- Automotive Components & Materials

- Automotive Camera Market

Automotive Camera Market Size, Share, and Growth Forecast, 2026 - 2033

Automotive Camera Market by Vehicle Type (Passenger Cars, Others), Technology (Digital/CMOS, Others), Hardware Type (Monocular, Stereo, Triple/Multi-lens), Application (ADAS, Parking/Surround View, Others), and Regional Analysis 2026 - 2033

Automotive Camera Market Size and Trends Analysis

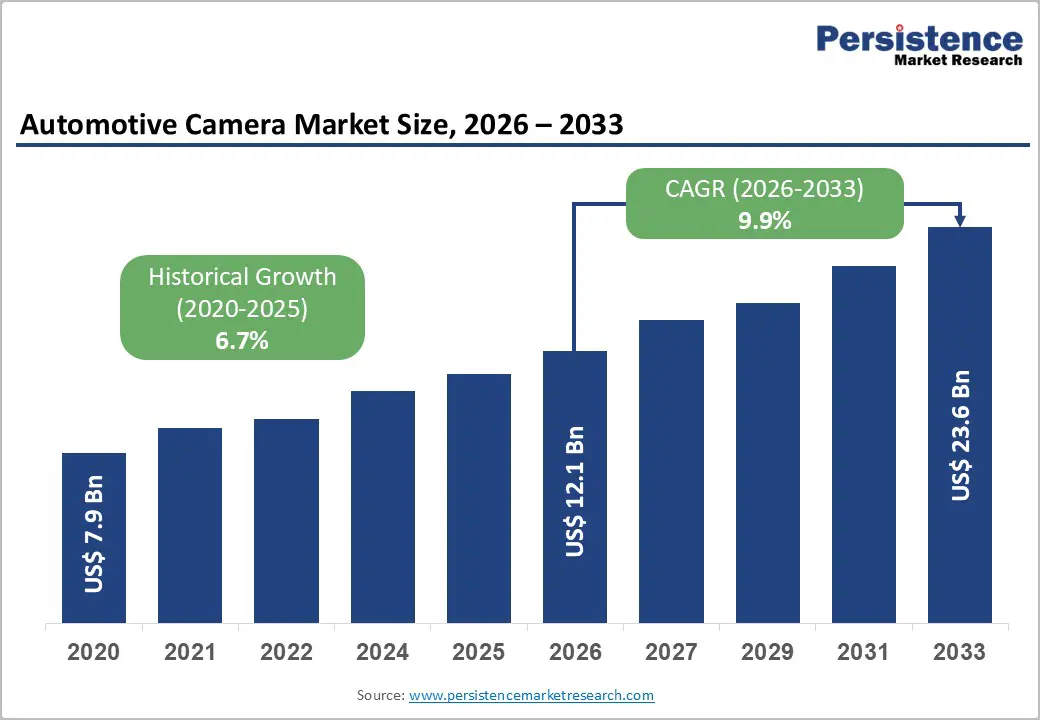

The global automotive camera market size is likely to be valued at US$12.1 billion in 2026 and is expected to reach US$23.6 billion by 2033, growing at a CAGR of 9.9% during the forecast period from 2026 to 2033, driven by the increasing global adoption of Advanced Driver Assistance Systems (ADAS) mandated by safety regulations, as well as the expansion of electric vehicles.

The integration of consumer electronics technology with automotive-grade hardware, particularly high-resolution CMOS (Complementary Metal-Oxide-Semiconductor) sensors, enables superior object detection, even in low-light environments, which is critical for achieving the stringent NCAP (New Car Assessment Programs) safety ratings.

Key Industry Highlights:

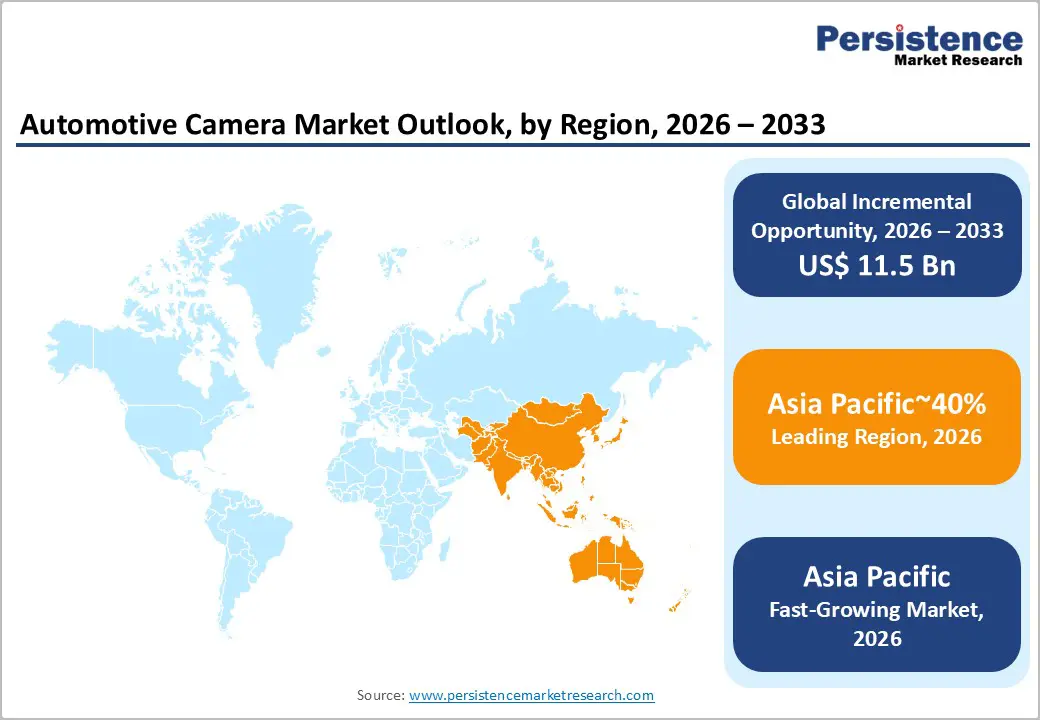

- Leading Region and the Fastest-growing Region: Asia Pacific, with around 40% share, supported by high vehicle production volumes in China and India, rapid adoption of ADAS technologies, and strong government safety regulations.

- Leading Technology: Digital/CMOS sensors are anticipated to remain the leading technology, holding around 72% share, as they offer high resolution, cost-efficiency, and integration compatibility for ADAS and parking camera systems.

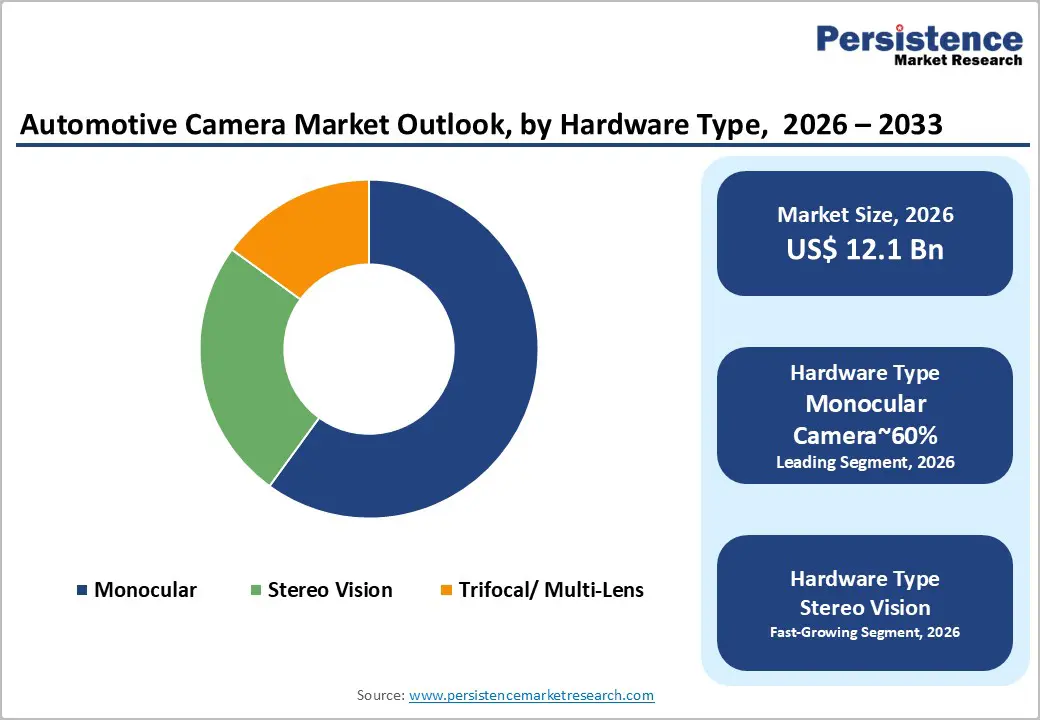

- Leading Hardware Type: Monocular camera systems are anticipated to remain the leading hardware type, holding around 60% share, as cost-effective, single-lens solutions dominate entry- and mid-level vehicles while providing sufficient functionality for basic.

| Key Insights | Details |

|---|---|

| Automotive Camera Market Size (2026E) | US$12.1 Bn |

| Market Value Forecast (2033F) | US$23.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis

Mandatory ADAS Regulatory Frameworks

Government regulations have evolved from voluntary guidelines to enforceable mandates, representing the most significant catalyst for growth in the ADAS camera market. Mandatory frameworks require specific safety technologies, such as forward-facing cameras for Automatic Emergency Braking (AEB) and driver-monitoring systems for drowsiness detection, as prerequisites for new vehicle compliance. This regulatory shift transforms ADAS features from optional enhancements into standard equipment, directly driving unit adoption across all passenger car segments.

The impact of these mandates is substantial: they effectively establish a guaranteed baseline demand for compliant camera systems, ensuring near-universal attachment rates in regulated regions. As a result, automotive manufacturers are compelled to integrate advanced imaging solutions into every new vehicle platform, supporting a predictable and sustained volume of sensor deployments. This creates a structural growth driver for ADAS camera suppliers, incentivizing investment in high-resolution imaging, compact sensor modules, and integration-ready software to meet evolving safety requirements while enabling compliance-driven market expansion.

Technological Advancements in Image Sensors

Rapid innovation in image sensor technology is a key driver of ADAS camera adoption, enhancing safety performance and enabling new functionalities. CMOS digital sensors currently dominate the market, but thermal long-wave infrared (LWIR) sensors are expanding rapidly due to their ability to detect objects in low-visibility conditions, such as fog, rain, or nighttime driving. Advances in AI-enabled image processing allow real-time object recognition and hazard detection, improving system reliability while reducing per-module costs.

These technological improvements also support broader ADAS integration in electric and high-end vehicles, where enhanced sensing capabilities are critical for autonomous features. By combining multi-spectral imaging with AI-driven analytics, manufacturers can achieve higher safety ratings and comply with stringent safety protocols more efficiently. In May 2024, Samsung showcased its 8.3MP ISOCELL Auto 1H1 sensor at Auto-Sens, Detroit, within the Automotive Technology sector. This imager offers a 120 dB dynamic range and LED Flicker Mitigation, improving visibility in challenging lighting conditions, which reduces board size and eliminates the need for external serializers, directly addressing cost and integration complexity.

Barrier Analysis

Semiconductor Supply Chain Volatility & Cost Complexity

The automotive camera market faces major challenges due to the fragility of the semiconductor supply chain. High-end cameras depend on specialized CMOS Image Sensors (CIS) and Image Signal Processors (ISPs), which are often produced alongside consumer electronics, exposing the sector to demand spikes across industries. Production concentration among a few suppliers creates vulnerability to disruptions from geopolitical tensions, natural disasters, or logistical failures. The automotive qualification process adds to this, as switching suppliers requires time-consuming and costly re-validation.

As camera resolutions rise (8MP+ ADAS systems), processing and system-level costs increase, particularly with high-speed data architectures such as Automotive Ethernet or GMSL2. Unpredictable ordering patterns and inventory fluctuations further destabilize pricing. In response, Sony's October 2025 introduction of the IMX828 sensor with a built-in MIPI A-PHY interface addresses cost and integration challenges by reducing board size and eliminating the need for external serializers.

Opportunity Analysis

Convergence of In-Cabin Monitoring and Health Technology

The integration of Driver Monitoring Systems (DMS) with broader health and safety technologies offers significant growth potential for the automotive camera market. Modern DMS can evolve into Occupant Monitoring Systems (OMS), capable of detecting child presence and monitoring passenger vitals using non-contact methods such as remote photoplethysmography (rPPG). This not only enhances safety, such as preventing heatstroke incidents, but also creates new opportunities for wellness applications, real-time health monitoring, and personalized infotainment.

By embedding AI-driven analytics, manufacturers can differentiate their vehicles, improve passenger experience, and open new revenue streams. In July 2025, Magna International secured five new OEM programs for Child Presence Detection (CPD), a critical safety application enabled by in-cabin cameras.

Thermal Cameras for Level 3+ Autonomy

Thermal imaging is a key growth driver for Level 3 and Level 4 autonomy, overcoming limitations of visible-light cameras and LiDAR in low-visibility conditions. Unlike CMOS sensors, which detect reflected light, Long-Wave Infrared (LWIR) sensing detects emitted heat, enabling reliable object detection in darkness, fog, glare, and backlighting. This capability is crucial for meeting safety requirements around pedestrian and vulnerable road user detection, vital for high automation where human fallback is minimized.

Thermal sensors also improve perception robustness in sensor-fusion systems, reducing risks in corner-case scenarios. With advances in wafer-level packaging and automotive-grade integration, thermal cameras are becoming commercially viable for premium vehicles and autonomous fleets. In January 2026, Bosch partnered with Kodiak AI to develop redundant hardware platforms for autonomous trucks, integrating thermal cameras alongside visible sensors and LiDAR, enhancing reliability and scalability in commercial transport.

Category–wise Analysis

Technology Insights

Digital (CMOS) technology is projected to dominate the automotive vision systems market, accounting for roughly 72% share, underpinned by its entrenched role in ADAS pipelines and centralized vehicle compute architectures across high-volume OEM programs. Adoption remains anchored by resolution scalability, low-latency transport, and software upgradability, with manufacturers prioritizing platform standardization and workflow integration in production vehicles. Ongoing platform evolution, such as GMSL3 and FPD-Link IV links, on-sensor processing, and high-dynamic-range imaging, continues to reinforce replacement cycles and utilization intensity. Vendors, including Sony Semiconductor, ON Semiconductor, and Samsung, are expanding portfolios with 8MP-class CMOS sensors and smart imaging stacks, while Tier-1s such as Bosch and Mobileye bundle perception software to lock in enterprise workflows and long-term programs.

Thermal imaging is anticipated to be the fastest-growing segment, driven by visibility gaps in low light, glare, and adverse weather across night-time AEB, wildlife detection, and 24/7 autonomy use cases. Momentum is being catalyzed by wafer-level packaging, higher-sensitivity cores, and hybrid ranging concepts that materially improve detection distance and reliability. Adoption is further supported by production-grade integration and automated calibration, reducing friction for first-time deployments. Companies including Teledyne FLIR, Adasky, and Lynred are scaling compact automotive cores and solid-state modules, with Magna integrating thermal-augmented stacks into series platforms.

Hardware Insights

Monocular camera systems are expected to dominate the automotive vision hardware market with around 60% share in 2026, underpinned by their entrenched role in high-volume ADAS deployments and cost-sensitive vehicle platforms. Adoption remains anchored by favorable unit economics, compact packaging behind the windshield, and AI-driven depth inference that extends capability without adding sensor complexity. Suppliers such as Mobileye, Continental, and Magna integrate monocular stacks into turnkey ADAS workflows, with Eye-Q-based perception pipelines and a wide range of camera modules locking in long-term production programs. This combination of mature infrastructure, scalable software pipelines, and predictable OEM demand sustains monocular leadership in standardized deployment models.

Stereo vision is likely to be the fastest-growing camera hardware segment, driven by depth-estimation limits of single-lens systems in hands-off driving, high-speed collision avoidance, and urban autonomy scenarios. Growth is catalyzed by dense disparity mapping, embedded accelerators within camera housings, and learning-based stereo matching that materially improves performance in rain, glare, and low contrast scenes. Companies including Continental, Hitachi Astemo, and Bosch are scaling production-grade stereo modules and hybrid multi-lens configurations for Level 3-ready platforms, while lens specialists such as Ricoh support long-term optical stability. This shift positions stereo as the preferred hardware layer for safety-critical depth perception in advanced automation.

Regional Insights

Asia Pacific Automotive Camera Market Trends

Asia Pacific is expected to remain the leading region in the automotive camera market, accounting for approximately 40% of the global market share in 2026, anchored by its position as the global production and deployment hub for camera-enabled vehicle architectures. China, Japan, and India are likely to sustain structural leadership as OEMs scale multi-camera configurations across mass-market platforms, with BYD standardizing multi-camera ADAS suites across entry-level and premium models. Local Tier 1 integration by Desay SV and Huawei is projected to deepen vertical control over camera modules and image signal processing, while Sony and Panasonic are expected to continue anchoring high-performance image sensor and optics supply. Urban driving complexity across major APAC cities is likely to keep surround-view, blind-spot, and front monocular camera penetration structurally high, reinforcing baseline demand across passenger and commercial fleets.

Asia Pacific is also projected to be the fastest-growing region, driven by rapid EV platform expansion and accelerated adoption of Level 2 and Level 2+ ADAS in affordable vehicle segments. Xiaomi EV’s Vision Fusion programs and Tata Motors’ camera-on-chip localization with Renesas are likely to compress system costs and broaden camera deployment beyond premium models. Interior sensing growth is expected to accelerate through dual-lens DMS and in-cabin cameras adopted by Nio and Xpeng, while AR-HUD integration in Japanese and Chinese vehicles is projected to expand front-camera utilization. Regulatory emphasis on AEB and driver monitoring is likely to structurally increase camera attachment rates, positioning APAC as the primary testbed for intelligent vehicle vision stacks.

North America Automotive Camera Market Trends

North America is set to remain a key, technology-driven automotive camera market, driven by a strong presence of OEMs, Tier 1 suppliers, and ADAS providers. The region will continue relying on integrated camera-compute stacks, with Mobileye’s EyeQ platforms forming the core vision layer for U.S. automakers and Magna leading in mirror-replacement and surround-view systems for Ford, GM, and Stellantis.

NVIDIA DRIVE’s centralized compute will enable the expansion of satellite camera designs, scaling systems, including Ford's BlueCruise. With suppliers such as OmniVision and Japanese imaging optics partners, North America will maintain access to high-res digital camera modules for safety-critical applications. Market growth will focus on ADAS and fleet solutions, with Mobileye, Garmin, and Magna expanding camera offerings across vehicles, fleets, and aftermarket platforms. Thermal and infrared cameras will grow in importance, particularly for night-time pedestrian detection, while collaborations with compute vendors such as NVIDIA will drive software-defined camera systems into mainstream production.

Europe Automotive Camera Market Trends

Europe is poised to remain the global leader in automotive camera regulation and technology, despite not being the largest or fastest-growing market by volume. The region is expected to continue setting the functional standards for safety-driven camera integration, particularly under GSR II, with Germany, France, and the U.K. influencing the adoption of technologies such as sign recognition, driver monitoring, and distraction detection. European OEMs, including BMW, Mercedes-Benz, Audi, Porsche, and Volvo, are expected to maintain high camera densities in their vehicles, while Tier 1 suppliers such as Bosch, Continental, Valeo, ZF, and Forvia will lead in integrating surround-view, stereo front cameras, and interior monitoring systems.

The market will continue to be bolstered by Euro NCAP protocols and Vision Zero programs, which push both premium and mass-market vehicles toward standardized multi-camera perception systems. Europe's strong supplier ecosystem and long-cycle OEM programs are likely to support industrial continuity, rather than rapid unit expansion. Bosch and Continental are set to enhance software-defined camera roadmaps for zonal architectures, while Valeo will scale near-field and rear-view cameras. ZF and Forvia are expected to expand camera systems in commercial vehicles, and specialists such as Lynred will remain key in thermal fusion for night-time AEB systems. This ecosystem ensures Europe’s ongoing role as the global benchmark for safety-critical automotive camera technologies.

Competitive Landscape

The global automotive camera market is moderately consolidated, with leading Tier 1 suppliers such as Continental, Bosch, Denso, Valeo, and Magna holding a strong influence through deep OEM relationships and large-scale module integration capabilities. These players matter because their long-term supply agreements, vehicle platform integration expertise, and compliance with automotive-grade quality standards position them as preferred partners for global automakers. Competitive power is concentrated at the system level, while Tier 2 module providers and regional suppliers remain more fragmented, sustaining competitive pressure in sub-assemblies and commoditized components.

Competitive positioning is defined by a clear split between component suppliers, such as Sony, onsemi, and OmniVision, which set sensor performance benchmarks, and system integrators such as Valeo, Bosch, Magna, and Continental, which package hardware with perception software into OEM-ready ADAS solutions. Industry behavior centers on software-defined sensing, tighter OEM co-development, and vertical collaboration across the stack, signaling rising competition as camera performance, perception accuracy, and system reliability become central to vehicle safety and autonomy roadmaps.

Key Industry Highlights:

- In January 2026, Mobileye acquired Mentee Robotics to advance physical AI for autonomous vehicles, enhancing camera-based perception. This bolsters scalable AV deployment, improving safety and efficiency in global fleets.

- In September 2025, Qualcomm and Valeo expanded their partnership to deliver pre-integrated ADAS/AD platforms using Snapdragon Ride solutions. This collaboration simplifies vehicle implementation, enhances safety-centric systems, and speeds up innovation for automakers worldwide.

- In April 2025, Valeo launched remanufactured LED headlamps and electronic parts with Stellantis. Supports circular economy goals while maintaining high-tech electronics in modern vehicles.

Companies Covered in Automotive Camera Market

- Continental AG

- Magna International

- Robert Bosch GmbH

- Valeo S.A.

- Denso Corporation

- Mobileye (Intel)

- ZF Friedrichshafen AG

- Aptiv PLC

- Sony Group

- onsemi

- OmniVision Technologies

- Gentex Corporation

- Hyundai Mobis

- Panasonic Holdings

- Samsung Electro-Mechanics

- Autoliv Inc.

Frequently Asked Questions

The global automotive camera market is projected to be valued at US$12.1 billion in 2026 and is expected to reach US$23.6 billion by 2033, driven by regulatory mandates for ADAS and the expansion of electric vehicles.

Governments worldwide are enforcing mandatory safety standards that require features such as Automatic Emergency Braking (AEB) and driver monitoring, transforming cameras from optional features into standard equipment and creating a guaranteed, high-volume demand across all new vehicle segments.

The automotive camera market is forecast to grow at a CAGR of 9.9% from 2026 to 2033, reflecting the rapid adoption of advanced vision systems for safety and autonomy.

Asia Pacific is the leading regional market, accounting for approximately 40% share, supported by high vehicle production volumes in China and India, rapid ADAS adoption, and strong government safety regulations.

The automotive camera market is moderately consolidated, with key Tier 1 system integrators including Continental AG, Robert Bosch GmbH, Valeo, and Magna International. Key sensor technology suppliers are Sony Semiconductor, onsemi, and OmniVision.