- Executive Summary

- Global Specialty Paper Market Snapshot, 2025 and 2032

- Market Opportunity Assessment, 2025 - 2032, US$ Bn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Key Trends

- Macro-economic Factors

- Global Sectoral Outlook

- Global GDP Growth Outlook

- COVID-19 Impact Analysis

- Forecast Factors - Relevance and Impact

- Value Added Insights

- Tool Adoption Analysis

- Regulatory Landscape

- Value Chain Analysis

- PESTLE Analysis

- Porter’s Five Force Analysis

- Price Analysis, 2024A

- Key Highlights

- Key Factors Impacting Deployment Costs

- Pricing Analysis, By Component Type

- Global Specialty Paper Market Outlook

- Key Highlights

- Market Volume (Units) Projections

- Market Size (US$ Bn) and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast

- Historical Market Size (US$ Bn) Analysis, 2019-2024

- Market Size (US$ Bn) Analysis and Forecast, 2025 - 2032

- Global Specialty Paper Market Outlook: Product Type

- Introduction / Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Product Type, 2019 - 2024

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2025 - 2032

- Packaging Papers

- Décor Papers

- Labeling Papers

- Office & Thermal Papers

- Carbonless Papers

- Kraft Papers

- Release Liners

- Others

- Market Attractiveness Analysis: Product Type

- Global Specialty Paper Market Outlook: Material

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis, By Material, 2019 - 2024

- Market Size (US$ Bn) Analysis and Forecast, By Material, 2025 - 2032

- Virgin Fiber

- Recycled Fiber

- Blended Fiber Compositions

- Specialty Pulp Mixtures

- Market Attractiveness Analysis: Material

- Global Specialty Paper Market Outlook: Functionality

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Functionality, 2019 - 2024

- Market Size (US$ Bn) Analysis and Forecast, By Functionality, 2025 - 2032

- Barrier & Grease-Proof

- Anti-Microbial

- Electrical Insulation

- Filtration

- Release Liner

- Digital-Print Substrates

- Market Attractiveness Analysis: Functionality

- Global Specialty Paper Market Outlook: Distribution Channel

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Distribution Channel, 2019 - 2024

- Market Size (US$ Bn) Analysis and Forecast, By Distribution Channel, 2025 - 2032

- Converters & Packers

- Industrial Direct Sales

- Specialty Retail

- Online B2B Channels

- Market Attractiveness Analysis: Distribution Channel

- Key Highlights

- Global Specialty Paper Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Region, 2019 - 2024

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Region, 2025 - 2032

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Specialty Paper Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2019 - 2024

- By Country

- By Product Type

- By Material

- By Functionality

- By Distribution Channel

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 - 2032

- U.S.

- Canada

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2025 - 2032

- Packaging Papers

- Décor Papers

- Labeling Papers

- Office & Thermal Papers

- Carbonless Papers

- Kraft Papers

- Release Liners

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Material, 2025 - 2032

- Virgin Fiber

- Recycled Fiber

- Blended Fiber Compositions

- Specialty Pulp Mixtures

- Market Size (US$ Bn) Analysis and Forecast, By Functionality, 2025 - 2032

- Barrier & Grease-Proof

- Anti-Microbial

- Electrical Insulation

- Filtration

- Release Liner

- Digital-Print Substrates

- Market Size (US$ Bn) Analysis and Forecast, By Distribution Channel, 2025 - 2032

- Converters & Packers

- Industrial Direct Sales

- Specialty Retail

- Online B2B Channels

- Market Attractiveness Analysis

- Europe Specialty Paper Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2019 - 2024

- By Country

- By Product Type

- By Material

- By Functionality

- By Distribution Channel

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 - 2032

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Türkiye

- Rest of Europe

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2025 - 2032

- Packaging Papers

- Décor Papers

- Labeling Papers

- Office & Thermal Papers

- Carbonless Papers

- Kraft Papers

- Release Liners

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Material, 2025 - 2032

- Virgin Fiber

- Recycled Fiber

- Blended Fiber Compositions

- Specialty Pulp Mixtures

- Market Size (US$ Bn) Analysis and Forecast, By Functionality, 2025 - 2032

- Barrier & Grease-Proof

- Anti-Microbial

- Electrical Insulation

- Filtration

- Release Liner

- Digital-Print Substrates

- Market Size (US$ Bn) Analysis and Forecast, By Distribution Channel, 2025 - 2032

- Converters & Packers

- Industrial Direct Sales

- Specialty Retail

- Online B2B Channels

- Market Attractiveness Analysis

- East Asia Specialty Paper Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2019 - 2024

- By Country

- By Product Type

- By Material

- By Functionality

- By Distribution Channel

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 - 2032

- China

- Japan

- South Korea

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2025 - 2032

- Packaging Papers

- Décor Papers

- Labeling Papers

- Office & Thermal Papers

- Carbonless Papers

- Kraft Papers

- Release Liners

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Material, 2025 - 2032

- Virgin Fiber

- Recycled Fiber

- Blended Fiber Compositions

- Specialty Pulp Mixtures

- Market Size (US$ Bn) Analysis and Forecast, By Functionality, 2025 - 2032

- Barrier & Grease-Proof

- Anti-Microbial

- Electrical Insulation

- Filtration

- Release Liner

- Digital-Print Substrates

- Market Size (US$ Bn) Analysis and Forecast, By Distribution Channel, 2025 - 2032

- Converters & Packers

- Industrial Direct Sales

- Specialty Retail

- Online B2B Channels

- Market Attractiveness Analysis

- South Asia & Oceania Specialty Paper Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2019 - 2024

- By Country

- By Product Type

- By Material

- By Functionality

- By Distribution Channel

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 - 2032

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2025 - 2032

- Packaging Papers

- Décor Papers

- Labeling Papers

- Office & Thermal Papers

- Carbonless Papers

- Kraft Papers

- Release Liners

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Material, 2025 - 2032

- Virgin Fiber

- Recycled Fiber

- Blended Fiber Compositions

- Specialty Pulp Mixtures

- Market Size (US$ Bn) Analysis and Forecast, By Functionality, 2025 - 2032

- Barrier & Grease-Proof

- Anti-Microbial

- Electrical Insulation

- Filtration

- Release Liner

- Digital-Print Substrates

- Market Size (US$ Bn) Analysis and Forecast, By Distribution Channel, 2025 - 2032

- Converters & Packers

- Industrial Direct Sales

- Specialty Retail

- Online B2B Channels

- Market Attractiveness Analysis

- Latin America Specialty Paper Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2019 - 2024

- By Country

- By Product Type

- By Material

- By Functionality

- By Distribution Channel

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 - 2032

- Brazil

- Mexico

- Rest of Latin America

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2025 - 2032

- Packaging Papers

- Décor Papers

- Labeling Papers

- Office & Thermal Papers

- Carbonless Papers

- Kraft Papers

- Release Liners

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Material, 2025 - 2032

- Virgin Fiber

- Recycled Fiber

- Blended Fiber Compositions

- Specialty Pulp Mixtures

- Market Size (US$ Bn) Analysis and Forecast, By Functionality, 2025 - 2032

- Barrier & Grease-Proof

- Anti-Microbial

- Electrical Insulation

- Filtration

- Release Liner

- Digital-Print Substrates

- Market Size (US$ Bn) Analysis and Forecast, By Distribution Channel, 2025 - 2032

- Converters & Packers

- Industrial Direct Sales

- Specialty Retail

- Online B2B Channels

- Market Attractiveness Analysis

- Middle East & Africa Specialty Paper Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2019 - 2024

- By Country

- By Product Type

- By Material

- By Functionality

- By Distribution Channel

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 - 2032

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2025 - 2032

- Packaging Papers

- Décor Papers

- Labeling Papers

- Office & Thermal Papers

- Carbonless Papers

- Kraft Papers

- Release Liners

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Material, 2025 - 2032

- Virgin Fiber

- Recycled Fiber

- Blended Fiber Compositions

- Specialty Pulp Mixtures

- Market Size (US$ Bn) Analysis and Forecast, By Functionality, 2025 - 2032

- Barrier & Grease-Proof

- Anti-Microbial

- Electrical Insulation

- Filtration

- Release Liner

- Digital-Print Substrates

- Market Size (US$ Bn) Analysis and Forecast, By Distribution Channel, 2025 - 2032

- Converters & Packers

- Industrial Direct Sales

- Specialty Retail

- Online B2B Channels

- Market Attractiveness Analysis

- Competition Landscape

- Market Share Analysis, 2024

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Company Profiles (Details - Overview, Financials, Strategy, Recent Developments)

- Mondi Group

- Overview

- Segments and Product Types

- Key Financials

- Market Developments

- Market Strategy

- Stora Enso Oyj

- Sappi Ltd

- UPM-Kymmene Corporation

- Domtar Corporation

- International Paper Company

- Ahlstrom-Munksjö Oyj

- Nippon Paper Industries Co., Ltd.

- Pixelle Specialty Solutions

- Glatfelter Corporation

- Twin Rivers Paper Company

- Burgo Group S.p.A.

- ITC Limited

- Daio Paper Corporation

- Oji Holdings Corporation

- Pudumjee Paper Products Ltd

- Fedrigoni S.p.A.

- Schweitzer-Mauduit International, Inc. (SWM)

- Kruger Inc.

- Verso Corporation

- Mondi Group

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Smart Packaging

- Specialty Paper Market

Specialty Paper Market Size, Share, and Growth Forecast, 2025 - 2032

Specialty Paper Market By Product Type (Packaging Papers, Décor Papers, Others), Material (Virgin Fiber, Recycled Fiber, Others), Functionality, Distribution Channel, and Regional Analysis for 2025 - 2032

Specialty Paper Market Size and Trends Analysis

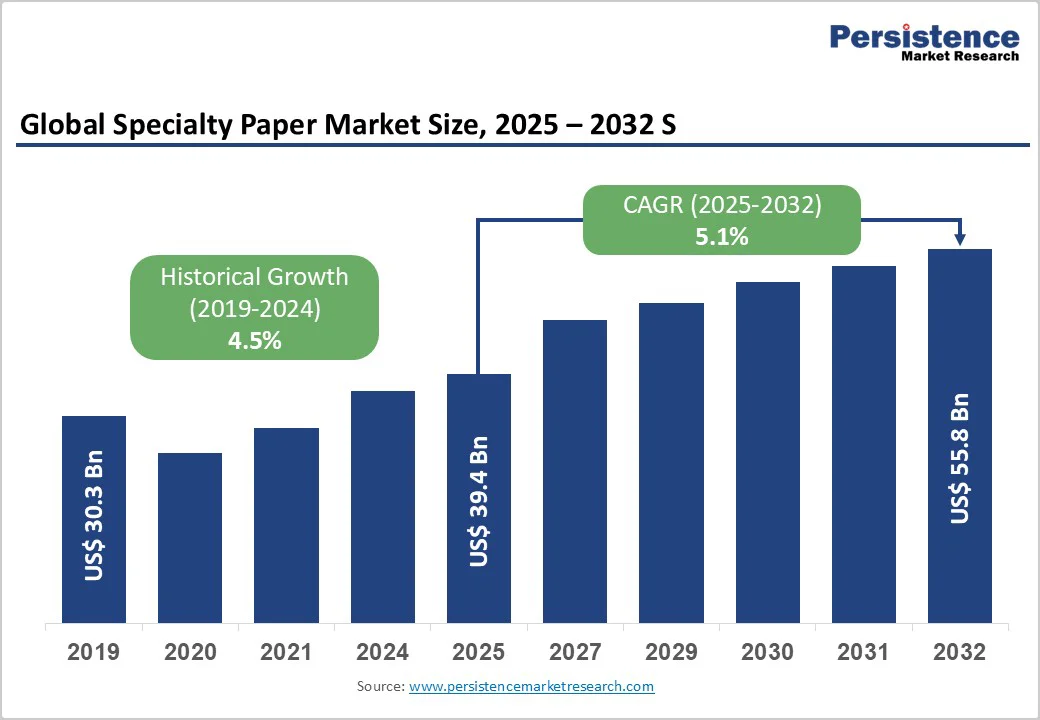

The global specialty paper market size is likely to be valued at US$39.4 Billion in 2025 and is expected to reach US$55.8 Billion by 2032, growing at a CAGR of 5.1% during the forecast period from 2025 to 2032, driven by growth in e-commerce packaging, fiber-based substitution for plastics, and technical paper applications such as filtration and electrical insulation underpins sustained demand.

Key Industry Highlights

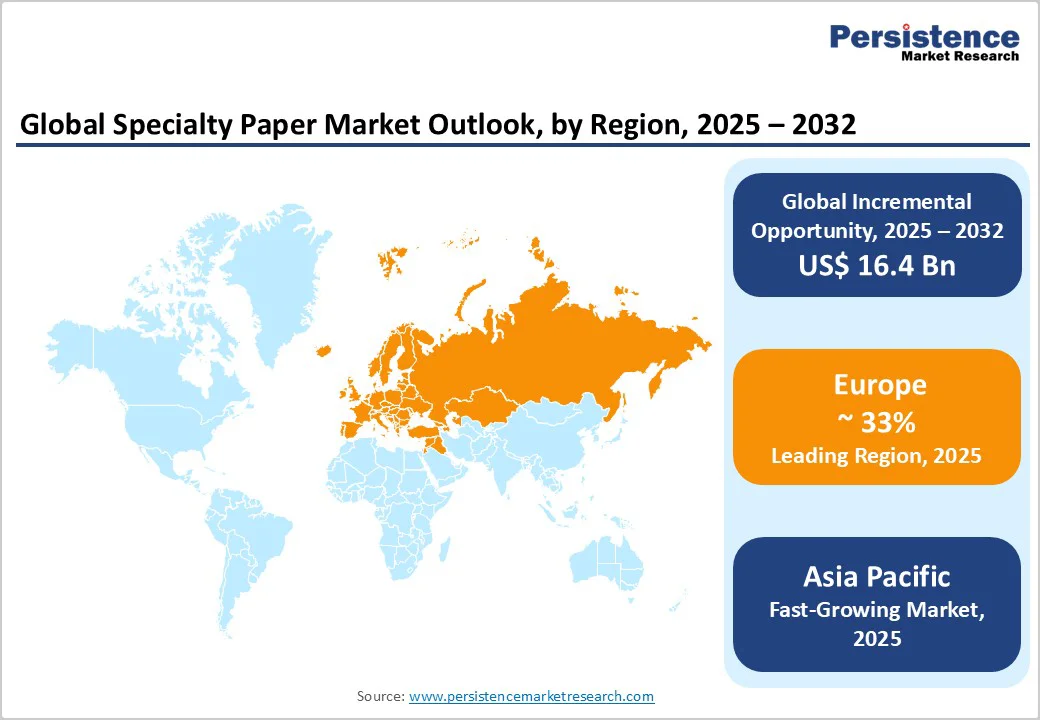

- Leading Region: Europe, accounting for 33% of global specialty paper market revenue in 2025, driven by advanced converting capacity, stringent sustainability mandates, and innovation in recyclable barrier and décor papers.

- Fastest-growing Region: Asia Pacific, supported by rising e-commerce packaging demand, plastic-substitution regulations, and local production of barrier and release-liner grades.

- Investment Plans: Major producers such as Mondi, Sappi, Stora Enso, and International Paper are investing in PFAS-free coatings, recyclable barrier papers, and digital-print substrates. Global investment in specialty paper capacity and coating modernization is estimated to exceed US$1 Billion through 2026.

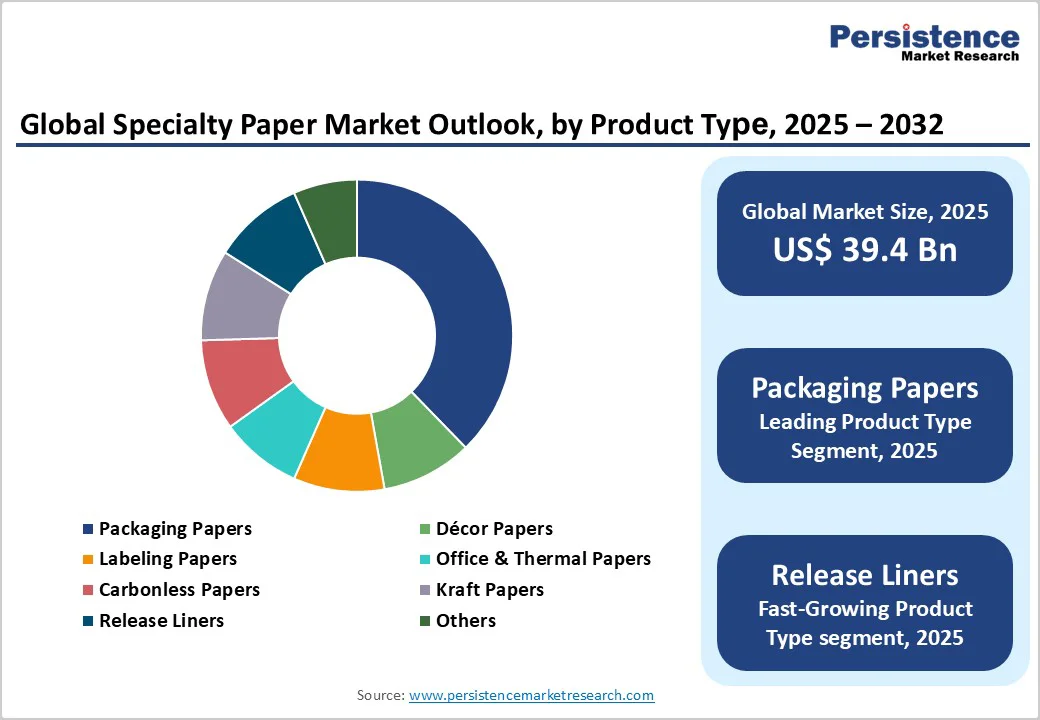

- Dominant Product Type: Packaging papers contribute around 39.7% of the total market value, fueled by sustainable brand initiatives, foodservice packaging, and e-commerce parcel growth.

- Leading Raw Material: Virgin fiber grades represent the majority share within raw materials, with over 58% of specialty paper production based on virgin wood pulp, due to superior strength, quality consistency, and food-contact compliance.

| Key Insights | Details |

|---|---|

| Specialty Paper Market Size (2025E) | US$39.4 Bn |

| Market Value Forecast (2032F) | US$55.8 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.1% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - E-Commerce and Fiber-Based Packaging Substitution

The global transition away from plastic packaging toward sustainable fiber-based solutions is a major value driver for specialty papers. Packaging and labeling applications now account for the largest demand share, bolstered by parcel shipping, protective wrapping, and foodservice requirements.

Government regulations restricting single-use plastics in the European Union, North America, and India accelerate this conversion. Analysts estimate that this substitution effect adds 0.7-1.0 percentage points to the overall industry CAGR. Higher-margin coated and functional barrier grades, grease-proof, water-resistant, and compostable, further enhance profitability and encourage mill modernization.

Technical and Functional Specialties

Industrial and healthcare applications, including filtration, electrical insulation, and release liners, are expanding rapidly. Technological advances in PFAS-free coatings, biodegradable barriers, and water-based formulations have enabled paper to replace complex multi-material laminates in critical uses.

These grades command premium pricing and often grow at 3-6% annually, outperforming commodity papers. Producers investing in new coating and converting technologies benefit from both environmental compliance and brand-owner procurement shifts favoring recyclable functional papers.

Barrier Analysis -Raw-Material and Energy Cost Volatility

Specialty paper producers are exposed to fluctuations in pulp, energy, and logistics costs, which compress margins and destabilize planning cycles. Spikes in fiber or chemical prices can erode earnings by several hundred basis points in low-margin mills. Regions dependent on imported pulp or fossil-fuel-based energy face heightened operational risk, especially smaller independent mills that lack integration. Persistent volatility limits near-term investment in high-value coating lines.

Regulatory and Technical Barriers for Coatings

Stringent regulation on PFAS and other legacy additives increases compliance costs and slow product rollout for certain barrier papers. Food-contact certification, recycled-content mandates, and safety testing extend time-to-market. Reformulation and conversion to compliant chemistries typically raise production costs per tonne by mid-single-digit percentages during transition years, challenging smaller manufacturers that lack R&D scale.

Opportunities - Recyclable High-Barrier Papers

The transition from plastic to recyclable paper laminates in flexible packaging offers a large incremental opportunity. Studies estimate that if 5-10% of plastic-based flexible packaging is substituted with paper-based barrier solutions by 2030, annual incremental specialty paper demand could exceed several hundred million U.S. dollars. Investment in coating innovation, compostable certifications, and brand-owner partnerships is critical for early movers to capture this growth with attractive capital returns.

Smart Labels and Functional Release Liners

Growth in RFID, smart packaging, and logistics tracking fuels demand for advanced label and release-liner substrates. Even modest share gains within the vast global labeling market translate into substantial absolute revenue due to higher price points of technical papers. Collaboration between paper mills, adhesive formulators, and sensor technology firms to co-develop stable, printable liners and smart substrates is an emerging high-margin frontier.

Category-wise Analysis

Product Type Insights

Packaging papers remain the largest segment of global specialty paper revenues, accounting for over 39.7% in 2025, according to CEPI and FAO. Growth is driven by sustainability trends and regulations phasing out single-use plastics. FMCG giants such as Nestlé, Unilever, and Coca-Cola are targeting recyclable or compostable paper packaging by 2030, fueling demand for coated kraft, sack kraft, and barrier-functional papers.

Producers such as Mondi, Stora Enso, and UPM-Kymmene are investing in advanced extrusion and dispersion coatings to deliver grease, moisture, and oxygen resistance without polyethylene, exemplified by Mondi’s FunctionalBarrier Paper Ultimate and Sappi’s Guard Pro OHS.

Release-liner papers, used in pressure-sensitive labels and adhesive tapes, are seeing strong growth as RFID and smart labeling drive demand for high-gloss silicone-coated base papers. Companies including Ahlstrom, Munksjö, and Fujifilm Specialty Papers are innovating with micro-coating and polymer-barrier technologies that enhance oil and vapor resistance while maintaining recyclability.

Ahlstrom’s 2025 acquisition of Pixelle’s Stevens Point mill expanded technical-grade capacity, while Sappi Europe’s mono-material barrier papers and Mitsubishi HiTec Paper’s Thermospan Next showcase fiber-based innovation compatible with digital printing.

Raw Material Insights

Virgin wood-pulp-based specialty papers represent over 58% of the global market, leading due to superior strength, brightness, and reliability in food-contact and medical uses. They are critical in applications such as medical sterilization wraps, flexible food packaging, and high-barrier papers, where fiber purity is essential.

Vertically integrated producers such as Stora Enso, UPM, and Domtar ensure traceability and FSC/PEFC-certified sourcing, delivering consistent quality and regulatory compliance. European and North American mills, supported by sustainable forestry and closed-loop water systems, are investing in higher-margin grades, exemplified by UPM’s Kaukas Mill and Stora Enso’s Oulu Mill.

Recycled fiber grades are the fastest-growing raw-material segment, fueled by circular-economy initiatives and emerging extended producer responsibility (EPR) regulations. Demand is rising in packaging, office papers, and decorative laminates.

Producers such as Mondi, Smurfit Kappa, and JK Paper are developing closed-loop recycling systems that convert post-consumer and post-industrial waste into premium specialty grades. Advances in bio-polymer coatings, nano-cellulose reinforcement, and enzymatic refining are mitigating fiber-shortening, impurity, and strength challenges.

Partnerships with chemical suppliers, including BASF and Kemira, enhance surface-treatment formulations, improving durability and performance and supporting the expansion of high-quality recycled specialty papers in sustainability-focused markets.

Regional Insights

Europe Specialty Paper Market Trends - Regulatory Innovation and Premium Packaging Leadership

Europe stands as the largest regional market by revenue for specialty paper, accounting for approximately 33% of the market. Principal markets include Germany, the U.K., France, and Spain. The region benefits from mature converting networks, stringent sustainability regulations, and strong demand for décor, labeling, and barrier papers.

Germany leads in production and exports, and the U.K. and France anchor label and packaging innovation. Growth drivers include the European Union’s packaging-waste legislation enforcing recyclability and recycled-content thresholds, and sophisticated brand-owner demand for premium tactile packaging.

Europe’s regulatory environment, including Extended Producer Responsibility (EPR) schemes and material restrictions, encourages innovation in recyclable paper products, while raising product-qualification costs and entry barriers for suppliers.

Investment activity concentrates on high-barrier coating lines, modernization of converting technology, and short-run décor printing capability. European firms have launched new functional grades targeting food packaging and e-commerce applications, sustaining the region’s leadership in specialty innovation.

Germany is the largest producer/exporter of specialty papers in Europe, with strong manufacturing infrastructure and converter networks servicing packaging, décor, and technical applications. In September 2025, Sappi Europe introduced two new recyclable mono-material high-barrier papers under the brands “Guard Pro OHS” and “Guard Pro OMH” designed for flow-wraps, sachets, and pouches, enhancing its recyclable-barrier offering.

North America Specialty Paper Market Trends-PFAS-Free Shift and Coated-Grade Consolidation

North America remains a key value contributor, with the U.S. dominating regional specialty paper demand. Capacity rationalization has shifted focus toward integrated producers, emphasizing coated and technical grades.

The U.S. leads demand for release-liners, filtration papers, and insulating substrates, supported by strong automotive, electronics, and healthcare industries. Canada contributes via pulp supply and smaller-scale converting operations. Growth drivers include booming e-commerce packaging, increased filtration needs in manufacturing, and rapid adoption of functional barrier coatings.

Regulatory influence is strong, especially state-level initiatives restricting PFAS and promoting sustainable packaging. Compliance requirements are accelerating the shift toward reformulated, PFAS-free coatings. Market differentiation rests on coating technology, supply security, and certification capabilities. Investment momentum favors food-contact-approved coating lines, digital-print substrates, and barrier-paper capacity expansions.

Private-equity investments in converting and label operations continue, reinforcing downstream integration trends. The U.S. accounts for the majority of North American specialty-paper value share. For example, a North America market report indicated the U.S. held around 65.6% share of the region in 2024.

In August 2025, International Paper announced the closure of two Georgia mills (in Savannah and Riceboro) and associated job cuts of approximately 1,100 employees, to streamline operations and focus on higher-value paper and packaging segments.

Asia Pacific Specialty Paper Market Trends - Fastest Growth and Sustainable Capacity Expansion

Asia Pacific is the fastest-growing region for specialty paper. The region’s expansion is anchored by China, Japan, India, and ASEAN economies. China exhibits the largest incremental volume growth, driven by massive packaging demand and new coating-line investments.

Japan remains a technology leader in high-performance technical papers and release liners. India and Southeast Asia (ASEAN) are emerging growth engines, propelled by urbanization, food-service expansion, and rising consumer incomes.

Key growth drivers include the e-commerce boom, manufacturing diversification, and sustainability regulations reducing plastic use. Regulatory adoption varies across the region, but voluntary corporate sustainability programs are stimulating demand for recyclable fiber-based solutions.

Cost advantages and access to raw materials position Asia Pacific as a production hub for global exports. Investments are focused on localizing premium barrier and release-liner production to substitute for imports.

Government initiatives promoting sustainable manufacturing further enhance the region’s opportunity for capacity growth and supply-chain localization. In August 2025, Mondi plc announced the ramp-up of its “FunctionalBarrier Paper Ultimate” line at its Solec (Poland) plant, which will service European and Asian markets, underlining the expansion of barrier-grade specialty paper supply into APAC and emphasizing global supply-chain localization.

Competitive Landscape

The global specialty paper industry is moderately consolidated. Major integrated producers, Mondi, Stora Enso, International Paper, UPM-Kymmene, Nippon Paper, and Ahlstrom-Munksjö, control significant market shares, while numerous regional specialists serve décor and technical niches.

Concentration varies by sub-segment: décor and printing are fragmented, whereas release-liner and barrier papers are more consolidated. Integrated firms with pulp and coating assets maintain stronger pricing power and supply security.

Leading players emphasize product differentiation through functional coatings, vertical integration to secure pulp and conversion assets, and sustainability certification for recycled content and chemical compliance. Expansion into Asia Pacific manufacturing and R&D collaboration with brand owners strengthens long-term competitive advantage.

Key Industry Developments

- In August 2025, Mondi launched its new “FunctionalBarrier Paper Ultimate”, a high-performance barrier paper with oxygen transmission rate (OTR) and water vapor transmission rate (WVTR) both below 0.5 units, designed to replace multi-material packaging and comply with circular-economy standards.

- In September 2025, Sappi Europe introduced two new recyclable mono-material high-barrier papers, “Guard Pro OHS” and “Guard Pro OMH”, engineered for flow-wraps, sachets, and pouches in food packaging that adhere to stricter EU regulations.

Companies Covered in Specialty Paper Market

- Mondi Group

- Stora Enso Oyj

- Sappi Ltd

- UPM-Kymmene Corporation

- Domtar Corporation

- International Paper Company

- Ahlstrom-Munksjö Oyj

- Nippon Paper Industries Co., Ltd.

- Pixelle Specialty Solutions

- Glatfelter Corporation

- Twin Rivers Paper Company

- Burgo Group S.p.A.

- ITC Limited

- Daio Paper Corporation

- Oji Holdings Corporation

- Pudumjee Paper Products Ltd

- Fedrigoni S.p.A.

- Schweitzer-Mauduit International, Inc. (SWM)

- Kruger Inc.

- Verso Corporation

Frequently Asked Questions

The specialty paper market size is valued at US$39.4 Billion in 2025.

By 2032, the specialty paper market is projected to reach US$55.8 Billion.

Key trends include the substitution of plastics with recyclable paper solutions, growth in barrier-coated and release-liner grades, and expanding use of recycled fibers aligned with global circular economy goals.

The packaging segment dominates the market, contributing nearly 39.7% of total revenue, driven by surging e-commerce activity, foodservice disposables, and sustainability mandates across developed economies.

The specialty paper market is expected to expand at a CAGR of 5.1% from 2025 to 2032.

Major companies include Mondi Group, Stora Enso Oyj, Sappi Ltd, UPM-Kymmene Corp., and Domtar Corporation.