- Power Generation, Transmission, & Distribution

- Current Transducer Market

Current Transducer Market Size, Share, and Growth Forecast, 2026 - 2033

Current Transducer Market by Current Sensing Method (Direct Current Sensing and Indirect Current Sensing), Loop Type (Closed Loop, and Open Loop), Technology (Isolated Current Transducers, and Non-Isolated Current Transducers), End-user (Industrial, Automotive, Consumer Electronics, Telecom & Networking, Healthcare, Energy & Power, and Others), and Regional Analysis for 2026 - 2033

Current Transducer Market Size and Trends Analysis

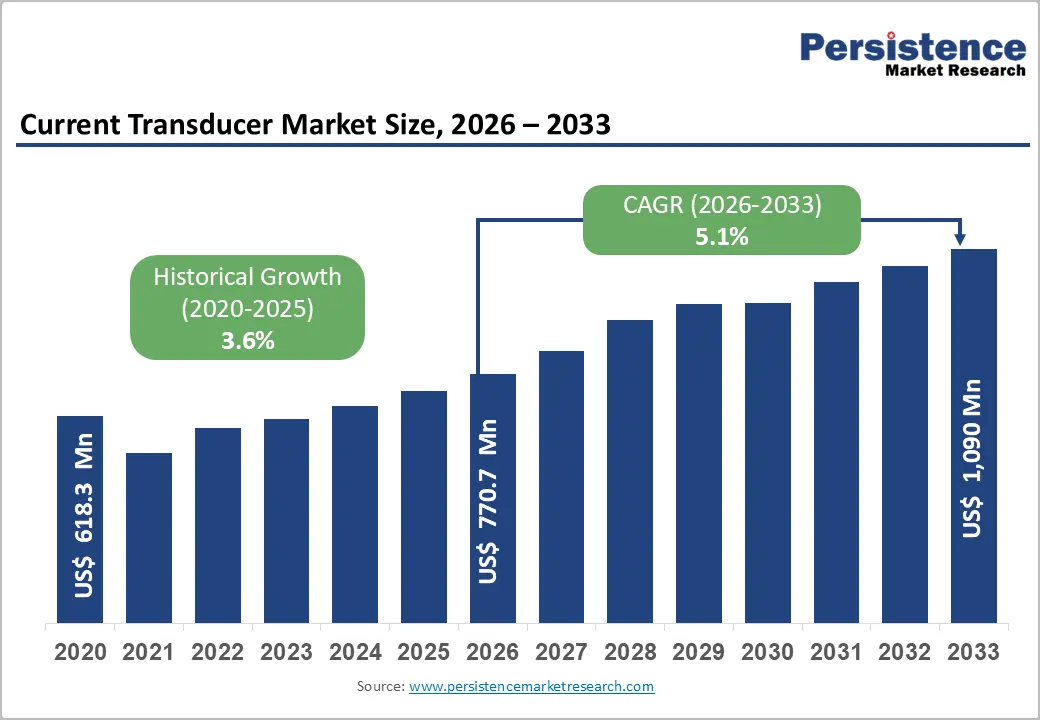

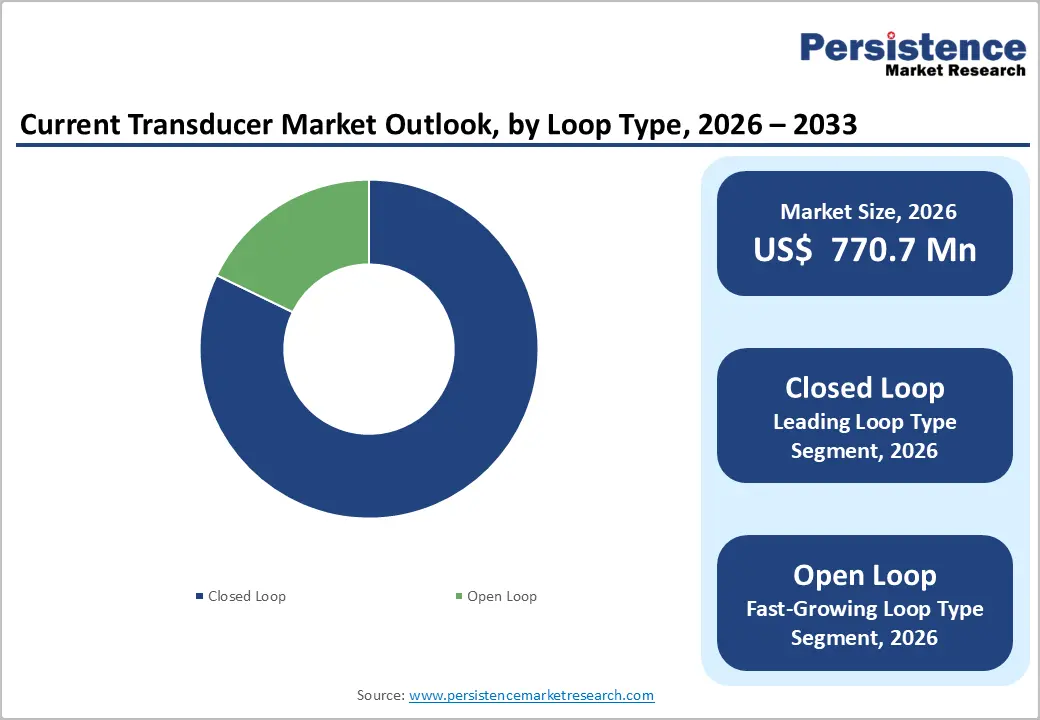

The global current transducer market size is likely to be valued at US$ 770.7 million in 2026 and is projected to reach US$ 1,090 million by 2033, growing at a CAGR of 5.1% between 2026 and 2033. The market has expanded steadily from US$ 618.3 million in 2020, reflecting a historical CAGR of 3.6%, and is now entering a faster growth phase driven by electrification, industrial automation, and renewable energy integration.

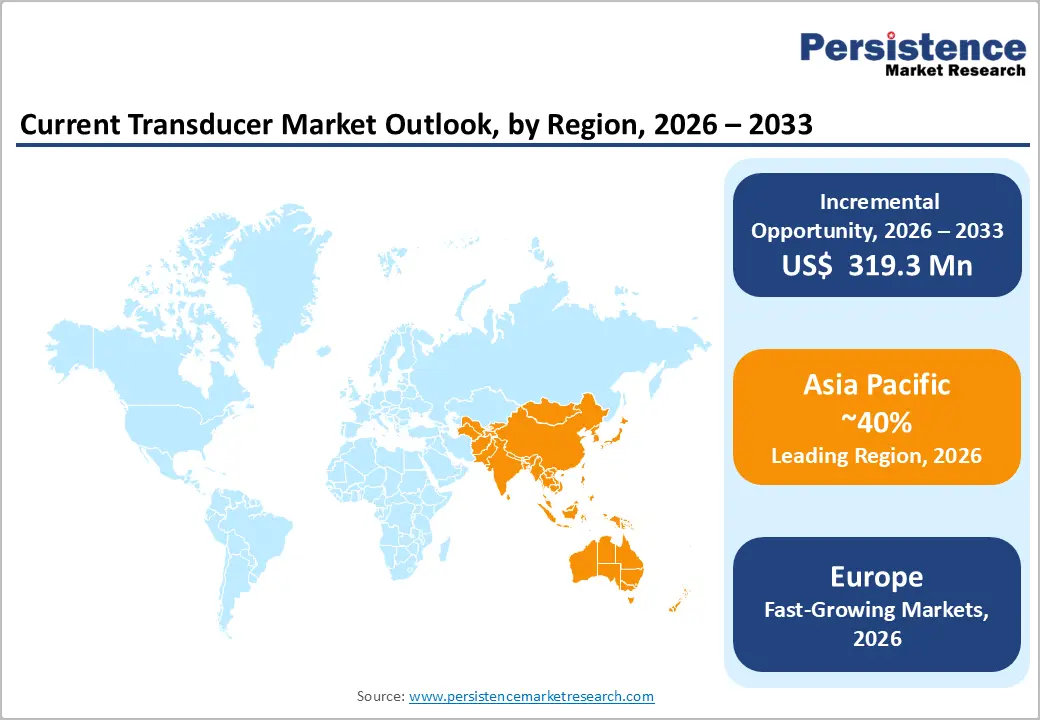

Direct current sensing and isolated current transducers dominate the market, while open-loop architectures and automotive applications are poised for the fastest growth. Asia Pacific leads with over 40% revenue share, supported by large-scale manufacturing and energy infrastructure investments, while Europe emerges as the fastest-growing region with a forecast CAGR of 5.7%.

Key Industry Highlights:

- Current Sensing Method Analysis: Direct current sensing dominates with over 70% revenue share, while indirect sensing is the fastest-growing method with a CAGR of 5.5%.

- Loop Type Analysis: Closed loop transducers account for more than 65% of revenue, but open loop solutions are expanding fastest with a 5.7% CAGR, supported by cost and size advantages.

- Technology Segment Analysis: Isolated current transducers hold above 70% revenue share, confirming the central role of galvanic isolation in industrial, energy, and automotive applications.

- End User Segment Analysis: The industrial end-user segment contributes over 35% of global revenue, while the automotive segment leads growth at 5.8% CAGR, driven by EV and electronics content growth.

- Regional Analysis: Asia Pacific leads with more than 40% revenue share, supported by manufacturing scale and infrastructure investments, while Europe is the fastest-growing region with a 5.7% CAGR.

- Recent strategic developments include next-generation isolated current sensor launches for EV and industrial drives, portfolio-enhancing M&A, and geographic expansions targeting Asia Pacific and Europe.

| Key Insights | Details |

|---|---|

|

Current Transducer Market Size (2026E) |

US$ 770.7 Mn |

|

Market Value Forecast (2033F) |

US$ 1090 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

5.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.6% |

Market Dynamics

Drivers - Rapid Growth in Electric Vehicle Adoption Accelerating Demand for Advanced Current Sensing Solutions

The rapid global adoption of electric vehicles is a key growth driver for advanced current sensing and transducer markets. According to the International Energy Agency (IEA), electric car sales exceeded 17 million units in 2024, representing more than 20% of total new vehicle sales worldwide and reflecting year-on-year growth of over 25%. The scale of expansion is underscored by the fact that the incremental electric cars sold in 2024 alone surpassed total global EV sales recorded in 2020. China continues to lead this transition, with more than 11 million electric cars sold in 2024, reinforcing the global momentum toward electrified mobility. This sustained growth in EV penetration is structurally increasing demand for high-performance current transducers, which are integral to battery management systems, inverters, onboard chargers, and power distribution units in electric and hybrid vehicles.

As modern vehicles adopt high-voltage architectures and increasingly dense power electronics, OEMs require current sensing solutions that deliver high accuracy, galvanic isolation, fast response times, and wide dynamic range. These technical demands favor advanced isolated current transducers and precision shunt-based sensing technologies. Consequently, the automotive end-user segment is emerging as the fastest-growing application, expanding at a CAGR of 5.8%, and is driving higher value content per vehicle and overall market value growth.

Accelerating electrification in industrial and energy systems

The shift toward electrified, digitally controlled industrial and energy infrastructure is a primary growth engine for the current transducer market. Governments and utilities are investing heavily in smart grids, renewable integration, and power quality monitoring, which depend on accurate current sensing for protection, billing, and grid stability. Industrial automation, including motor drives, variable frequency drives, and robotics, requires high-precision current transducers to optimize efficiency and prevent equipment failures. As global electricity demand continues to grow in line with GDP and urbanization trends, and as industries pursue energy efficiency and predictive maintenance, demand for reliable, isolated current transducers in medium- and high-voltage systems will continue to expand, supporting the uplift from a 3.6% historical CAGR to 5.1% going forward.

Restraint - Design complexity and integration challenges in high-reliability applications

Integrating current transducers into safety-critical systems (e.g., grid protection, EV powertrains, medical equipment) demands rigorous qualification, calibration, insulation coordination, and standards compliance. These requirements lengthen design cycles and increase validation costs. In some cases, system designers may prefer well-understood legacy topologies to avoid qualification risk, slowing migration to newer transducer technologies. Additionally, the need to manage electromagnetic interference, thermal drift, and long-term stability raises engineering complexity. This can discourage smaller OEMs from adopting advanced solutions, especially where in-house expertise is limited, acting as a structural brake on the highest-end segments.

Opportunity - Smart grids, advanced metering, and power quality solutions

Utilities and commercial facilities are investing in smart meters, advanced metering infrastructure (AMI), and power quality analyzers to reduce losses and improve reliability. High-precision current transducers can be embedded in these systems as well as in feeder monitoring units, reclosers, and protection relays. As markets modernize aging grids and integrate DERs (distributed energy resources), the addressable demand for compact, accurate, and temperature-stable current transducers will grow. This opportunity is particularly strong in Asia Pacific and Europe, where grid modernization and decarbonization policies are accelerating, providing a scalable and recurring demand base over the forecast period.

Category-wise Analysis

Current Sensing Method Insights - Direct Sensing Dominates Today While Indirect Methods Accelerate with Electrification Demand

Direct current sensing remains the leading method in the global current transducer market, accounting for over 70% of total revenue share. Its dominance is driven by high accuracy, strong linearity, and cost efficiency, particularly in low- to medium-voltage applications. Technologies such as shunt resistors and integrated current sense amplifiers are widely adopted due to their mature supply ecosystem and ease of integration with both analog and digital signal-processing architectures. OEMs across industrial equipment, automotive electronics, and consumer devices favor direct sensing because of its relatively low bill-of-materials cost and proven reliability. Extensive deployment in power supplies, motor drives, and battery management systems further reinforces its position as the default sensing solution. As a result, direct sensing is expected to remain the baseline choice for many system designs despite evolving performance requirements.

In contrast, indirect current sensing represents the fastest-growing segment, expanding at a CAGR of approximately 5.5%. Based on magnetic field technologies such as Hall effect and fluxgate sensors, indirect sensing offers galvanic isolation, enhanced operational safety, and superior performance in high-voltage and high-current environments. These attributes make it especially suitable for electric vehicle powertrains, renewable energy inverters, and grid-connected applications. Although its current revenue share is smaller, rising electrification, stricter safety regulations, and increasing system voltages are steadily accelerating adoption, supporting long-term market share expansion.

Loop Type Insights - Closed Loop Dominance and Open Loop Growth Shaping Current Transducer Market Dynamics

By loop type analysis, closed loop current transducers emerge as the leading segment, accounting for more than 65% of total revenue, driven by their superior performance in accuracy-critical applications. Their strong adoption is closely linked to requirements for high precision, fast response times, and excellent linearity across wide current ranges. These characteristics make closed loop transducers indispensable in precision motor drives, servo systems, industrial automation equipment, and advanced power conversion systems, where accurate current feedback is essential for operational efficiency, system stability, and safety. The feedback-based operating principle minimizes offset and drift while delivering robust dynamic performance, allowing these devices to command premium pricing in mission-critical industrial and energy applications. As a result, closed loop technology continues to dominate the installed base across industrial and power end-user segments.

In contrast, open loop current transducers represent the fastest-growing segment, projected to expand at a CAGR of 5.7%. Their simpler design, lower manufacturing cost, reduced power consumption, and compact form factor make them well suited for high-volume, space-constrained applications such as consumer electronics, compact power supplies, and various automotive subsystems. Ongoing advancements in magnetic materials, compensation techniques, and signal processing are steadily narrowing the performance gap with closed loop solutions, enabling open loop designs to secure an increasing share of new design wins.

Technology Insights - Isolated Current Transducers Dominate Revenue While Non-Isolated Technologies Drive Emerging Growth

Isolated current transducers represent the leading technology segment, accounting for over 70% of total market revenue, highlighting the growing importance of galvanic isolation in modern electrical and electronic systems. Isolation plays a critical role in safeguarding low-voltage control electronics from high-voltage power stages, ensuring operational safety, regulatory compliance, and long-term system reliability. This requirement is particularly pronounced across industrial motor drives, grid infrastructure, electric vehicle powertrains, and medical equipment. Technologies such as Hall effect and fluxgate-based isolated transducers provide strong electrical insulation, high common-mode transient immunity, and stable performance over extended service lifetimes. Their dominance is further reinforced by the industry-wide shift toward higher voltage architectures, including 800 V electric vehicle platforms and high-voltage direct current systems, alongside increasingly stringent global safety standards that make isolation essential in new designs.

In contrast, non-isolated current transducers, although holding a smaller overall share, are emerging as the fastest-growing segment. Their lower cost, compact size, and ease of integration make them well-suited for low-voltage, board-level applications where system-level isolation is already present. As designers pursue higher power density, finer current monitoring, and cost optimization in consumer electronics, computing, telecom power supplies, and industrial controls, adoption of non-isolated sensing solutions continues to accelerate, driving strong unit-volume growth.

End-user Insights - Industrial Dominance and Automotive Electrification Driving Current Transducer End-User Demand Globally

The industrial segment represents the leading end-user category in the global current transducer market, accounting for more than 35% of total revenue. Its dominance is supported by widespread deployment across factory automation, motor drives, process industries, heavy machinery, and industrial power supply systems. Industrial customers place strong emphasis on measurement accuracy, operational reliability, and long-term stability, as equipment often runs continuously under harsh environmental conditions. Current transducers are extensively integrated into motor control centers, variable frequency drives, welding systems, uninterruptible power supplies, and power conditioning equipment. Continued modernization of manufacturing facilities, rising adoption of Industrial Internet of Things (IIoT) platforms, and stricter energy efficiency targets sustain steady baseline demand. In addition, the large installed base across industrial facilities creates a consistent replacement and retrofit market, reinforcing the segment’s long-term revenue stability.

In contrast, the automotive segment is emerging as the fastest-growing end-user, expanding at a CAGR of 5.8%. Growth is driven by rapid vehicle electrification, including electric, hybrid, and plug-in hybrid vehicles, alongside increasing electronic complexity. Current transducers play a critical role in battery management systems, traction inverters, DC-DC converters, on-board chargers, and auxiliary subsystems. As automakers adopt higher-voltage architectures to improve efficiency, safety, and battery longevity, demand for precise, isolated, and temperature-resistant current sensing solutions continues to accelerate.

Regional Insights and Trends

Asia Pacific Leads Global Current Transducer Demand Through Industrialization and Electrification Growth

Asia Pacific represents the largest and most influential regional market, accounting for more than 40% of global revenue and is expected to retain its leadership throughout the forecast period. The region’s dominance is underpinned by extensive manufacturing ecosystems, rapid industrialization, expanding power infrastructure, and strong growth across automotive, electronics, and industrial automation sectors. China plays a pivotal role as both a major production base and end-use market for current transducers, supplying domestic and global OEMs serving industrial equipment, renewable energy systems, and electric vehicles. Japan strengthens regional demand through advanced automation, robotics, and automotive manufacturing, where high precision, reliability, and quality standards drive adoption of premium sensing solutions.

India and ASEAN economies are emerging as high-growth markets, supported by accelerating investments in renewable energy capacity, grid modernization, industrial automation, and large-scale infrastructure development. These trends are significantly expanding the addressable market for current transducers across power generation, distribution, and end-use applications. Asia Pacific also benefits from cost-competitive manufacturing, localized supply chains, and strong component ecosystems that support both global brands and regional players. Favorable policy frameworks promoting renewable energy, EV adoption, and smart city development further reinforce long-term demand. Despite its mature scale, continued expansion in EVs, solar installations, and data centers ensures Asia Pacific remains the primary driver of global volume growth.

North America Drives Premium Current Transducer Demand Through Innovation And Infrastructure Investments

North America represents a mature yet strategically vital market for current transducers, distinguished by high technology adoption, the strong presence of leading OEMs, and well-established regulatory frameworks focused on electrical safety and energy efficiency. The United States anchors regional demand, driven by sustained investments in grid modernization, hyperscale data centers, electric mobility, and advanced industrial automation. Current transducers are extensively deployed across utility-scale renewable energy installations, commercial and industrial buildings, and mission-critical facilities such as hospitals and data centers, where accuracy and reliability are non-negotiable. Stringent regulations governing grid reliability and electrical safety further reinforce demand for high-quality, certified transducer solutions.

The region benefits from a robust innovation ecosystem, with semiconductor and sensor manufacturers actively developing advanced Hall-effect and fluxgate-based technologies. These solutions are increasingly integrated with digital interfaces, diagnostics, and smart monitoring capabilities, supporting growth in premium segments such as smart transducers and highly integrated current-sense ICs. Although overall market growth in North America is comparatively moderate relative to the Asia Pacific, the region continues to define global performance benchmarks and technical standards. Competitive intensity remains high, as global tier-1 suppliers and specialized niche players compete on innovation, long-term reliability, and value-added services. Continued expansion of EV charging infrastructure and data center capacity remains a key investment theme, sustaining long-term demand.

Competitive Landscape

The current transducer market is moderately consolidated at the high-performance end, with a set of global players holding significant shares, while fragmented regional manufacturers compete in cost-sensitive and niche segments. Leading companies typically focus on isolated transducers and advanced sensing ICs, addressing industrial, automotive, and energy applications where reliability and certification are critical. Market concentration is higher in safety-critical and high-voltage segments, where barriers to entry are elevated by technology complexity and qualification requirements. Competitive positioning hinges on technology differentiation, application expertise, and global support capabilities, rather than price alone.

Key Industry Developments:

- In April 2025, Allegro MicroSystems introduced three new solutions designed to enhance motor drives, motor control, and thermal management performance for e-mobility and industrial automation applications. The ACS37035 and ACS37630 current sensors, along with the A89347 automotive-grade fan driver IC, offer improved accuracy, efficiency, and thermal performance across a wide range of use cases.

- In March 2025, Danisense announced the introduction of Transducer Electronic Datasheet (TEDS) functionality in its current-sense transducers. The new feature is designed to help engineers optimize laboratory testing procedures by simplifying system setup and improving measurement accuracy in test and calibration environments.

- In March 2025, Diodes Incorporated unveiled its first series of advanced InSb Hall element sensors for rotation speed detection and current measurement. These sensors target consumer and industrial applications, including laptops, mobile devices, household appliances, and brushless motors, and are offered in standard 4-pin SOT23-4 and SIP-4 packages to improve accessibility and integration.

- In December 2024, NOVOSENSE Microelectronics launched a new range of automotive-grade, high-bandwidth current sensors requiring no external isolation components. The NSM211x series is intended for applications such as onboard chargers, DC-DC converters, motor control systems, EV charging stations, and fuel-cell platforms.

- In October 2024, A research study published by Wiley presented an integrated quantum diamond sensor capable of precise, wide-range current measurement. The solution employs optical fiber and directional microwave antennas to minimize size and power consumption on the high-voltage side, enabling zero power usage at high voltage and remote signal demodulation over distances exceeding 10 meters.

- In 2023, Danisense launched a new high-performance current transducer specifically designed for automotive EV test benches and battery testing applications. The product features a large 41.2 mm aperture to accommodate high-power cables and connectors, supports a nominal current rating of 1000 Arms, and delivers ultra-high linearity of 1 ppm, addressing the accuracy demands of advanced EV validation environments.

Companies Covered in Current Transducer Market

- ABB

- Texas Instrument Inc.

- Johnson Control Inc.

- Topstek Inc.

- Veris industries

- NK Technologies

- CR Magnetic

- Siemens AG

- Hobart

- Johnson controls FDC

- Other Market Players

Frequently Asked Questions

The Current Transducer market is estimated to be valued at US$ 770.7 Mn in 2026.

The primary demand driver for the current transducer market is the rapid global electrification of energy, mobility, and industrial systems, which require precise, reliable, and real-time current measurement for safety, efficiency, and control.

In 2026, the Asia Pacific region will dominate the market with an exceeding 75% revenue share in the global Current Transducer market.

Among current sensing methods, direct current sensing has the highest preference, capturing beyond 70% of the market revenue share in 2026, surpassing other current sensing methods.

ABB, Texas Instrument Inc., Johnson Control Inc., Topstek Inc., Veris Industries, and NK Technologies. There are a few leading players in the Current Transducer market.