- Executive Summary

- Global Tugboats Market Snapshot, 2024 and 2031

- Market Opportunity Assessment, 2024 - 2031, US$ Bn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Challenges

- Key Trends

- Product Lifecycle Analysis

- Tugboats Market: Value Chain

- List of Raw Material Supplier

- List of Manufacturers

- List of Distributors

- Profitability Analysis

- Forecast Factors - Relevance and Impact

- Covid-19 Impact Assessment

- PESTLE Analysis

- Porter Five Force’s Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Service Type Landscape

- Macro-Economic Factors

- Global Sectorial Outlook

- Global GDP Growth Outlook

- Global Parent Market Overview

- Price Trend Analysis, 2019 - 2031

- Key Highlights

- Key Factors Impacting Product Prices

- Prices By Engine Power/Boat Type/Service Type

- Regional Prices and Product Preferences

- Global Tugboats Market Outlook: Historical (2019 - 2024) and Forecast (2024 - 2031)

- Key Highlights

- Market Size and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Bn) Analysis and Forecast

- Historical Market Size Analysis, 2019-2023

- Current Market Size Forecast, 2024-2031

- Global Tugboats Market Outlook: Engine Power

- Introduction / Key Findings

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Engine Power, 2019 - 2024

- Current Market Size (US$ Bn) and Volume ( Unit) Forecast By Engine Power, 2025- 2032

- <2000 HP

- 2000-5000 HP

- 5000-8000 HP

- >8000 HP.

- Market Attractiveness Analysis: Engine Power

- Global Tugboats Market Outlook: Boat Type

- Introduction / Key Findings

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Boat Type, 2019 - 2024

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Boat Type, 2025- 2032

- Conventional tug

- Tractor Tug

- Azimuthal Stern Drive (ASD) Tugs

- Others

- Market Attractiveness Analysis: Boat Type

- Global Tugboats Market Outlook: Service Type

- Introduction / Key Findings

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Service Type, 2019 - 2024

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Service Type, 2025- 2032

- Harbour Assistance

- Towage & Salvage

- Escort Services

- Offshore Support

- Ice-Breaking

- Others.

- Market Attractiveness Analysis: Service Type

- Global Tugboats Market Outlook: Fuel Type

- Introduction / Key Findings

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Fuel Type, 2019 - 2024

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Fuel Type, 2025- 2032

- Diesel

- Gasoline

- Electric

- Market Attractiveness Analysis: Fuel Type

- Key Highlights

- Global Tugboats Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Region, 2019 - 2024

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Region, 2025- 2032

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Tugboats Market Outlook: Historical (2019 - 2024) and Forecast (2025- 2032)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Market, 2019 - 2024

- By Country

- By Engine Power

- By Boat Type

- By Service Type

- By Fuel Type

- Current Market Size (US$ Bn) and Volume ( Unit) Forecast By Country, 2025- 2032

- U.S.

- Canada

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Engine Power, 2025- 2032

- <2000 HP

- 2000-5000 HP

- 5000-8000 HP

- >8000 HP.

- Current Market Size (US$ Bn) and Volume ( Unit) Forecast By Boat Type, 2025- 2032

- Conventional tug

- Tractor Tug

- Azimuthal Stern Drive (ASD) Tugs

- Others

- Current Market Size (US$ Bn) and Volume ( Unit) Forecast By Service Type, 2025- 2032

- Harbour Assistance

- Towage & Salvage

- Escort Services

- Offshore Support

- Ice-Breaking

- Others

- Current Market Size (US$ Bn) and Volume ( Unit) Forecast By Fuel Type, 2025- 2032

- Diesel

- Gasoline

- Electric

- Market Attractiveness Analysis

- Europe Tugboats Market Outlook: Historical (2019 - 2024) and Forecast (2025- 2032)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Market, 2019 - 2024

- By Country

- By Engine Power

- By Boat Type

- By Service Type

- By Fuel Type

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Country, 2025- 2032

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Rest of Europe

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Engine Power, 2025- 2032

- <2000 HP

- 2000-5000 HP

- 5000-8000 HP

- >8000 HP

- Current Market Size (US$ Bn) and Volume ( Unit) Forecast By Boat Type, 2025- 2032

- Conventional tug

- Tractor Tug

- Azimuthal Stern Drive (ASD) Tugs

- Others

- Current Market Size (US$ Bn) and Volume ( Unit) Forecast By Service Type, 2025- 2032

- Harbour Assistance

- Towage & Salvage

- Escort Services

- Offshore Support

- Ice-Breaking

- Others

- Current Market Size (US$ Bn) and Volume ( Unit) Forecast By Fuel Type, 2025- 2032

- Diesel

- Gasoline

- Electric

- Market Attractivenes Analysis

- East Asia Tugboats Market Outlook: Historical (2019 - 2024) and Forecast (2025- 2032)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Market, 2019 - 2024

- By Country

- By Engine Power

- By Boat Type

- By Service Type

- By Fuel Type

- Current Market Size (US$ Bn) and Volume ( Unit) Forecast By Country, 2025- 2032

- China

- Japan

- South Korea

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Engine Power, 2025- 2032

- <2000 HP

- 2000-5000 HP

- 5000-8000 HP

- >8000 HP

- Current Market Size (US$ Bn) and Volume ( Unit) Forecast By Boat Type, 2025- 2032

- Conventional tug

- Tractor Tug

- Azimuthal Stern Drive (ASD) Tugs

- Others

- Current Market Size (US$ Bn) and Volume ( Unit) Forecast By Service Type, 2025- 2032

- Harbour Assistance

- Towage & Salvage

- Escort Services

- Offshore Support

- Ice-Breaking

- Others

- Current Market Size (US$ Bn) and Volume ( Unit) Forecast By Fuel Type, 2025- 2032

- Diesel

- Gasoline

- Electric

- Market Attractiveness Analysis

- South Asia & Oceania Tugboats Market Outlook: Historical (2019 - 2024) and Forecast (2025- 2032)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Market, 2019 - 2024

- By Country

- By Engine Power

- By Boat Type

- By Service Type

- By Fuel Type

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Country, 2025- 2032

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Engine Power, 2025- 2032

- <2000 HP

- 2000-5000 HP

- 5000-8000 HP

- >8000 HP

- Current Market Size (US$ Bn) and Volume ( Unit) Forecast By Boat Type, 2025- 2032

- Conventional tug

- Tractor Tug

- Azimuthal Stern Drive (ASD) Tugs

- Others

- Current Market Size (US$ Bn) and Volume ( Unit) Forecast By Service Type, 2025- 2032

- Harbour Assistance

- Towage & Salvage

- Escort Services

- Offshore Support

- Ice-Breaking

- Others

- Current Market Size (US$ Bn) and Volume ( Unit) Forecast By Fuel Type, 2025- 2032

- Diesel

- Gasoline

- Electric

- Market Attractiveness Analysis

- Latin America Tugboats Market Outlook: Historical (2019 - 2024) and Forecast (2025- 2032)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Market, 2019 - 2024

- By Country

- By Engine Power

- By Boat Type

- By Service Type

- By Fuel Type

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Country, 2025- 2032

- Brazil

- Mexico

- Rest of Latin America

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Engine Power, 2025- 2032

- <2000 HP

- 2000-5000 HP

- 5000-8000 HP

- >8000 HP

- Current Market Size (US$ Bn) and Volume ( Unit) Forecast By Boat Type, 2025- 2032

- Conventional tug

- Tractor Tug

- Azimuthal Stern Drive (ASD) Tugs

- Others

- Current Market Size (US$ Bn) and Volume ( Unit) Forecast By Service Type, 2025- 2032

- Harbour Assistance

- Towage & Salvage

- Escort Services

- Offshore Support

- Ice-Breaking

- Others

- Current Market Size (US$ Bn) and Volume ( Unit) Forecast By Fuel Type, 2025- 2032

- Diesel

- Gasoline

- Electric

- Market Attractiveness Analysis

- Middle East & Africa Tugboats Market Outlook: Historical (2019 - 2024) and Forecast (2025- 2032)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Market, 2019 - 2024

- By Country

- By Engine Power

- By Boat Type

- By Service Type

- By Fuel Type

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Country, 2025- 2032

- GCC

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Engine Power, 2025- 2032

- <2000 HP

- 2000-5000 HP

- 5000-8000 HP

- >8000 HP

- Current Market Size (US$ Bn) and Volume ( Unit) Forecast By Boat Type, 2025- 2032

- Conventional tug

- Tractor Tug

- Azimuthal Stern Drive (ASD) Tugs

- Others

- Current Market Size (US$ Bn) and Volume ( Unit) Forecast By Service Type, 2025- 2032

- Harbour Assistance

- Towage & Salvage

- Escort Services

- Offshore Support

- Ice-Breaking

- Others

- Current Market Size (US$ Bn) and Volume ( Unit) Forecast By Fuel Type, 2025- 2032

- Diesel

- Gasoline

- Electric

- Market Attractiveness Analysis

- Competition Landscape

- Market Share Analysis, 2024

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Apparent Production Capacity

- Company Profiles (Details - Overview, Financials, Strategy, Recent Developments)

- Damen Shipyards Group

- Overview

- Segments and Products

- Key Financials

- Market Developments

- Market Strategy

- Sanmar Shipyards

- Ranger Tugs.

- ODC Marine

- Gladding-Hearn

- MERRÉ

- Norfolk Tug Company

- SYM Naval

- Crowley Maritime Corporation

- Cochin Shipyard Limited

- Cheoy Lee Shipyards Ltd

- mol Group

- Damen Shipyards Group

- Note: List of companies is not exhaustive in nature. It is subject to further augmentation during course of research

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Marine

- Tugboat Market

Tugboat Market Size, Share, and Growth Forecast for 2025 - 2032

Tugboat Market by Engine Type (<2000 HP, 2000-5000 HP, 5000-8000 HP, >8000 HP), Boat Type (Conventional tug, Tractor Tug, Azimuthal Stern Drive (ASD) Tugs, Others) Service Type (Harbour Assistance, Towage & Salvage, Escort Services, Offshore Support, Ice-Breaking, Others), Fuel Type ( Diesel, Gasoline, Electric) and Regional Analysis

Tugboat Market Size and Trend Analysis

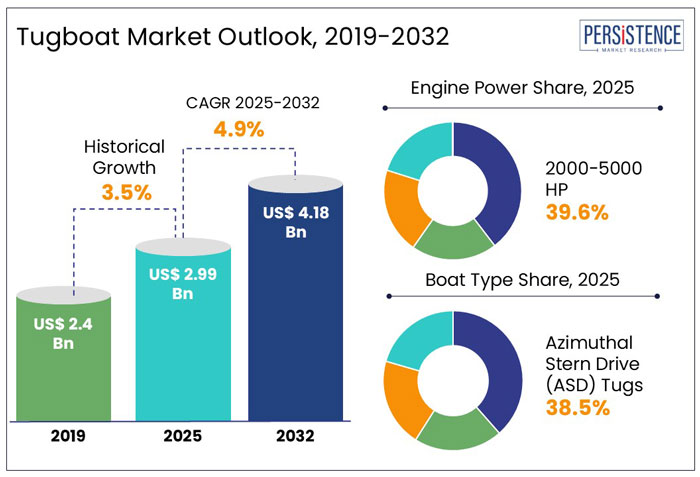

The global tugboat market size is anticipated to rise from US$ 2.99 Bn in 2025 to US$ 4.18 Bn by 2032. It is projected to witness a CAGR of 4.9% from 2025 to 2032.

In the heart of the maritime industry, a quiet yet powerful transformation is taking place. Tugboats, often seen as the workhorses of ports and harbors, are now embracing sustainability and innovation like never before.

With fleet modernization, eco-friendly designs, and the rise of electric-powered tugboats, the industry is steering toward a cleaner, more efficient future.

- Svitzer, a global leader in towage services, has emerged as a trailblazer in adopting hydrotreated vegetable oil (HVO) biofuels, making its UK fleet significantly more sustainable. With ambitious plans to expand into Australia and Europe, Svitzer is proving that greener alternatives are not just possible but practical.

- As per studies carried out by Persistence Market Research, in 2023, global maritime trade volumes surged to 12,292 million tons, marking a 2.4% increase after a dip in 2022. Over the forecast period, the sector is projected to grow by 2% in 2024 and maintain an average of 2.4% annual growth through 2029, signaling strong economic resilience and easing global pressures.

As maritime trade continues to expand, the demand for efficient and sustainable tugboat operations is set to rise. With a growing emphasis on alternative fuels and cutting-edge vessel designs, the industry is not just keeping up with change; it’s leading the way. By embracing innovation, tugboats are evolving from silent helpers to key players in a greener, more sustainable shipping future.

Key Highlights of the Market

- North America holds a 25.8% market share, driven by a robust marine economy and investments in fleet modernization.

- East Asian shipyards produce nearly 100 port-assist vessels annually, with China, Japan, and South Korea leading global deliveries.

- Azimuth Stern Drive (ASD) tugs are expected to dominate with a 38.5% market share in 2024, favored for their maneuverability and efficiency.

- Battery-electric and hybrid tugboats are gaining traction, with Svitzer investing in zero-emission vessels.

- HVO and LNG-powered tugboats are increasingly used, with Svitzer expanding its HVO fleet to Australia and Europe.

- Towage services type will account for 14% of the market share in 2025, driven by global fleet expansion and acquisitions.

- The 2,000-5,000 HP segment is set to hold a 39.6% market share, catering to the growing demand for mid-range power vessels.

|

Market Attributes |

Key Insights |

|

Market Size (2025E) |

US$ 2.99 Bn |

|

Projected Market Value (2032F) |

US$ 4.18 Mn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

4.9% |

|

Historical Market Growth Rate (CAGR 2019 to 2024) |

3.5% |

Historical Growth and Course Ahead

Stable Growth Amid Fleet Modernization

The tugboat market has been steadily evolving, adapting to the demands of a rapidly changing maritime landscape. Between 2019 and 2024, the sector experienced moderate growth, expanding at a CAGR of 3.5%. The CAGR was a reflection of increasing global trade, expanding ports, and a strong push toward fleet modernization.

Shipbuilders weren’t just designing bigger and more powerful tugboats; they were focusing on fuel efficiency and environmental compliance, ensuring vessels met strict emissions regulations.

The adoption of hybrid propulsion and NOx reduction technologies gained momentum as operators looked for ways to balance performance with environmental responsibility.

- One such milestone came on July 20, 2020, when the U.S. Department of Transportation’s SLSDC commissioned the SEAWAY GUARDIAN, the first American-built vessel for the St. Lawrence Seaway in over six decades.

A Push Toward Emissions-Free Towage Bolsters Market

As the industry looks ahead, growth is set to accelerate, with a projected CAGR of 4.9% from 2025 to 2032. But this next phase of expansion won’t just be about numbers, it will be about sustainability.

The maritime world is entering an era of battery-electric and hybrid propulsion systems, driven by stricter emissions mandates and the increasing need for efficient, eco-friendly port operations.

Shipbuilders are now doubling down on zero-emission vessels, while maritime operators are aligning investments with carbon neutrality targets to stay ahead of global regulations.

- A perfect example of this shift came on January 15, 2025, when Svitzer made headlines by ordering a battery-powered vessel for operations in the Resund Strait. The vessel was a bold statement, reinforcing Svitzer’s commitment to decarbonization and setting a new benchmark for emissions-free towage services.

The future of the tugboat industry is no longer just about power and performance; it’s about progress, sustainability, and a commitment to navigating a cleaner, greener maritime world.

Market Dynamics

Market Growth Drivers

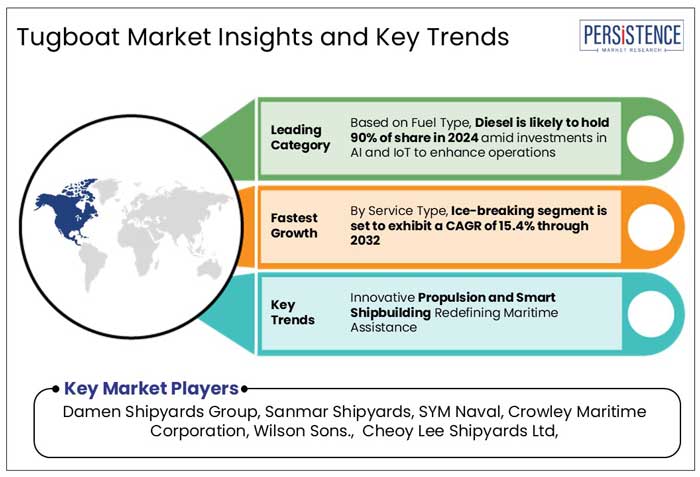

Innovative Propulsion and Smart Shipbuilding Redefining Maritime Assistance

The tugboat industry is witnessing a rapid transformation driven by strategic partnerships, fleet upgrades, and advanced propulsion systems. Shipbuilders are expanding their global reach through key agreements aimed at enhancing vessel capabilities.

- Damen Shipyards’ contract with the Lithuanian Defence Resources Agency for an ASD Tug 3010 highlights growing investment in high-performance naval support vessels.

- Damen’s partnership with Sri Lanka Shipping Company Limited marks its first supply of modern harbor support vessels to the region, reinforcing its footprint in South Asia.

These developments highlight the growing need for efficient, technology-driven workboats across commercial and defense sectors..

Standardized production models and advanced propulsion technologies are reshaping fleet efficiency and performance.

- Damen’s strategy of pre-constructing in-demand vessel types has enabled rapid deployment, as seen in the quick handover of two ASD 2312 units to Sri Lanka Shipping Company.

- Sanmar Shipyards has deepened its partnership with SCHOTTEL, making it the exclusive supplier of rudder propellers for its upgraded workboat series.

By integrating SCHOTTEL’s propulsion systems, these vessels can achieve up to 60 tons of bollard pull, enhancing maneuverability and operational capabilities. This industry-wide push for high-performance solutions ensures cost-effective and reliable vessel operations.

Sustainability is also a key driver shaping the future of maritime assistance, with ports and operators prioritizing environmentally friendly solutions.

- Damen Shipyards has launched a circular dismantling and recycling initiative, aligning with EU regulations to promote responsible vessel disposal.

- Sanmar Shipyards is advancing battery-electric models such as the ElectRA class, highlighting the industry’s shift toward decarbonization.

By integrating battery-powered propulsion, these next-generation workboats significantly reduce emissions while maintaining operational efficiency. With regulatory pressures increasing, demand for eco-conscious designs is set to rise, pushing manufacturers to accelerate innovation in sustainable vessel construction.

Market Restraining Factors

Infrastructure Gaps for Sustainable Harbor Support Vessels and Long Lifecycle of Existing Vessels Restricts Market Growth

The industries transition to sustainability is hindered by inadequate infrastructure to support green technologies. While some companies are investing in electric and methanol-powered vessels, widespread adoption depends on expanding ports with charging stations, hydrogen refueling, and methanol bunkering. Without these facilities, integrating eco-friendly harbor tugs remains impractical, limiting the shift to cleaner operations.

Aging fleets further slow modernization, with many support vessels operating beyond their expected lifespan. High replacement costs and the complexity of retrofitting older units with electric or alternative fuel engines discourage operators from upgrading. This reliance on outdated models delays sustainability efforts, making it difficult for the industry to align with global clean energy goals.

Key Market Opportunities

Collaborative Ventures Paving the Way for Advanced Tugboat Technologies

The maritime support vessel industry is witnessing rapid advancements through strategic collaborations aimed at fleet modernization and enhanced operational efficiency.

- Adani Ports’ agreement with Cochin Shipyard Ltd. to construct state-of-the-art harbor vessels in India, backed by 'Make in India' and 'Aatmanirbhar Bharat' initiatives, highlights the growing emphasis on domestic manufacturing and self-reliance in the shipbuilding sector.

Such partnerships offer significant opportunities for local and international manufacturers to tap into the increasing demand for technologically advanced maritime assist vessels.

Leading global operators are also engaging in key ventures that bolster market growth and maritime infrastructure.

- Svitzer’s collaboration with Shipyard Rio Maguari to develop 2300 Rampart Series vessels in Brazil enhances port operations across the country’s vital export hubs for commodities like grain, oil, and metals.

These developments create a strong demand for high-powered, multi-functional support ships designed for complex port and offshore operations, reinforcing opportunities for shipbuilders and technology providers focused on efficiency and safety.

The increasing investments in next-generation fleet upgrades further accelerate opportunities in sustainable and high-tech vessel solutions.

- Crowley’s introduction of the all-electric eWolf in San Diego, paired with a dedicated charging station, showcases the shift toward eco-friendly maritime operations.

As ports and shipping companies adopt greener technologies, manufacturers and innovators specializing in electric propulsion, alternative fuels, and autonomous navigation systems stand to benefit from the sectors transformation.

Tugboats Market Insights and Trends

Fuel Type Insights

Rising Adoption of Electric-Powered Support Vessels Driven by Sustainability and Regulatory Pressures

The electric-powered segment is an emerging category in the fuel type classification, currently holding a share of 42% and expected to witness substantial growth in the coming years.

Electric maritime support vessels are gaining traction as ports and fleet operators prioritize sustainability and emissions reduction. These vessels, equipped with high-capacity battery systems and shore charging infrastructure, offer a cleaner alternative to conventional fuel-powered models.

Key developments in this space reflect the growing adoption of electrified maritime solutions.

- Sanmar Shipyards' delivery of three all-electric models—HaiSea Brave, HaiSea Wamis, and HaiSea Wee'Git—to HaiSea Marine in Canada underscores the industry's commitment to reducing CO? emissions, with an expected reduction of 10,000 tonnes annually.

- SAAM Towage's integration of Dynamo I and Dynamo II at Vancouver's Neptune Terminal aligns with Teck Resources' sustainability goals, contributing to a 40% emissions intensity reduction in shipping by 2030.

The rising global demand for green port operations is set to accelerate investments in electric and hybrid-electric maritime assistance vessels across key regions, reinforcing this segment's long-term potential.

Service Type Insights

Towage services are set to hold 14% of the market share in 2025, driven by strategic acquisitions and global fleet expansions

As ports transition toward greener operations, towage providers focusing on hybrid and electric propulsion systems are expected to gain a competitive edge in the evolving market landscape.

Technological advancements and sustainability initiatives are reshaping the towage segment, with operators prioritizing high-performance and eco-friendly fleets.

- Svitzer's investment in next-generation TRAnsverse 2900 and Rampart 2300 series vessels in Brazil highlights the demand for maneuverability, fuel efficiency, and compliance with stricter environmental regulations.

Boluda Towage's acquisition of Smit Lamnalco has positioned it as the largest towage operator worldwide, enhancing operational efficiency across key maritime regions such as Australia, the Middle East, and West Africa. This consolidation trend is fueling competition and bolstering the capacity of fleet operators to meet the evolving needs of global trade and port infrastructure.

Regional Analysis

Increasing Demand for Port Assistance Vessels in East Asia to Accumulate 22.5% of the Total Market Share

East Asia remains a dominant force in ship construction, with shipyards across the region producing nearly 100 port-assist vessels annually. By mid-November 2022, around 75 such vessels had been delivered, supporting both domestic and international port operations. A major driver behind this demand is the need for modernizing fleets to handle larger vessels, including ultra-large container ships.

Chinese shipbuilders, particularly Jiangsu Zhenjiang Shipyards, led production, delivering at least 24 units and launching another 10, primarily for Chinese port operators. These new vessels, featuring azimuth stern drive (ASD) propulsion systems, offer varying power capacities to accommodate different operational requirements.

Beyond China, shipyards in Japan, South Korea, and Southeast Asia were also active in fulfilling international orders. Guangzhou Shunhai Shipyards delivered port-assist vessels to Indian and Myanmar-based operators, while Cheoy Lee Shipyards in China focused on supplying escort vessels for LNG terminal operations in the Philippines.

Japanese shipyards constructed specialized units for India's Adani Harbour Services. Indonesian and Malaysian builders also played a significant role, with multiple owners commissioning new units to support domestic and regional trade routes. This robust shipbuilding activity highlights East Asia's pivotal role in meeting the evolving needs of global port operations.

Economic Growth and Huge Investments in Boat Manufacturing Propel North America’s Market Share

North America holds a substantial market share in the global market, driven by its robust marine economy. According to the Marine Economy Satellite Account (MESA), the American marine sector contributed US$476 billion to the economy in 2022, accounting for nearly 2% of the nation’s GDP.

The industry generated $777 billion in sales and supported 2.4 million jobs, highlighting its significance in national economic growth. Investments in port infrastructure, fleet modernization, and rising maritime trade continue to drive demand for tugboats across key ports in the region.

Competitive Landscape for the Market

The tugboat market is witnessing increased competition as shipbuilders focus on sustainability, efficiency, and advanced propulsion technologies. Companies like Damen Shipyards and Sanmar Shipyards are leading with hybrid and electric tug developments, while others like Cochin Shipyard and Cheoy Lee Shipyards cater to regional demand.

Strategic partnerships with propulsion specialists such as Voith and SCHOTTEL are enhancing vessel maneuverability and fuel efficiency. As ports and offshore operators push for lower emissions, the industry is rapidly adopting battery-powered and hybrid solutions, driving a long-term transformation in the market.

Recent Industry Developments

- In November 2024, Damen Shipyards Group delivered six RSD Tugs 2513 to the Port of Antwerp-Bruges, including the first fully electric RSD-E Tug 2513 for zero-emission operations. The other five vessels feature Damen Marine NOx Reduction Systems, ensuring IMO Tier III compliance. This aligns with the port’s goal of carbon neutrality by 2050.

- In October 2024, Sanmar Shipyards began construction on four electric tugs for BOTA? Petroleum Pipeline Corporation. This project strengthens sustainable towage operations in Türkiye, highlighting a shift toward eco-friendly maritime solutions.

Companies Covered in Tugboat Market

- Damen Shipyards Group

- Sanmar Shipyards

- Ranger Tugs.

- ODC Marine

- Gladding-Hearn

- MERRÉ

- Norfolk Tug Company

- SYM Naval

- Crowley Maritime Corporation

- Cochin Shipyard Limited

- Cheoy Lee Shipyards Ltd

- mol Group

Frequently Asked Questions

The market is projected to witness a CAGR of 4.9%, growing from US$ 2.99 billion in 2025 to US$ 4.18 billion by 2032.

Azimuthal Stern Drive segment to hold a share of 38.5% in 2024.

The North America is poised to dominate the market during the forecast period.

East Asia is to capture a significant share of 22.5% by 2024.

Damen Shipyards Group, Sanmar Shipyards, SYM Naval, are the leading participants in the global market.