- Automotive Components & Materials

- Automotive Horn Systems Market

Automotive Horn Systems Market Size, Share, and Growth Forecast, 2025 - 2032

Automotive Horn Systems Market By Product Type (Electric Horns, Air Horns), Sound Level (Below 100 dB, 100 dB -120 dB, Above 120 dB), Vehicle Type, and Regional Analysis for 2025 – 2032

Automotive Horn Systems Market Size and Trends Analysis

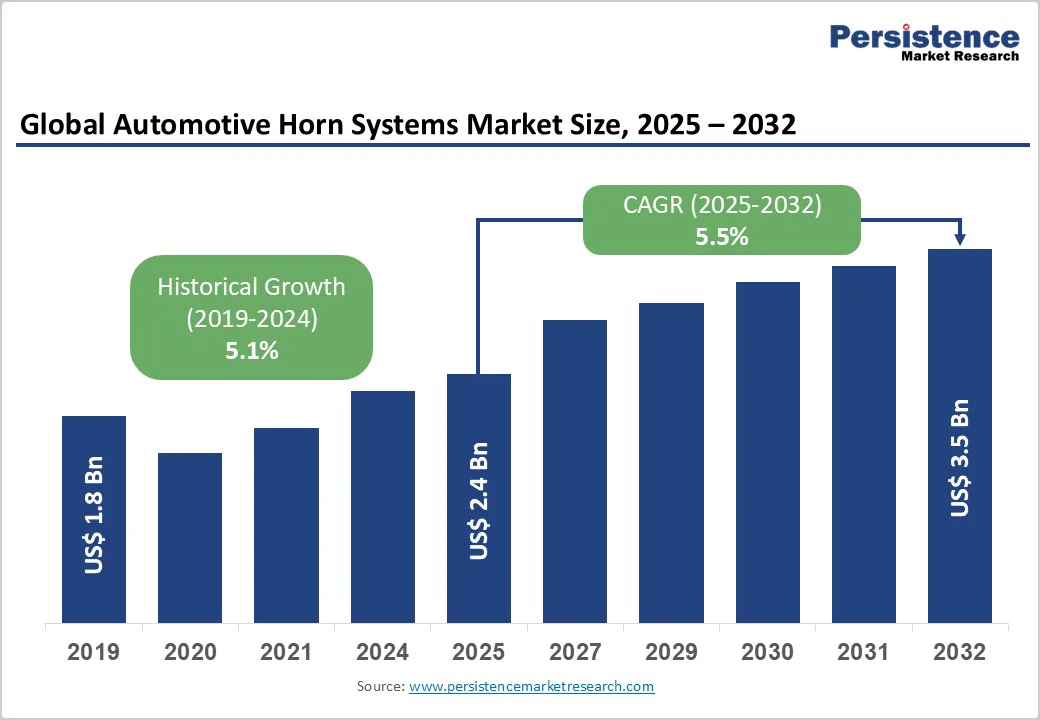

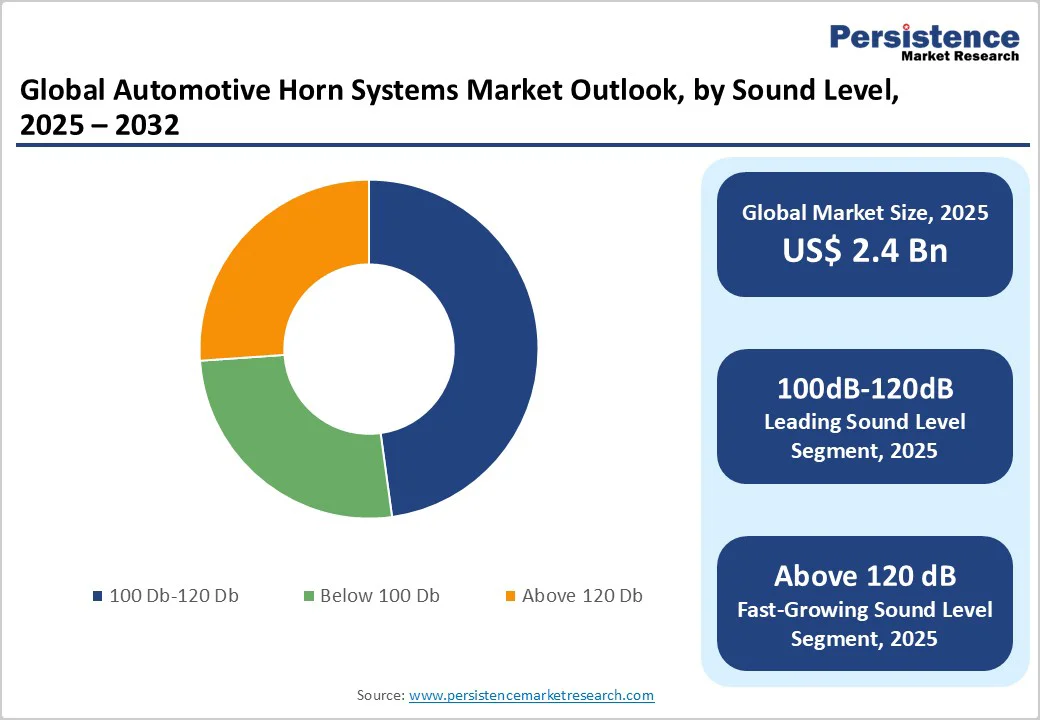

The global automotive horn systems market size is likely to be valued US$2.4 Billion in 2025, estimated to US$3.5 Billion by 2032, growing at a CAGR of 5.5% during the forecast period from 2025 to 2032, driven by the increasing prevalence of road safety regulations, rising vehicle production, and advancements in horn technologies. The need for effective audible warning systems, particularly in high-traffic urban areas, has significantly boosted the adoption of automotive horn systems across various demographics. The market is further propelled by innovations in electric and air horns, catering to preferences for compact and high-decibel options. The growing acceptance of automotive horn systems as standard safety features, particularly in passenger cars, is a key growth factor.

Key Industry Highlights:

- Leading Region: Asia Pacific, commanding a 45% market share in 2025, driven by massive vehicle manufacturing, high prevalence of two-wheelers, and strong R&D activities in India.

- Fastest-growing Region: Europe, fueled by stringent safety norms, rising awareness of audible alerts, and growing investments in automotive innovation in countries Germany and UK.

- Dominant Product Type: Electric horns, holding approximately 65% of the market share, due to their reliability and ease of integration.

- Leading Sound Level: 100 dB -120 dB, accounting for over 50% of market revenue, driven by balanced audibility and regulatory compliance.

- Leading Vehicle Type: Passenger cars, contributing nearly 40% of market revenue, due to urban commuting demands.

- Key Market Driver: Increasing government mandates for vehicle safety and audible warning systems are boosting demand for reliable and compliant horn technologies.

- Market Opportunity: Rising replacement demand and customization trends, especially in emerging markets, create lucrative opportunities for horn manufacturers.

| Key Insights | Details |

|---|---|

| Automotive Horn Systems Market Size (2025E) | US$2.4 Bn |

| Market Value Forecast (2032F) | US$3.5 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Road Safety Regulations and Demand for Audible Warning Systems

The rising prevalence of road safety regulations and increasing demand for audible warning systems are key factors driving the growth of the vehicle horn market. Governments across the globe are tightening safety norms to reduce road accidents and enhance driver awareness, leading to mandatory installation of horns that meet specific sound and frequency standards. These regulations ensure that horns are effective yet compliant with noise pollution norms, prompting manufacturers to innovate with electronic and dual-tone systems.

The surge in urban traffic and the need for quick communication between vehicles have amplified the adoption of advanced audible warning systems in both passenger and commercial vehicles. Automakers are integrating smart and eco-friendly horns equipped with electronic controls to deliver precise and reliable alerts. Additionally, the growing production of electric and hybrid vehicles is spurring the development of low-power, compact, and customizable horn systems.

High Development and Regulatory Compliance Costs

The high costs associated with development and regulatory approval of automotive horn systems pose a significant restraint on market growth. Manufacturers are required to meet stringent safety, environmental, and noise-level regulations that vary across regions, leading to complex and expensive testing, certification, and redesign processes. Developing horns that comply with international standards such as ECE, AIS, and SAE involves advanced acoustic engineering, durable materials, and electronic integration, all of which increase production costs.

The shift toward electric and hybrid vehicles demands specialized low-voltage systems that maintain performance while minimizing energy consumption, further escalating research and development expenses. Small and medium-sized manufacturers often struggle to keep up with these evolving compliance requirements, limiting market entry and innovation. Additionally, regulatory updates on permissible sound levels and sustainability standards push companies to continuously upgrade product lines and manufacturing processes, impacting profit margins.

Advancements in Smart and Integrated Horn Technologies

Advancements in smart and integrated horn technologies present significant growth opportunities for the automotive horn systems market. Modern vehicles are increasingly adopting electronic and digitally controlled horn systems that can be integrated with advanced driver-assistance systems (ADAS) and vehicle communication networks. These smart horns are capable of modulating sound levels, tones, and durations based on driving conditions, enabling more context-sensitive alerts for example, gentle alerts for urban settings and louder tones for highways.

Integration with vehicle sensors allows automatic activation in potential collision scenarios, improving response times and preventing accidents. Furthermore, the rise of electric and hybrid vehicles has driven the development of low-noise, energy-efficient horns compatible with 12V and 48V systems. Some manufacturers are also exploring AI-enabled and connected horn systems that can communicate with nearby vehicles or infrastructure to enhance road coordination. These innovations not only meet global safety and noise compliance standards but also align with the growing trend toward intelligent, eco-friendly, and personalized automotive technologies, marking a major leap forward in vehicle communication systems.

Category-wise Analysis

Product Type Insights

Electric Horns dominates the market, accounting for 65% of the share in 2025. Its dominance is driven by reliability, compact design, and cost-effectiveness, making it a preferred choice for passenger cars. Electric horns, such as those from Fiamm Group, provide consistent sound with minimal maintenance, ensuring compatibility. Its efficiency and integration make it preferred for manufacturers.

Air Horns is the fastest-growing segment, driven by high decibel output and increasing adoption in commercial vehicles. Air horns offer superior audibility, appealing for heavy-duty uses. Focus on pneumatic innovation accelerates adoption in Asia Pacific and North America.

Sound Level Insights

100 dB -120 dB leads the market, holding approximately 50% of the share in 2025, driven by its ideal balance between audibility and urban noise compliance. These horns are widely used in passenger cars and two-wheelers for effective signaling, offering accessibility, regulatory compliance, and strong demand across both developed and emerging automotive markets.

Above 120 dB is the fastest-growing segment, propelled by increasing industrial applications and widespread use in commercial vehicles. These high-decibel horns provide strong, clear alerts essential for large or noisy environments. Their rapid adoption is further supported by evolving safety regulations and the demand for reliable, high-performance warning systems.

Vehicle Type Insights

Passenger Cars leads the market, contributing nearly 40% of revenue in 2025. Their widespread use for daily commuting and emphasis on advanced safety features drive this leadership. Integrated horn systems in passenger vehicles enhance driver communication, reliability, and compliance with evolving safety regulations, reinforcing their strong market position.

Two Wheelers is the fastest-growing segment, driven by massive production volumes in Asia Pacific and rising road safety awareness among riders. Increasing demand for affordable yet high-performance horn systems enhance adoption across motorcycles and scooters. Manufacturers focus on durable, compact, and energy-efficient solutions to meet regional safety and cost expectations.

Regional Insights

Asia Pacific Automotive Horn Systems Market Trends

Asia Pacific is the leading market for automotive horn systems, accounts 45% share in 2025, driven by expanding vehicle production, rising middle-class ownership, and high two-wheeler volumes across key countries such as China, India, Japan, and South Korea. Governments in the region are enforcing stricter road safety and noise regulations, boosting demand for reliable and efficient audible warning systems. Local manufacturing advantages, including cost-effective labor and a strong supplier base, make Asia Pacific not only a major consumer market but also a global production hub for automotive horn systems.

The rapid adoption of electric and hybrid vehicles is further shaping the market, prompting the development of low-voltage, energy-efficient, and electronically integrated horn systems compatible with EV platforms and pedestrian safety features. Additionally, the aftermarket segment is growing rapidly as consumers seek performance upgrades, distinct sound profiles, and better audibility in densely populated urban environments.

North America Automotive Horn Systems Market Trends

North America is projected to account for nearly 25% of the global Automotive Horn Systems Market in 2025, driven by high vehicle safety standards and automotive production in the U.S. The region benefits from high vehicle ownership rates, a strong automotive manufacturing base, and a mature aftermarket network that drives both OEM installations and replacement demand. Stringent safety and noise-pollution regulations in the U.S. and Canada continue to shape product development, prompting manufacturers to design horns that ensure optimal audibility while complying with noise limits.

The growing adoption of electric and hybrid vehicles has further influenced innovation, leading to the development of low-voltage, energy-efficient, and electronically controlled horn systems integrated with advanced driver-assistance systems (ADAS). The rising focus on vehicle personalization and advanced sound modulation technologies supports the trend toward smart, multi-tone, and digital horns.

Europe Automotive Horn Systems Market Trends

Europe holds 20% share in 2025 and is the fastest-growing region, driven by stringent EU safety and noise-emission regulations that mandate reliable audible warning systems, particularly in hybrid and electric vehicles. With the rising adoption of EVs across Europe, demand for advanced horn technologies that enhance pedestrian safety has surged. Automakers are increasingly integrating electronic, multi-tone, and smart horn systems that connect with vehicle electronics and driver-assistance systems to deliver precise, situation-based alerts.

The strong presence of premium and luxury car manufacturers in Germany, France, and the UK further contributes to the adoption of technologically advanced and durable horn systems. Additionally, growing concerns over urban noise pollution are encouraging the development of eco-friendly, compliant horns that balance audibility with reduced environmental impact.

Competitive Landscape

The global automotive horn systems market is highly competitive, characterized by a mix of global automotive suppliers and specialized manufacturers. In developed regions North America and Europe, large players such as Robert Bosch GmbH, Hella KGaA Hueck & Co., and Denso Corporation dominate through advanced R&D capabilities and established supply chains.

In the Asia Pacific, regional players such as Uno Minda are gaining traction by offering cost-effective solutions tailored to local markets. Companies are focusing on product innovation, such as smart and integrated horns, to gain a competitive edge. Strategic partnerships, acquisitions, and investments in acoustic technologies are further intensifying the competitive landscape.

Key Developments

- In March 2024, Robert Bosch GmbH introduced a new range of smart horn systems that integrate AI for enhanced safety features.

- In April 2024, Uno Minda introduced the “Ultimo C80” premium trumpet horn in the Indian aftermarket, developed in collaboration with Clarton Horn S.A.U. (Spain) and delivering over 105 dB output.

Companies Covered in Automotive Horn Systems Market

- Fiamm Group

- Hella KGaA Hueck & Co.

- Robert Bosch GmbH

- Uno Minda

- Denso Corporation

- Imasen Electric Industrial Co. Ltd.

- Wolo Manufacturing Corp.

- INFAC Corporation

- Seger

- MARCO S.p.A.

- Others

Frequently Asked Questions

The global automotive horn systems market is projected to reach US$2.4 Billion in 2025.

The rising prevalence of road safety regulations and demand for audible warning systems are key drivers.

The market is poised to witness a CAGR of 5.5% from 2025 to 2032.

Advancements in smart and integrated horn technologies are a key opportunity.

Fiamm Group, Hella KGaA Hueck & Co., Robert Bosch GmbH, Denso Corporation, and Uno Minda are key players.