- Non-food Packaging

- Minimalist Packaging Market

Minimalist Packaging Market Size, Share, and Growth Forecast 2026 - 2033

Minimalist Packaging Market by Material (Paper & Paperboard, Plastics, Glass, Metals, Others), by Packaging Type (Boxes & Cartons, Bags & Pouches, Bottles & Jars, Trays & Clamshells, Others), by End-use (Food & Beverages, Personal Care & Cosmetics, Fashion & Apparel, Household, Healthcare, Others), by Regional Analysis, 2026 - 2033

Minimalist Packaging Market Size and Trend Analysis

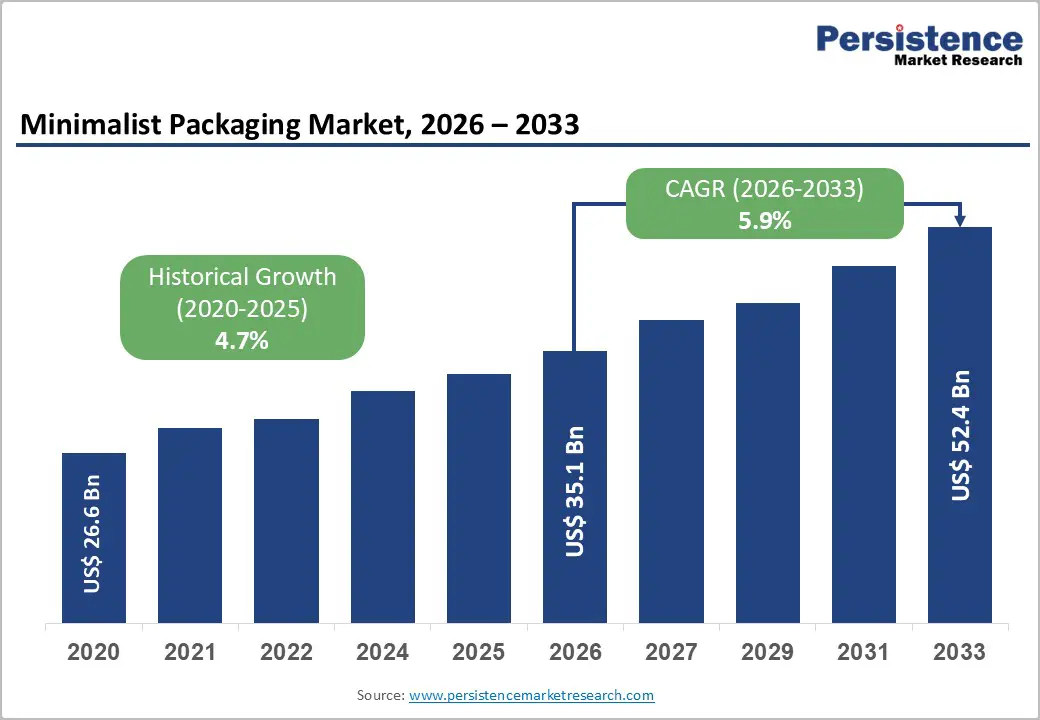

The global Minimalist Packaging Market size is likely to be valued at US$ 35.1 Billion in 2026 and is expected to reach US$ 52.4 Billion by 2033, growing at a CAGR of 5.9% during the forecast period from 2026 to 2033. The market is expanding steadily because brand owners across consumer goods, beauty, food, and e-commerce are redesigning packs to reduce material use, improve shelf appeal, and align with sustainability expectations.

Key Market Highlights

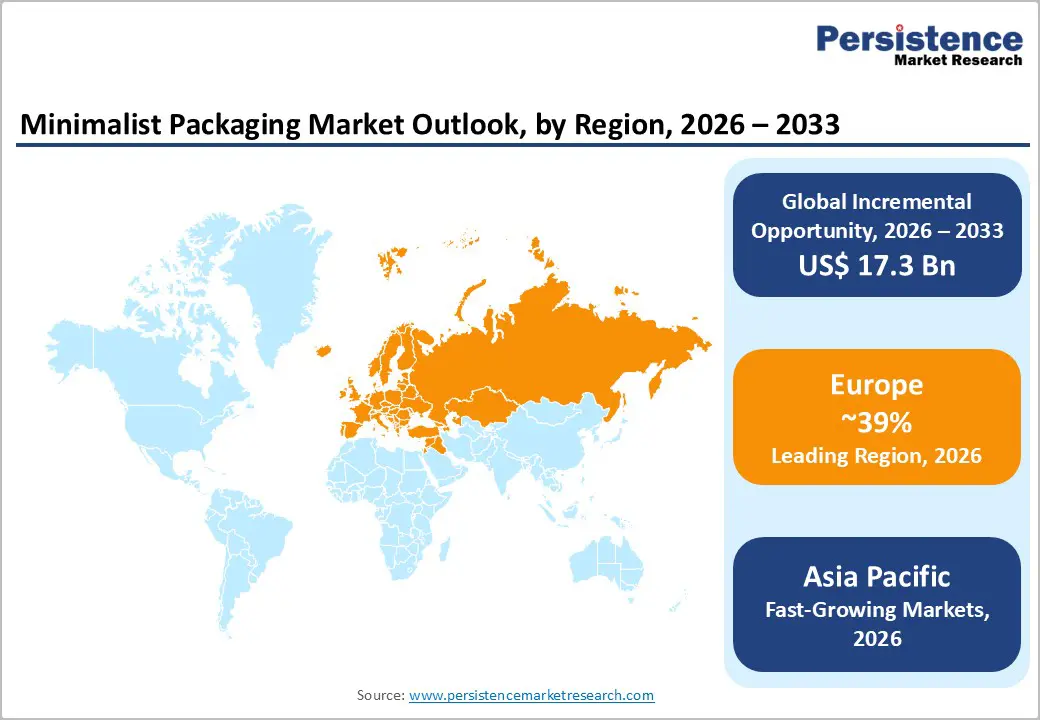

- Leading Region: Europe remains the leading regional market for minimalist packaging holding 39% share, supported by sustainability regulation, strong consumer preference for low-waste formats, and broad brand adoption across Food & Beverages, Personal Care & Cosmetics, and premium retail packaging applications.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region with rising CAGR of 7.1%, driven by expanding e-commerce, rising organized retail, growing domestic consumer brands, and scalable packaging conversion capacity across China, Japan, India, and major ASEAN manufacturing and consumption markets.

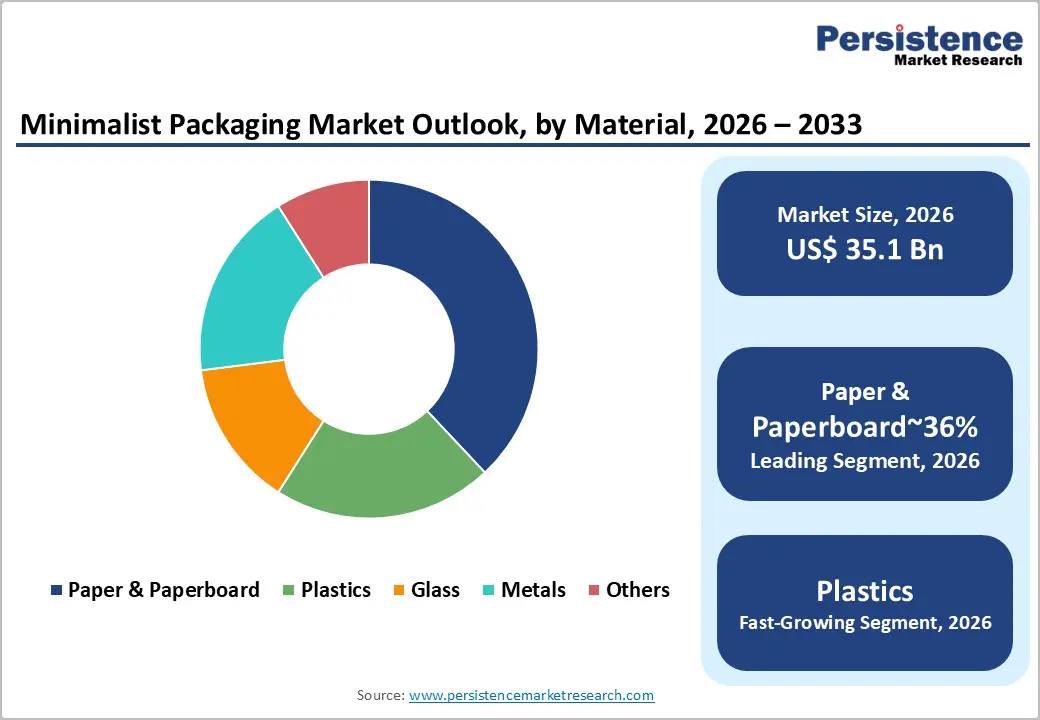

- Leading Segment: Paper & Paperboard is the dominant material segment, accounting for about 36% of market share, because it aligns strongly with minimalist design, recyclability goals, lightweight construction, and consumer preference for simple and visibly sustainable packaging formats.

- Fastest-Growing Segment: Personal Care & Cosmetics is one of the fastest-growing end-use segments, as minimalist aesthetics, refillable formats, clean branding, and premium dispensing solutions increasingly shape packaging decisions in skincare, haircare, fragrance, and wellness categories.

- Key Opportunity: The strongest market opportunity lies in paper-based substitution and mono-material innovation, where packaging suppliers can help brands reduce component count, improve recyclability, simplify shelf presentation, and lower logistics intensity without sacrificing functional performance.

| Key Insights | Details |

|---|---|

|

Minimalist Packaging Market Size (2026E) |

US$ 35.1 Billion |

|

Market Value Forecast (2033F) |

US$ 52.4 Billion |

|

Projected Growth CAGR (2026–2033) |

5.9% |

|

Historical Market Growth (2020–2025) |

4.7% |

DRO Analysis

Drivers - Sustainability-Led Packaging Redesign Across Consumer Industries

Minimalist packaging is gaining strong momentum as it directly supports waste reduction, lighter packaging formats, and easier recyclability without compromising product protection. Companies across Food & Beverages, Personal Care & Cosmetics, and Household sectors are actively removing unnecessary decorative layers, secondary wraps, excess inserts, and complex multi-material structures. This shift helps improve both environmental positioning and cost efficiency.

In real-world applications, minimalist packaging uses fewer inks, reduced laminates, and simplified structural designs, enabling better production efficiency and lower material consumption. The trend is particularly strong in premium personal care, clean-label food products, and direct-to-consumer brands, where packaging aesthetics remain important but over-packaging is increasingly discouraged. As consumer awareness rises, minimalist packaging is no longer just a design choice but is evolving into a strategic standard for modern, sustainable packaging development across industries globally.

E-commerce Expansion and Demand for Right-Sized Functional Packaging

The rapid growth of e-commerce is significantly driving demand for minimalist packaging, as online brands require packaging that is protective, lightweight, visually clean, and easy to standardize. Minimalist designs help reduce empty space, simplify packaging structure, and improve cube efficiency during transportation, which directly lowers logistics and fulfillment costs.

Packaging formats such as boxes, cartons, bags, and pouches are increasingly being redesigned with clean graphics, fewer components, and optimized dimensions to meet both operational and branding needs. This trend is especially relevant in industries like fashion, beauty, health, and specialty foods, where packaging often serves as the first physical interaction between the brand and the customer. As online retail continues to expand globally, minimalist packaging is becoming more attractive because it combines cost efficiency with improved customer experience and strong brand presentation.

Restraints - Performance Limits in Some High-Barrier and Premium Applications

Despite its advantages, minimalist packaging faces challenges in product categories that require high barrier protection, luxury differentiation, or extended shelf life. Certain food, pharmaceutical, and cosmetic products still depend on complex multi-layer materials, coated surfaces, and rigid premium packaging formats that do not easily align with minimalist principles. While reducing layers and decorative elements improves sustainability perception, it may raise concerns about durability, leakage resistance, tamper evidence, and protection against moisture or oxygen.

These functional requirements are critical in sensitive applications, making companies cautious about adopting minimalist solutions. As a result, adoption remains slower in segments where regulatory compliance, product safety, and premium branding are more important than material reduction. Businesses must carefully balance sustainability goals with performance needs to ensure product integrity is not compromised while transitioning to simpler packaging formats.

Higher Redesign and Conversion Costs for Brand Owners

Although minimalist packaging offers long-term cost benefits, the initial transition can be expensive for many companies. Businesses often need to invest in structural redesign, simplified artwork, new material testing, tooling upgrades, and adjustments to existing packaging lines. These changes can create short-term financial pressure, particularly for small and mid-sized companies with limited production volumes or multiple product variations.

The minimalist packaging often requires more precise material engineering to maintain strength and functionality while using less material. This can increase development complexity and upfront costs. While savings from reduced material usage are achievable over time, the initial investment phase can slow adoption. Companies must carefully plan the transition to ensure cost efficiency without disrupting production processes or compromising packaging quality during the redesign and implementation stages.

Opportunities - Premium Beauty and Personal Care Brands Adopting Refillable and Clean Aesthetic Formats

A major opportunity in the minimalist packaging market lies within the personal care and cosmetics industry, where simplicity is strongly linked with premium branding and sustainability. Many beauty brands are adopting clean, minimal designs that feature subtle graphics, mono-material components, standardized closures, and refillable packaging systems. These designs reduce visual clutter while enhancing perceived product quality and environmental value.

This shift is increasing demand for minimalist bottles, jars, airless packaging systems, paper-based cartons, and low-decoration secondary packaging. Companies that successfully combine elegant design with refill functionality, accurate dispensing, and recyclable or reusable materials are well-positioned to gain competitive advantage. This trend is particularly strong in skincare, haircare, fragrance, and wellness segments, where packaging plays a key role in both product differentiation and brand storytelling, making minimalist packaging a valuable strategic tool.

Paper-Based Substitution and Mono-Material Innovation Across Food and Retail Packaging

Another key opportunity is the growing shift from difficult-to-recycle multi-material packaging to paper-based and mono-material solutions that align with minimalist design principles. Companies are increasingly exploring paperboard structures, simplified flexible packaging, and retail-ready formats that reduce unnecessary components and improve recyclability. This trend is especially visible in foodservice, bakery, dry foods, apparel, and household goods, where brands aim to achieve practical sustainability improvements.

Minimalist packaging that reduces coatings, plastic elements, inserts, and decorative features is gaining strong attention. Suppliers that can provide lightweight paper-based packaging with high print quality, strong shelf appeal, and adequate barrier protection are likely to benefit the most. The opportunity becomes even stronger when minimalist design is combined with easy recycling, as brands increasingly prefer packaging that is both visually simple and environmentally responsible for consumers.

Category-wise Analysis

Material Insights

Paper and paperboard dominate the minimalist packaging market, accounting for approximately 36% of total market share. Their leadership is driven by strong alignment with minimalist principles such as lightweight construction, simple print designs, reduced material complexity, and high consumer acceptance as a sustainable option. Paper-based packaging is widely used in boxes, cartons, sleeves, folding cartons, rigid packaging, and certain pouch replacement applications where brands prefer a clean and simple look.

It is especially popular among food, apparel, personal care, and e-commerce brands due to its ability to support branding with minimal ink usage and subtle design elements. Although plastic materials continue to play an important role in flexible and protective packaging, paper and paperboard remain dominant because they better support sustainability messaging and minimalist visual appeal. This makes them the preferred choice for companies focusing on eco-friendly packaging strategies.

Packaging Type Insights

Boxes and cartons lead the packaging type segment, holding around 34% of the global minimalist packaging market. Their strong position comes from their versatility across industries such as retail, e-commerce, food, personal care, healthcare, and apparel. Brands increasingly prefer these formats because they allow simple structural designs with minimal decoration, fewer inserts, and reduced secondary packaging layers. Minimalist boxes and cartons provide an ideal balance between product protection, visual presentation, stackability, and recyclability.

They also support efficient shipping through right-sized packaging, simplified printing processes, and compatibility with automated production lines. While bags and pouches are growing rapidly due to their lightweight nature and material efficiency, boxes and cartons remain dominant as they are widely accepted across both premium and mass-market segments without requiring major changes in consumer handling or usage behavior.

End-user Insights

Food and beverages represent the largest end-use segment in the minimalist packaging market, accounting for approximately 31% of total market share. This leadership is mainly due to the high volume of packaging required in the sector and continuous pressure to reduce waste and improve efficiency. Minimalist packaging is increasingly used for products such as dry foods, bakery items, beverages, snacks, meal kits, and specialty foods.

Simple graphics, fewer packaging layers, and lightweight designs help enhance both functionality and premium appeal. Additionally, the growth of private-label brands and clean-label products has increased the demand for simple and transparent packaging designs. While personal care and cosmetics are emerging as the fastest-growing segment due to premiumization and refill trends, food and beverages remain the largest contributor because of their scale, wide retail presence, and consistent demand for cost-effective and sustainable packaging solutions.

Regional Insights

North America Minimalist Packaging Market Trends

North America represents a mature yet highly innovative market for minimalist packaging, led by the United States. Companies across packaged food, beauty, household, and e-commerce sectors are actively redesigning packaging to reduce material usage and improve recyclability. The region benefits from a strong ecosystem of brand owners, packaging converters, and design specialists who are driving the adoption of simple, functional packaging solutions.

Minimalist packaging aligns well with direct-to-consumer trends, where clean design often reflects premium quality, transparency, and environmental responsibility. Additionally, increasing regulatory focus on packaging waste reduction and recycled content is supporting this shift. Although regulations differ across states and regions, the overall direction encourages simpler and more recyclable packaging formats. As a result, paper-based packaging, mono-material solutions, and minimalist secondary packaging are gaining strong traction, with the United States continuing to lead due to its scale and innovation capacity.

Europe Minimalist Packaging Market Trends

Europe is one of the most advanced markets for minimalist packaging, driven by strong sustainability regulations, high consumer awareness, and a well-established premium design culture. Countries such as Germany, the United Kingdom, France, and Spain are actively adopting packaging solutions that reduce unnecessary components and improve recyclability. European brands are leading the shift toward paper-based materials, refillable packaging systems, mono-material designs, and premium minimalist formats, especially in cosmetics and specialty retail sectors.

Regulatory frameworks across the region are also encouraging packaging reduction and circular economy practices, making minimalist design a practical solution for compliance. Germany stands out due to its strong packaging industry and large consumer market, while the UK and France play key roles in driving innovation in beauty and wellness packaging. Overall, Europe continues to influence global packaging standards with its strong focus on sustainability and design excellence.

Asia Pacific Minimalist Packaging Market Trends

Asia Pacific is the fastest-growing region in the minimalist packaging market, supported by rapid urbanization, rising consumer demand, and expanding e-commerce activities. Countries such as China, Japan, India, and those in Southeast Asia are witnessing increasing adoption of minimalist packaging as brands aim to reduce costs and improve efficiency. The trend is particularly strong among online-first brands in beauty, fashion, electronics, and packaged foods, where simple packaging enhances both logistics and brand perception.

China plays a key role due to its large-scale manufacturing and packaging production capabilities, while Japan contributes with its advanced design aesthetics and premium packaging standards. India is emerging as a major growth market with expanding retail and e-commerce sectors. Across ASEAN countries, minimalist packaging is gaining popularity as businesses seek scalable, affordable, and sustainable packaging solutions for both domestic and export markets.

Competitive Landscape

The global minimalist packaging market is moderately fragmented, with competition spread across large packaging companies, specialty manufacturers, and regional converters. Leading players focus on innovation in lightweight design, high-quality materials, mono-material packaging, refillable solutions, and simplified yet premium aesthetics. Companies such as Smurfit Kappa, Mondi, DS Smith, Graphic Packaging International, AptarGroup, Huhtamaki, and Quadpack are actively investing in packaging simplification and sustainability.

Key trends include the development of refill systems, minimalist luxury packaging, e-commerce-friendly paper formats, and design services that help brands reduce packaging weight and complexity. These companies aim to deliver packaging solutions that maintain product protection and visual appeal while minimizing material usage. As demand for sustainable packaging continues to grow, competition is expected to focus more on innovation, scalability, and the ability to meet evolving environmental and consumer expectations.

Key Developments:

- In July, 2024: Smurfit Kappa completed its combination with WestRock, significantly expanding its global paper-based packaging operations. The merger enhances scale, innovation, and supply capabilities, enabling better delivery of lightweight, recyclable, and minimalist corrugated and carton packaging solutions.

- In April, 2024: DS Smith agreed to be acquired by International Paper, strengthening combined expertise in paper production and packaging design. This move is expected to enhance circular packaging innovation and support growing demand for sustainable, fiber-based minimalist packaging solutions.

- In December 2024: AptarGroup expanded its focus on recyclable, refillable, and mono-material dispensing technologies. The company is actively supporting beauty and personal care brands with simplified, premium packaging designs that reduce component complexity while improving sustainability and enhancing overall user experience.

Companies Covered in Minimalist Packaging Market

- Smurfit Kappa

- Mondi

- DS Smith

- Graphic Packaging International

- Virospack

- Quadpack

- APackaging Group

- AptarGroup

- Huhtamaki Oyj

- EPL Limited

- Refine Packaging

- Golden Arrow, Inc.

- Oliver Inc.

- Lipack Packaging

- Richpack

- WestRock

Frequently Asked Questions

The global Minimalist Packaging Market is estimated at US$ 35.1 Billion in 2026 and is projected to reach US$ 52.4 Billion by 2033, expanding at a CAGR of 5.9% during the forecast period.

The primary growth driver is the rising preference for packaging that uses fewer materials, improves recyclability, lowers logistics costs, and supports clean, premium, sustainability-led brand positioning across consumer goods categories.

Paper & Paperboard leads the market with an estimated 36% share because it fits minimalist design goals, supports lightweight and recyclable formats, and works well across cartons, sleeves, secondary packs, and e-commerce packaging.

Europe is the leading regional market due to strong regulatory pressure on packaging waste, high consumer sustainability awareness, and widespread adoption of simplified, recyclable, and premium minimalist packaging across major end-use industries.

A major opportunity lies in paper-based substitution, mono-material innovation, and refill-ready premium packaging, especially for Personal Care & Cosmetics, food brands, and online retail categories seeking lower-waste packaging solutions.

Key market participants include Smurfit Kappa, Mondi, DS Smith, Graphic Packaging International, Virospack, Quadpack, APackaging Group, AptarGroup, Huhtamaki Oyj, EPL Limited, Oliver Inc., Lipack Packaging, and Richpack.