- Automotive Components & Materials

- Torque Converter Market

Torque Converter Market Size, Share, and Growth Forecast, 2026 – 2033

Torque Converter Market by Transmission Type (Automatic Transmission (AT), Continuously Variable Transmission (CVT), Dual-Clutch Transmission (DCT)), Component (Clutch Plate, Damper, Impeller, Stator, Turbine), Application (Passenger Cars, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs), Hybrid Vehicles), and Regional Analysis for 2026 - 2033

Torque Converter Market Share and Trends Analysis

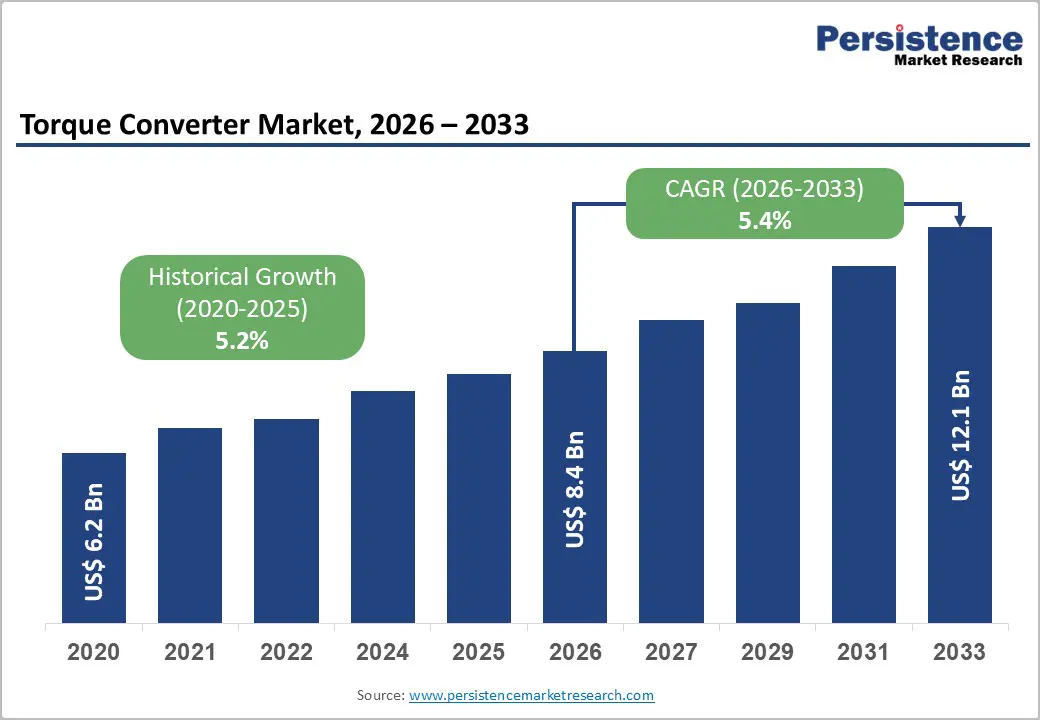

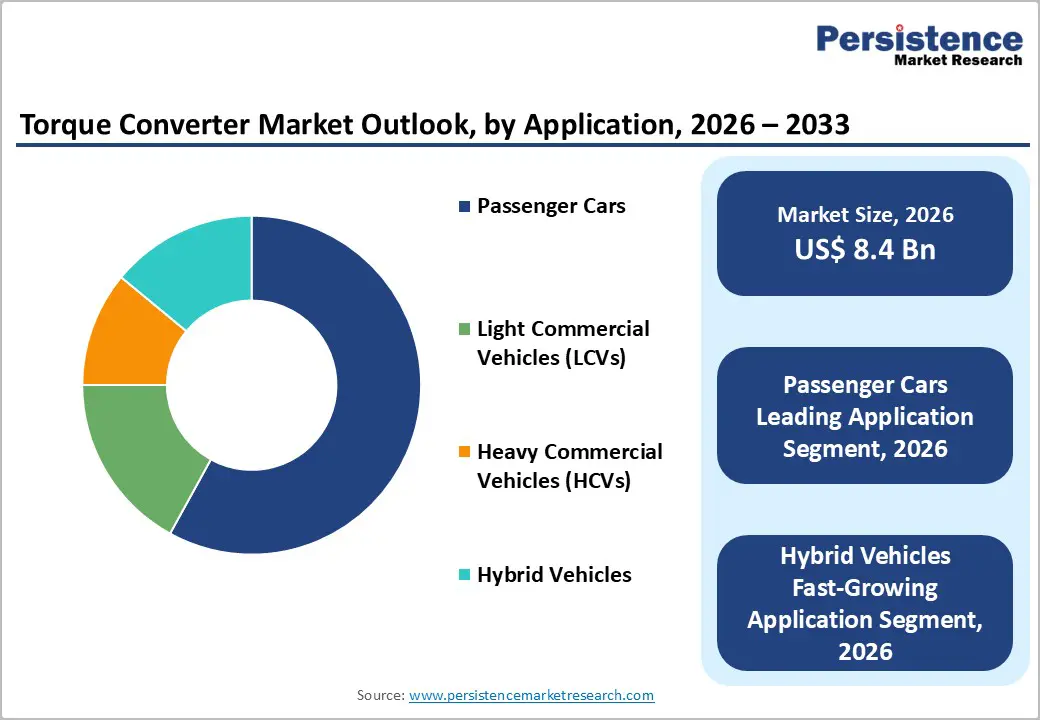

The global torque converter market size is likely to be valued at US$ 8.4 billion in 2026, and is projected to reach US$ 12.1 billion by 2033, growing at a CAGR of 5.4% during the forecast period 2026–2033.

Market expansion is primarily supported by the sustained dominance of automatic transmission vehicles, which continue to gain share across both passenger and commercial vehicle categories due to improved driving comfort, urban traffic conditions, and declining cost differentials versus manual systems. The rising penetration of hybrid powertrains further reinforces demand, as torque converters remain essential for managing frequent start-stop cycles and optimizing torque delivery in hybrid architectures.

Stringent fuel efficiency and emission regulations across North America, Europe, and Asia Pacific have accelerated original equipment manufacturer (OEM) adoption of lock-up and efficiency-optimized torque converters. Continued OEM investments in transmission optimization, durability, and noise, vibration, & harshness (NVH) reduction enhance product value, while vehicle parc expansion in Asia Pacific and steady replacement demand in mature automotive markets provide long-term structural growth stability.

Key Industry Highlights

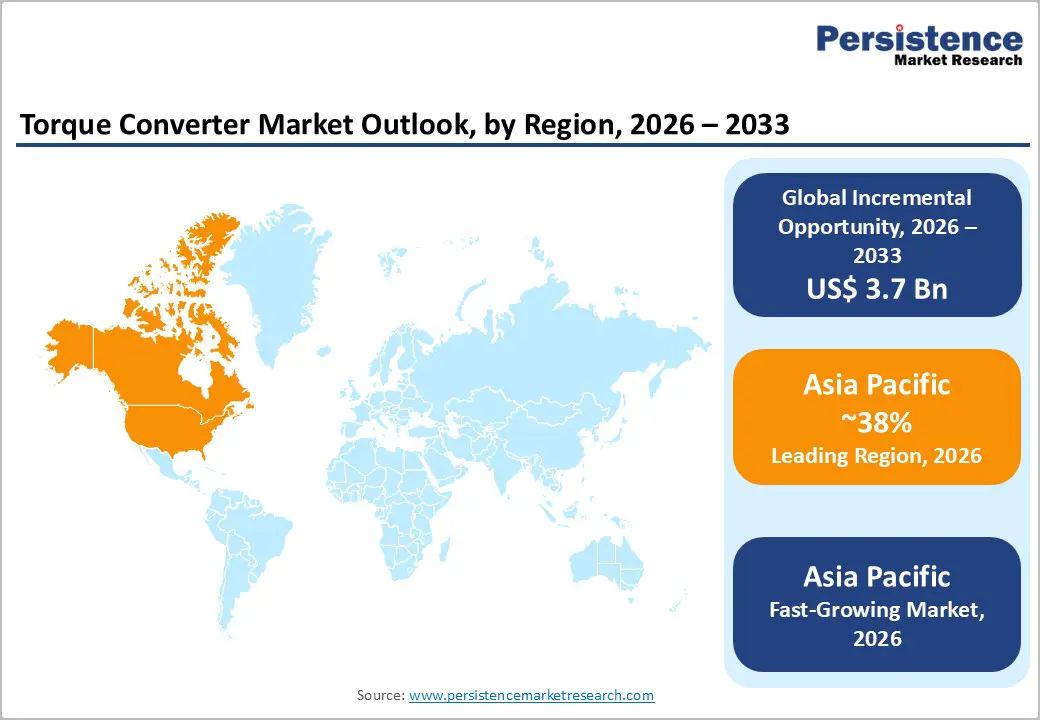

- Regional Leadership: Asia Pacific is anticipated to lead with over 38% market share in 2026 and register a 6.3% CAGR through 2033, owing to localized transmission manufacturing.

- Dominant Transmission: Automatic transmission (AT) is projected to hold around 62% revenue share in 2026, while continuously variable transmission (CVT) is set to surge through 2033, driven by fuel efficiency gains.

- Leading Component: Impellers are slated to secure about 37% revenue share in 2026, while dampers are expected to grow the fastest during 2026-2033, fueled by rising NVH control needs in hybrid powertrains.

- Leading Application: Passenger cars are expected to account for approximately 58% revenue share in 2026, while hybrid vehicles are likely to be the fastest-growing at an estimated 7.2% CAGR through 2033, boosted by tightening emission norms.

- Regulatory Impact: Fuel efficiency and emission regulations are expected to increase per-unit torque converter value, accelerating adoption of advanced lock-up and efficiency-optimized designs.

- Competitive Environment: Competitive strategies increasingly focus on localization and hybrid optimization, enabling leading suppliers to sustain the annual revenue growth through long-term OEM partnerships.

| Key Insights | Details |

|---|---|

| Torque Converter Market Size (2026E) | US$ 8.4 Bn |

| Market Value Forecast (2033F) | US$ 12.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Adoption of Automatic and Hybrid Transmission Systems

The accelerating shift toward AT systems continues to bolster torque converter demand across global vehicle platforms. OEMs are increasingly prioritizing AT solutions to improve driver comfort, enhance drivability in urban traffic, and meet tightening regulatory requirements related to fuel efficiency. As a result, automatic and semi-automatic transmissions achieved over 68% penetration in global passenger vehicle sales in 2025, reflecting a sustained move away from manual systems. Torque converters remain central to AT architectures due to their ability to deliver smooth power transfer, absorb drivetrain shock, and improve low-speed torque performance. These functional advantages make torque converters indispensable across mass-market and premium vehicle categories.

Major OEMs such as Skoda and Volkswagen have announced plans to introduce advanced 8-speed automatic torque converter transmissions in high-growth markets, including India by 2026, targeting improved fuel efficiency and compliance with evolving emission norms. At the same time, hybrid powertrain adoption is accelerating as part of OEM powertrain diversification strategies, with expanded offerings of self-charging and plug-in hybrid vehicles across global lineups. Hybrid platforms rely on optimized torque converter designs to manage frequent start-stop cycles and torque modulation, ensuring the component’s continued relevance during the transition toward electrification.

Regulatory Pressure on Efficiency and Commercial Vehicle Growth

Stringent fuel efficiency and emission regulations across major automotive markets have become a key catalyst for drivetrain optimization and torque converter enhancements. Regulatory authorities are increasingly shifting compliance focus toward fleet-wide efficiency improvements, compelling OEMs to adopt advanced transmission technologies that minimize energy losses. This has directly supported the adoption of high-efficiency and lock-up torque converters, which improve fuel economy and help reduce greenhouse gas emissions without compromising vehicle performance. As regulatory scrutiny intensifies, torque converter optimization is emerging as a cost-effective pathway for OEMs to meet tightening standards across multiple vehicle segments.

Regulatory momentum accelerated further, when the U.S. Environmental Protection Agency (EPA) finalized new tailpipe emission standards aimed at significantly reducing carbon emissions while increasing the share of hybrid and electric vehicles in the new vehicle mix. Parallel regulatory action in Asia is reinforcing this trend, with India introducing stricter fleet-average fuel efficiency norms by removing small-car concessions from 2027, thereby pushing automakers toward cleaner powertrains and efficient automatic transmissions. The sustained growth in light and heavy commercial vehicle production continues to support torque converter demand, as logistics, construction, and infrastructure sectors favor durable transmission solutions capable of delivering high torque under heavy operating loads.

Structural Shift towards Fully Electric Powertrains

The gradual transition toward battery electric vehicles (BEVs) represents a structural restraint for the torque converter market, as BEVs eliminate conventional multi-speed transmissions and associated hydraulic components. BEVs accounted for 18% of global light-vehicle sales in 2025, with especially high penetration across Europe and China, reflecting strong regulatory support and accelerating charging infrastructure deployment. In several advanced markets, policy incentives and taxation frameworks increasingly favor electric drivetrains over internal combustion platforms, directly reducing the long-term addressable market for torque converters.

This shift has become more pronounced during past years, as leading automotive markets reported record BEV adoption milestones. For example, certain European countries have reached near-total electrification of new passenger vehicle sales, signaling how rapidly internal combustion engine (ICE)-based platforms can be displaced under supportive regulation. While hybrid vehicles continue to mitigate near-term risk by retaining torque converter architectures, sustained BEV expansion could gradually cap demand beyond 2035, particularly as OEMs realign product portfolios toward fully electric platforms.

High Precision Manufacturing Requirements and Cost Sensitivity

Torque converters are high-precision mechanical assemblies requiring advanced machining, controlled heat treatment, and precise balancing to meet OEM performance and durability standards. This complexity makes them inherently cost-sensitive components. Volatility in steel and specialty alloy prices has increased component cost variability by 12–15% since 2022, placing sustained pressure on supplier margins and cost predictability. Rising energy and logistics costs across global manufacturing hubs have further compounded production challenges.

Recent industry developments have reinforced these pressures, with automotive manufacturers and suppliers publicly highlighting the impact of raw material inflation, trade-related tariffs, and supply chain disruptions on drivetrain component costs. In price-sensitive vehicle segments, particularly in emerging markets, these cost dynamics can delay the adoption of advanced torque converter designs such as multi-plate lock-up systems and enhanced dampers. As a result, suppliers face a constrained ability to pass on cost increases, underscoring the importance of scale efficiencies, localization, and process automation to protect long-term profitability.

Expansion of Hybrid Vehicle Production and Platform Commitment

Hybrid vehicles represent the most immediate and scalable growth opportunity for the torque converter market, supported by rising production volumes across major automotive regions. National automotive bodies in Japan, China, and India indicate that hybrid vehicle output is expected to exceed 14 million units annually by 2030, reinforcing hybrids as a mainstream powertrain choice. Torque converters optimized for hybrid duty cycles, incorporating reinforced dampers and advanced lock-up clutches, enable smooth torque blending and frequent start-stop operation. These enhanced designs command higher average selling prices and strengthen value realization.

In early 2026, Toyota Motor Corporation announced plans to raise hybrid and plug-in hybrid production by around 30% by 2028, with hybrids expected to account for nearly 60% of its global output across key markets. This signals a long-term commitment to hybrid architectures that continue to rely on torque converters for drivability and efficiency. Similarly, Hyundai Motor Group introduced its next-generation hybrid system in 2025, emphasizing improved torque management, fuel efficiency, and performance. Such OEM-led investments reinforce the structural relevance of torque converters within electrified powertrains. These developments enhances demand visibility and reduce adoption risk for hybrid-optimized components.

Localization of Transmission Manufacturing and Advanced Integration

Government-led localization initiatives in India, ASEAN, and Latin America present a significant opportunity for torque converter suppliers to expand regional manufacturing footprints. Policies promoting domestic automotive production, including tariff rationalization and incentive-based manufacturing programs, are reshaping supplier ecosystems. India’s Automotive Production-Linked Incentive (PLI) Scheme, which allocates over US$ 3.2 billion toward drivetrain and transmission localization, exemplifies this shift. These measures lower supply-chain risk, reduce logistics costs, and improve OEM–supplier collaboration. Localized production also enables faster customization for region-specific transmission requirements. These factors collectively create favorable conditions for new torque converter manufacturing hubs in emerging markets.

The technological integration with multi-speed automatic and hybridized transmission systems is opening niche but high-value opportunities. OEM demand for smoother shift quality, lower noise and vibration, and higher drivetrain efficiency is accelerating adoption of advanced torque converter architectures. This trend is particularly evident in premium passenger vehicles across Europe and North America, where refined driving dynamics are a key differentiator. Hybrid torque converter designs are increasingly paired with sophisticated transmission systems to balance efficiency and comfort. These integrations raise per-unit content value and strengthen supplier positioning. As transmission complexity increases, torque converters remain central to achieving performance and refinement targets.

Category-wise Analysis

Transmission Type Insights

Automatic transmission is expected to maintain its leadership in 2026, accounting for approximately 62% of the torque converter market revenue share, driven by widespread adoption across passenger cars and commercial vehicles, particularly in urbanized markets where smooth drivability is essential. AT systems rely on torque converters to ensure seamless power delivery, reduce drivetrain shock, and enhance driver comfort, reinforcing OEM preference for AT architectures. Replacement demand in mature automotive markets further supports revenue stability. This dominance is reinforced by recent OEM actions; in 2026, Hyundai announced the shift of its Santa Fe SUV from a dual-clutch system to an eight-speed torque-converter automatic, citing improved reliability and real-world performance. Such decisions highlight the sustained industry preference for torque-converter automatics in mainstream vehicle platforms.

Continuously variable transmission is projected to be the fastest-growing transmission technology, projected to expand at a CAGR exceeding 6.1% through 2033, driven by rising demand for fuel-efficient and cost-optimized drivetrains. Adoption is particularly strong in compact and mid-sized passenger vehicles across the Asia Pacific region, where mileage performance is a key purchase criterion. Automakers favor CVTs for their ability to maintain optimal engine speeds and support regulatory fuel-efficiency targets. Torque converters integrated with CVT systems are increasingly engineered for higher efficiency and improved responsiveness, addressing earlier limitations in torque handling. OEMs are standardizing these optimized CVT–torque converter pairings across high-volume models, supporting deeper penetration in price-sensitive segments and contributing meaningfully to incremental torque converter demand over the forecast period.

Application Insights

Passenger cars are likely to continue to be the largest application, holding nearly 58% of the torque converter market share in 2026. This leadership reflects high automatic transmission penetration across the passenger vehicle fleet and consistent aftermarket demand as vehicle parc ages in mature markets. Consumer preferences for comfort-oriented driving experiences and technology-enhanced vehicle performance further sustain the popularity of torque converter–equipped vehicles. Passenger cars also benefit from ongoing product refreshes that emphasize refinement and drivability, underscoring the continued role of torque converters in mainstream mobility.

Hybrid vehicles are poised to become the fastest-growing application segment, exhibiting an estimated 7.2% CAGR during the 2026-2033 forecast period, supported by government incentives and OEM electrification strategies. Torque converters designed for hybrid duty cycles are increasingly standardized across global platforms because of their ability to manage frequent start-stop transitions and blend electric and internal combustion power smoothly. A 2026 example showing hybrid application momentum is the all-new Toyota RAV4’s electrified lineup, which offers both next-generation hybrid and plug-in hybrid variants globally across North America, Japan, China, and Europe. This expansion of hybrid offerings, with deliveries rolling into 2026, reinforces torque converter relevance in transitioning powertrain architectures and supports above-average demand growth through the forecast period.

Regional Insights

North America Torque Converter Market Trends

North America is forecasted to remain a structurally important market for torque converters in 2026, with the United States acting as the primary demand anchor. Automatic transmission penetration across new vehicle sales is firmly established, creating a stable foundation for sustained demand in both passenger cars and commercial vehicles. A large and aging installed vehicle base continues to support steady aftermarket replacement activity. OEMs in the region prioritize drivability, durability, and reliability as core product attributes, reinforcing the role of torque converters in mainstream vehicle architectures. Demand dynamics are largely value-driven rather than volume-led. This supports predictable revenue streams and long product life cycles for suppliers.

Regulatory developments further reinforce this market outlook. In 2025, the U.S. EPA finalized multi-year greenhouse gas emission standards extending through 2032, compelling OEMs to achieve efficiency gains at the drivetrain level. These requirements directly support wider adoption of optimized automatic transmissions and lock-up torque converters. In parallel, General Motors announced propulsion system investment upgrades in 2026 to support next-generation automatic and hybrid transmissions at U.S. manufacturing facilities. Such investments signal continued OEM commitment to torque-converter-based platforms. These regulatory pressure and capital deployment underscore the long-term relevance of torque converters in North America.

Europe Torque Converter Market Trends

Europe is a strategically important regional market for torque converters in 2026, led by Germany, France, and the U.K. The regional automotive mix is strongly skewed toward premium and performance-oriented vehicles, where smooth torque transfer, refinement, and driving comfort are critical differentiators. While battery electric vehicle adoption continues to accelerate, hybrids retain a central role in the transitional powertrain landscape. This balance sustains torque converter demand across passenger cars and light commercial vehicles. OEMs continue to deploy automatic and hybrid transmissions across multiple segments. As a result, Europe remains a high-value, engineering-intensive market rather than a volume-led one.

The Euro 7 emission standards, formally approved in 2025, has intensified focus on real-world emissions performance and drivetrain efficiency. These standards extend compliance responsibility beyond engines to include transmission and power delivery systems. In response, Stellantis announced expanded hybrid automatic transmission production across European plants in 2026, targeting regulatory compliance without compromising driving comfort. European suppliers are increasingly prioritizing lightweight materials, advanced damping, and NVH optimization. These efforts reinforce torque converter relevance, particularly in premium and hybrid vehicle platforms.

Asia Pacific Torque Converter Market Trends

Asia Pacific is anticipated to lead with over 38% of the torque converter market value in 2026 and register a 6.3% CAGR through 2033, driven by high vehicle production and localized transmission manufacturing. China, Japan, and India dominate regional demand, supported by high vehicle production volumes and steadily rising adoption of automatic transmissions. Rapid urbanization and expanding middle-class mobility continue to shift consumer preferences toward comfort-oriented and convenience-focused vehicles. Increasing traffic congestion in major cities further strengthens demand for automatic drivetrains. A growing vehicle parc also reinforces aftermarket replacement activity. Collectively, these factors position Asia Pacific as the primary engine of global market growth.

Policy support and industrial scale continue to accelerate this momentum. In 2025, China’s Ministry of Industry and Information Technology reaffirmed hybrid vehicles as a core transitional technology, extending policy backing for efficient internal combustion and hybrid powertrains. In 2026, India approved additional disbursements under its Automotive PLI Scheme, accelerating localization of drivetrain and transmission components. These initiatives are encouraging capacity expansion and supplier investment across the region. OEMs are also deepening local sourcing strategies to improve cost competitiveness. As a result, Asia Pacific remains the most attractive long-term investment destination for global torque converter suppliers.

Competitive Landscape

The global torque converter market is moderately consolidated, with leading Tier-1 suppliers such as ZF Friedrichshafen, Aisin Corporation, BorgWarner, Schaeffler, and Valeo accounting for a significant share of global demand. These players benefit from long-standing OEM relationships, global manufacturing scale, and deep expertise in automatic and hybrid transmissions. Vertically integrated capabilities in design, precision machining, and testing strengthen entry barriers. Continuous R&D investment focuses on lock-up efficiency, NVH reduction, and thermal performance. Such strengths reinforce supplier positioning across mass-market and premium vehicle segments.

Regional and specialized suppliers remain competitive by targeting specific vehicle categories or local OEM ecosystems, particularly in Asia Pacific. High capital requirements, stringent OEM qualification processes, and durability standards continue to limit new entrants. However, localization mandates and hybrid powertrain growth are enabling regional suppliers to expand their footprint. Competitive strategies increasingly emphasize cost efficiency and proximity to OEM plants. Over the medium term, the market is expected to see selective consolidation, driven by capacity optimization, technology partnerships, and targeted acquisitions rather than broad-based mergers.

Key Industry Developments

- In February 2026, AISIN announced a ¥ 32 billion investment to expand CVT production in Haryana and establish a new automatic transmission facility in Maharashtra. The move supports India’s rapid shift toward automatic transmissions and reinforces localization under the “Make in India” initiative.

- In January 2026, Škoda launched a facelifted Kushaq SUV featuring a segment-first eight-speed torque-converter AT, enhancing driving refinement and fuel efficiency for the compact SUV class. The update strengthens Škoda’s competitive positioning in the Indian market by offering advanced transmission technology previously unavailable at this level.

- In October 2025, Hyundai Motor India unveiled the second-generation Venue compact sport utility vehicle (SUV), introducing a diesel automatic variant for the first time, powered by a 1.5-litre U2 common rail direct injection (CRDi) engine paired with a six-speed torque converter automatic transmission. The updated lineup retains existing petrol options while adding advanced drive modes and traction control features.

Companies Covered in Torque Converter Market

- ZF Friedrichshafen AG

- Aisin Corporation

- BorgWarner Inc.

- Schaeffler AG

- Valeo SA

- Exedy Corporation

- Continental AG

- Punch Powertrain

- Allison Transmission

- Sonnax Industries

- Jatco Ltd.

- Magna International

Frequently Asked Questions

The global torque converter market is projected to reach US$ 8.4 billion in 2026.

Increasing automatic transmission penetration, sustained hybrid vehicle adoption, and soaring demand for improved drivability and efficiency are driving the market.

The market is poised to witness a CAGR of approximately 5.4% from 2026 to 2033.

Opportunities are concentrated in hybrid powertrain integration, lightweight component innovation, and vehicle manufacturing automation in developing economies.

ZF Friedrichshafen, Aisin Corporation, BorgWarner, Schaeffler, and Valeo, are a few among the leading players in the market.