- Medical Devices

- Assistive Technology (AT) Market

Assistive Technology (AT) Market Size, Share, and Growth Forecast, 2026 - 2033

Assistive Technology (AT) Market by Device Type (Mobility Aids, Hearing Aids, Vision Aids, Communication Aids), End-User (Hospitals, Clinics, Home Care Settings), Portability (Portable, Non-Portable), and Regional Analysis for 2026-2033

Assistive Technology (AT) Market Share and Trends Analysis

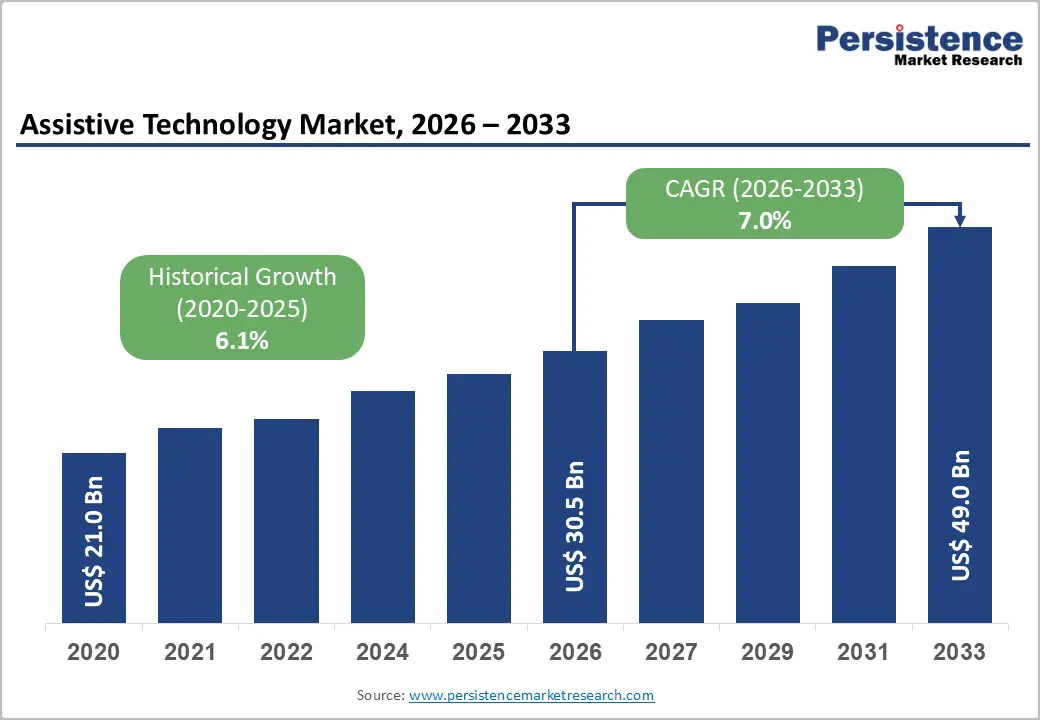

The global assistive technology (AT) market size is likely to be valued at US$ 30.5 billion in 2026, and is projected to reach US$ 49.0 billion by 2033, growing at a CAGR of 7% during the forecast period 2026−2033. This expansion is mainly occurring due to aging demographics across developed economies and the increasing prevalence of chronic conditions that require long-term support. Stakeholders are presently observing a rise in the number of individuals with disabilities, which is fueling the demand for specialized solutions such as mobility aids and hearing devices. Progressive government initiatives are actively supporting this trend by mandating strict accessibility standards in both public and private infrastructure. Technological convergence is currently enabling the development of more sophisticated and user-friendly devices that improve independence for diverse populations.

Engineers are presently integrating Artificial Intelligence (AI), Internet of Things (IoT) connectivity, and miniaturized sensors into everyday assistive tools. These advancements are transforming traditional hardware into intelligent systems that can monitor health metrics and automate home environments in real time. These smart technologies are rapidly elevating the quality of life for millions of users by providing more intuitive navigation and communication options.

Key Industry Highlights

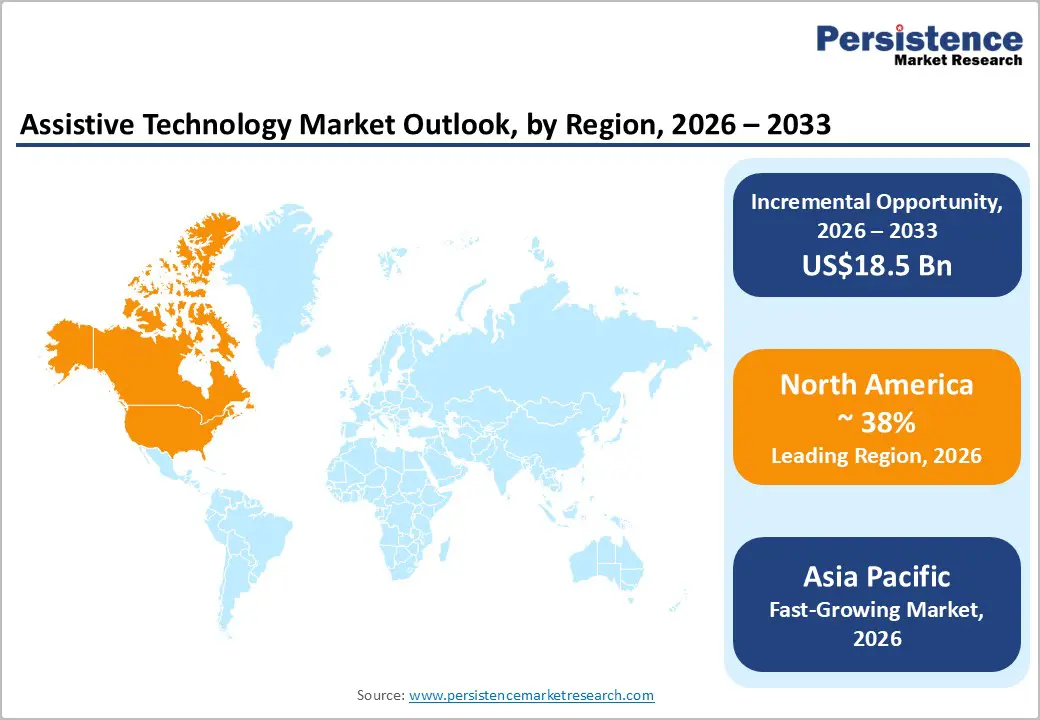

- Dominant Region: North America is expected to command about 38% of the AT market share in 2026, supported by high healthcare spending and strong legal protections for individuals with disabilities.

- Fastest-growing Region: The Asia Pacific market is slated to be the fastest-growing through 2033, due to the rapid demographic changes and strong expansion in healthcare and long-term care infrastructure.

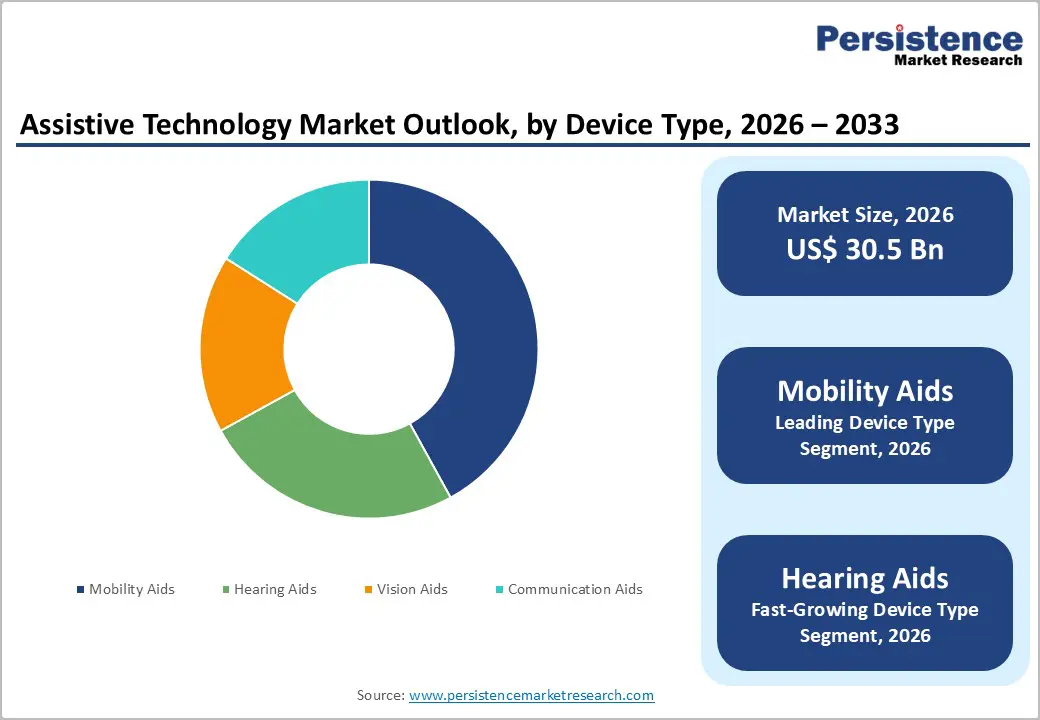

- Leading & Fastest-growing Device Types: Mobility aids are likely to hold approximately 42% of the revenue share in 2026, while hearing aids are set to be the fastest-growing segment during the 2026-2033 forecast period.

- End-User Dominance: Home care settings are poised to dominate with around 58% revenue share in 2026, whereas hospitals are expected to be the fastest-growing segment over the 2026-2033 forecast period.

- January 2026: Verdane acquired a majority stake in Smartbox, a global provider of augmentative and alternative communication (AAC) software and hardware, accelerating Smartbox’s international growth and expanding access to its assistive technology solutions.

| Key Insights | Details |

|---|---|

| Assistive Technology (AT) Market Size (2026E) | US$ 30.5 Bn |

| Market Value Forecast (2033F) | US$ 49.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Accelerating Population Aging and Disability Prevalence

The World Health Organization (WHO) estimates that over 1.3 billion people globally experience significant disability, representing approximately 16% of the world's population. This reality, combined with persistent gaps in care delivery, is shifting healthcare systems and families toward solutions that support independence rather than exclusive reliance on institutional care. Assistive technologies now sit at the intersection of healthcare, consumer electronics, and rehabilitation services, creating a durable demand base that is less exposed to short-term economic fluctuations. Organizations that recognize these evolving needs can position assistive products not only as medical devices, but also as essential enablers of meaningful participation in work, education, and community life.

Demographic trends further strengthen the structural case for AT adoption, as population profiles evolve across both advanced and middle-income economies. Rapid aging is reshaping household spending priorities, with families increasingly seeking practical solutions that help older adults remain mobile, communicate clearly, and manage daily activities in their own homes. The rising prevalence of chronic conditions such as arthritis, cardiovascular diseases, and neurological disorders across a wider range of age groups is broadening the potential user base well beyond older adults, reinforcing long-term demand for these solutions.

Technological Complexity and User Adoption Challenges

Increasing sophistication in assistive technologies can unintentionally limit real-world adoption, especially among older adults who often have lower levels of digital confidence and experience. Many solutions now rely on elements such as complex user interfaces, smartphone connectivity, and regular software updates, which can feel overwhelming without tailored guidance. When users do not receive structured onboarding, practical demonstrations, or accessible troubleshooting support, they may struggle to build trust in the device and fail to incorporate it into daily routines in a consistent way.

This highlights the importance of human-centered design and service models that emphasize simplicity, familiarity, and consistent support across the entire product lifecycle. Organizations can mitigate abandonment risks by investing in intuitive interfaces, optional low-technology operating modes, and coordinated training programs for both users and caregivers. More interoperable ecosystems, where mobility aids, hearing solutions, and daily living assistance products operate together seamlessly, can also reduce cognitive burden and make multi-device environments easier to manage. This approach improves user satisfaction and strengthens long-term adherence, while enhancing perceived value for payers, healthcare providers, and families.

Artificial Intelligence and Robotics Enabling Next-Generation Assistive Solutions

Advancements in robotics, computer vision, and machine learning are reshaping the next wave of assistive technologies and broadening what is possible for users with mobility and sensory limitations. Emerging categories such as robotic exoskeletons for gait assistance, AI-enabled prosthetics with more natural movement patterns, and autonomous navigation systems for people with visual impairments are moving from research settings into everyday use. These developments signal a shift from purely compensatory devices toward solutions that can restore functional capabilities and support more independent living in home, community, and workplace environments.

Robotic prosthetics and autonomous wheelchairs show how hardware, software, and neuroscience are converging into integrated platforms rather than remaining separate devices. Neural interface technologies that interpret muscle or nerve signals, when combined with embedded sensors and adaptive algorithms, enable more intuitive control and can provide a degree of sensory feedback that improves user confidence and everyday usability. Autonomous wheelchair systems that rely on technologies such as lidar, depth-sensing cameras, and computer vision support safer navigation in crowded or unfamiliar environments, reduce caregiver burden, and enhance access to public spaces.

Category-wise Analysis

Device Type Insights

Mobility aids are poised to dominate in 2026, commanding approximately 42% of the assistive technology market revenue share. This leadership position reflects the fundamental prevalence of mobility-related disabilities across aging populations and individuals with physical impairments. The segment encompasses wheelchairs (manual and powered), walkers, canes, crutches, mobility scooters, and patient lifting systems. Widespread insurance reimbursement coverage across developed markets through Medicare, Medicaid, and private health insurance reduces financial adoption barriers for prescribed mobility devices. Distribution advantages through established medical equipment retailers, pharmacy chains, and expanding e-commerce platforms ensure broad market accessibility.

Hearing aids are likely to be the fastest-growing segment during the 2026-2033 forecast period. Modern hearing aids integrate Bluetooth connectivity, enabling direct smartphone streaming, artificial intelligence algorithms that automatically adjust settings based on environmental acoustics, and rechargeable battery systems, eliminating disposable battery maintenance. Rising awareness of untreated hearing loss, cognitive decline and dementia risk drives proactive adoption among aging populations seeking preventive health interventions. The technological breakthroughs in miniaturization, digital signal processing, and wireless connectivity have dramatically improved device performance and user experience.

End-User Insights

Home care settings are slated to lead with approximately 58% of the AT market revenue share in 2026. This leadership reflects the fundamental trend of aging-in-place, where elderly populations and individuals with disabilities prioritize remaining in familiar residential environments rather than relocating to institutional care facilities. The segment encompasses individual consumers purchasing devices for personal use, family caregivers supporting disabled or elderly relatives, and professional home healthcare agencies providing in-home medical services. Healthcare cost containment pressures across developed markets incentivize early discharge from hospitals and rehabilitation centers, shifting ongoing care to home settings where assistive technologies enable safe, independent living.

Hospitals are expected to be the fastest-growing segment over the 2026-2033 forecast period, driven by global healthcare infrastructure expansion and increased regulatory emphasis on patient safety and accessibility standards. Modern hospitals require comprehensive assistive technology portfolios, including patient lifting systems, specialized hospital beds with advanced positioning capabilities, mobility aids for rehabilitation departments, communication devices for speech-impaired patients, and accessibility equipment ensuring ADA compliance throughout facilities. Value-based care models incentivize hospitals to invest in assistive technologies that reduce patient fall incidents, prevent pressure ulcers, accelerate rehabilitation outcomes, and enable earlier discharge, thereby improving quality metrics and reducing readmission penalties.

Portability Insights

The non-portable segment is anticipated to lead with an approximate 54% of the AT market share in 2026. Non-portable assistive technologies are designed for stationary installation in residential, clinical, or institutional settings. This segment includes permanent home modifications such as stairlifts, ceiling-mounted patient lift systems, roll-in showers, height-adjustable hospital beds, stationary standing frames, and fixed accessibility infrastructure. Healthcare facilities prioritize durable, high-capacity stationary equipment designed for intensive daily use across multiple patients, with institutional-grade devices commanding premium pricing reflecting enhanced load capacities, infection control features, and extended service life requirements.

Portable devices are projected to be the fastest-growing segment during the 2026-2033 forecast period. This segment encompasses foldable wheelchairs, collapsible walkers, portable oxygen concentrators, travel-sized hearing aids, portable communication devices, lightweight mobility scooters, and wearable assistive technologies. Technological innovations enabling substantial weight reduction without compromising structural integrity drive adoption, with carbon fiber wheelchairs weighing under 18 pounds providing full functionality while fitting standard vehicle trunks. The increasing prevalence of remote work and digital connectivity enables disabled professionals to maintain flexible lifestyles, creating demand for portable solutions supporting mobility.

Regional Insights

North America Assistive Technology (AT) Market Trends

North America is set to command a significant portion of the assistive technology market share at an estimated 38% in 2026, underpinned by high healthcare spending, strong legal protections for individuals with disabilities, and relatively broad reimbursement coverage. The United States sets the tone for regional demand, as disability rights legislation such as the Americans with Disabilities Act (ADA) embeds accessibility expectations into public infrastructure, workplaces, transport, and digital services, which in turn drives sustained uptake of assistive solutions across mobility, communication, and daily living categories. Canada reinforces regional growth through universal healthcare coverage and provincial assistive device programs that provide structured funding mechanisms for equipment acquisition, supporting more equitable access for eligible users.

North America offers a highly attractive innovation and commercialization environment, but it also presents nuanced access constraints that market participants must navigate. The United States Food and Drug Administration (FDA) provides clear regulatory pathways for assistive products that qualify as medical devices, which supports clinical credibility and investor confidence while also setting a high bar for safety, effectiveness, and evidence generation. Manufacturers, payers, and policymakers, this combination of advanced infrastructure and persistent affordability barriers highlights the need for pricing models, service bundles, and funding partnerships that preserve innovation incentives while improving financial accessibility for a broader user base.

Europe Assistive Technology (AT) Market Trends

Europe represents a highly significant market for assistive technologies, underpinned by strong social welfare models, statutory health insurance structures, and a long-standing commitment to accessibility and universal design principles. Germany anchors regional demand through its extensive statutory health insurance system and advanced engineering capabilities, which support early adoption of high-specification mobility aids, prosthetics, and rehabilitation devices. The United Kingdom, France, Spain, and Italy provide additional scale through large, publicly funded health systems and growing focus on aging-in-place and community-based care. Nordic countries reinforce the region’s strategic importance by embedding accessibility into urban planning and public services, which encourages routine use of assistive solutions in transport, education, and workplace environments.

The regional market gains additional strength from close collaboration between public authorities, healthcare providers, research institutions, and private manufacturers, which supports continuous innovation and robust evidence generation. Joint initiatives such as pilot programs, structured procurement frameworks, and standardized guidelines help accelerate the adoption of new solutions in everyday environments such as homes, workplaces, schools, and public transport. This environment creates opportunities to co-design products with users and payers, align portfolios with reimbursement requirements, and scale successful models across multiple countries while remaining responsive to local regulatory and funding conditions.

Asia Pacific Assistive Technology (AT) Market Trends

Asia Pacific is anticipated to be the fastest-growing market for assistive technologies, driven by rapid demographic aging, rising household incomes, and strong expansion in healthcare and long-term care infrastructure. China anchors regional demand through large-scale investment in elderly care facilities, disability support services, and domestic device manufacturing, which together create both volume and cost advantages across core categories such as mobility aids, hearing solutions, and daily living assistance products. Japan combines universal healthcare coverage, advanced robotics capabilities, and a strong policy focus on aging in place, positioning the country as a test bed for sophisticated solutions that support independent living and ease pressure on formal care systems. India and other large emerging economies add further momentum as governments implement accessibility legislation, disability rights frameworks, and national campaigns that promote inclusive infrastructure and strengthen awareness among both providers and consumers.

Manufacturing strengths in countries such as China, Taiwan, and South Korea support cost-competitive production and enable regional and global scaling, but limited insurance coverage in many markets still makes assistive technology largely an out-of-pocket purchase, which concentrates adoption in urban and higher-income segments. Gaps in rehabilitation capacity, uneven distribution networks, and infrastructure constraints in parts of Southeast Asia can delay uptake outside major cities, while stigma associated with visible disability aids in some society’s drives preference for discreet, aesthetically minimalist designs that resemble consumer electronics rather than traditional medical equipment.

Competitive Landscape

Leading market participants such as Invacare Corporation, Sunrise Medical, Ottobock SE, Permobil AB, and Medline Industries are currently maintaining a dominant presence within the moderately fragmented assistive technology market landscape. These industry leaders are collectively control nearly 40% of the total market share through expansive global distribution networks. The competitive environment is presently fostering continuous innovation and targeted product upgrades to strengthen strategic market positioning. These organizations are further solidifying their influence by forming strategic partnerships and broadening their integrated solution offerings. This consolidation of expertise is ensuring that the sector remains highly competitive while delivering robust financial performance.

Market participants are currently prioritizing research & development (R&D) to deliver advanced, user-centric assistive devices that address a wide spectrum of functional needs. This sustained focus on technological progress is actively creating a steady pipeline of next-generation products, such as intelligent mobility aids and AI-powered sensory systems. Industry experts are presently identifying this commitment to innovation as a critical determinant of long-term differentiation and relevance. By 2033, manufacturers will have successfully integrated more sophisticated sensors and user-friendly interfaces into their core portfolios to enhance patient autonomy. This ongoing evolution is ensuring that assistive technologies continue to meet the complex requirements of an aging global population.

Key Industry Developments

- In October 2025, Motorica, a global MedTech company specializing in assistive technologies, launched a Digital Prosthetics Program in India that uses 3D scanning, digital modeling, and 3D printing to produce highly customized mechanical prosthetic arms more quickly and accurately than traditional mold-based methods.

- In July 2025, IIIT Allahabad signed a MoU with STPI and its subsidiary STPINEXT to set up a Centre of Entrepreneurship in assistive technology in Prayagraj, creating an ecosystem to support startups developing solutions for persons with disabilities, the elderly, and people with special needs.

- In June 2025, WHO/Europe released a Guide for Assistive Technology (AT) Market Assessment and Shaping to help countries and stakeholders understand and improve AT markets through targeted interventions, practical frameworks, and tools for assessing supply, demand, pricing, and distribution. The guide emphasizes collaboration with the private sector, stakeholder mapping, and examples from recent assessments to support wider access to wheelchairs, hearing aids, prosthetics, and communication devices.

Companies Covered in Assistive Technology (AT) Market

- Invacare Corporation

- Sunrise Medical

- Ottobock SE

- Permobil AB

- Pride Mobility Products Corporation

- Drive DeVilbiss Healthcare

- Medline Industries

- GF Health Products

- Arjo

- Handicare Group

- Karman Healthcare

- WHILL Inc.

- Tobii Dynavox

- Ekso Bionics

Frequently Asked Questions

The global assistive technology (AT) market is projected to reach US$ 30.5 billion in 2026.

The market is driven by aging populations, rising prevalence of disabilities and chronic conditions, supportive policy and reimbursement frameworks, and rapid advances in digital, sensor, and robotics technologies.

The market is poised to witness a CAGR of 7% from 2026 to 2033.

Integration of AI and IoT into assistive solutions, growth of home- and community-based care, and increasing focus on inclusive design across consumer and healthcare ecosystems are generating novel opportunities.

Invacare Corporation, Sunrise Medical, Ottobock SE, Permobil AB, and Medline Industries are some of the key players in the market.