- Automotive Components & Materials

- Automotive Camera Cleaning System Market

Automotive Camera Cleaning System Market Size, Share, and Growth Forecast for 2025 - 2032

Automotive Camera Cleaning System Market by Vehicle Type (Passenger Vehicles, Commercial Vehicles), Nozzle (Fixed Type, Telescopic Type, and Nano Type), Application (Parking, Front Safety Monitoring, Interjection), Sales Channel, and Regional Analysis for 2025 - 2032

Automotive Camera Cleaning System Market Share and Trends Analysis

The global automotive camera cleaning system market size is anticipated to rise from US$ 1,382.4 Bn in 2025 to US$ 3,225.6 Bn by 2032. It is projected to grow at a CAGR of 15.2% from 2025 to 2032.

The automotive camera cleaning system market size has witnessed a significant growth due to the increasing adoption of advanced driver assistance systems (ADAS) and autonomous vehicles. These systems rely heavily on clear and unobstructed camera lenses for accurate operation, making camera cleaning systems crucial for vehicle safety and functionality.

With the proliferation of ADAS in vehicles, the demand for reliable automotive camera cleaning systems is expected to soar. These systems ensure that cameras maintain optimal visibility in various weather conditions, enhancing the effectiveness of safety features such as lane departure warning and adaptive cruise control.

The rise of electric vehicles presents new opportunities for the market. EV manufacturers are increasingly incorporating advanced ADAS features into their vehicles, necessitating efficient cleaning systems to maintain clear camera lenses.

Key Industry Highlights:

- Growing demand for camera-based safety features fuels the market growth.

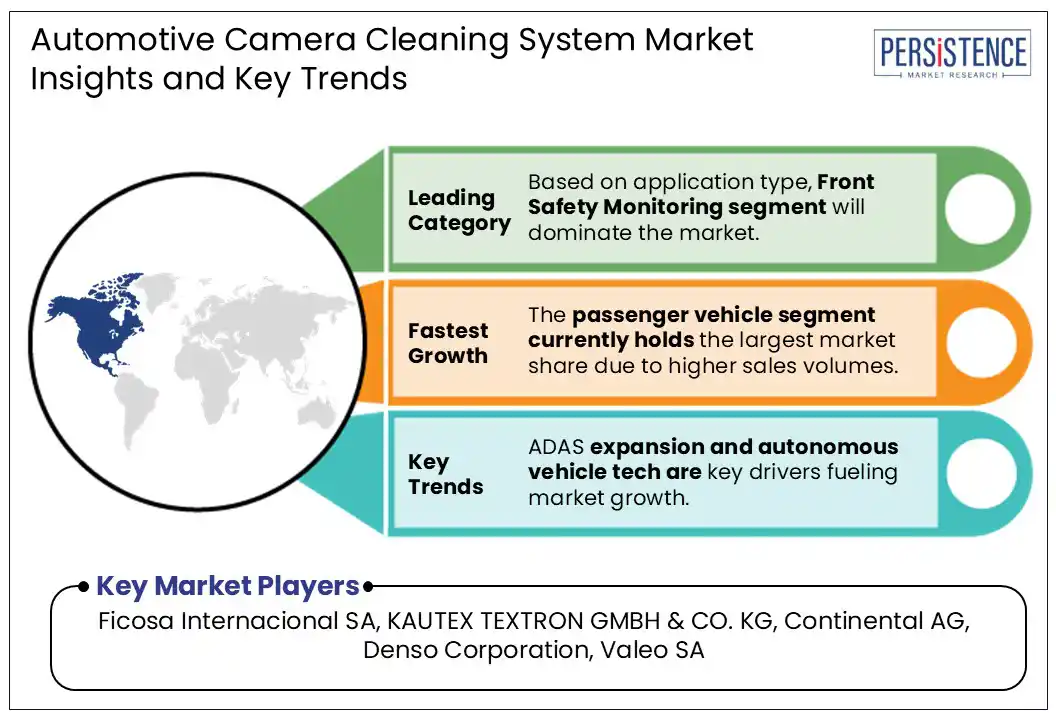

- The proliferation of ADAS and the development of autonomous vehicles are the primary drivers of market growth.

- Increasing consumer awareness about safety features is driving the adoption of automotive camera cleaning systems.

- The passenger vehicle segment currently holds the largest market share due to higher sales volumes.

- Asia Pacific is expected to lead the market due to rapid industrialization and increasing vehicle production.

- Based on vehicle type, passenger vehicle segment to grow substantially in the market.

- Based on application type, Front Safety Monitoring segment will dominate the market.

|

Global Market Attribute |

Key Insights |

|

Automotive Camera Cleaning System Market Size (2025E) |

US$ 1,382.4 Bn |

|

Market Value Forecast (2032F) |

US$ 3,225.6 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

15.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

11.5% |

Market Dynamics

Driver - Evolution of autonomous driving technologies fuels industry growth

The evolution of autonomous driving technologies represents another pivotal driver for the automotive camera cleaning system market. Autonomous vehicles rely heavily on a suite of sensors and cameras to perceive their environment and make real-time decisions. These cameras must maintain better visibility to ensure accurate data capture and processing, which is critical for achieving higher levels of autonomy.

As AV technologies advance from driver assistance features to fully autonomous capabilities, the complexity and sophistication of camera systems increase exponentially. AVs require not only enhanced camera resolution and coverage but also seamless operation of cleaning systems to prevent any disruption in sensor performance. This drives the development of cutting-edge camera cleaning solutions capable of meeting stringent reliability and performance standards demanded by AV manufacturers and regulatory bodies.

Advancements in vehicle electrification and the evolution of autonomous driving technologies are pivotal drivers propelling the automotive camera cleaning system market forward. Manufacturers and stakeholders in this market are poised to capitalize on these drivers by innovating and delivering advanced cleaning solutions.

Restraint - Limited awareness and education, challenges growth

Many consumers are unaware of the benefits that automotive camera cleaning systems provide. Clear camera lenses are essential for the reliable operation of ADAS features such as lane departure warning, adaptive cruise control, and collision avoidance systems. Without proper education, consumers may not fully acknowledge the functioning of camera cleaning systems and how they contribute to overall vehicle safety and performance.

There is a perception among several consumers that vehicles equipped with advanced safety features, including camera cleaning systems, come at a higher cost. Limited awareness about the potential long-term benefits and safety advantages of these systems may deter consumers from choosing vehicles with such features, especially if they perceive them as unnecessary expenses.

Consumers may also have concerns about the reliability and effectiveness of camera cleaning systems, particularly in challenging weather conditions or over extended periods of use. Without adequate education about the capabilities and maintenance requirements of these systems, potential buyers may hesitate to invest in vehicles equipped with them.

Opportunity - Expansion of aftermarket sales induces demand for automotive cleaning systems

The aftermarket segment presents another significant opportunity for industry participants in the automotive camera cleaning system market. As vehicle owners increasingly seek to upgrade and maintain their vehicles' safety and performance features, aftermarket sales of camera cleaning systems are poised for growth.

Many vehicles on the road today are equipped with basic or older-generation camera cleaning systems. The aftermarket offers opportunities to retrofit these vehicles with advanced cleaning technologies, such as high-efficiency pumps, precision cleaning nozzles, and eco-friendly cleaning fluids. Upgrading existing systems can enhance reliability and performance, aligning vehicles with current safety standards and consumer expectations.

Increasing consumer awareness about the benefits of camera cleaning systems through educational campaigns can stimulate aftermarket demand. Industry participants can educate vehicle owners about the importance of clear camera visibility for safety, regulatory compliance, and overall vehicle performance.

Category-wise Analysis

Vehicle Type Insights

Advanced driver assistance systems are becoming increasingly prevalent in passenger vehicles, driven by rising consumer demand for enhanced safety features. ADAS rely heavily on camera-based technologies for functions such as lane departure warning, adaptive cruise control, and automatic emergency braking.

Clear and unobstructed camera lenses are crucial for the accurate operation of these systems, necessitating effective camera cleaning solutions. Stringent regulatory mandates and safety standards worldwide are compelling automotive manufacturers to integrate advanced safety technologies into passenger vehicles.

Globally enforced regulatory mandates and stringent safety standards are increasingly compelling automotive manufacturers to integrate cutting-edge safety technologies into passenger vehicle.

Application Insights

The front safety monitoring application is expected to dominate the market. This dominance is driven by the critical role front cameras play in Advanced Driver Assistance Systems (ADAS) and autonomous driving technologies, where clear visibility is essential for collision avoidance, pedestrian detection, and lane keeping.

Front safety cameras are integral to vehicle safety, requiring reliable cleaning systems to maintain sensor accuracy under diverse weather and road conditions. As regulatory mandates on vehicle safety tighten, manufacturers prioritize front camera cleaning to ensure uninterrupted functionality. The growing adoption of electric and autonomous vehicles further fuels demand for sophisticated cleaning systems in this segment.

Key manufacturers such as Continental, Valeo, Ficosa, and Waymo are advancing cleaning technologies tailored for front safety cameras. For instance, Ficosa has developed an innovative hybrid cleaning system combining water and pressurized air to efficiently clean camera lenses automatically, enhancing safety and driver comfort without adding significant weight or cost.

Regional Insights

Asia Pacific Automotive Camera Cleaning System Market Trends

Asia Pacific is witnessing a rapid surge in the automotive camera cleaning systems market. This growth is fueled by the rising sales of both passenger and commercial vehicles, coupled with heightened awareness regarding vehicle safety standards. Key markets driving the demand include China, Japan, South Korea, and India, where robust economic activity and technological advancement are accelerating the adoption of camera cleaning system.

Asia Pacific expected to be emerging automotive camera cleaning system market. A few factors that are estimated to provide opportunity for the market players in the region are the growing awareness regarding safety technologies and increasing production as well as sales of vehicles. Leading contributors to market growth in this region are Japan, India and China.

North America Automotive Camera Cleaning System Market Trends

North America dominates the automotive camera cleaning system market, accounting for over 30% of the global revenue in 2025. The region is expected to grow at a CAGR of approximately 20.4% from 2025 to 2032. This growth is driven by the high penetration of advanced driver-assistance systems (ADAS) and increasing regulatory mandates, such as the 2023 U.S federal law requiring backup cameras in all new vehicles, which emphasize camera reliability and safety. The demand for improved camera functionality in varying weather conditions fuels the adoption of camera cleaning systems.

Technological advancements, including automatic and sensor-triggered cleaning mechanisms, are being integrated by key manufacturers like dlhBOWLES, Continental, and Valeo to enhance system efficiency and driver safety. Furthermore, the rising consumer focus on vehicle safety and the expansion of electric and autonomous vehicles in North America contribute to the robust market growth.

Europe Automotive Camera Cleaning System Market Trends

The Europe automotive camera cleaning system market is poised for robust growth, driven by increasing integration of camera-based Advanced Driver Assistance Systems (ADAS) in vehicles and stringent safety regulations. Germany, the United Kingdom, and France lead the regional market due to their strong automotive industries and high consumer demand for advanced safety features.

Government policies promoting safer and autonomous vehicles, along with rising disposable incomes and financial incentives, further stimulate market expansion across Western and Eastern Europe. Technological advancements such as automated cleaning mechanisms with intelligent sensors that activate cleaning only when needed are being rapidly adopted by key manufacturers such as Continental, Valeo, and Ficosa. These innovations ensure optimal camera functionality by removing dirt, fog, and moisture, which is critical for reliable ADAS performance.

Competitive Landscape

Competitive rivalry in the global automotive camera cleaning system market is likely to become more intense in the coming years, as technological evolution continues at a robust pace. Tech giants are collaborating with other companies, universities, and researchers to innovate.

Large manufacturers are directing their investments toward innovations in fluid types or nozzle types to enhance a system's existing functionality. Critically growing need to pioneer better technology will facilitate the strategic collaborations between industry players.

Tech giants are collaborating with other companies, universities, and researchers to innovate. Hence, large manufacturers are directing their investments toward innovations in fluid types or nozzle types to enhance a system's existing functionality. Critically growing need to pioneer better technology will facilitate the strategic collaborations between industry players.

Key Industry Developments

- In January 2024, Valeo joined forces with Teledyne FLIR, a division of Teledyne Technologies Incorporated, to pioneer thermal imaging technology in the automotive realm. This strategic alliance aims to bolster road safety by integrating advanced thermal imaging cameras into the next evolution of Advanced Driver-Assistance Systems (ADAS), ushering in a new era of vehicle safety and enhancing the well-being of all road users

- In March 2022, Calsonic Kansei Corporation embarked on a pioneering initiative: the development of a self-cleaning camera system. This innovative technology integrates cutting-edge features like hydrophobic coatings and ultrasonic cleaning mechanisms. By preventing dirt buildup, the system guarantees uninterrupted clarity for camera-based applications, enhancing overall reliability and performance.

Companies Covered in Automotive Camera Cleaning System Market

- Ficosa Internacional SA

- KAUTEX TEXTRON GMBH & CO. KG

- dlhBOWLES

- Continental AG

- Denso Corporation

- Shenzhen Mingshang Industrial Co., Ltd.

- Valeo SA

- MAGNA ELECTRONICS INC.

- MS FOSTER & ASSOCIATES, INC.

- Panasonic Corp.

Frequently Asked Questions

The market is set to reach US$ 1,382.4 Bn in 2025.

Expansion of autonomous and semi-autonomous vehicles and an increase in the number of vehicle-mounted cameras are the major growth drivers.

The industry is estimated to rise at a CAGR of 15.2% through 2032.

Rising adoption of Advanced Driver Assistance Systems (ADAS), and a surge in autonomous and semi-autonomous Vehicles are the key market opportunities.

Ficosa Internacional SA, KAUTEX TEXTRON GMBH & CO. KG, Continental AG, Denso Corporation, Valeo SA are a few leading players.