- Packaging

- Nanographic Printing Market

Nanographic Printing Market Size, Share, and Growth Forecast, 2026 - 2033

Nanographic Printing Market by Printing Type (Sheet-Fed, Web-Fed, Others), Application (Packaging, Commercial Printing, Others), End-user, and Regional Analysis for 2026 - 2033

Nanographic Printing Market Size and Trends Analysis

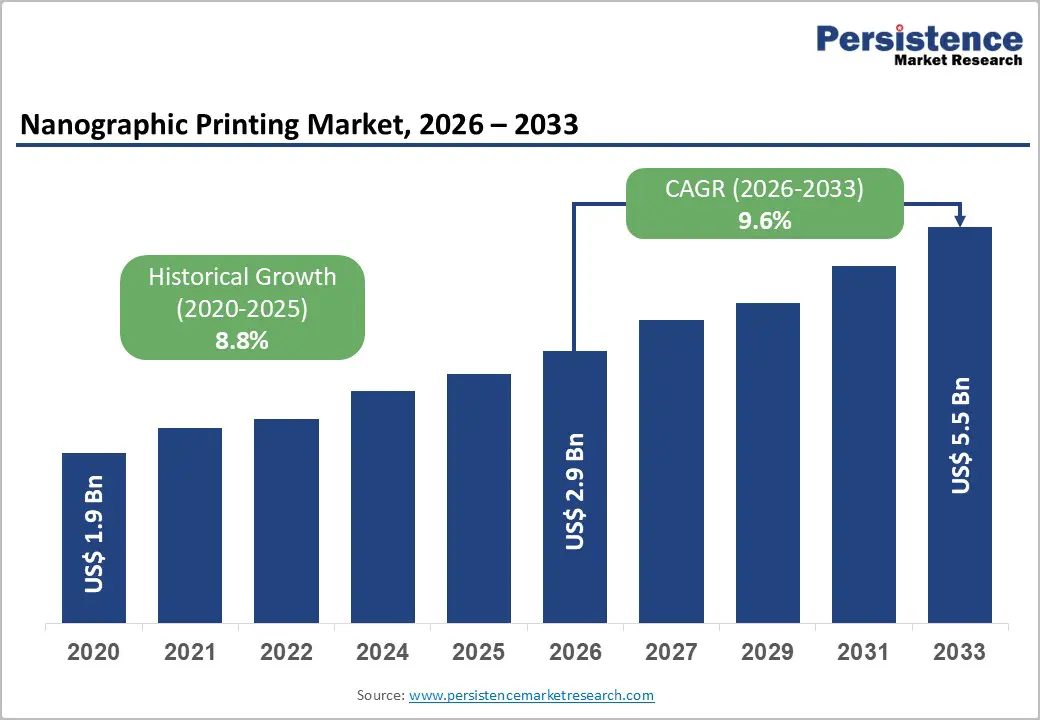

The global nanographic printing market size is likely to be valued at US$2.9 billion in 2026 and is expected to reach US$5.5 billion by 2033, growing at a CAGR of 9.6% between 2026 and 2033, driven by the convergence of offset-quality output with digital production flexibility, accelerating adoption in short-to-medium run packaging, and rising demand for sustainable, customizable print solutions.

Sheet-fed platforms and packaging applications dominate current deployments, while the Asia Pacific is emerging as the fastest-growing region. North America maintains market leadership due to early technology adoption and a mature print ecosystem.

Key Industry Highlights

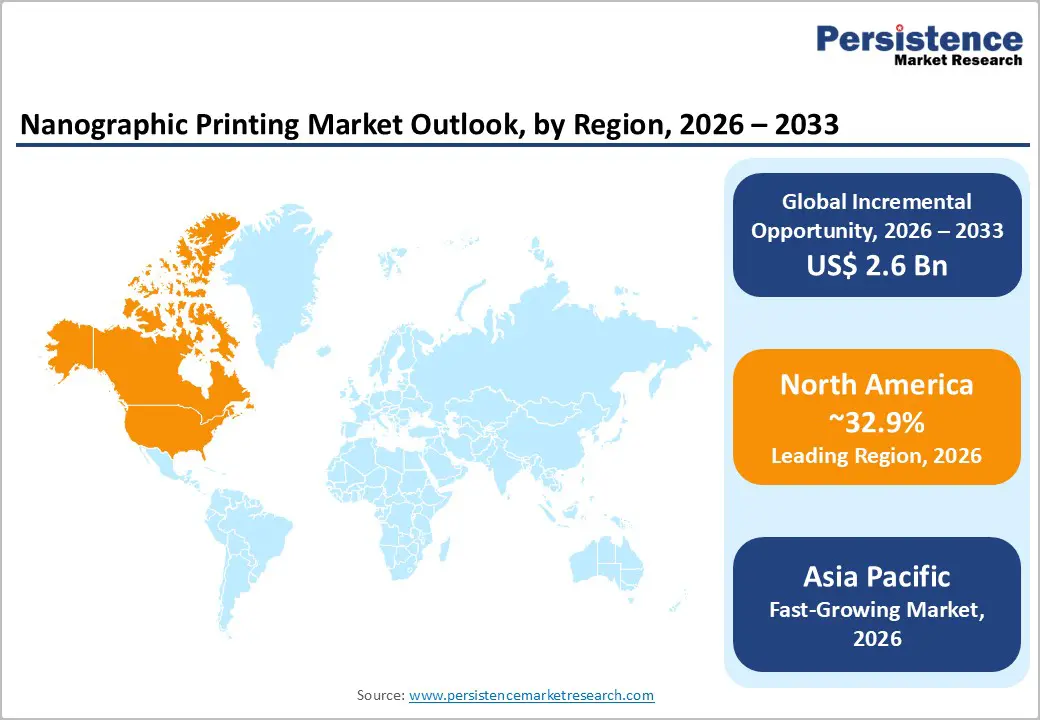

- Leading Region: North America is projected to account for 32.9% of market share, driven by early adoption among U.S.-based packaging converters and commercial printers, strong e-commerce demand, advanced finishing infrastructure, and favorable access to capital and service ecosystems.

- Fastest-Growing Region: Asia Pacific, projected to record the highest regional CAGR, supported by the rapid expansion of organized retail and e-commerce in China and India, export-oriented packaging investments across ASEAN, and the growing adoption of digital print technologies by large regional converter groups.

- Investment Plans: Capital investment remains focused on B1 sheet-fed nanographic presses and selective web-fed/hybrid platforms, with converters prioritizing short-run packaging, SKU rationalization, and offset substitution. Investments are increasingly structured through phased rollouts, leasing models, and vendor-backed financing, particularly in North America and the Asia Pacific.

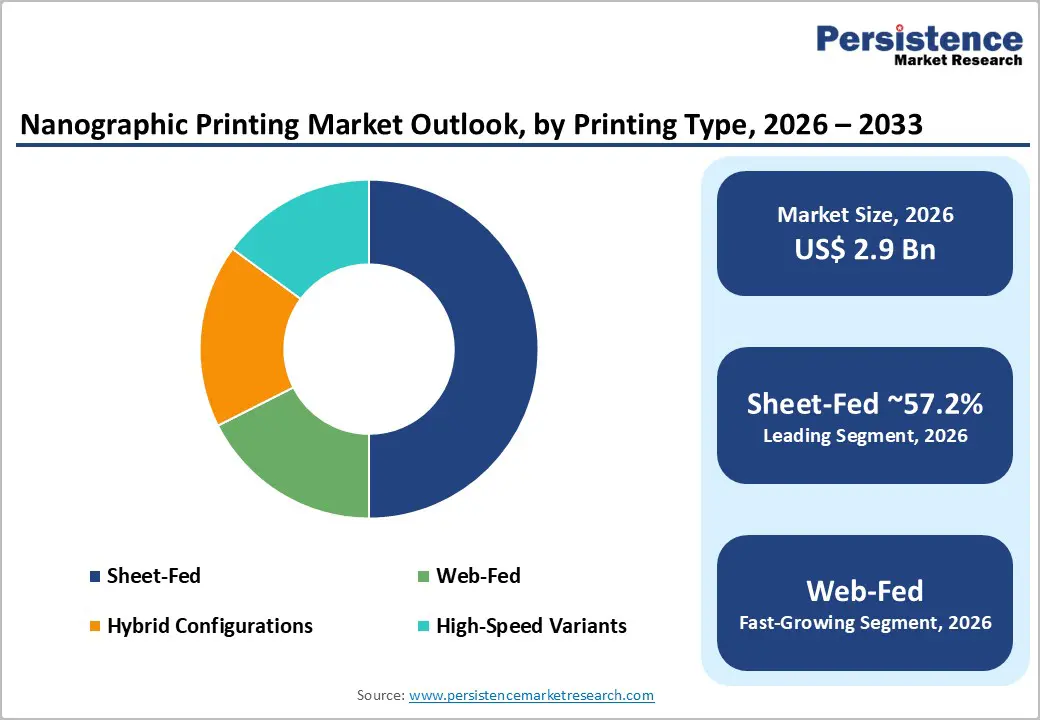

- Dominant Printing Type: Sheet-fed nanographic printing is anticipated to hold a 57.2% market share, favored for its compatibility with existing folding carton infrastructure, consistent image quality, and strong economics for short- to medium-sized production runs.

- Leading Application: Packaging is estimated to represent approximately 44.1% of market share, led by folding cartons and premium paperboard applications, where frequent artwork changes, regulatory updates, and localized branding support sustained demand for nanographic printing solutions.

| Key Insights | Details |

|---|---|

| Nanographic Printing Market Size (2026E) | US$2.9 Bn |

| Market Value Forecast (2033F) | US$5.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Offset Economics Combined with Digital Flexibility

Nanographic printing bridges the structural gap between conventional offset and digital printing by delivering offset-grade print quality with digital production efficiency. The process forms a dry polymer film on a heated blanket, allowing precise ink transfer with minimal substrate interaction. This architecture significantly reduces make-ready time, plate costs, and waste associated with offset printing. Packaging converters benefit from the ability to profitably produce short-to-medium runs while supporting SKU proliferation and frequent design changes. As brand portfolios expand and seasonal campaigns accelerate, this economic flexibility improves asset utilization and lowers per-unit production costs for jobs that fall below offset break-even volumes.

Packaging Demand and Sustainability Alignment

Packaging represents a major revenue contributor, accounting for approximately 44.1% of total market revenue. Brand owners increasingly require on-demand packaging, regional customization, and rapid design iterations, all of which favor the adoption of digital printing. Nanographic printing supports a broad range of paperboard and coated substrates, enabling converters to reduce overproduction and inventory obsolescence. Lower waste generation and efficient material usage align with corporate sustainability targets and regulatory pressure favoring recyclable and lower-impact packaging. The growth of e-commerce and private-label brands further expands demand for flexible, short-run packaging formats.

Throughput Improvements and Next-Generation Press Platforms

Recent advances in press engineering have significantly improved nanographic printing productivity. New-generation B1 sheet-fed presses offer substantially higher sheets-per-hour capability, narrowing the historical throughput gap between digital and high-speed offset printing. Higher production speeds reduce cost per impression, increase uptime efficiency, and allow digital presses to handle longer short-run and mid-volume jobs. These performance gains are influencing replacement and augmentation decisions among large commercial printers and packaging converters, enabling a broader mix of offset jobs to migrate to nanographic platforms that meet substrate compatibility and finishing requirements.

Barrier Analysis - High Capital Requirements and Investment Risk

Nanographic presses, particularly B1-format systems, require substantial upfront capital investment and facility readiness, including power capacity, material handling, and finishing integration. These requirements present a barrier for mid-sized converters and commercial printers with constrained capital budgets. Investment decisions are further influenced by concerns around vendor stability, long-term service support, and technology ramp-up timelines. From a financial perspective, extended payback periods and sensitivity to uptime performance increase perceived risk, leading some potential adopters to delay or phase investments rather than commit to full-scale deployment.

Substrate Qualification and Finishing Compatibility

Despite broad substrate support, certain coated, metallized, or specialty materials require additional validation in nanographic printing workflows. Finishing processes such as lamination, varnishing, and die-cutting may behave differently compared to offset-printed outputs, particularly in packaging applications. These technical variables can increase pre-press testing, qualification time, and setup costs for early jobs. For low-margin or high-volume products, the additional effort required during initial SKU conversion may slow adoption, especially when offset processes remain well-optimized for those formats.

Opportunity Analysis - Emerging Markets and Converter Modernization

Asia Pacific and selected European markets present significant growth opportunities as packaging converters modernize production infrastructure. Asia Pacific is the fastest-growing region, driven by expanding consumer markets, e-commerce penetration, and export-oriented packaging demand. If the region increases its share of global nanographic installations by 5-8 percentage points over the forecast period, incremental market value could reach several hundred million dollars. Local financing models, service hubs, and joint venture deployments can accelerate adoption in markets where offset capacity is extensive but increasingly misaligned with evolving brand requirements.

Premium Short-Run Packaging and Personalization

Brands are allocating higher budgets to limited-edition, personalized, and campaign-driven packaging that delivers faster market impact. Nanographic printing enables premium pricing for short-run, high-quality packaging where speed, customization, and visual differentiation are critical. Converters that integrate design, data management, and rapid production workflows are positioned to capture this value through differentiated service offerings.

Category-wise Analysis

Printing Type Insights

Sheet-fed nanographic printing is anticipated to remain the dominant printing type, retaining approximately 57.2% of market share through the end of the decade, supported by its strong alignment with established folding carton and commercial print workflows. B1-format sheet-fed presses integrate seamlessly with existing die-cutting, folding, and finishing infrastructure, significantly lowering adoption friction for converters transitioning from offset lithography. These systems deliver consistent registration accuracy, high color stability, and offset-comparable image quality across coated and uncoated paperboard substrates.

Adoption has been strongest in North America and Western Europe, where mid-to-large converters deploy sheet-fed nanography for short-to-medium production runs, typically below 10,000 sheets, that are increasingly uneconomical on conventional offset presses. For example, folding carton converters supplying pharmaceutical secondary packaging and premium food cartons use sheet-fed nanography to accommodate frequent SKU changes and regulatory-driven artwork revisions. Key operational benefits include faster turnaround times, reduced makeready waste, and enhanced responsiveness to brand-driven design updates, reinforcing the segment’s leadership position.

Web-fed nanographic configurations are the fastest-growing segment of the printing type. These systems are optimized for continuous-feed applications, including labels, flexible packaging, corrugated pre-print liners, and selected paper-based e-commerce packaging formats. Growth is driven by rising demand for higher throughput, roll-to-roll workflows, and inline finishing capabilities that improve operational efficiency in high-volume environments.

Web-fed nanographic solutions enable converters to address high-SKU, short-repeat production models, particularly for omnichannel retail and subscription-based packaging. While adoption remains concentrated among technologically mature converters with validated substrate compatibility and automated finishing lines, vendor roadmaps, beta installations, and pilot commercial deployments indicate expanding readiness and broader market penetration over the forecast period.

Application Insights

Packaging is anticipated to maintain a leading revenue share of approximately 44.1%, making it the most influential application segment within the nanographic printing market. Demand is concentrated in folding cartons, litho-laminated packaging, premium paperboard boxes, and select corrugated display applications. Growth is primarily driven by brand owner requirements for frequent artwork refreshes, regulatory labeling updates, SKU proliferation, and localized or regionalized packaging content.

Converters are increasingly reallocating select SKUs from offset to nanographic platforms to reduce inventory obsolescence, compress lead times, and improve speed-to-market. For example, food, cosmetics, and nutraceutical brands leverage nanography for limited-edition packaging and seasonal campaigns without incurring high plate and setup costs. Packaging applications also benefit from higher per-unit print values and value-added finishing, which support stronger ROI profiles and accelerate press utilization rates among early adopters.

Commercial printing is likely to be the fastest-growing application segment, driven by the structural shift toward short-run, high-quality, and on-demand print requirements. Nanographic printing increasingly replaces offset in applications such as point-of-sale materials, marketing collateral, catalogs, brochures, and event-specific promotional print, where run lengths fall below traditional offset break-even thresholds.

Personalization, versioning, and rapid campaign turnaround are central growth drivers. Retail chains, FMCG marketers, and event-driven advertisers are fueling demand for fast-turn promotional print with consistent color reproduction across distributed locations. Large commercial printers are also expanding into packaging prototypes, retail displays, and short-run cartons, using nanography to diversify revenue streams and stabilize press utilization. This convergence between commercial and packaging print applications is reinforcing sustained growth momentum and reshaping traditional segment boundaries.

Regional Insights

North America Nanographic Printing Market Trends - Short-Run CPG Packaging and E-Commerce-Driven Digital Migration

North America is projected to lead the market with a 32.9% share, underpinned by the dominant position of the U.S. in both high-value packaging conversion and commercial print services. The U.S. market benefits from a dense concentration of large-scale packaging converters, national commercial printers, and multinational brand owners that actively pursue short-run optimization and SKU rationalization. Strong e-commerce penetration, particularly across food, personal care, and health categories, has accelerated demand for on-demand folding cartons, promotional packaging, and rapid-turn POS materials, favoring B1-format sheet-fed nanographic presses.

Several early commercial installations of nanographic platforms across the U.S. have reinforced market confidence, particularly among converters serving consumer packaged goods (CPG) and pharmaceutical secondary packaging. Large North American print groups have publicly emphasized digital migration strategies centered on reducing makeready waste and improving responsiveness to brand artwork changes. In parallel, the region’s well-developed finishing and converting ecosystem, including die-cutting, gluing, and embellishment, lowers integration risk for nanographic presses compared to less mature markets. Access to capital through equipment leasing, vendor-backed financing, and private equity support further reduces adoption barriers.

Regulatory and sustainability pressures also shape regional demand. Extended producer responsibility (EPR) frameworks emerging at the state level, along with corporate sustainability commitments from major retailers and brand owners, encourage shorter production cycles and lower inventory obsolescence, strengthening the business case for nanography. While vendor concentration and platform maturity remain monitored risks, North America continues to be a priority market for high-margin, short-run packaging and premium commercial print, particularly where speed-to-market and design agility translate directly into brand value.

Europe Nanographic Printing Market Trends - Regulation-Led Digital Transformation in Premium and Multilingual Packaging

Europe represents a mature yet steadily expanding market for nanographic printing, led by Germany, the U.K., France, and Spain, where structural shifts toward flexible, regulation-compliant print production are well underway. Germany anchors regional demand through its strong industrial printing base and advanced manufacturing capabilities, with converters integrating nanographic presses to complement offset capacity in folding carton and specialty packaging workflows. The U.K. and France exhibit particularly strong uptake in short-run branded packaging and commercial print, driven by retail marketing intensity and high design turnover.

A defining regional catalyst is regulatory harmonization around packaging waste, recyclability, and traceability, driven by EU-level directives and national enforcement mechanisms. These frameworks are accelerating digital press adoption as converters seek to minimize overruns, comply with labeling updates, and support multilingual packaging across cross-border supply chains. As a result, European converters are modernizing press fleets with B1 digital platforms and narrow-web solutions, prioritizing flexibility over pure volume efficiency.

Notably, premium retail packaging demand, especially in cosmetics, luxury food, and specialty beverages, supports nanographic adoption by justifying higher per-unit print costs through enhanced visual quality and reduced lead times. Southern European markets, including Spain, are leveraging digital print to optimize export-oriented packaging runs, while Northern Europe emphasizes sustainability-driven production models. Growth is expected to remain stable rather than explosive, but Europe continues to serve as a reference market for regulatory-driven digital transformation and quality-led nanographic deployment.

Asia Pacific Nanographic Printing Market Trends - High-Growth Adoption Fueled by Export Manufacturing and Retail Modernization

Asia Pacific is the fastest-growing regional market for nanographic printing, driven by expanding domestic consumption, export-oriented packaging demand, and the accelerating modernization of print infrastructure. China, Japan, India, and ASEAN markets represent distinct growth profiles but share a common shift toward digital technologies that enable shorter runs, faster turnaround, and SKU proliferation. China leads regional adoption by volume, supported by large converter groups investing in advanced digital platforms to serve multinational brand owners and cross-border e-commerce packaging requirements.

Japan’s market development is more selective, with nanographic printing deployed primarily for high-value packaging applications where color precision, consistency, and substrate performance are critical. Japanese converters emphasize quality assurance and process control, aligning well with nanographic capabilities. In India, rapid growth in organized retail, food delivery, and e-commerce logistics is creating demand for on-demand folding cartons, corrugated pre-print, and promotional materials, particularly among regional brand owners seeking flexibility without large inventory exposure.

ASEAN markets, including Vietnam, Thailand, and Indonesia, are emerging as secondary growth hubs, supported by competitive manufacturing costs and increasing foreign investment in packaging capacity. Flexible financing structures, phased equipment rollouts, and improving local service support are enabling the gradual adoption of nanographic platforms. As regional vendor service networks mature and substrate compatibility broadens, the Asia Pacific is positioned to capture the largest share of incremental market growth, especially in packaging-driven applications tied to consumer goods and export manufacturing.

Competitive Landscape

The global nanographic printing market is moderately concentrated around technology innovators and established press manufacturers. Competition centers on press productivity, total cost of ownership, substrate compatibility, and service reliability. While nanography remains a distinct technology category, adjacent high-speed digital and inkjet platforms influence purchasing decisions. Market share is distributed between equipment suppliers and large print service providers operating mixed-technology fleets.

Developments include the launch of next-generation B1 nanographic presses with higher throughput, commercial installations by large packaging groups to expand short-run capacity, and industry restructuring events that may lead to consolidation and renewed investment focus. These developments underscore both the maturation of the technology and the importance of financial and operational stability in vendor selection.

Leading players emphasize continuous innovation, regional expansion through service and financing, and value-added offerings such as design integration and variable data printing. Competitive differentiation increasingly depends on reliability, workflow integration, and the ability to support scalable production economics.

Key Industry Developments

- In January 2025, Marketing Alliance Group installed a second Landa S11 nanographic printing press with the PrintAI module at its Paramount Printing facility to support expanding production for health, beauty, and retail display applications, reflecting rising demand for high-quality, short-run printing services.

Companies Covered in Nanographic Printing Market

- Landa Digital Printing

- HP (Hewlett-Packard)

- Komori Corporation

- Koenig & Bauer

- Durst Group

- Fujifilm

- Xerox

- Canon

- Konica Minolta

- Ricoh

- Epson

- Heidelberg

- Manroland Goss

- Screen Holdings

- KBA-MHI (joint venture)

- EFI (Electronics For Imaging)

- Kodak

- Agfa Graphics

Frequently Asked Questions

The global nanographic printing market is likely to be valued at US$2.9 billion in 2026.

By 2033, the nanographic printing market is expected to reach US$5.5 billion.

Key trends include the shift from offset to digital printing for short-to-medium runs, rising demand for customized and localized packaging, improvements in press throughput and economics, and increasing adoption of on-demand, low-waste production models aligned with sustainability goals.

Sheet-fed nanographic printing is the leading segment, holding 57.2% market share, supported by strong compatibility with folding carton applications and existing finishing infrastructure.

The nanographic printing market is projected to grow at a CAGR of 9.6% between 2026 and 2033.

Major players include Landa Digital Printing, HP (Indigo and PageWide divisions), Komori Corporation, Koenig & Bauer/Durst, and Fujifilm.