV subframe and engine cradle production in Shenzhen, supporting modular EV platforms and large-scale domestic distribution. ASEAN countries are increasingly becoming manufacturing hubs, attracting foreign direct investment from global OEMs seeking regional efficiency. Strong industrial growth and EV adoption position the region as a global supply hub.

Long-term growth in the Asia Pacific is projected to have the fastest growth with a CAGR of around 7% through 2033, driven by EV adoption, fleet electrification, and industrial expansion. OEMs are investing in lightweight and composite cradles to meet efficiency and regulatory targets. Suppliers are scaling localized production capacity to meet rising demand. Regional infrastructure and logistics initiatives further support electric fleet growth. Advanced manufacturing techniques, including robotics and digital simulation, are being deployed to reduce defects and production costs. Strategic investments from both government and private players reinforce the region’s leadership. Asia Pacific is set to remain the dominant market and fastest-growing region globally.

Competitive Landscape

The global automotive engine cradle market structure is moderately consolidated, with leading suppliers such as Hyundai Mobis, Gestamp, Magna International, Thyssenkrupp, and Faurecia collectively controlling a significant portion of the revenue. These companies leverage long-standing OEM relationships, advanced engineering capabilities, and expertise in metallic and composite subframe systems. They also invest heavily in R&D for lightweighting, EV-compatible architectures, and NVH-optimized designs, maintaining technological leadership across passenger and commercial vehicle segments.

Regional and niche suppliers, including Schaeffler, Bharat Forge, and Yapp Automotive, focus on specialized segments or strongholds in emerging markets such as India, ASEAN, and Eastern Europe. Barriers to entry, including high capital requirements, complex supply chain integration, and compliance with crash and safety regulations, limit new competitors. However, trends such as EV electrification and modular vehicle platforms are creating opportunities for suppliers to collaborate with software, simulation, and advanced manufacturing technology providers. Market consolidation is expected to continue gradually, with global leaders pursuing strategic acquisitions and regional expansions, while smaller suppliers differentiate through niche capabilities and innovation partnerships.

Key Industry Developments

- In October 2025, Benteler signed a Memorandum of Understanding (MoU) with Chenzhi Group to form a joint venture focused on intelligent chassis systems and structural components for new energy vehicles in the Chengdu-Chongqing region. The collaboration integrates R&D efforts to develop next-generation “chassis + battery + body” designs, enhancing new energy vehicle (NEV) underbody architecture capacity and manufacturing capabilities.

- In October 2025, Benteler Group inaugurated a new module plant in Beijing, China, through a joint venture with BHAP. The facility has a designed annual capacity of 350,000 chassis suspension modules for Beijing Benz vehicles, expanding Benteler’s presence in China and reinforcing collaboration with local partners to support future mobility solutions.

- In July 2025, Japanese automotive supplier Astemo announced a £100 million investment to establish a new EV inverter production line at its Bolton, UK factory. Supported by the UK government’s Automotive Transformation Fund, the project will create around 220 high-skilled jobs and establish the UK’s first domestic production capability for advanced EV components, strengthening Europe’s EV supply chain.

Companies Covered in Automotive Engine Cradle Market

- Magna International

- Gestamp Automoción

- Benteler Group

- ZF Friedrichshafen AG

- Tenneco

- Aisin Corporation

- Hyundai Mobis

- Martinrea International

- Tower International

- Yorozu Corporation

- JBM Auto

- NHK Spring

Frequently Asked Questions

The global automotive engine cradle market is projected to reach US$ 5.4 billion in 2026.

The key drivers include rising global vehicle production, modular vehicle platform adoption, stringent safety and emission regulations, and growing electrification of passenger and commercial vehicles.

The market is expected to grow at a CAGR of 6% from 2026 to 2033.

Opportunities lie in EV-optimized lightweight cradle designs, expansion in light commercial vehicle fleets, and adoption of advanced manufacturing technologies such as hydroforming, robotic welding, and digital twin simulation.

Hyundai Mobis, Gestamp, Magna International, Thyssenkrupp, Faurecia, Bharat Forge, and Yapp Automotive are some of the leading players.