- Executive Summary

- Global Turbine Control System Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Turbine Market Overview

- Global Turbine Market by Type

- Forecast Factors – Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 – 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Turbine Control System Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Global Turbine Control System Market Outlook: Turbine Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by Turbine Type, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Turbine Type, 2026-2033

- Steam Turbine

- Gas Turbine

- Market Attractiveness Analysis: Turbine Type

- Global Turbine Control System Market Outlook: Function

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by Function, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Function, 2026-2033

- Speed Control

- Temperature Control

- Load Control

- Pressure Control

- Market Attractiveness Analysis: Function

- Global Turbine Control System Market Outlook: Component

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by Component, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Component, 2026-2033

- Hardware

- Software

- Market Attractiveness Analysis: Component

- Global Turbine Control System Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Turbine Control System Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) Forecast, by Turbine Type, 2026-2033

- Steam Turbine

- Gas Turbine

- North America Market Size (US$ Bn) Forecast, by Function, 2026-2033

- Speed Control

- Temperature Control

- Load Control

- Pressure Control

- North America Market Size (US$ Bn) Forecast, by Component, 2026-2033

- Hardware

- Software

- Europe Turbine Control System Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) Forecast, by Turbine Type, 2026-2033

- Steam Turbine

- Gas Turbine

- Europe Market Size (US$ Bn) Forecast, by Function, 2026-2033

- Speed Control

- Temperature Control

- Load Control

- Pressure Control

- Europe Market Size (US$ Bn) Forecast, by Component, 2026-2033

- Hardware

- Software

- East Asia Turbine Control System Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) Forecast, by Turbine Type, 2026-2033

- Steam Turbine

- Gas Turbine

- East Asia Market Size (US$ Bn) Forecast, by Function, 2026-2033

- Speed Control

- Temperature Control

- Load Control

- Pressure Control

- East Asia Market Size (US$ Bn) Forecast, by Component, 2026-2033

- Hardware

- Software

- South Asia & Oceania Turbine Control System Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Turbine Type, 2026-2033

- Steam Turbine

- Gas Turbine

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Function, 2026-2033

- Speed Control

- Temperature Control

- Load Control

- Pressure Control

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Component, 2026-2033

- Hardware

- Software

- Latin America Turbine Control System Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) Forecast, by Turbine Type, 2026-2033

- Steam Turbine

- Gas Turbine

- Latin America Market Size (US$ Bn) Forecast, by Function, 2026-2033

- Speed Control

- Temperature Control

- Load Control

- Pressure Control

- Latin America Market Size (US$ Bn) Forecast, by Component, 2026-2033

- Hardware

- Software

- Middle East & Africa Turbine Control System Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) Forecast, by Turbine Type, 2026-2033

- Steam Turbine

- Gas Turbine

- Middle East & Africa Market Size (US$ Bn) Forecast, by Function, 2026-2033

- Speed Control

- Temperature Control

- Load Control

- Pressure Control

- Middle East & Africa Market Size (US$ Bn) Forecast, by Component, 2026-2033

- Hardware

- Software

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- ABB

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Siemens Energy

- Eaton

- General Electric

- Schneider Electric

- Honeywell International

- Voith GmbH & Co. KGaA

- Emerson Electric Co.

- Rockwell Automation

- Yokogawa Electric Corporation

- Mitsubishi Electric Corporation

- WOODWARD

- Vestas

- Danfoss

- ANDRITZ

- ABB

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Renewable Energy

- Turbine Control System Market

Turbine Control System Market Size, Share, and Growth Forecast 2026 - 2033

Turbine Control System Market by Turbine Type (Steam Turbine, Gas Turbine), by Function (Speed Control, Temperature Control, Load Control, Pressure Control), by Component (Hardware, Software), and Regional Analysis for 2026 - 2033

Turbine Control System Market Size and Trend Analysis

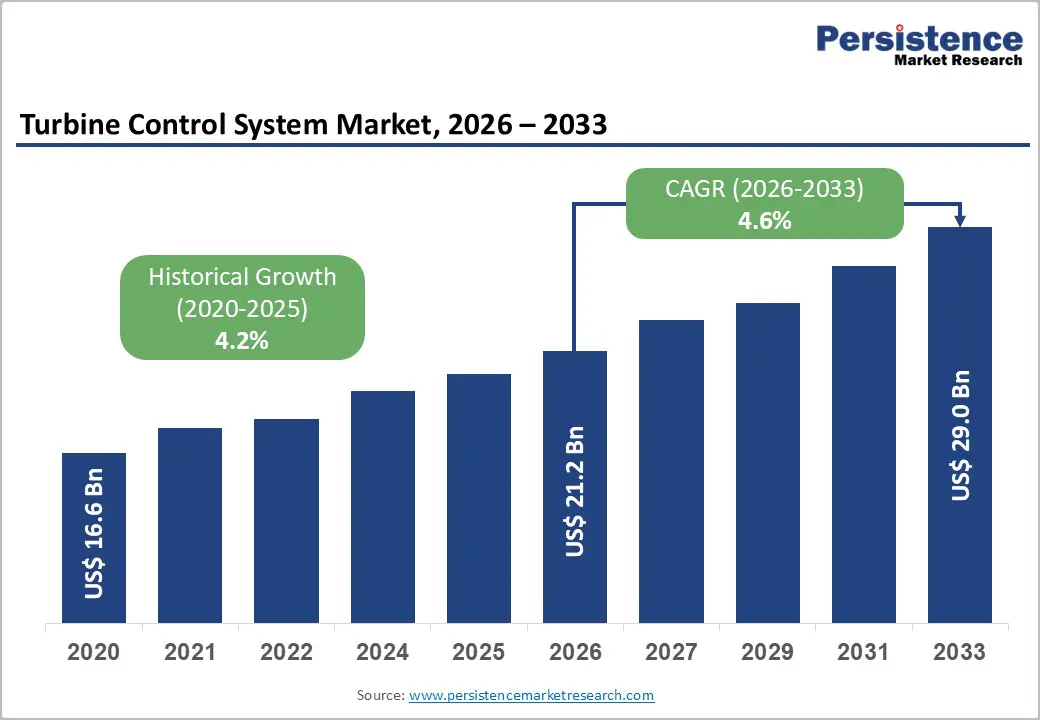

The global Turbine Control System market size is supposed to be valued at US$ 21.2 Billion in 2026 and is projected to reach US$ 29.0 Billion by 2033, growing at a CAGR of 4.6% between 2026 and 2033. The market's consistent and sustained growth is underpinned by the global power generation sector's accelerating investment in digital automation, operational efficiency optimization, and grid-reliability enhancement across gas and steam turbine fleets, both new and aging.

Key Industry Highlights:

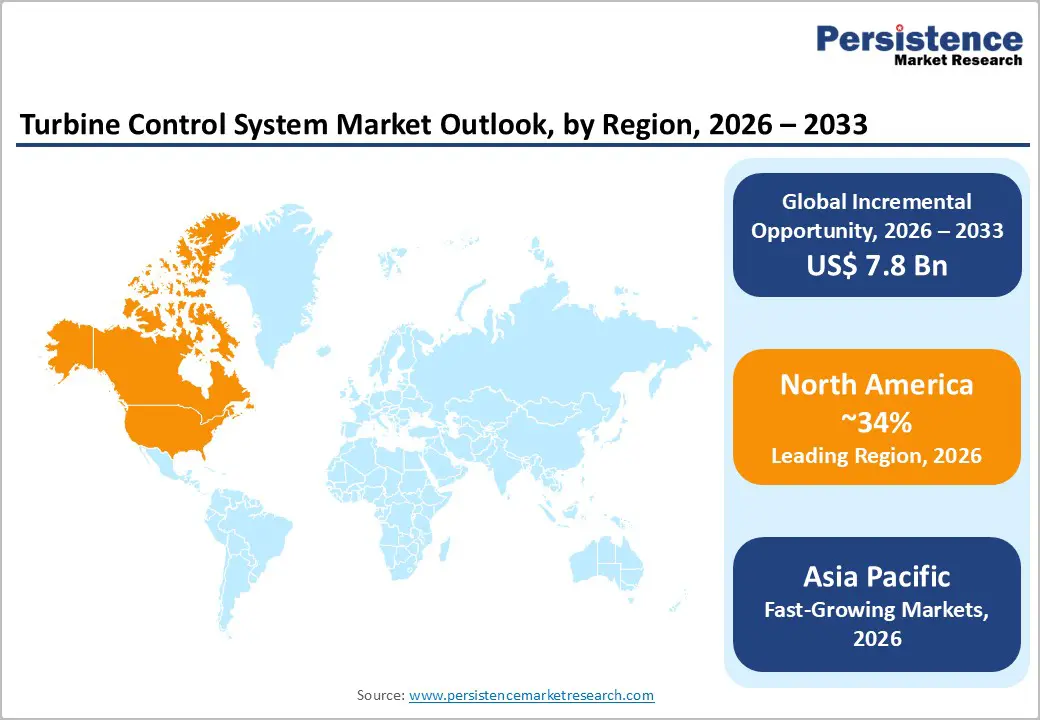

- Dominant Region: North America leads the global Turbine Control System market, anchored by the U.S. EIA's confirmation that natural gas-fired plants generated approximately 43% of total U.S. electricity in 2024, ensuring the world's largest gas turbine control system procurement volume, compounded by mandatory NERC CIP cybersecurity and EPA emissions monitoring compliance driving continuous system upgrades.

- Growing Region: Asia Pacific is the fastest-growing region, driven by China's NEA adding over 200 GW of new power capacity in 2024 and India's National Electricity Plan targeting 80+ GW of additional thermal generation by 2032, collectively generating the highest incremental turbine control system procurement volumes of any global region through the forecast period.

- Dominant Turbine Type: Gas Turbines dominate the Turbine Type segment with approximately 43% revenue share, driven by gas turbines' dual role as baseload generators and rapid-response backup to renewable energy sources, requiring the most sophisticated and continuously active control system architectures.

- Growing Component: Software is the fastest-growing component, expanding at above-average rates fueled by AI-powered analytics, digital twin platforms, and cloud-based remote monitoring subscriptions, with the gas turbine control software market projected to exceed US$ 2 Billion by 2034 as recurring software revenue models gain adoption across utility and industrial operators globally.

- Opportunity: Wind turbine control system expansion represents the key market opportunity, with the IEA confirming record 120 GW of global wind capacity additions in 2024 and accelerating offshore wind programs across Europe, China, and the U.S. creating structurally growing demand for ruggedized, AI-integrated turbine control platforms engineered for remote and harsh marine operating environments.

| Key Insights | Details |

|---|---|

|

Turbine Control System Market Size (2026E) |

US$ 21.2 Billion |

|

Market Value Forecast (2033F) |

US$ 29.0 Billion |

|

Projected Growth CAGR (2026–2033) |

4.6% |

|

Historical Market Growth (2020–2025) |

4.2% |

Market Dynamics

Drivers - Accelerating Digitalization and AI Integration in Turbine Operations Driving Advanced Control System Adoption

The integration of Artificial Intelligence (AI), machine learning (ML), and Industrial Internet of Things (IIoT) technologies into turbine control systems is fundamentally reshaping the global market, generating strong demand for next-generation digital control platforms that deliver real-time performance optimization, predictive maintenance, and automated fault detection capabilities.

Siemens Energy's SPPA-T3000 control system and WOODWARD's IIoT-prepared turbine controllers, which feature high-speed data logging and triple modular redundant (TMR) configurations, exemplify the market's rapid advancement toward intelligent, fail-safe digital control architectures. The IEA's digital infrastructure investment benchmarks confirm that power sector digitalization globally attracted over US$ 50 billion in investment in 2023 alone, with turbine control systems representing a significant share of this critical digital infrastructure spending.

Aging Global Turbine Fleet and Grid Modernization Programs Creating Large Retrofit Demand Pipeline

The global power generation industry maintains an extensive installed base of aging gas and steam turbines equipped with legacy analog and first-generation digital control systems that are increasingly unable to meet modern performance, emissions, and cybersecurity requirements, creating a massive and structurally durable retrofit and modernization demand pipeline. The U.S. Department of Energy (DOE) has documented that a significant proportion of the U.S. power generation fleet consists of gas turbines installed before 2000, many of which require urgent control system upgrades to comply with EPA's emissions monitoring and reporting requirements and to enable NERC CIP cybersecurity compliance.

The North American Electric Reliability Corporation (NERC) reported in its 2024 Long-Term Reliability Assessment that grid flexibility requirements are increasing substantially due to rising renewable penetration, compelling turbine fleet operators to invest in advanced control systems capable of faster ramp rates and improved frequency response. Retrofit turbine control contracts, such as GE Power Systems' acquisition of WOODWARD's turbine control retrofit business, demonstrate the scale of commercial opportunity in this high-growth aftermarket segment.

Restraints - High Initial Capital Investment and Long Payback Periods Deterring Smaller Operator Upgrades

The implementation of advanced turbine control systems, particularly full DCS-based or triple-redundant digital control architectures for large gas and steam turbine installations, requires substantial upfront capital investment in hardware, software licensing, engineering, installation, and operator training, often ranging from several hundred thousand to multiple millions of U.S. dollars per turbine unit.

For smaller independent power producers, industrial plant operators in developing markets, and utility operators managing large distributed turbine fleets, these high capital requirements create significant budget constraints that can extend decision timelines and defer or cancel upgrade projects. The World Bank's global energy access data confirms that financing remains the primary bottleneck for infrastructure modernization in Sub-Saharan Africa and parts of South Asia, limiting market penetration in price-sensitive growth regions.

Cybersecurity Vulnerabilities in Networked Digital Control Systems Raising Operational Risk Concerns

The increasing connectivity of turbine control systems through IIoT, cloud integration, and enterprise-level SCADA networks has dramatically expanded the attack surface for cyberattacks targeting critical power infrastructure, creating a restraint that simultaneously elevates the technical requirements and compliance costs for turbine control system deployment. The U.S. Cybersecurity and Infrastructure Security Agency (CISA) has repeatedly identified industrial control systems in power generation facilities as high-priority cyberattack targets, noting that sophisticated threat actors have demonstrated the capability to disrupt turbine operations through network intrusion.

NERC CIP standards in North America and the EU Network and Information Security (NIS2) Directive in Europe impose mandatory cybersecurity standards for operational technology (OT) systems, including turbine control platforms, requiring costly security assessments, architecture hardening, and incident response capability investments that add meaningful overhead to turbine control system procurement and operational budgets.

Opportunity - Wind Turbine Control System Expansion Driven by Global Renewable Energy Capacity Buildout

The global renewable energy sector's unprecedented expansion, particularly in wind power, is creating a structurally growing and commercially significant new demand category for turbine control system manufacturers, as wind turbines require sophisticated, multi-parameter real-time control systems fundamentally different from conventional thermal turbine control architectures. The IEA's Renewables 2024 Report confirmed that global wind power capacity additions exceeded 120 GW in 2024 alone, the highest annual addition ever recorded, bringing cumulative global wind capacity to over 1,100 GW. Each newly commissioned wind turbine requires a dedicated control system managing pitch control, yaw control, speed regulation, power output optimization, and grid compliance monitoring simultaneously.

Vestas, the world's leading wind turbine manufacturer, and Siemens Gamesa have developed proprietary advanced turbine control platforms that integrate real-time SCADA monitoring, predictive maintenance algorithms, and AI-driven energy yield optimization. The accelerating offshore wind program commitments across Europe, China, and the United States are driving particular demand for ruggedized, remote-capable turbine control systems engineered for harsh marine operating environments where human access for maintenance is severely limited and system reliability is non-negotiable.

Gas Turbine Modernization and Combined Cycle Power Plant Expansion Creating Premium Control System Demand

The global power generation sector's accelerating transition toward Combined Cycle Gas Turbine (CCGT) plants, prized for their industry-leading thermal efficiencies of 60–63% and rapid operational flexibility required to complement intermittent renewable generation, is creating elevated demand for the most advanced and sophisticated turbine control system architectures available. The IEA's World Energy Outlook 2024 projects that gas-fired power generation will play a critical transitional role in global electricity systems through at least 2035, as the primary dispatchable backup to solar and wind capacity, ensuring sustained large-scale investment in CCGT plant construction and associated turbine control modernization.

General Electric's HA-series gas turbines, currently the world's highest-efficiency commercial gas turbines at 63.08% combined cycle efficiency, require state-of-the-art multi-parameter control platforms that orchestrate thousands of sensor inputs, combustion dynamics management, and emissions compliance monitoring in real time. The U.S. DOE's gas turbine technology advancement programs, and Siemens Energy's global CCGT project pipeline, reportedly exceeding 30 GW in backlog as of 2024, collectively ensure a sustained multi-year procurement demand for premium turbine control systems across the forecast period.

Category-wise Insights

By Turbine Type

The gas turbine segment leads the global Turbine Control System market by turbine type, commanding approximately 43% of total turbine type segment revenue in 2026. Gas turbines' market leadership in control system adoption is anchored in their critical and growing role as both baseload power generators and rapid-response peaking units in electricity systems experiencing rising renewable energy penetration volatility. Gas turbine control systems demand the most sophisticated real-time management architectures, monitoring and regulating combustion temperature, compressor pressure ratios, turbine speed, exhaust emissions, and fuel-air mixture simultaneously to maintain thermodynamic performance within extremely narrow operating bands.

GE's HA-series and Siemens Energy's SGT series turbines require control platforms certified to IEC 61511 functional safety standards and API 670 vibration monitoring compliance, reflecting the high technical specification baseline for premium gas turbine control procurement. The Steam Turbine segment remains substantial, driven by nuclear, coal, and industrial process steam applications, but grows more slowly due to the sector's less rapid fleet expansion compared to gas turbine deployment.

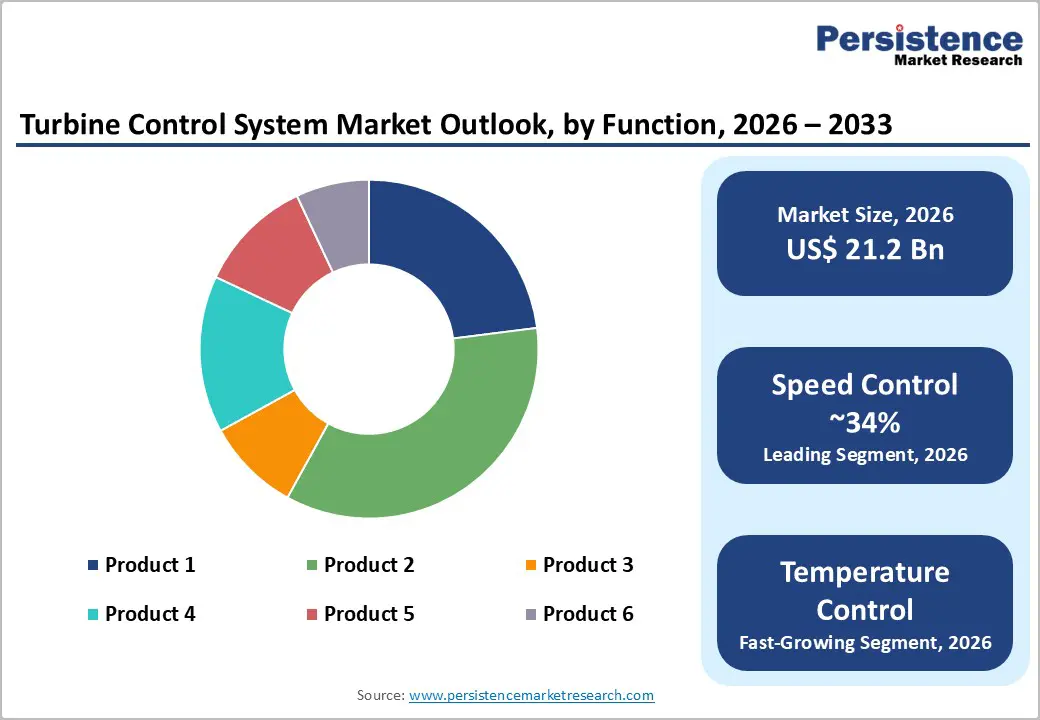

By Function

The speed control function segment leads the global Turbine Control System market by function, accounting for approximately 34% of total function segment revenue in 2026. Speed control is the most fundamental and universally required function across all turbine types, governing the precise rotational speed of turbine shafts to maintain synchronous frequency output (50 Hz or 60 Hz) at grid interconnection points in accordance with NERC, ENTSO-E, and national grid code requirements. Any deviation from target speed, whether due to load changes, fuel supply variations, or mechanical disturbances, must be corrected within milliseconds to prevent grid instability, making speed control the most safety-critical and continuously active control function in any turbine operation. WOODWARD's governors and speed control systems, engineered for both aeroderivative and heavy-duty gas turbines in simplex, dual-redundant, and triple modular redundant configurations, represent the commercial benchmark for high-reliability speed control technology globally.

The temperature control function is the fastest-growing segment, driven by intensifying emissions compliance requirements and combustion efficiency optimization in gas turbines, where precise turbine inlet temperature management is the primary lever for maximizing thermal efficiency while maintaining NOx and CO emissions within regulatory limits.

By Component

The hardware component segment leads the global Turbine Control System market, representing approximately 62% of total component segment revenue in 2026. Turbine control hardware, encompassing programmable logic controllers (PLCs), distributed control system (DCS) cabinets, sensors, actuators, governors, I/O modules, human-machine interfaces (HMIs), and communication network infrastructure, constitutes the foundational physical layer of every turbine control system installation and commands the largest share of project capital expenditure in both new installations and retrofit projects. The hardware segment's dominance reflects the capital-intensive nature of turbine control system architecture, where specialized high-reliability components rated for industrial-grade temperature, vibration, and electromagnetic interference environments carry significant per-unit price premiums compared to commercial-grade equivalents.

ABB, Rockwell Automation, and Emerson Electric are the market's leading hardware platform providers, offering fully integrated turbine control cabinets with embedded functional safety certification. The Software segment is the fastest-growing component, expanding at notably above-average rates driven by the rise of AI-powered analytics platforms, digital twin simulation environments, and cloud-based remote monitoring subscriptions that create recurring revenue streams for control system vendors beyond the initial hardware sale.

Regional Insights

North America Turbine Control System Market Trends

North America leads the global Turbine Control System market, anchored by the United States' position as the world's largest single gas turbine power generation fleet operator and the most advanced regulatory ecosystem for turbine control digitalization and cybersecurity compliance. The U.S. EIA reported that natural gas-fired power plants generated approximately 43% of U.S. net electricity in 2024, the single largest source of U.S. power generation, ensuring the nation's gas turbine control system market remains the world's highest-volume by revenue. NERC CIP standards, EPA's Clean Air Act monitoring requirements, and the DOE's grid modernization programs collectively create a dense regulatory framework that mandates continuous turbine control system upgrades across the U.S. power generation fleet.

GE Vernova, Emerson Electric, and WOODWARD, all headquartered in the United States, are the dominant North American turbine control system suppliers, maintaining deeply embedded customer relationships with major utilities including Duke Energy, NextEra Energy, and Dominion Energy. The U.S. Inflation Reduction Act (IRA)'s investment tax credits for clean energy generation are stimulating a new wave of combined cycle gas turbine plant construction and existing gas turbine retrofit projects, both of which require state-of-the-art turbine control system procurement. Canada contributes through its extensive hydropower turbine control modernization programs managed under provincial utility frameworks including Hydro-Québec and BC Hydro, which are actively upgrading legacy governor and control systems to meet modern grid code compliance standards.

Europe Turbine Control System Market Trends

Europe is a technology-leadership market for turbine control systems, driven by the continent's complex and rapidly evolving electricity grid dynamics, characterized by the world's highest renewable energy penetration rates, that impose the most demanding flexibility, frequency response, and ramp-rate requirements on dispatchable turbine fleets. Germany leads European turbine control system demand, underpinned by its extensive combined cycle gas turbine infrastructure serving as critical backup capacity for the country's expanding solar and wind generation fleet. Siemens Energy, headquartered in Munich, Germany, maintains global technology leadership in both gas turbine systems and their associated digital control platforms through its SPPA-T3000 system and growing portfolio of AI-enhanced turbine performance optimization solutions.

The European Union's Fit for 55 package and the EU Emissions Trading System (EU ETS), which imposes increasing carbon costs on gas-fired power generation, are compelling operators to maximize turbine thermal efficiency through advanced control system optimization, creating a strong economic incentive for premium control system adoption across European turbine fleets. France's nuclear fleet, operated by EDF, is undergoing a major control system modernization program as part of the Grand Carénage life-extension project, generating substantial procurement demand for steam turbine control system upgrades at scale. ABB and Yokogawa Electric are expanding their European turbine control service networks to capture the growing demand for control system life-cycle management services across the continent's aging turbine infrastructure.

Asia Pacific Turbine Control System Trends

Asia Pacific is the fastest-growing regional market for turbine control systems globally, propelled by the region's massive ongoing power generation capacity expansion, concentrated in China, India, Japan, and ASEAN, which is deploying both new gas-fired combined cycle plants and undertaking large-scale modernization of legacy coal and gas turbine fleets. China's National Energy Administration (NEA) confirmed that the country added over 200 GW of new power generation capacity in 2024 alone, the largest single-year capacity addition of any country in history, with gas turbines forming a critical part of China's flexible power generation infrastructure alongside its dominant coal and renewables fleet. China's State Grid Corporation and China Southern Power Grid are actively upgrading turbine control systems across their vast distributed turbine fleets to meet national grid stability and renewable integration mandates.

India's power sector is undergoing transformative expansion under the National Electricity Plan 2023–2032, which targets adding over 80 GW of thermal generation capacity by 2032 alongside massive renewable additions, sustaining significant procurement demand for both new turbine control installations and retrofit programs across NTPC's and state utility fleets. Japan's post-Fukushima energy security strategy has re-emphasized gas turbine combined cycle development, with Mitsubishi Electric and Yokogawa Electric serving as the dominant domestic turbine control system suppliers for major Japanese utility projects. ASEAN economies, particularly Vietnam, Indonesia, and Thailand, are rapidly expanding gas-fired power generation infrastructure to fuel industrial growth, generating growing procurement demand for turbine control systems that local manufacturers are beginning to supply cost-competitively, complementing imports from global leaders.

Competitive Landscape

The global Turbine Control System market is moderately consolidated at the premium technology tier, with a small number of global industrial automation and power equipment leaders, Siemens Energy, GE Vernova, ABB, Emerson Electric, Honeywell International, and WOODWARD, collectively dominating the high-value new installation and OEM-integrated control system segments. These players differentiate through proprietary control platform architectures, IEC 61511 functional safety certification portfolios, embedded AI analytics capabilities, and comprehensive lifecycle service agreements that create substantial customer switching costs.

Emerging business model trends include turbine performance-as-a-service, where control system vendors share in fuel savings and efficiency gains, and cloud-based remote monitoring subscription models generating recurring revenue. Mid-tier specialists including Yokogawa Electric and Mitsubishi Electric compete effectively in Asia Pacific through localization and deep OEM turbine manufacturer partnerships.

Key Developments

- In January 2025, Siemens Energy announced an expanded partnership with Microsoft to integrate Azure-based AI analytics into its SPPA-T3000 turbine control platform, enabling predictive combustion optimization and remote performance monitoring for gas turbine operators across its global installed base.

- In February 2024, GE Power Systems completed the acquisition of WOODWARD Governor Company's turbine control retrofit business, strengthening its aftermarket position in industrial turbine control upgrades across power generation, gas processing, and hydropower sectors.

- In 2024, WOODWARD launched its next-generation ProTech TPS turbine protection system featuring enhanced IIoT connectivity, high-speed data logging, and triple modular redundant configurations, targeting both new gas turbine installations and retrofit applications in industrial power generation globally.

Companies Covered in Turbine Control System Market

- ABB

- Siemens Energy

- Eaton

- General Electric

- Schneider Electric

- Honeywell International

- Voith GmbH & Co. KGaA

- Emerson Electric Co.

- Rockwell Automation

- Yokogawa Electric Corporation

- Mitsubishi Electric Corporation

- WOODWARD

- Vestas

- Danfoss

- ANDRITZ

- Hitachi

Frequently Asked Questions

The global Turbine Control System market is estimated to be valued at US$ 21.2 Billion in 2026 and is projected to reach US$ 29.0 Billion by 2033, registering a forecast CAGR of 4.6% between 2026 and 2033. The market recorded a historical growth rate of 4.2% CAGR between 2020 and 2025, supported by power sector digitalization and grid modernization investment globally.

The key growth drivers are the global power sector's accelerating adoption of AI, IIoT, and digital control architectures, with power sector digitalization attracting over US$ 50 billion in annual global investment per the IEA, and the extensive retrofit demand from the aging global turbine fleet, catalyzed by mandatory NERC CIP cybersecurity standards and EPA emissions monitoring compliance requirements compelling continuous control system upgrades.

Gas Turbines lead the Turbine Type category with approximately 43% revenue share in 2026, corroborated by the confirmed 43.40% platform share in 2025. Gas turbines' leadership reflects their critical dual role as baseload generators and rapid-response peaking units requiring the most sophisticated real-time multi-parameter control systems, managing combustion temperature, speed, emissions, and pressure simultaneously within millisecond response requirements.

North America leads the global Turbine Control System market, anchored by the United States' status as the world's largest gas turbine power generation operator, with natural gas generating approximately 43% of total U.S. electricity in 2024 per the U.S. EIA. Mandatory NERC CIP cybersecurity standards and EPA emissions compliance create a continuous cycle of turbine control system upgrades across the country's extensive and aging turbine fleet.

The most significant growth opportunity is the global wind turbine control system expansion, driven by the IEA's confirmation of record 120 GW of wind capacity additions in 2024 and accelerating offshore wind programs. Each new wind turbine requires dedicated multi-parameter control systems, creating a structurally growing and high-volume demand pipeline for manufacturers developing ruggedized, AI-integrated, and remote-capable turbine control platforms.

The leading companies include Siemens Energy, General Electric (GE Vernova), ABB, Emerson Electric Co., Honeywell International, WOODWARD, Rockwell Automation, Yokogawa Electric Corporation, Mitsubishi Electric Corporation, Schneider Electric, Voith GmbH & Co. KGaA, Vestas, Eaton, Danfoss, and ANDRITZ, among other prominent technology providers operating across global turbine control system design, manufacturing, installation, and lifecycle service segments.