- Smart Packaging

- Cushioned Mailer Market

Cushioned Mailer Market Size, Share, and Growth Forecast, 2026 - 2033

Cushioned Mailer Market by Material (Recycled Kraft Paper, Honeycomb-Lined Paper, Others), Cushioning Type (Macerated Paper Padding, Honeycomb Paper Core, Others), Application, and Regional Analysis for 2026 - 2033

Cushioned Mailer Market Size and Trends Analysis

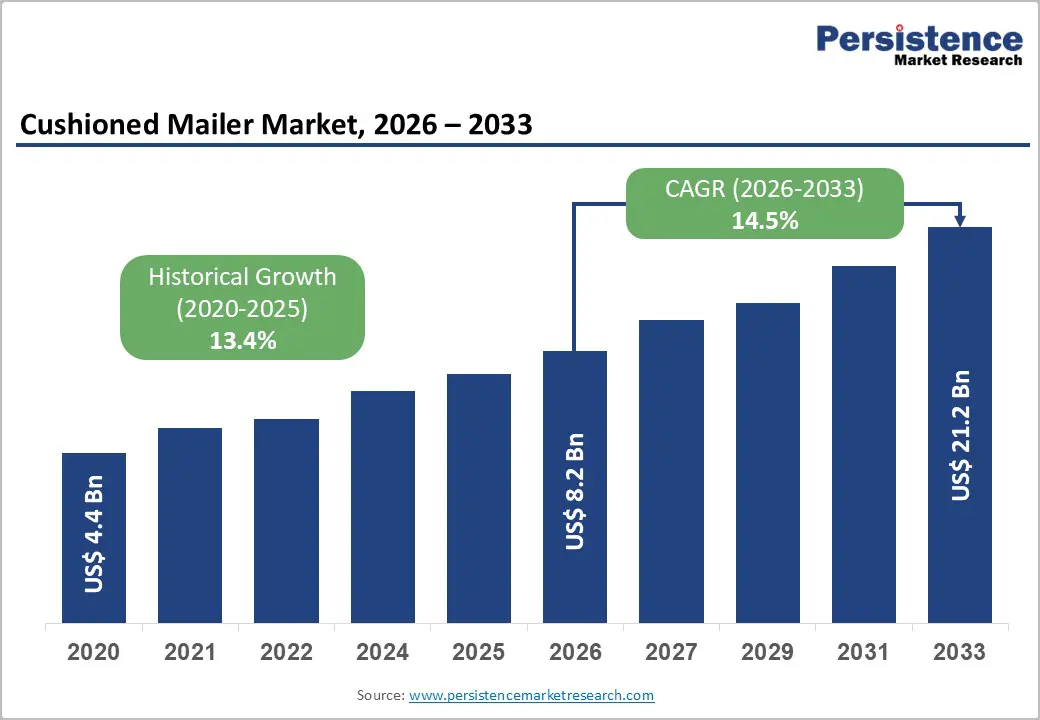

The global cushioned mailer market size is likely to be valued at US$8.2 billion in 2026 and is expected to reach US$21.2 billion by 2033, growing at a CAGR of 14.5% between 2026 and 2033, driven primarily by expanding e-commerce shipment volumes, regulatory pressure favoring recyclable protective materials, and supplier investments in lightweight, paper-based cushioning technologies.

Demand remains concentrated in e-commerce and retail logistics, while paper-based padded solutions, particularly recycled kraft formats, continue to gain share as brands and regulators accelerate the shift toward circular packaging systems. Rising order volumes, increased cross-border shipment of small-format goods such as electronics and cosmetics, and growing pressure to reduce return-related costs are driving the adoption of lightweight, high-performance mailers. Manufacturers are scaling paper-based cushioning technologies to balance protection performance, cost efficiency, and regulatory compliance.

Key Industry Highlights

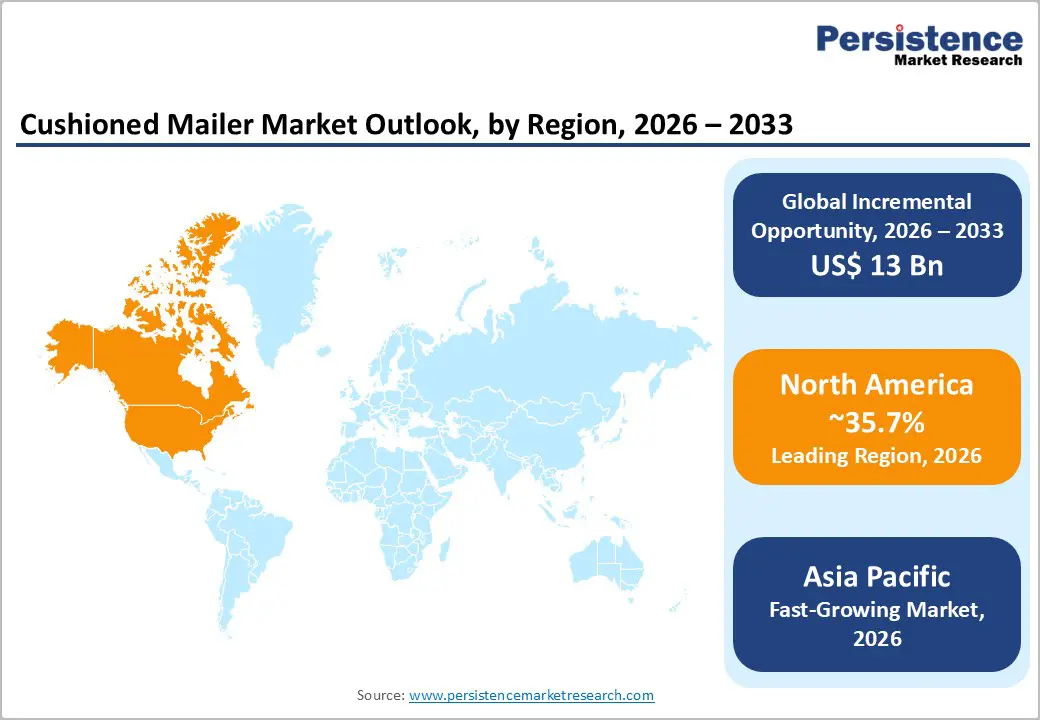

- Leading Region: North America is projected to account for approximately 35.7% of market share, supported by dense fulfillment networks, high e-commerce penetration, and strong investment in automated, paper-based cushioning systems.

- Fastest-growing Region: Asia Pacific, registering the highest regional growth rate, driven by rapid e-commerce expansion in China, India, and Southeast Asia, alongside rising investments in local paper cushioning and honeycomb production capacity.

- Investment Plans: Converters and protective-packaging suppliers are prioritizing paper-based cushioning capacity, honeycomb production lines, and on-demand fulfillment integration, with capital allocation increasingly shifting toward recyclable materials and automation-ready solutions across North America, Europe, and the Asia Pacific.

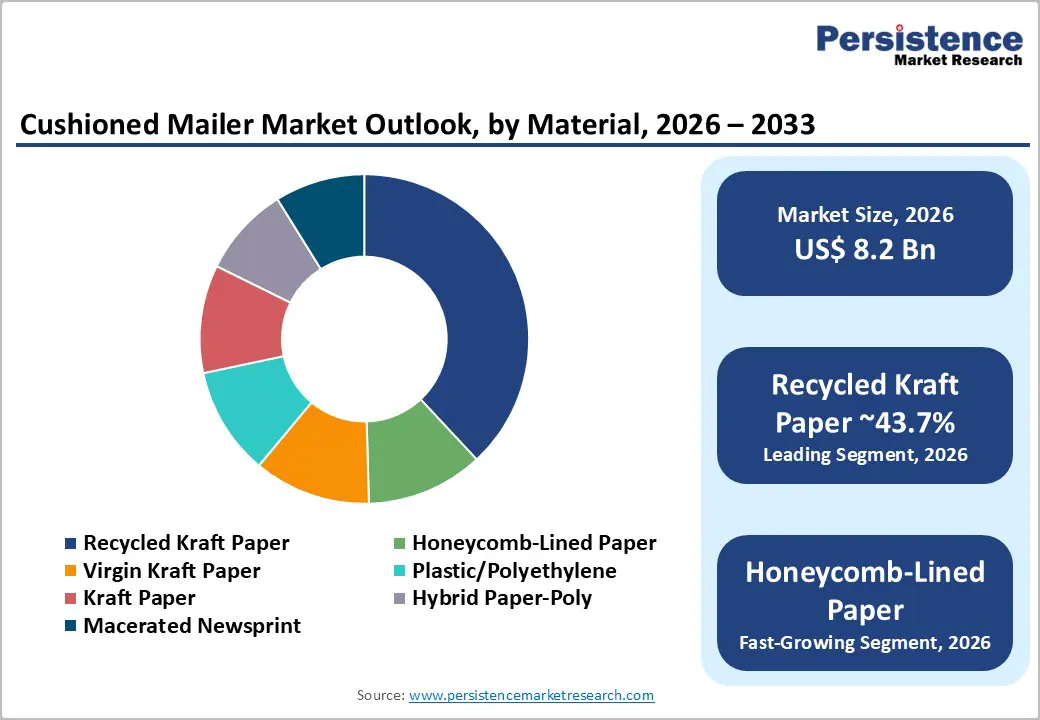

- Dominant Material: Recycled kraft paper, anticipated to hold approximately 43.7% share by material, reflecting regulatory pressure, brand sustainability commitments, and broad adoption in outer mailers and internal paper-based cushioning formats.

- Leading Cushioning Type: E-commerce and retail logistics are estimated to account for around 56.3% of market share in 2026, driven by high parcel volumes, direct-to-consumer shipping growth, and retailer sustainability standards influencing packaging material selection.

| Key Insights | Details |

|---|---|

| Cushioned Mailer Market Size (2026E) | US$8.2 Bn |

| Market Value Forecast (2033F) | US$21.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 14.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 13.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - E-commerce Volume Growth and Unitization Economics

The expansion of online retail remains the primary driver of demand for cushioned mailers. Growing parcel volumes for small, high-value products, including consumer electronics, cosmetics, personal care items, and subscription shipments, are increasing the need for protective yet lightweight packaging that minimizes dimensional-weight charges. Mailer formats continue to gain share over rigid corrugated alternatives as they reduce shipping weight, warehouse storage requirements, and packaging material usage. Lower damage rates during transit further reduce returns and reverse-logistics costs. These structural advantages support sustained demand for cushioned mailers that combine protective performance with logistics efficiency.

Regulatory and Retailer Sustainability Requirements

Regulatory initiatives, particularly in Europe, are tightening recyclability and recycled-content requirements for packaging materials. Retailers and fulfillment platforms are also strengthening internal sustainability standards and supplier compliance criteria. These developments are pushing brand owners to replace fossil-based plastic padding with paper-based cushioning solutions such as recycled kraft, honeycomb cores, and molded fiber. With regulatory timelines accelerating from mid-2026 onward, sellers shipping into regulated markets face near-term compliance obligations, prompting increased capital investment in paper cushioning capacity and closer collaboration among converters, paper mills, and e-commerce platforms.

Innovation in Paper Cushioning and Cost Convergence

Advances in paper-based cushioning technologies, including honeycomb structures, reinforced kraft bubble laminates, and automated on-demand cushioning systems, are significantly improving performance characteristics. Enhanced crush resistance, puncture strength, and shock absorption are enabling paper-based mailers to substitute traditional polyethylene bubble solutions in electronics and fragile-goods applications. Scale investments by major converters are also narrowing cost differentials with plastic-padded mailers. As total landed costs increasingly favor lighter, recyclable packaging, adoption of paper-based cushioned mailers continues to accelerate.

Barrier Analysis - Raw-Material Availability and Price Volatility

Availability and quality of recycled paper feedstock remain key operational challenges. Rising demand for recovered fiber across the broader packaging industry can tighten supply, particularly for high-grade recycled kraft suitable for cushioning applications. Short-term price volatility increases input costs for converters and may slow substitution away from plastic, where cost stability is critical. Without long-term supply contracts or investment in recycling infrastructure, fluctuations in feedstock pricing can raise operating costs by low- to mid-single-digit percentages, depending on regional sourcing dynamics and contract structures.

Performance Limitations versus Polymer Solutions

Despite continued innovation, paper-based cushioning solutions still face performance limitations in certain use cases. Moisture sensitivity, tear resistance, and barrier performance remain inferior to polymer bubble mailers in wet environments or high-puncture-risk shipments. Electronics requiring anti-static protection or enhanced moisture barriers often need hybrid constructions or secondary liners. Where adequate protection cannot be assured without added materials, buyers may retain polymer options, slowing full material substitution and increasing the importance of continued research into coatings and recyclable barrier technologies.

Opportunity Analysis - On-Demand Cushioning and Fulfillment Integration

On-demand cushioning systems installed directly within fulfillment centers allow mailers and protective padding to be produced in real time, reducing inventory requirements and packaging waste. These systems enable SKU-level customization, support just-in-time operations, and optimize shipping cube utilization. Retailers and third-party logistics providers benefit from reduced packaging complexity and measurable logistics savings. If even a modest share of large fulfillment centers adopt on-site cushioning systems, incremental equipment and consumables revenue could represent a meaningful portion of total cushioned mailer expenditure by the end of the decade.

Premiumization and Branded Packaging Experiences

Brands increasingly use sustainable, printed cushioned mailers as part of differentiated unboxing experiences. Premium recyclable mailers enhance brand perception while supporting sustainability commitments. These solutions typically command higher margins and contribute to lower return rates through improved product protection. For consumer brands allocating a small share of gross revenue to packaging, upgrades to premium paper-based cushioned mailers are economically viable and scalable. Strategic partnerships between converters and brand design teams create opportunities to capture value through customization and aesthetic differentiation.

Category-wise Analysis

Material Insights

Recycled kraft paper is anticipated to account for approximately 43.7% of total material demand in 2026, supported by strong regulatory alignment and brand-level commitments to recyclable and recycled-content packaging. The material is widely deployed both as the outer mailer substrate and as internal cushioning in macerated paper padding, kraft bubble laminates, and paper honeycomb structures. Ongoing investment in reinforced kraft grades and paper-bubble constructions has enhanced tear resistance, puncture strength, and compression performance while preserving curbside recyclability. Large converters increasingly prioritize kraft-based product portfolios for high-volume retail and marketplace clients, reinforcing the segment’s leadership across North America and Europe.

Honeycomb-lined paper mailers are likely to expand, driven by their high strength-to-weight ratios, superior shock dispersion, and compatibility with recycled fiber streams. These solutions are increasingly replacing molded pulp inserts and select polymer cushions in electronics, cosmetics, and premium personal-care shipments where protection and sustainability must coexist. Investments in continuous honeycomb production lines and automated lamination systems are improving throughput consistency and lowering unit costs. Adoption is particularly strong in regulated markets where retailers favor mono-material, paper-based protective solutions that simplify recycling and compliance reporting.

Cushioning Type Insights

Macerated paper padding is anticipated to capture approximately 40% of total cushioning-type demand in 2026, reflecting its cost efficiency, high compatibility with recycled content, and ease of integration into existing mailer production and fulfillment workflows. It is commonly used for books, apparel, household goods, and subscription box shipments, where moderate protection is sufficient, and volume efficiency is prioritized. The widespread availability of recycled paper feedstock and relatively low technical complexity make macerated padding particularly attractive to small and mid-sized e-commerce sellers. Its compatibility with on-demand cushioning systems further supports sustained adoption across decentralized fulfillment environments.

Honeycomb paper cores are likely to be the fastest-growing cushioning type, supported by superior energy absorption, structural rigidity, and thin-profile protection. These cores are increasingly used in consumer electronics accessories, small appliances, beauty products, and premium direct-to-consumer shipments, where damage reduction and dimensional-weight efficiency are critical. Honeycomb cushioning reduces package volume and eliminates the need for secondary void fill, improving shipping economics. Consistent performance outcomes, combined with strong sustainability messaging and recyclability, are accelerating adoption among brands seeking both protection assurance and environmental credibility.

Regional Insights

North America Cushioned Mailer Market Trends - E-commerce Automation and Paper-Based Packaging Innovation

North America leads the market with an estimated 35.7% share in 2026, supported by dense fulfillment infrastructure, high e-commerce penetration, and advanced packaging automation across the U.S. Large-scale retailers and logistics platforms such as Amazon, Walmart, and Target continue to influence packaging material choices through sustainability scorecards and supplier compliance programs, accelerating adoption of recyclable and paper-based cushioned mailers.

Packaging suppliers, including Sealed Air, Pregis, and Ranpak, have expanded paper cushioning portfolios and automation-compatible mailer solutions to meet high-throughput fulfillment requirements. Growing scrutiny of environmental claims by regulators and consumer advocacy groups has further pushed brands toward fiber-based materials with clearer recyclability pathways. Continued investment in honeycomb production lines, on-demand cushioning systems, and automated mailer insertion equipment supports rapid product commercialization and positions North America as a technology and innovation leader in the market.

Europe Cushioned Mailer Market Trends-PPWR Compliance and Circular-Economy Mailer Standardization

Europe represents a sustainability-driven market shaped by regulatory harmonization under the Packaging and Packaging Waste Regulation (PPWR) and strong circular-economy mandates. Recyclability, recycled-content thresholds, and waste-reduction targets are accelerating substitution toward paper-based cushioning across the region. Germany, the U.K., and France lead adoption due to mature e-commerce ecosystems and strict extended producer responsibility frameworks.

Major retailers and fashion brands such as Zalando, H&M, and Tesco have increased the use of paper-based padded mailers to align with public sustainability commitments and reporting obligations. Packaging converters, including Smurfit Westrock, DS Smith, and Mondi, are expanding kraft paper cushioning and honeycomb capabilities while consolidating regional operations to secure recycled fiber supply. Cross-border e-commerce within the EU further reinforces demand for standardized, regulation-compliant cushioned mailers that simplify recycling across multiple markets.

Asia Pacific Cushioned Mailer Market Trends: E-commerce Scale, Local Manufacturing, and Sustainability Uptake

Asia Pacific is likely to be the fastest-growing region in the cushioned mailer market, driven by rapid e-commerce expansion, proximity to manufacturing, and rising domestic consumption. China leads both production and demand, driven by large-scale fulfillment operations supporting platforms such as Alibaba, JD.com, and Pinduoduo, which increasingly promote lightweight and recyclable packaging to reduce logistics costs and waste.

India and Southeast Asia show strong growth potential as last-mile infrastructure improves and direct-to-consumer shipping expands. Regional packaging suppliers and global players are investing in local honeycomb paper core production and paper padding capacity to serve high-volume markets efficiently. As sustainability awareness rises and governments begin strengthening waste-management policies, paper-based cushioned mailers are gaining traction, positioning the Asia Pacific as both a major manufacturing hub and a rapidly expanding consumption market.

Competitive Landscape

The global cushioned mailer market is moderately concentrated among large global converters and protective-packaging specialists, alongside a fragmented base of regional manufacturers. Competitive positioning is defined by feedstock security, proprietary cushioning technologies, manufacturing scale, and the ability to integrate with fulfillment operations.

Recent activity includes expansion of paper-based mailer portfolios, strategic acquisitions to strengthen recycled fiber access, and pilot programs for on-site cushioning systems within fulfillment centers. These developments reflect a broader shift toward sustainable materials, operational efficiency, and customer-embedded packaging solutions.

Leading companies emphasize sustainability-driven innovation, vertical integration for raw-material security, bundled equipment-and-consumables models, and selective acquisitions to expand paper cushioning capacity and geographic reach.

Key Industry Developments

- In November 2025, DS Smith introduced a new range of 100% recyclable cardboard buffers aimed at protecting industrial machinery components, reflecting a broader movement toward recyclable protective materials that also influence cushioned mailer product development.

- In April 2025, Novolex completed its acquisition of Pactiv Evergreen, strengthening its sustainable mailers portfolio and expanding its fiber-based packaging capabilities, including paper-padded mailer solutions.

Companies Covered in Cushioned Mailer Market

- Sealed Air

- Pregis

- Ranpak

- Smurfit Westrock

- DS Smith

- Mondi

- Intertape Polymer Group

- ProAmpac

- Storopack

- Huhtamaki

- Packsize

- Polyair

- Rajapack

- Shorr Packaging

- International Paper

- Uline

- Pratt Industries

- Berry Global

Frequently Asked Questions

The global cushioned mailer market size is valued at US$ 8.2 billion in 2026.

By 2033, the cushioned mailer market is expected to reach US$ 21.2 billion.

Key trends include the shift from plastic to paper-based cushioned mailers, rising use of recycled kraft paper and honeycomb structures, integration of on-demand cushioning systems in fulfillment centers, and growing emphasis on regulatory compliance and sustainability scorecards from major retailers and marketplaces.

By application, e-commerce and retail logistics are the leading segment, accounting for approximately 56.3% of market share, while recycled kraft paper dominates by material with around 43.7% share.

The cushioned mailer market is projected to grow at a CAGR of 14.5% between 2026 and 2033.

Major players with strong cushioned mailer and paper-based protective packaging portfolios include Sealed Air, Pregis, Ranpak, Smurfit Westrock, and Mondi.