1. Executive Summary

1.1. Global Automotive Diagnostic Scan Tools Market Snapshot, 2024 and 2031

1.2. Market Opportunity Assessment, 2024 - 2031, US$ Bn

1.3. Key Market Trends

1.4. Future Market Projections

1.5. Premium Market Insights

1.6. Industry Developments and Key Market Events

1.7. PMR Analysis and Recommendations

2. Market Overview

2.1. Market Scope and Definition

2.2. Market Dynamics

2.2.1. Drivers

2.2.2. Restraints

2.2.3. Opportunity

2.2.4. Challenges

2.2.5. Key Trends

2.3. Product Lifecycle Analysis

2.4. Automotive Diagnostic Scan Tools Market: Value Chain

2.4.1. List of Raw Material Supplier

2.4.2. List of Manufacturers

2.4.3. List of Distributors

2.4.4. Profitability Analysis

2.5. Forecast Factors - Relevance and Impact

2.6. Covid-19 Impact Assessment

2.7. PESTLE Analysis

2.8. Porter Five Force’s Analysis

2.9. Geopolitical Tensions: Market Impact

2.10. Regulatory and Technology Landscape

3. Macro-Economic Factors

3.1. Global Sectorial Outlook

3.2. Global GDP Growth Outlook

3.3. Global Parent Market Overview

4. Price Trend Analysis, 2019 - 2031

4.1. Key Highlights

4.2. Key Factors Impacting Product Prices

4.3. Prices By Offering Type/Workshop Equipment/Handheld Scan Tools

4.4. Regional Prices and Product Preferences

5. Global Automotive Diagnostic Scan Tools Market Outlook: Historical (2019 - 2023) and Forecast (2024 - 2031)

5.1. Key Highlights

5.1.1. Market Size and Y-o-Y Growth

5.1.2. Absolute $ Opportunity

5.2. Market Size (US$ Bn) Analysis and Forecast

5.2.1. Historical Market Size Analysis, 2019-2023

5.2.2. Current Market Size Forecast, 2024-2031

5.3. Global Automotive Diagnostic Scan Tools Market Outlook: Offering Type

5.3.1. Introduction / Key Findings

5.3.2. Historical Market Size (US$ Bn) Analysis By Offering Type, 2019 - 2023

5.3.3. Current Market Size (US$ Bn) Forecast By Offering Type, 2024 - 2031

5.3.3.1. Diagnostic Equipment

5.3.3.2. Hardware Diagnostic Software

5.4. Market Attractiveness Analysis: Offering Type

5.5. Global Automotive Diagnostic Scan Tools Market Outlook: Workshop Equipment

5.5.1. Introduction / Key Findings

5.5.2. Historical Market Size (US$ Bn) Analysis By Workshop Equipment, 2019 - 2023

5.5.3. Current Market Size (US$ Bn) Forecast By Workshop Equipment, 2024 - 2031

5.5.3.1. Wheel Alignment Equipment

5.5.3.2. Exhaust Gas Analyzer

5.5.3.3. Paint Scan Equipment

5.5.3.4. Dynamometer Headlight Tester

5.5.3.5. Fuel Injection Diagnostic

5.5.3.6. Pressure Leak Detection

5.5.3.7. Engine Analyzer

5.6. Market Attractiveness Analysis: Workshop Equipment

5.7. Global Automotive Diagnostic Scan Tools Market Outlook: Handheld Scan Tools

5.7.1. Introduction / Key Findings

5.7.2. Historical Market Size (US$ Bn) Analysis By Handheld Scan Tools, 2019 - 2023

5.7.3. Current Market Size (US$ Bn) Forecast By Handheld Scan Tools, 2024 - 2031

5.7.3.1. Scanners

5.7.3.2. Code Readers

5.7.3.3. TPMS Tool

5.7.3.4. Digital Pressure Tester

5.8. Market Attractiveness Analysis: Handheld Scan Tools

5.9. Global Automotive Diagnostic Scan Tools Market Outlook: Vehicle Type

5.9.1. Introduction / Key Findings

5.9.2. Historical Market Size (US$ Bn) Analysis By Vehicle Type, 2019 - 2023

5.9.3. Current Market Size (US$ Bn) Forecast By Vehicle Type, 2024 - 2031

5.9.3.1. Passenger Cars

5.9.3.2. Commercial Vehicles

5.10. Market Attractiveness Analysis: Vehicle Type

6. Global Automotive Diagnostic Scan Tools Market Outlook: Region

6.1. Key Highlights

6.2. Historical Market Size (US$ Bn) Analysis By Region, 2019 - 2023

6.3. Current Market Size (US$ Bn) Forecast By Region, 2024 - 2031

6.3.1. North America

6.3.2. Europe

6.3.3. East Asia

6.3.4. South Asia and Oceania

6.3.5. Latin America

6.3.6. Middle East & Africa

6.4. Market Attractiveness Analysis: Region

7. North America Automotive Diagnostic Scan Tools Market Outlook: Historical (2019 - 2023) and Forecast (2024 - 2031)

7.1. Key Highlights

7.2. Pricing Analysis

7.3. Historical Market Size (US$ Bn) Analysis By Market, 2019 - 2023

7.3.1. By Country

7.3.2. By Offering Type

7.3.3. By Workshop Equipment

7.3.4. By Handheld Scan Tools

7.3.5. By Vehicle Type

7.4. Current Market Size (US$ Bn) Forecast By Country, 2024 - 2031

7.4.1. U.S.

7.4.2. Canada

7.5. Current Market Size (US$ Bn) Forecast By Offering Type, 2024 - 2031

7.5.1. Diagnostic Equipment

7.5.2. Hardware Diagnostic Software

7.6. Current Market Size (US$ Bn) Forecast By Workshop Equipment, 2024 - 2031

7.6.1. Wheel alignment equipment

7.6.2. Exhaust gas analyzer

7.6.3. Paint scan equipment Dynamometer Headlight Tester

7.6.4. Fuel Injection Diagnostic

7.6.5. Pressure Leak Detection

7.6.6. Engine Analyzer

7.7. Current Market Size (US$ Bn) Forecast By Handheld Scan Tools, 2024 - 2031

7.7.1. Scanners

7.7.2. Code readers

7.7.3. TPMS Tool

7.7.4. Digital Pressure Tester

7.8. Current Market Size (US$ Bn) Forecast By Vehicle Type, 2024 - 2031

7.8.1. Passenger Cars

7.8.2. Commercial Vehicles

7.9. Market Attractiveness Analysis

8. Europe Automotive Diagnostic Scan Tools Market Outlook: Historical (2019 - 2023) and Forecast (2024 - 2031)

8.1. Key Highlights

8.2. Pricing Analysis

8.3. Historical Market Size (US$ Bn) Analysis By Market, 2019 - 2023

8.3.1. By Country

8.3.2. By Offering Type

8.3.3. By Workshop Equipment

8.3.4. By Handheld Scan Tools

8.3.5. By Vehicle Type

8.4. Current Market Size (US$ Bn) Forecast By Country, 2024 - 2031

8.4.1. Germany

8.4.2. France

8.4.3. U.K.

8.4.4. Italy

8.4.5. Spain

8.4.6. Russia

8.4.7. Rest of Europe

8.5. Current Market Size (US$ Bn) Forecast By Workshop Equipment, 2024 - 2031

8.5.1. Diagnostic Equipment

8.5.2. Hardware Diagnostic Software

8.6. Current Market Size (US$ Bn) Forecast By Workshop Equipment, 2024 - 2031

8.6.1. Wheel alignment equipment

8.6.2. Exhaust gas analyzer

8.6.3. Paint scan equipment Dynamometer Headlight Tester

8.6.4. Fuel Injection Diagnostic

8.6.5. Pressure Leak Detection

8.6.6. Engine Analyzer

8.7. Current Market Size (US$ Bn) Forecast By Handheld Scan Tools, 2024 - 2031

8.7.1. Scanners

8.7.2. Code readers

8.7.3. TPMS Tool

8.7.4. Digital Pressure Tester

8.8. Current Market Size (US$ Bn) Forecast By Vehicle Type, 2024 - 2031

8.8.1. Passenger Cars

8.8.2. Commercial Vehicles

8.9. Market Attractiveness Analysis

9. East Asia Automotive Diagnostic Scan Tools Market Outlook: Historical (2019 - 2023) and Forecast (2024 - 2031)

9.1. Key Highlights

9.2. Pricing Analysis

9.3. Historical Market Size (US$ Bn) Analysis By Market, 2019 - 2023

9.3.1. By Country

9.3.2. By Offering Type

9.3.3. By Workshop Equipment

9.3.4. By Handheld Scan Tools

9.3.5. By Vehicle Type

9.4. Current Market Size (US$ Bn) Forecast By Country, 2024 - 2031

9.4.1. China

9.4.2. Japan

9.4.3. South Korea

9.5. Current Market Size (US$ Bn) Forecast By Offering Type, 2024 - 2031

9.5.1. Diagnostic Equipment

9.5.2. Hardware Diagnostic Software

9.6. Current Market Size (US$ Bn) Forecast By Workshop Equipment, 2024 - 2031

9.6.1. Wheel alignment equipment

9.6.2. Exhaust gas analyzer

9.6.3. Paint scan equipment Dynamometer Headlight Tester

9.6.4. Fuel Injection Diagnostic

9.6.5. Pressure Leak Detection

9.6.6. Engine Analyzer

9.7. Current Market Size (US$ Bn) Forecast By Handheld Scan Tools, 2024 - 2031

9.7.1. Scanners

9.7.2. Code readers

9.7.3. TPMS Tool

9.7.4. Digital Pressure Tester

9.8. Current Market Size (US$ Bn) Forecast By Vehicle Type, 2024 - 2031

9.8.1. Passenger Cars

9.8.2. Commercial Vehicles

9.9. Market Attractiveness Analysis

10. South Asia & Oceania Automotive Diagnostic Scan Tools Market Outlook: Historical (2019 - 2023) and Forecast (2024 - 2031)

10.1. Key Highlights

10.2. Pricing Analysis

10.3. Historical Market Size (US$ Bn) Analysis By Market, 2019 - 2023

10.3.1. By Country

10.3.2. By Offering Type

10.3.3. By Workshop Equipment

10.3.4. By Handheld Scan Tools

10.3.5. By Vehicle Type

10.4. Current Market Size (US$ Bn) Forecast By Country, 2024 - 2031

10.4.1. India

10.4.2. Southeast Asia

10.4.3. ANZ

10.4.4. Rest of South Asia & Oceania

10.5. Current Market Size (US$ Bn) Forecast By Offering Type, 2024 - 2031

10.5.1. Diagnostic Equipment

10.5.2. Hardware Diagnostic Software

10.6. Current Market Size (US$ Bn) Forecast By Workshop Equipment, 2024 - 2031

10.6.1. Wheel alignment equipment

10.6.2. Exhaust gas analyzer

10.6.3. Paint scan equipment Dynamometer Headlight Tester

10.6.4. Fuel Injection Diagnostic

10.6.5. Pressure Leak Detection

10.6.6. Engine Analyzer

10.7. Current Market Size (US$ Bn) Forecast By Handheld Scan Tools, 2024 - 2031

10.7.1. Scanners

10.7.2. Code readers

10.7.3. TPMS Tool

10.7.4. Digital Pressure Tester

10.8. Current Market Size (US$ Bn) Forecast By Vehicle Type, 2024 - 2031

10.8.1. Passenger Cars

10.8.2. Commercial Vehicles

10.9. Market Attractiveness Analysis

11. Latin America Automotive Diagnostic Scan Tools Market Outlook: Historical (2019 - 2023) and Forecast (2024 - 2031)

11.1. Key Highlights

11.2. Pricing Analysis

11.3. Historical Market Size (US$ Bn) Analysis By Market, 2019 - 2023

11.3.1. By Country

11.3.2. By Offering Type

11.3.3. By Workshop Equipment

11.3.4. By Handheld Scan Tools

11.3.5. By Vehicle Type

11.4. Current Market Size (US$ Bn) Forecast By Country, 2024 - 2031

11.4.1. Brazil

11.4.2. Mexico

11.4.3. Rest of Latin America

11.5. Current Market Size (US$ Bn) Forecast By Offering Type, 2024 - 2031

11.5.1. Diagnostic Equipment

11.5.2. Hardware Diagnostic Software

11.6. Current Market Size (US$ Bn) Forecast By Workshop Equipment, 2024 - 2031

11.6.1. Wheel alignment equipment

11.6.2. Exhaust gas analyzer

11.6.3. Paint scan equipment Dynamometer Headlight Tester

11.6.4. Fuel Injection Diagnostic

11.6.5. Pressure Leak Detection

11.6.6. Engine Analyzer

11.7. Current Market Size (US$ Bn) Forecast By Handheld Scan Tools, 2024 - 2031

11.7.1. Scanners

11.7.2. Code readers

11.7.3. TPMS Tool

11.7.4. Digital Pressure Tester

11.8. Current Market Size (US$ Bn) Forecast By Vehicle Type, 2024 - 2031

11.8.1. Passenger Cars

11.8.2. Commercial Vehicles

11.9. Market Attractiveness Analysis

12. Middle East & Africa Automotive Diagnostic Scan Tools Market Outlook: Historical (2019 - 2023) and Forecast (2024 - 2031)

12.1. Key Highlights

12.2. Pricing Analysis

12.3. Historical Market Size (US$ Bn) Analysis By Market, 2019 - 2023

12.3.1. By Country

12.3.2. By Offering Type

12.3.3. By Workshop Equipment

12.3.4. By Handheld Scan Tools

12.3.5. By Vehicle Type

12.4. Current Market Size (US$ Bn) Forecast By Country, 2024 - 2031

12.4.1. GCC

12.4.2. Egypt

12.4.3. South Africa

12.4.4. Northern Africa

12.4.5. Rest of Middle East & Africa

12.5. Current Market Size (US$ Bn) Forecast By Offering Type, 2024 - 2031

12.5.1. Diagnostic Equipment

12.5.2. Hardware Diagnostic Software

12.6. Current Market Size (US$ Bn) Forecast By Workshop Equipment, 2024 - 2031

12.6.1. Wheel alignment equipment

12.6.2. Exhaust gas analyzer

12.6.3. Paint scan equipment Dynamometer Headlight Tester

12.6.4. Fuel Injection Diagnostic

12.6.5. Pressure Leak Detection

12.6.6. Engine Analyzer

12.7. Current Market Size (US$ Bn) Forecast By Handheld Scan Tools, 2024 - 2031

12.7.1. Scanners

12.7.2. Code readers

12.7.3. TPMS Tool

12.7.4. Digital Pressure Tester

12.8. Current Market Size (US$ Bn) Forecast By Vehicle Type, 2024 - 2031

12.8.1. Passenger Cars

12.8.2. Commercial Vehicles

12.9. Market Attractiveness Analysis

13. Competition Landscape

13.1. Market Share Analysis, 2023

13.2. Market Structure

13.2.1. Competition Intensity Mapping By Market

13.2.2. Competition Dashboard

13.2.3. Apparent Production Capacity

13.3. Company Profiles (Details - Overview, Financials, Strategy, Recent Developments)

13.3.1. ACTIA Group

13.3.1.1. Overview

13.3.1.2. Segments and Products

13.3.1.3. Key Financials

13.3.1.4. Market Developments

13.3.1.5. Market Strategy

13.3.2. Snap-on Incorporated

13.3.3. Softing AG

13.3.4. Robert Bosch GmbH

13.3.5. Delphi Technologies

13.3.6. Denso Corporation

13.3.7. SPX Corporation

13.3.8. Continental AG

13.3.9. SGS SA

13.3.10. Horiba, Ltd.

Note: List of companies is not exhaustive in nature. It is subject to further augmentation during course of research

14. Appendix

14.1. Research Methodology

14.2. Research Assumptions

14.3. Acronyms and Abbreviations

- Automotive Components & Materials

- Automotive Diagnostic Scan Tools Market

Automotive Diagnostic Scan Tools Market Size, Share, and Growth Forecast for 2024 - 2031

Automotive Diagnostic Scan Tools Market by Offering Type (Diagnostic Equipment, Hardware Diagnostic Software), Workshop Equipment (Wheel Alignment Equipment, Exhaust Gas Analyzer, Paint Scan Equipment, Dynamometer Headlight Tester, Fuel Injection Diagnostic, Pressure Leak Detection, Engine Analyzer), Handheld Scan Tools (Scanners, Code Readers, TPMS Tool, Digital Pressure Tester), Vehicle Type (Passenger Cars, Commercial Vehicles), and Regional Analysis from 2024 to 2031

Automotive Diagnostic Scan Tools Market Size and Share Analysis

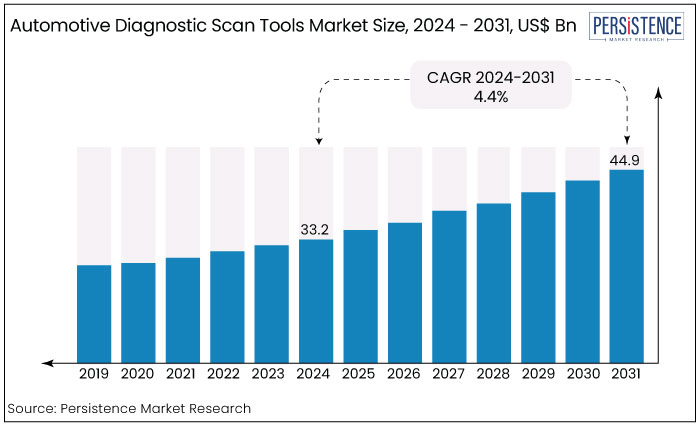

The global automotive diagnostic scan tools market is projected to witness a CAGR of 4.4% during the forecast period from 2024 to 2031. It is anticipated to increase from US$ 33.2 Bn recorded in 2024 to a staggering US$ 44.9 Bn by 2031. The market is set to rise through 2031 due to increasing vehicle complexity.

The market is also likely to be driven by a growing shift toward unique diagnostic systems equipped with artificial intelligence and machine learning. These are projected to help enhance fault detection and predictive maintenance capabilities.

The increasing focus on vehicle safety and compliance with regulations are also anticipated to fuel demand for sophisticated diagnostic tools. For instance, the Corporate Average Fuel Economy (CAFE) Standards regulate the average fuel economy of a manufacturer's fleet of passenger cars and light trucks. The goal is to improve fuel efficiency and reduce greenhouse gas emissions. The fleet average is set to reach 49 miles per gallon (mpg) by 2026.

Key Highlights of the Market

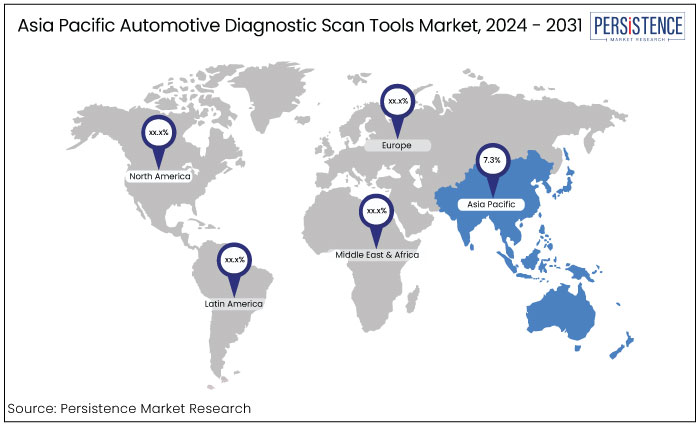

- Asia Pacific is projected to rise at a CAGR of 7.3% from 2024 to 2031 amid increasing demand for innovative diagnostic tools from India and China.

- Europe’s commercial vehicle scanner industry is expected to hold 30.2% of share in 2024 due to rapid shift toward AI and machine learning for enhanced fault detection and predictive maintenance.

- Based on vehicle type, the passenger cars segment leads the market accounting for about 70% of share in 2024 owing to the rise of electric and hybrid vehicles worldwide.

- In terms of offering type, the diagnostic equipment segment holds the largest share at 60.1% due to mandatory OBD-II port implementation in Europe and North America.

- Increasing complexity of automotive systems is anticipated to push demand for advanced diagnostic equipment.

- Key players are set to launch innovative scan tools capable of detecting issues in vehicles in real time.

|

Market Attributes |

Key Insights |

|

Automotive Diagnostic Scan Tools Market Size (2024E) |

US$ 33.2 Bn |

|

Projected Market Value (2031F) |

US$ 44.9 Bn |

|

Global Market Growth Rate (CAGR 2024 to 2031) |

4.4% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

3.9% |

Asia Pacific Automotive Diagnostic Scan Tools Market Leads Amid Government Investments

|

Region |

CAGR through 2031 |

|

Asia Pacific |

7.3% |

Asia Pacific is set to lead the automotive diagnostic scan tools industry and rise at a CAGR of 7.3% from 2024 to 2031. The region's growth is primarily driven by rapid innovations in technologies and rising demand for passenger cars.

Government investments aimed at developing diagnostic tools are also expected to create new growth opportunities. A booming automotive industry and enhanced manufacturing capabilities are also contributing to this growth. This combination positions the region as a key player in the automotive diagnostics industry. Apart from government bodies, several private companies are investing in enhancing and advancing these tools. For example,

- In August 2024, DC Connected Car GmbH, a Germany-based company, raised around US$ 2.29 Mn for its AI-driven remote vehicle diagnostics offering. The seed funding round will likely help develop AI diagnostic tools for roadside assistance, warranty, and repair.

Europe Automotive Diagnostic Scan Tools Market to Bolster with Strict Safety Norms

|

Region |

Market Share in 2024 |

|

Europe |

30.2% |

The automotive diagnostic scan tools market share in Europe is expected to remain at 30.2% In 2024. This is attributed to a booming automotive industry and a keen focus on technological innovations. The demand for cutting-edge diagnostic tools is also being driven by strict regulations associated with vehicle emissions and safety standards.

Several companies in Europe are actively rolling out innovative solutions, positioning the region as a significant hub in terms of market growth.

- A notable example is Anyline, based in Austria, which introduced the Tire Sidewall Scanner in 2023. This tool captures detailed tire sidewall information in a single photo. It enhances tire inventory management for hotels and streamlines workflows by digitizing traditional tire data.

Passenger Carmakers Seek Unique Tools to Repair Complex Systems

|

Category |

Market Share in 2024 |

|

Vehicle Type- Passenger Cars |

70% |

Based on vehicle type, the passenger car segment is currently leading the market. The segment benefits from the increasing complexity of automotive systems and the growing number of passenger cars on the road. It is projected to hold about 70% of the total automotive diagnostic tools industry share.

In 2023, the U.S. produced approximately 1.75 million passenger cars. The number is anticipated to rise in various parts of the globe, apart from the U.S. Keeping this sales figure in mind, various companies are developing automotive diagnostic tools mainly for passenger cars. For instance,

- Companies like Snap-on Incorporated are well known for their high-quality diagnostic tools and equipment. They cater to both professional mechanics and automotive technicians. Their products are widely used in the automotive repair industry, particularly for passenger vehicles, which has contributed to their strong market position and profitability.

Effective Fault Evaluation Requirements Spur Demand for Diagnostic Equipment

|

Category |

Market Share in 2024 |

|

Offering Type - Diagnostic Equipment |

60.1% |

In terms of offering type, the diagnostic equipment segment is currently leading the automotive scanner programmer industry. It holds a key share, primarily due to the mandatory implementation of diagnostic hardware, such as OBD-II ports, in all vehicles across regions like Europe and North America. In 2024, the segment accounted for approximately 60.1% of the total market share.

Increasing complexity of automotive systems and growing need for effective fault identification tools further drive demand for advanced diagnostic equipment. Various companies are set to focus on developing effective OBD-based solutions for vehicles. For instance,

- In 2023, Reliance Jio, headquartered in India, introduced the JioMotive, an OBD-based telematics solution for cars. The plug-and-play device offers real-time tracking, geofencing, tow alerts, and Time Fence. It also analyzes driving performance and allows users to monitor vehicle parameters like battery health, engine load, coolant temperature, and air intake temperature.

Market Introduction and Trend Analysis

The automotive diagnostic scan tools market is experiencing significant growth driven by technological advancements and increasing vehicle complexity. A prominent trend is the shift toward advanced diagnostic systems that utilize artificial intelligence and machine learning. These also help enhance fault detection and predictive maintenance capabilities.

The rise of electric and hybrid vehicles is further prompting the development of specialized diagnostics tailored to these technologies. The integration of cloud-based solutions allows for real-time data analysis and remote diagnostics, improving efficiency across repair shops and service centers. Additionally, the number of vehicle accidents is increasing. For instance, in the U.S., in 2022, about 42,514 fatal car accidents were reported.

The growing emphasis on vehicle safety and compliance with stringent regulations continues to fuel demand for sophisticated diagnostic tools. These are likely to ensure that automotive professionals can effectively maintain and repair modern vehicles. As a result, the market is poised for continued expansion and innovation.

Historical Growth and Course Ahead

The automotive diagnostic scan tools market witnessed steady growth at a CAGR of 3.9% from 2019 to 2023. This growth was fueled by the increasing complexity of vehicle systems, rising demand for novel electronic components, and surging need for advanced diagnostic solutions. As vehicles become technologically advanced, the demand for efficient and accurate diagnostic tools rose, thereby pushing the market forward.

The global market is projected to rise with a CAGR of 4.4% from 2024 to 2031. This upward trend is set to be driven by the proliferation of electric and hybrid vehicles. These vehicles require specialized diagnostic tools and the integration of advanced technologies like AI and cloud computing. Several companies are introducing innovative solutions for effective diagnosis of vehicles to compete with their rivals. For instance,

- In October 2024, XtoolOnline, a California-based firm, launched the XTOOL D5/D5S. It is an affordable and reliable diagnostic tool designed for automotive technicians and DIY enthusiasts. It offers basic diagnostics for four systems and complete OBD2 functionality, with 9 special functions.

The ongoing emphasis on vehicle safety and compliance with stringent regulations will likely continue to bolster demand for high-quality diagnostic tools. As automotive technology evolves, the diagnostic tools market is poised for significant innovations, offering new opportunities in the coming years.

Market Growth Drivers

Car Reprogramming Tool Demand to Rise with High Sales of Passenger Vehicles

The automotive diagnostic scan tools market is set to surge amid rising sales of passenger cars, which are witnessing a significant increase in key countries like China, the United States., and the United Kingdom. High demand for low-emission vehicles and rising government support for vehicle inspections are prompting manufacturers to broaden their offerings of diagnostic tools globally. Government bodies in various countries are hence launching several initiatives in this field. For instance,

- Clean Vehicle Assistance Program, funded by California Climate Investments, aims to reduce greenhouse gas emissions and improve public health. While primarily focused on clean vehicle access, it also supports initiatives that can enhance vehicle safety and inspections, particularly in disadvantaged communities.

Passenger cars represent the fastest-growing segment in the automotive industry. Sales of these cars are increasing rapidly. In 2023, the U.S. auto industry sold around 15.5 million light vehicle units. It includes about 3.12 million passenger cars and just under 12.4 million light trucks. This proves that many people are shifting toward passenger car services. Additionally, rapid urbanization in emerging economies is fueling the need for personal vehicles, further boosting the market.

Mandates Revolving around OBD-II Installation to Fuel Sales

Stringent government regulations in the United States and Europe now mandate all vehicles to be equipped with On-Board Diagnostics II (OBD-II). This system enables GPS fleet tracking devices to gather important data, including fuel consumption, engine revolutions, fault codes, and vehicle speed. Telemetry devices further analyze this information to assess fuel efficiency, trip duration, and instances of speeding, among other metrics.

Fleet operators can then use software interfaces to monitor their vehicles' performance and usage effectively. As a result, the growing adoption of on-board diagnostics in commercial fleets is expected to significantly contribute to the automotive diagnostic scan tools market growth. Government bodies in the U.S. and Europe have further initiated several programs. For example,

- In the U.S., the Environmental Protection Agency (EPA) has established rules that require OBD-II systems to fully evaluate the entire emission control system of vehicles. This ensures that vehicles meet stringent emissions standards throughout their operational life.

Market Restraining Factors

High Initial Cost of Advanced Tools to Hamper Market Expansion

The steep initial costs of advanced diagnostic equipment pose challenges for market growth, particularly for small-scale businesses trying to enter the industry. Economic downturns further exacerbate these obstacles, hindering progress. However, these challenges are motivating companies to create more affordable solutions, fostering resilience and adaptability in the market. As businesses respond to economic fluctuations and financial constraints, they are finding innovative ways to navigate these difficulties, ultimately supporting the market's evolution and growth.

Rising Demand for Skilled Technicians and Complex Functioning to Decline Sales

The complex functioning of digital car circuit scanner diagnostic tools requires the expertise of highly skilled technicians. This can be a main barrier to their widespread adoption among consumers.

Several vehicle owners may find it challenging to understand the detailed information provided by these tools or lack the technical knowledge to interpret faulty codes and diagnostic data effectively. This complexity can lead to reliance on professional services, which may deter a few consumers from utilizing these advanced tools. As a result, fostering greater accessibility and training for technicians is essential to encourage consumer confidence and promote high use of diagnostic scan tools in the automotive market. For example,

- In July 2023, Innova Electronics, a California-based company, introduced its Smart Diagnostic System tablets and RepairSolutions PRO app. These tools were mainly designed for professional automotive repair use. These are easy to use, optimize diagnostic processes, save time of technicians, and enhance customer communication, backed by ASE-certified technicians.

Key Market Opportunities

Companies like Repairify Focus on Remote Diagnostics to Mark Their Presence

Remote diagnostics is a key trend rapidly propelling the professional automotive scan tools industry. With rapid technological advancements, it is now possible to monitor and analyze vehicle systems in real time. It further allows for efficient detection and resolution of issues from a distance. This approach not only speeds up troubleshooting but also helps minimize downtime and lower maintenance costs.

Remote diagnostics are further paving the way for digital solutions that enable effective and timely vehicle diagnostics. This makes it easier for both consumers and technicians to maintain and repair vehicles. For instance,

- In June 2023, U.S.-based Repairify declared its upcoming asTech All-In-One solution for local and remote automotive diagnostics, calibrations, and programming. It allows users to scan 45+ vehicle brands as well as identify calibrations and electronic repair events. It also enables remote and local calibrations, connects to remote Master Techs and Certified Technicians, and provides access to verified pre- and post-scan reports.

Increasing Use of Smartphones in Automotive Diagnostics to Create Opportunities

Increasing smartphone use has offered comfort and accessibility to several users. In the U.S., in 2023, about 81.6% of individuals, or approximately 270 million people, likely owned a smartphone. The number of people using mobile devices is anticipated to rise in future.

As automotive diagnostic devices and scanners are mobile compatible, these can be used to perform tests, scan vehicles, and receive reports directly on mobile devices. This convenience means that technicians and vehicle owners can access crucial information on the go, making the diagnostic process more efficient and user-friendly. With everything at their fingertips, users can quickly troubleshoot issues and stay informed about their vehicle’s performance, enhancing the experience of using diagnostic tools.

Competitive Landscape for the Automotive Diagnostic Scan Tools Market

The automotive diagnostic scan tools industry is highly competitive, with several players striving to innovate and capture high shares. Companies are focusing on developing advanced features like remote diagnostics and mobile compatibility to enhance user experience.

U.S.-based Snap-on Incorporated, for instance, has been launching several innovative products since 2022, including the Solus Edge. It is a powerful diagnostic tool that combines unique vehicle coverage with enhanced data management capabilities. The device allows technicians to perform comprehensive diagnostics quickly and efficiently. It also positions Snap-on as a leader in the market and sets a high standard for technological innovations in automotive diagnostics.

Recent Industry Developments

- In October 2024, Launch Tech Co., a China-based company, introduced the Launch CRP123E OBD2 Scanner. It is a reliable and user-friendly diagnostic tool. It offers lifetime free updates, advanced diagnostic capabilities, and a user-friendly interface. The scanner also helps diagnose issues with the Evaporative Emission Control (EVAP) system, saving trips to the auto shop.

- In August 2024, Bosch Diagnostics, a Germany-based company, released a new 6.0 software update for its ADS X series scan tool. It aims to improve diagnostic scan efficiency and vehicle coverage. The update includes a topology view and battery voltage indicator, which improve scan times by an average of 57% among popular brands in Asia and Europe.

- In April 2024, Germany-based MAHLE Aftermarket announced that it will launch the second generation of its workshop diagnostic tools, MAHLE TechPRO® and BRAIN BEE Connex. The new tools were redesigned to improve usability and efficiency, allowing workshop teams to easily access and use the tools.

Companies Covered in Automotive Diagnostic Scan Tools Market

- ACTIA Group

- Snap-on Incorporated

- Softing AG

- Robert Bosch GmbH

- Delphi Technologies

- Denso Corporation

- SPX Corporation

- Continental AG

- SGS SA

- Horiba, Ltd.

Frequently Asked Questions

The market is set to reach US$ 44.9 Bn by 2031.

It refers to an electronic device that helps evaluate problems in a vehicle by connecting to its computer system.

The BlueDriver Bluetooth Pro is considered the best scan tool, as of 2024.

ACTIA Group, Snap-on Incorporated, and Softing AG are some of the best scan tool manufacturers.

OBD-II generic, OBD-II enhanced, and factory scan tools are the three key types.