- Executive Summary

- Global Automotive Battery Market Snapshot 2025 and 2032

- Market Opportunity Assessment, 2025-2032, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Automotive Industry Overview

- Global Battery Industry Overview

- Forecast Factors - Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2019 - 2032

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Automotive Battery Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Global Automotive Battery Market Outlook: Battery Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Battery Type, 2019-2024

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Battery Type, 2025-2032

- Lead Acid

- Flooded

- Absorbed Glass Mat

- Gel Cell Battery

- Lithium Ion

- NiMH

- Others

- Lead Acid

- Market Attractiveness Analysis: Battery Type

- Global Automotive Battery Market Outlook: Vehicle Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Vehicle Type, 2019-2024

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Vehicle Type, 2025-2032

- IC Engine

- Two Wheelers

- Passenger Cars

- LCV

- HCV

- Electric & Hybrid Vehicles

- Two Wheelers

- Passenger Cars

- LCV

- HCV

- IC Engine

- Market Attractiveness Analysis: Vehicle Type

- Global Automotive Battery Market Outlook: Sales Channel

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Sales Channel, 2019-2024

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Sales Channel, 2025-2032

- OEM

- Aftermarket

- Market Attractiveness Analysis: Sales Channel

- Global Automotive Battery Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Region, 2019-2024

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Region, 2025-2032

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Automotive Battery Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2025-2032

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Battery Type, 2025-2032

- Lead Acid

- Flooded

- Absorbed Glass Mat

- Gel Cell Battery

- Lithium Ion

- NiMH

- Others

- Lead Acid

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Vehicle Type, 2025-2032

- IC Engine

- Two Wheelers

- Passenger Cars

- LCV

- HCV

- Electric & Hybrid Vehicles

- Two Wheelers

- Passenger Cars

- LCV

- HCV

- IC Engine

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Sales Channel, 2025-2032

- OEM

- Aftermarket

- Europe Automotive Battery Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2025-2032

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Battery Type, 2025-2032

- Lead Acid

- Flooded

- Absorbed Glass Mat

- Gel Cell Battery

- Lithium Ion

- NiMH

- Others

- Lead Acid

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Vehicle Type, 2025-2032

- IC Engine

- Two Wheelers

- Passenger Cars

- LCV

- HCV

- Electric & Hybrid Vehicles

- Two Wheelers

- Passenger Cars

- LCV

- HCV

- IC Engine

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Sales Channel, 2025-2032

- OEM

- Aftermarket

- East Asia Automotive Battery Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2025-2032

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Battery Type, 2025-2032

- Lead Acid

- Flooded

- Absorbed Glass Mat

- Gel Cell Battery

- Lithium Ion

- NiMH

- Others

- Lead Acid

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Vehicle Type, 2025-2032

- IC Engine

- Two Wheelers

- Passenger Cars

- LCV

- HCV

- Electric & Hybrid Vehicles

- Two Wheelers

- Passenger Cars

- LCV

- HCV

- IC Engine

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Sales Channel, 2025-2032

- OEM

- Aftermarket

- South Asia & Oceania Automotive Battery Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2025-2032

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Battery Type, 2025-2032

- Lead Acid

- Flooded

- Absorbed Glass Mat

- Gel Cell Battery

- Lithium Ion

- NiMH

- Others

- Lead Acid

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Vehicle Type, 2025-2032

- IC Engine

- Two Wheelers

- Passenger Cars

- LCV

- HCV

- Electric & Hybrid Vehicles

- Two Wheelers

- Passenger Cars

- LCV

- HCV

- IC Engine

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Sales Channel, 2025-2032

- OEM

- Aftermarket

- Latin America Automotive Battery Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2025-2032

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Battery Type, 2025-2032

- Lead Acid

- Flooded

- Absorbed Glass Mat

- Gel Cell Battery

- Lithium Ion

- NiMH

- Others

- Lead Acid

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Vehicle Type, 2025-2032

- IC Engine

- Two Wheelers

- Passenger Cars

- LCV

- HCV

- Electric & Hybrid Vehicles

- Two Wheelers

- Passenger Cars

- LCV

- HCV

- IC Engine

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Sales Channel, 2025-2032

- OEM

- Aftermarket

- Middle East & Africa Automotive Battery Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2025-2032

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Battery Type, 2025-2032

- Lead Acid

- Flooded

- Absorbed Glass Mat

- Gel Cell Battery

- Lithium Ion

- NiMH

- Others

- Lead Acid

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Vehicle Type, 2025-2032

- IC Engine

- Two Wheelers

- Passenger Cars

- LCV

- HCV

- Electric & Hybrid Vehicles

- Two Wheelers

- Passenger Cars

- LCV

- HCV

- IC Engine

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Sales Channel, 2025-2032

- OEM

- Aftermarket

- Competition Landscape

- Market Share Analysis, 2024

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Contemporary Amperex Technology Co. Ltd. (CATL)

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- LG Energy Solution

- Panasonic Holdings Corporation

- BYD Company Ltd.

- Samsung SDI Co. Ltd.

- GS Yuasa Corporation

- Clarios (formerly Johnson Controls Power Solutions)

- Toshiba Corporation

- A123 Systems LLC

- Hitachi Chemical Co., Ltd.

- Exide Technologies

- Amara Raja Batteries Ltd.

- Contemporary Amperex Technology Co. Ltd. (CATL)

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Automotive Components & Materials

- Automotive Battery Market

Automotive Battery Market Size, Share, and Growth Forecast for 2025 - 2032

Automotive Battery Market, Share and Growth Forecast by Battery Type (Lead Acid, Lithium Ion, NiMH, Others), by Vehicle Type (IC Engine, and Electric & Hybrid Vehicles), by Sales Channel (OEM, Aftermarket), and Regional Analysis 2025 - 2032

Automotive Battery Market Size and Trends Analysis

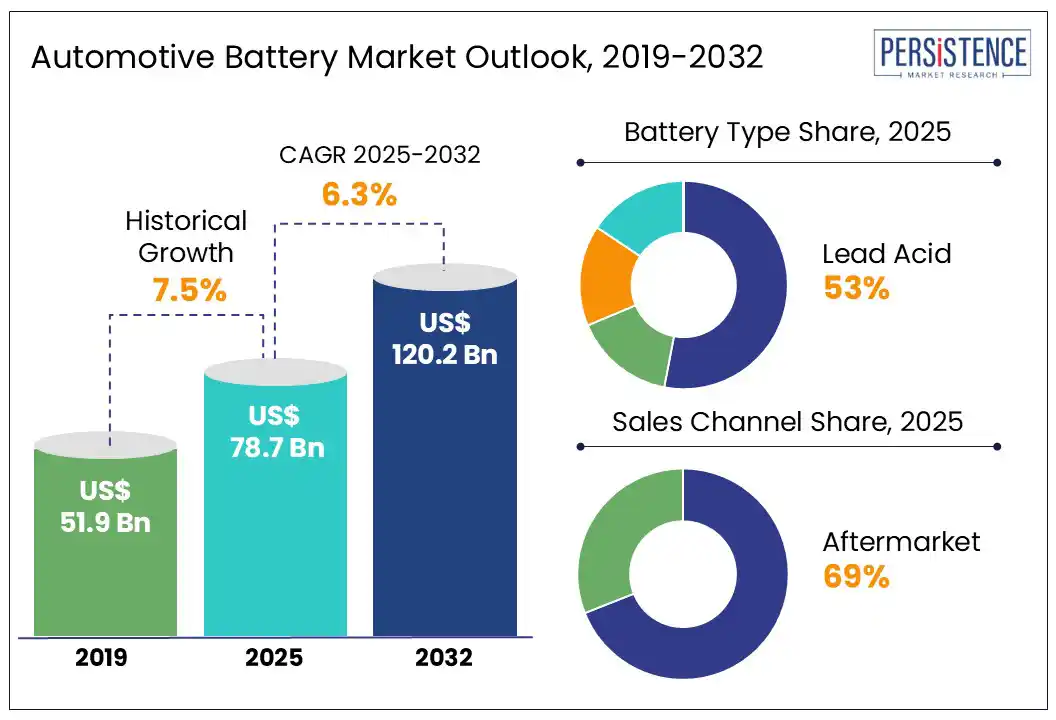

The global automotive battery market size is likely to be valued at US$ 78.7 Bn in 2025 and is expected to reach US$ 120.2 Bn by 2032 growing at a CAGR of 6.3% during the forecast period. Automotive batteries operate on rechargeable basis and supply electric energy to automobiles, most essentially for the automotive SLI (starting, lighting, and ignition) system. The batteries also constantly power automobile accessories such as radio, music players, air conditioners, wipers and charging plugs.

The energy density per unit weight (Wh/kg) is highest in Gasoline batteries, followed by Li-ion and Ni-MH, and is least in Lead-Acid batteries. Lead-Acid batteries are an aging automotive battery technology. Due to its simple or mature technology coupled with fluctuating lead prices in last few years, much of the automotives batteries research is focused on drifting away from this technology.

Key Industry Highlights:

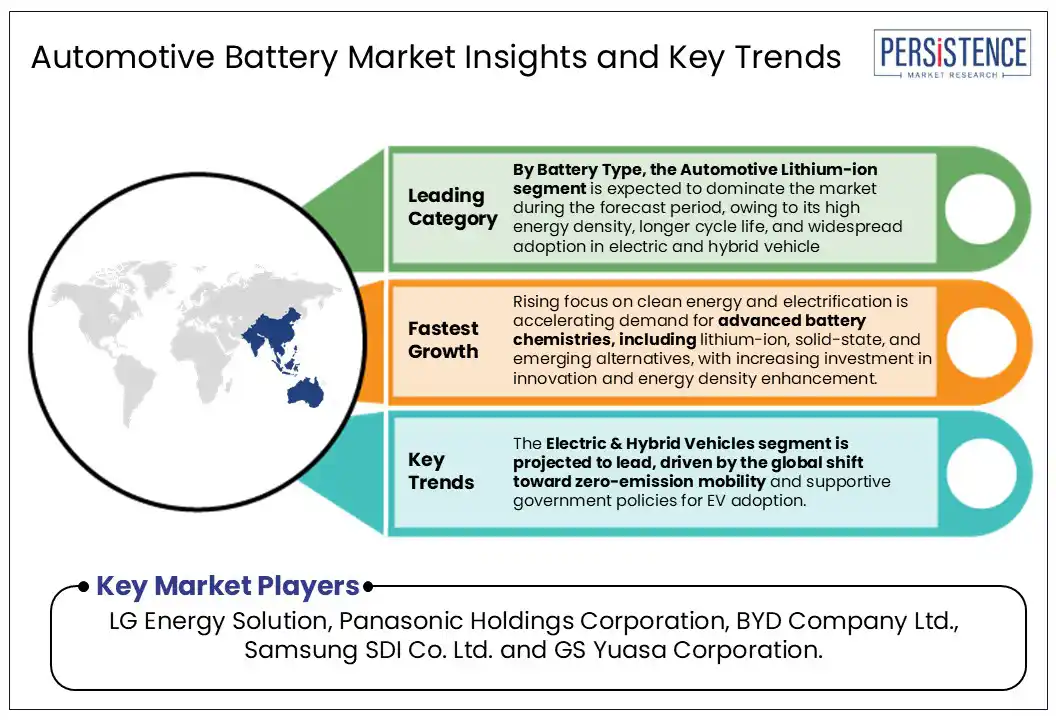

- Rising focus on clean energy and electrification is accelerating demand for advanced battery chemistries, including lithium-ion, solid-state, and emerging alternatives, with increasing investment in innovation and energy density enhancement.

- By Battery Type, the Automotive Lithium-ion segment is expected to dominate the market during the forecast period, owing to its high energy density, longer cycle life, and widespread adoption in electric and hybrid vehicles.

- By Vehicle Type, the Electric & Hybrid Vehicles segment is projected to lead, driven by the global shift toward zero-emission mobility and supportive government policies for EV adoption.

- By Sales Channel, the OEM segment holds the largest market share, supported by direct integration of batteries into new vehicles and automaker partnerships with battery manufacturers.

- Asia Pacific is forecast to remain the dominant region through 2032, led by strong EV production in China, India, and South Korea, as well as favorable policy frameworks and a growing EV supply-chain ecosystem.

| Global Market Attribute | Key Insights |

| Automotive Battery Market Size (2025E) | US$ 78.7 Bn |

| Market Value Forecast (2032F) | US$ 120.2 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 7.5% |

Market Dynamics

Driver - Growing Use of Integrated Electronics Encourages Market Growth

Electronics play a crucial role in enhancing vehicle performance by optimizing two key areas: improving powertrain efficiency to reduce emissions and fuel consumption, and enhancing chassis, exterior, and interior systems to boost safety and comfort. In conventional internal combustion engine (ICE) vehicles, electronics make up approximately 40% of the components, a figure that increases to nearly 75% in hybrid and electric vehicles. These systems contribute around 25% to 30% of total production costs and account for about 90% of automotive innovations. Advances in safety features, connectivity, and telematics are expected to drive future growth in automotive electronics.

The growing demand for vehicle efficiency has led to the development of technologies such as start-stop systems, which shut off the engine during idling to save fuel. During these idle periods, the vehicle’s electronics are powered by the battery, which also supports engine restart. This shift is increasing demand for advanced automotive batteries with higher energy density and improved performance.

Restraint - Supply Chain Vulnerabilities as Restraints in the Automotive Battery Market

The automotive battery market faces significant restraints due to its heavy reliance on critical raw materials like lithium, cobalt, and nickel. These minerals are predominantly sourced from regions prone to political instability, such as the Democratic Republic of Congo (cobalt), South America’s Lithium Triangle, and Indonesia or Russia (nickel). This geographic concentration exposes the supply chain to disruptions from political unrest, trade disputes, or regulatory changes, which can halt mining operations or restrict exports.

Such instability often leads to sharp price fluctuations. For example, lithium and cobalt prices have experienced swings of over 800% and 300% respectively in recent years, directly impacting battery production costs and planning for manufacturers. Additionally, ethical and environmental concerns in mining regions further complicate sourcing. These factors collectively create uncertainty, inflate costs, and hinder the scalability and affordability of automotive batteries, posing a substantial restraint to market growth and global electrification efforts.

Opportunity -Advancement in battery technology and developing battery recycling capabilities

Steer-by-wire technology is gaining traction amid increasing environmental concerns and stringent regulations focused on driver safety and comfort. This innovative system eliminates the traditional mechanical link between the steering wheel and the wheels, replacing it with electronic controls, sensors, and software. By removing bulky mechanical components, steer-by-wire significantly reduces vehicle weight, contributing to improved fuel efficiency and lower carbon emissions a key focus for automakers striving to meet global emission standards.

Beyond environmental benefits, this technology enhances vehicle stability and handling, requiring less steering effort and enabling greater precision. It also supports the advancement of autonomous driving by offering flexible steering control. Major automotive players such as Bosch, Nissan, and Nexteer have made significant strides in developing and promoting steer-by-wire systems, signaling growing industry adoption. According to industry insights, steer-by-wire is expected to become a core component of next-generation vehicles, driven by the shift toward electrification, autonomy, and digitalization in the automotive sector.

Category-wise Analysis

Battery Type Insights

The Automotive lead-acid battery segment continues to dominate the global battery market due to its cost-effectiveness, reliability, and widespread use in internal combustion engine (ICE) vehicles. These batteries are primarily used for starting, lighting, and ignition (SLI) functions and are favored for their mature technology and recyclability. Despite the rapid growth of lithium-ion batteries in the electric vehicle segment, lead-acid batteries maintain a stronghold in the global market due to their affordability and established infrastructure. Their continued relevance in passenger cars, commercial vehicles, and aftermarket replacements ensures sustained demand across both developed and emerging markets.

Flooded lead-acid batteries dominate the market, holding nearly 60% of the global revenue share in 2025. These batteries are widely preferred in conventional internal combustion engine (ICE) vehicles due to their low manufacturing cost, proven reliability, and ease of availability. Flooded lead-acid remains the top choice for applications in light commercial vehicles (LCVs), two-wheelers, and entry-level passenger cars, especially in cost-sensitive markets across Asia Pacific, Latin America, and Africa.

Sales Channel Insights

The aftermarket segment is expected to register the fastest growth in the automotive battery market, with a projected CAGR of 5.6% from 2025 to 2032. This growth is primarily fueled by the increasing need for battery replacements in aging vehicle fleets, especially across Asia Pacific, Latin America, and Africa, where vehicles typically remain in service for extended periods.

Extreme weather conditions, including intense heat and cold, further contribute to battery degradation, boosting demand for replacements. The availability of affordable replacement options and a well-established battery recycling infrastructure also make the aftermarket segment highly attractive for manufacturers and suppliers.

Meanwhile, the OEM segment continues to hold a substantial market share, driven by the ongoing production of new ICE and hybrid vehicles that rely on lead-acid batteries for starting, lighting, and ignition (SLI) functions. However, OEM segment growth is comparatively slower due to advancements in battery technology and longer battery life, which reduce replacement frequency during the vehicle lifecycle.

Regional Insights and Trends

Asia Pacific Automotive Battery Market Trends

Asia Pacific led the global automotive battery market in 2025, holding the largest market share due to several key factors. The region is home to some of the world’s leading battery manufacturers and has witnessed a rapid surge in electric vehicle (EV) adoption, supported by strong government initiatives promoting clean mobility. Countries such as China, Japan, and South Korea are at the forefront of battery production, R&D, and technological innovation.

China automotive battery market held a substantial revenue share of the regional industry in 2025. China has successfully obtained nearly 80% of global lithium chemical production, and an impressive 70% of cell manufacturing for the electric vehicles industry. In addition, government initiatives to offer subsidies determined by the cost gap between electric vehicles and vehicles powered by internal combustion engines are driving market growth.

Meanwhile, India and Southeast Asian countries are experiencing growing vehicle ownership and increasing public and private investments in EV infrastructure, further driving battery demand. These combined factors make Asia Pacific the most dynamic and influential region in shaping the future of the global automotive battery market.

For instance, in April 2024, Panasonic Energy Co., Ltd., one of the prominent primary battery manufacturers and part of Panasonic Group, completed construction of its new production facility within its Suminoe premises in Osaka, Japan.

North America Automotive Battery Market Trends

North America is projected to be the fastest-growing region in the automotive battery market, fueled by rising electric vehicle adoption, stringent emission norms, and robust investments in local battery production. The U.S. and Canada are leading this growth, supported by favorable government policies, including federal and state tax incentives, carbon neutrality targets, and funding for EV charging infrastructure. These initiatives have boosted consumer interest in clean transportation.

Major automakers such as Tesla, General Motors, and Ford are investing heavily in battery gigafactories, strengthening domestic manufacturing capabilities, and reducing dependency on imports. These developments not only support local job creation but also position North America as a key player in the global battery supply chain. With expanding EV infrastructure and a strong push for sustainability, the region is set to play a crucial role in shaping the future of automotive battery technologies.

U.S. regulations regarding recycling and environmental compliance have contributed to a robust circular supply chain for lead-acid batteries. More than 95% of automotive lead-acid batteries in the USA are recycled, reinforcing their environmental sustainability.

Automotive Lead Acid Batteries Remain Integral to Europe’s Automotive Market Amid Electrification Push

The automotive lead acid battery market continues to play a vital role across the European Union, particularly in supporting ICE and hybrid vehicles during the ongoing EV transition. AGM (Absorbent Glass Mat) and EFB (Enhanced Flooded Battery) technologies dominate due to their compatibility with Start-Stop systems, which are mandated under Euro 6 and Euro 7 emission norms. European OEMs prioritize robust battery recycling and consistent chemistry standards, ensuring seamless integration and minimal environmental impact.

Key countries like Germany, France, Italy, and Spain lead in both battery manufacturing and vehicle production. Despite the push toward full electrification, lead-acid batteries remain prominent in OEM and aftermarket applications, supporting various systems in small cars, taxis, LCVs, and EVs as secondary power sources.

In the U.K, demand remains steady, especially in the aftermarket, with consumers favoring cost-effective AGM and EFB replacements for traditional and hybrid vehicles. The U.K.’s robust automotive service network and strong battery recycling ecosystem further support the market while aligning national sustainability objectives.

Competitive Landscape

Key players in the global automotive battery market include Exide Technologies, GS Yuasa International Ltd., Panasonic Holdings Corporation, LG Energy Solution, East Penn Manufacturing, and others. The industry has become highly competitive, prompting companies to adopt strategies such as increased R&D, innovative product development, and facility expansion to gain a competitive edge. These companies focus on delivering high-quality products while expanding manufacturing capacity and investing in infrastructure. Many also pursue vertical integration to strengthen their position across the value chain.

Through these initiatives, automotive battery manufacturers aim to meet rising global demand, reduce production costs, enhance operational efficiency, and broaden their customer base. Innovation and technology development remain central to sustaining long-term competitiveness in this dynamic market.

Key Industry Developments:

- In March 2024, Exide Technologies acquired BE-Power GmbH. This strategic partnership represents a significant achievement as both companies can unite their respective strengths to drive innovative efforts with increased investments in the advanced lithium-ion business.

- In May 2024, EnerSys signed an agreement to acquire Bren-Tronic, Inc., a prominent manufacturer of lithium batteries and charging solutions. The deal strengthened EnerSys's positioning and enhanced its portfolio related to the Specialty Aerospace and defense business.

Companies Covered in Automotive Battery Market

- Contemporary Amperex Technology Co. Ltd. (CATL)

- LG Energy Solution

- Panasonic Holdings Corporation

- BYD Company Ltd.

- Samsung SDI Co. Ltd.

- EnerSys

- GS Yuasa Corporation

- Clarios (formerly Johnson Controls Power Solutions)

- Toshiba Corporation

- A123 Systems LLC

- Hitachi Chemical Co., Ltd.

- Exide Technologies

- Amara Raja Batteries Ltd.

Frequently Asked Questions

The automotive battery market is estimated to be valued at US$ 78.7 Bn in 2025.

Rapid growth in Electric Vehicle (EV) adoption and rising vehicle production are the key demand driver for the automotive battery market.

The automotive battery market is estimated to rise at a CAGR of 6.3% through 2032.

Government incentives & green policies, and expansion of battery manufacturing & gigafactories are the key market opportunities.

The global automotive battery market is dominated by major players such as LG Energy Solution, Panasonic Holdings Corporation, BYD Company Ltd., Samsung SDI Co. Ltd. and GS Yuasa Corporation.