- Food Ingredients & Additives

- Plant Protein Ingredients Market

Plant Protein Ingredients Market Size, Share, and Growth Forecast, 2026 - 2033

Plant Protein Ingredients Market by Product Type (Pea, Soybean, Wheat, Bean, Peanut, Legume, Others), Functionality (Emulsification and Stabilizing, Foaming, Nutrition, Adhesion, Others), Application, End-user, and Regional Analysis for 2026 - 2033

Plant Protein Ingredients Market Size and Trends Analysis

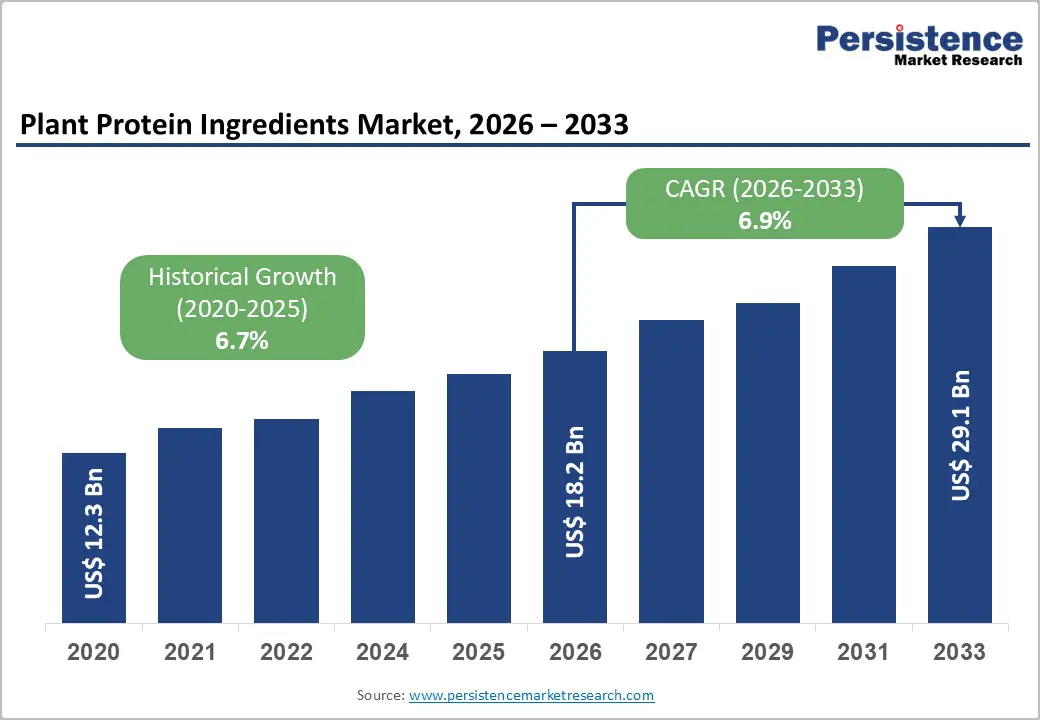

The global plant protein ingredients market size is likely to be valued at US$18.2 billion in 2026, and is expected to reach US$29.1 billion by 2033, growing at a CAGR of 6.9% during the forecast period from 2026 to 2033, driven by the increasing adoption of plant-based diets, rising demand for sustainable protein sources in food and beverages, and advancements in extraction and texturization technologies.

Growing demand for high-quality, clean-label plant protein ingredients, especially pea and soybean, is accelerating adoption across applications. Advances in emulsification and nutritional functionality are further boosting uptake by offering more versatile, allergen-friendly options. Growing awareness of plant-based protein ingredients as essential for health, sustainability, and affordable nutrition in emerging markets remains a key driver of the plant protein ingredients market's expansion.

Key Industry Highlights:

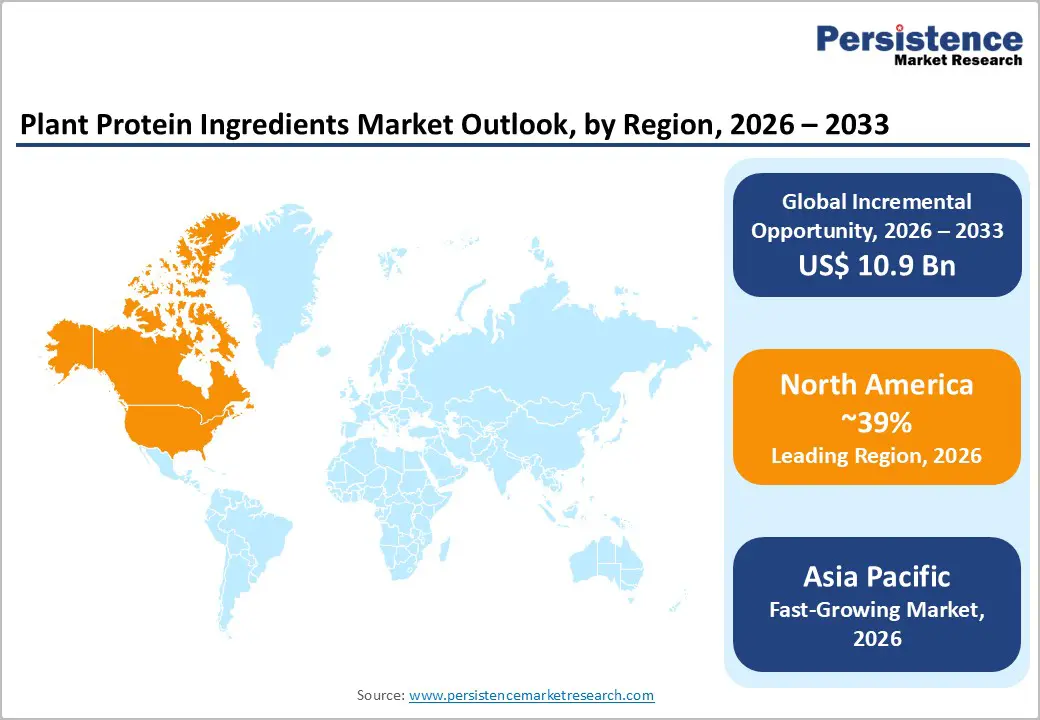

- Leading Region: North America, anticipated to account for a 39% market share in 2026, driven by strong vegan trends, high consumer spending on plant-based products, and robust innovation in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by rising middle-class demand, urbanization, and growing investments in pea and soy processing in China and India.

- Dominant Product Type: Pea, to hold approximately 30% of the market share, as it offers neutral taste, high digestibility, and non-GMO appeal.

- Leading Functionality: Nutrition, to account for over 40% of the market revenue in 2026, due to its role in protein fortification across food and supplements.

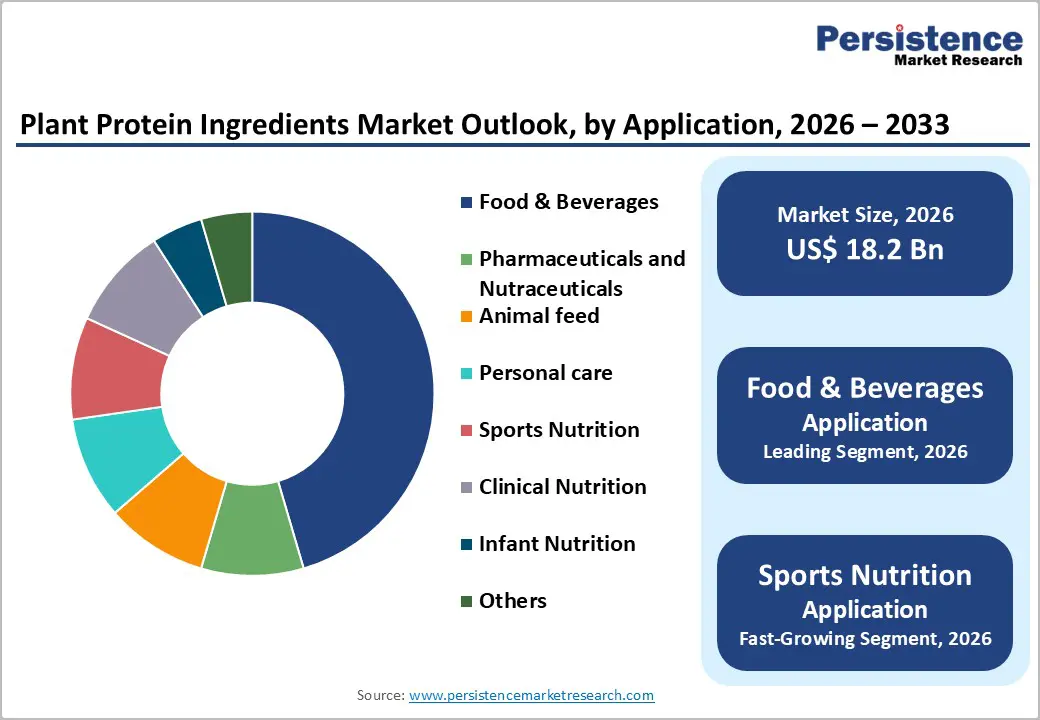

- Leading Application: Food and beverages, to contribute nearly 50% of the market revenue in 2026, due to extensive use in meat alternatives, dairy substitutes, and snacks.

- Leading End-user: Retail consumers will lead, with approximately 40% revenue share in 2026, driven by direct demand for plant-based packaged foods and supplements.

| Key Insights | Details |

|---|---|

|

Plant Protein Ingredients Market Size (2026E) |

US$18.2 Bn |

|

Market Value Forecast (2033F) |

US$29.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Advancements in Protein Extraction and Processing Technologies

Advancements in protein extraction and processing technologies have significantly enhanced the quality, functionality, and applicability of plant protein ingredients. Traditional methods such as wet extraction have evolved with refined controls over pH, temperature, and solvent use, resulting in higher protein yields with improved purity and reduced off-flavors. Emerging techniques such as dry fractionation separate protein from plant sources without water or chemicals, preserving native protein structures and enhancing nutritional value while lowering energy and water use.

Innovations in membrane filtration and enzymatic processing allow for the selective removal of non-protein components, producing concentrates and isolates with tailored solubility, emulsification, and gelation properties. These processing approaches also help retain essential amino acids and reduce naturally occurring anti-nutritional factors in many plant matrices. Advances in high-moisture extrusion create texturized proteins that mimic the fibrous texture of meat, enabling better performance in analog products. Controlled heat–moisture treatment and shear cell technology improve texture and mouthfeel without relying on additives. The integration of fermentation-assisted processing improves flavor profiles and enhances digestibility by modifying protein structures through microbial action.

High Development and Processing Costs

High development and processing costs present a significant barrier for companies advancing next-generation plant protein ingredients and novel extraction systems. Developing innovative grades, such as high-purity pea isolates, non-GMO soy concentrates, or hypoallergenic rice proteins, requires extensive research, specialized fractionation, and advanced drying technologies that are far more expensive than those for animal proteins. Functionality is an even greater challenge: many premium variants, emulsification-enhanced lots, and low-anti-nutrient products are sensitive to pH, heat, and solubility, requiring rigorous optimization to ensure they remain effective throughout formulation and storage. Achieving long-term performance often requires costly sensory trials, sophisticated functional testing, and high-grade raw materials, significantly increasing R&D expenditures.

Meeting stringent regulatory expectations for allergen labeling, GMO status, and batch consistency requires multiple validation studies under various conditions and across several production batches. This adds both time and financial burden to development timelines. Scaling up manufacturing requires controlled extruders, specialized dryers, and quality-assurance systems, further driving up overall costs. For smaller processors, these challenges can limit premium diversification or delay commercialization.

Expansion in Texturization and Clean-Label Delivery Platforms

Expansion in texturization and clean-label plant protein delivery platforms is transforming the global nutrition landscape by addressing two major challenges, texture limitations and consumer trust barriers. Texturization platforms are engineered to achieve meat-like fibers, reducing reliance on binders and enabling realistic meat analogs in granules and isolates. Innovations, such as high-moisture extrusion, shear-cell technology, fiber alignment, and hybrid blending, significantly improve mouthfeel and reduce crumbliness, lowering formulation costs for brands and consumer campaigns.

Progress in clean-label platforms, including organic pea proteins, non-GMO soy, fermented rice, and legume concentrates, supports more transparent nutrition by minimizing additives, the industry’s first line of defense against clean-label scrutiny. These formats eliminate synthetic stabilizers, enhance functionality, and allow versatile use without masking agents, making them highly suitable for mass food programs. New technologies such as enzymatic modification, bio-fortification, and VLP-based encapsulation further enhance flavor and nutrient response.

Category-wise Analysis

Product Type Insights

The pea segment is anticipated to dominate the market, accounting for approximately 30% of the market share in 2026. Its dominance is driven by neutral taste, high protein content, and non-GMO status, making it preferred for meat alternatives. Pea provides excellent emulsification, ensures nutrition, and contributes to sustainability, making it suitable for large-scale food campaigns. Beyond Meat, a leading plant-based meat company, uses pea protein isolate as a primary protein source in its core product lines, including Beyond Burger and Beyond Beef. Pea protein delivers high protein content (~20 g per serving), contributes desirable texture and emulsification that mimic meat, and supports a neutral flavor base that can be seasoned to appeal to mainstream consumers. As the pea protein used is non-GMO and derived from peas rather than soy or animal sources, it aligns with clean-label and sustainability expectations.

Soybeans are likely to be the fastest-growing segment, due to their cost-effectiveness and expanding use in traditional and emerging markets. Its high-yield profile makes it ideal for targeted affordability, reducing overall costs. Continuous innovations in non-GMO soy are further strengthening its acceptance, as demand for proven, versatile proteins accelerates. Cargill, Inc., a major global agribusiness and food ingredients supplier, offers Prosante® Textured Soy Protein, a cost-effective soy protein ingredient widely used in food formulations across North America and Europe. Cargill highlights that its textured soy flour provides an economical, complete plant protein solution that can be incorporated into a variety of food products, including beef patties, meatballs, snacks, cereals, and vegetarian nuggets.

Functionality Insights

Nutrition is expected to lead the plant protein ingredients market, holding approximately 40% of the share in 2026, driven by protein fortification needs, large supplement programs, and strong global demand for high amino acid profiles. Their dominance continues as brands expand functional foods. Rising adoption of emulsification and expanded foaming campaigns highlight the growing focus on multi-functional benefits. Laird Superfood, a brand known for plant-based wellness products, expanded its portfolio with a Protein Instant Latte formulated with a proprietary blend of plant proteins, including pumpkin seed protein, as well as pea and hemp proteins. This product is targeted at nutritional fortification and functional food positioning by providing elevated protein content in a convenient beverage format, responding to strong global demand for nutrient-dense, high-amino-acid products.

The emulsification and stabilizing segment is likely to be the fastest-growing, due to strong momentum in dairy alternatives and expanding inclusion of plant proteins in emulsions. The growing shift toward creamy, stable platforms, along with improved texture, is accelerating adoption. Advancements in pea and soy emulsifiers and the continued progress of hybrid stabilizers entering food trials drive market growth. Ripple Foods (U.S.–based plant-based food company) makes pea-protein–based dairy alternatives such as pea milk and Greek-style yogurt that leverage the emulsification and stabilizing functionality of plant proteins to create creamy, smooth products. Ripple’s beverages and yogurts use pea protein as a core structural and stabilizing ingredient, enabling oil-in-water emulsions that mimic the mouthfeel and texture of dairy milk and yogurt without animal proteins.

Application Insights

The food and beverages segment is expected to dominate, contributing nearly 50% of the revenue share in 2026, as it remains the primary hub for meat analogs, large-scale formulation programs, and the management of diverse products requiring protein fortification. Their strong integration, trained formulators, and ability to handle high-volume or clean-label blends drive higher consumption. The food & beverages sectors are leading pea rollouts and administering emerging soy trials. Nestlé S.A. has significantly expanded its plant-based beverage portfolio using plant proteins, particularly pea and oat proteins, to drive growth in the food and beverage sector. Products such as the oat- and pea-based Nesfit beverage in Brazil and Nesquik GoodNes in the U.S. combine plant proteins with fortified nutrients (e.g., vitamins and minerals) to create protein-rich, consumer-friendly drinks that appeal to health- and sustainability-oriented consumers.

Sports nutrition is likely to be the fastest-growing segment, driven by its strong fitness presence and expanding role in protein powders. They offer convenient, quick, and accessible dosing, attracting athletes who prefer plant-based, high-performance settings. Increased outreach programs, recovery focus, and wider availability of routine and premium proteins further accelerate uptake, boosting rapid adoption across both urban and semi-urban areas. Optimum Nutrition, a major global sports nutrition brand under Glanbia plc, launched Gold Standard 100% Plant Protein, a plant-based protein powder formulated with organic pea, brown rice, and sacha inchi proteins to support muscle recovery and performance in fitness settings. This product targets athletes and fitness enthusiasts looking for plant-based alternatives to traditional whey/sports supplements, offering convenient, high-protein dosing that fits into training and recovery routines.

End-user Insights

Industrial food manufacturers are expected to lead the market, accounting for approximately 45% of revenue in 2026, due to their large-scale operations and consistent demand for high-volume protein inputs across varied product lines. These manufacturers incorporate plant proteins into meat alternatives, dairy substitutes, bakery items, ready-to-eat meals, and fortified foods, fueling steady market growth. Their in-house formulation capabilities enable efficient use of plant proteins to optimize nutrition, texture, and product stability, while centralized sourcing helps reduce costs. For instance, Nestlé S.A., the world’s largest food and beverage company, has significantly expanded its plant-based portfolio by integrating proteins such as pea, soy, and oat across multiple mainstream food categories. Nestlé’s offerings, including the Garden Gourmet Sensational Burger, Carnation Vegan products, and Coffee-Mate Natural Bliss oat creamer, replace animal-derived proteins with plant-based alternatives to meet consumer demands for nutrition, sustainability, and familiar taste profiles.

Retail consumers are likely to be the fastest-growing end-user segment, driven by shifting dietary preferences and rising household-level health awareness. Consumers are increasingly purchasing plant-protein-fortified foods, beverages, and supplements through supermarkets and online platforms for everyday nutrition. The availability of convenient formats such as ready-to-drink shakes, protein bars, and home-use protein powders supports regular consumption. The Kroger Co., one of the largest supermarket chains in the U.S., significantly expanded its Simple Truth Plant-Based product line, a private-label range of plant protein foods sold directly to retail consumers. This range includes plant-based burgers, vegan ground “meat,” plant-based sausages, and other meat alternatives, which are prominently merchandised in Kroger’s supermarket aisles. Retail strategies such as dedicated plant-based sections and convenient shelf placement alongside conventional products have helped attract mainstream shoppers and flexitarians, increasing everyday consumption of plant-protein foods.

Regional Insights

North America Plant Protein Ingredients Market Trends

North America is projected to lead, accounting for nearly 39% of the market share in 2026, driven by the region’s advanced food innovation infrastructure, strong research and development capabilities, and high public awareness of plant-based benefits. Processing systems in the U.S. and Canada provide extensive support for formulation programs, ensuring broad access to plant protein ingredients across food, supplement, and animal feed markets. Increasing demand for pea, convenient, and easy-to-incorporate forms is further accelerating adoption, as these formats improve functionality and reduce barriers associated with animal proteins.

Optimum Nutrition, one of the most recognized sports nutrition brands in North America, offers Gold Standard 100% Plant Protein, a plant-based protein powder formulated for athletes and fitness enthusiasts looking for high-quality protein to support muscle strength, recovery, and performance. This product combines pea, rice, and fava bean proteins to deliver 24 g of plant protein per serving, including all nine essential amino acids, making it suitable for post-workout dosing and daily athletic nutrition routines. The formulation is designed for ease of mixing, digestibility, and performance support, which aligns with the sports nutrition segment’s role in driving high-volume adoption of plant protein in the U.S. and Canada.

Innovation in plant protein technology, including stable texturization, improved extraction delivery, and targeted nutritional enhancement, is attracting significant investment from both public and private sectors. Government initiatives and vegan campaigns continue to promote meat reduction, environmental concerns, and emerging flexitarian threats, thereby sustaining market demand. The growing focus on soy blends and specialty uses, particularly for nutraceuticals and others, is expanding the target applications for plant protein ingredients.

Europe Plant Protein Ingredients Market Trends

Europe is being driven by growing awareness of sustainability benefits, robust processing infrastructure, and government-backed green initiatives. Countries, including Germany, France, and the U.K., have well-established food systems that facilitate the regular integration of plant proteins and promote the adoption of innovative protein delivery methods. These sustainable formulations are especially attractive to general consumers, environmentally conscious buyers, and supplement users, enhancing both compliance and reach.

Technological advancements in plant protein development, such as enhanced functionality, application-targeted delivery, and improved organic grades, are further boosting market potential. European authorities are increasingly supporting research and trials for proteins against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, clean-label options is aligned with the region’s focus on preventive nutrition and reducing animal intake. Public awareness campaigns and transition drives are expanding reach in both urban and rural areas, while suppliers are investing in fractionation and novel variants to increase efficacy.

Asia Pacific Plant Protein Ingredients Market Trends

Asia Pacific is likely to be the fastest-growing market for plant protein ingredients in 2026, driven by rising protein awareness, increasing government initiatives, and expanding application programs across the region. Countries such as India, China, Japan, and Southeast Asian nations are actively promoting protein campaigns to address nutritional growth and emerging vegan needs. Plant protein ingredients are particularly attractive in these regions due to their local sourcing, ease of processing, and suitability for large-scale food drives in both urban and rural populations.

Technological advancements are enabling the development of stable, effective, and easy-to-formulate plant protein ingredients that can withstand challenging climatic conditions and minimize dependence on waste. These innovations are critical for reaching remote facilities and improving overall nutritional coverage. Growing demand for food & beverages, nutraceuticals, and animal feed applications is contributing to market expansion. Public-private partnerships, increased agro expenditure, and rising investment in extraction research and manufacturing capacity are further accelerating growth. The convenience of protein delivery, combined with improved functionality and reduced risk of deficiency, positions plant protein ingredients as a preferred choice.

Competitive Landscape

The global plant protein ingredients market features competition between established agri-processors and emerging clean-label brands. In North America and Europe, Cargill and ADM lead through strong R&D, distribution networks, and food ties, bolstered by innovative isolates and functional programs. In Asia Pacific, Ingredion advances with localized solutions, enhancing accessibility. Functional delivery boosts versatility, cuts animal risks, and enables mass formulations across regions.

Strategic partnerships, collaborations, and acquisitions merge expertise, expand sourcing, and speed commercialization. Organic formulations solve purity issues, aiding penetration in health-focused areas.

Key Industry Developments

- In November 2025, Tetra Pak launched sunflower protein, a plant-based ingredient with up to 50% protein, fiber, vitamins, and antioxidants, featuring a neutral, slightly nutty flavor and off-white color for versatile food and beverage applications.

- In February 2024, Roquette developed and launched NUTRALYS® Pea F853M, NUTRALYS® H85, NUTRALYS® T Pea 700FL, and NUTRALYS® T Pea 700M to expand its pea protein portfolio and help food manufacturers overcome formulation challenges in plant-protein foods and beverages.

Companies Covered in Plant Protein Ingredients Market

- Cargill Incorporated

- ADM

- Kerry Group plc.

- Ingredion

- dsm-firmenich

- Roquette Frères

- Wilmar International Ltd

- Glanbia PLC

- Prinova Group LLC

- Axiom Foods, Inc.

Frequently Asked Questions

The global plant protein ingredients market is projected to reach US$18.2 billion in 2026.

The rising prevalence of plant-based diets and demand for sustainable protein sources are the key drivers.

The plant protein ingredients market is poised to witness a CAGR of 6.9% from 2026 to 2033.

Advancements in texturization and clean-label delivery platforms are the key opportunities.

Cargill, Incorporated, ADM, Kerry Group plc, Ingredion, and DSM-Firmenich are the key players.