- Healthcare Services

- Remote Patient Monitoring Market

Remote Patient Monitoring Market Size, Share, and Growth Forecast 2026 - 2033

Remote Patient Monitoring Market by Component (Devices / Hardware, Software, Services), by Application (Chronic Disease Management, Post-acute / Hospital-at-home Care, Home Health Monitoring, Preventive Care & Wellness, Elderly Care / Rehabilitation), End-user (Hospitals & Clinics, Home Healthcare Providers, Ambulatory Care Centers, Long-term Care Facilities, Others), and Regional Analysis, 2026 - 2033

Remote Patient Monitoring Market Share and Trends Analysis

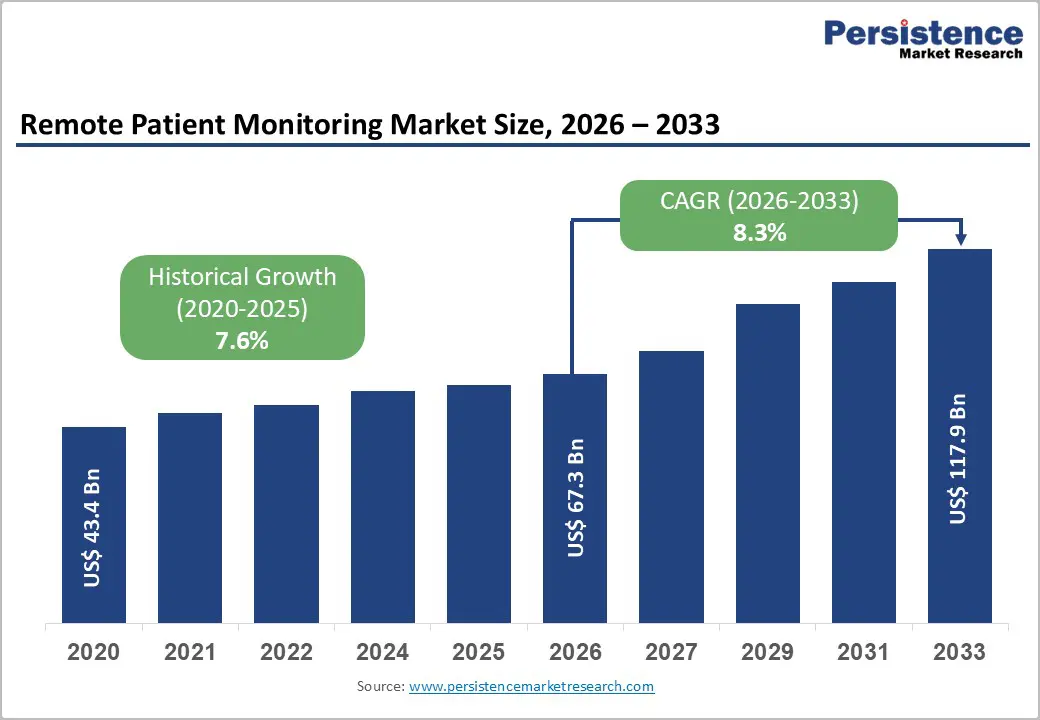

The global remote patient monitoring (RPM) market size is expected to be valued at US$ 67.3 billion in 2026 and projected to reach US$ 117.9 billion by 2033, growing at a CAGR of 8.3% between 2026 and 2033. Rapid adoption of connected health platforms, combined with rising prevalence of chronic diseases and supportive reimbursement policies, is accelerating the shift from episodic in-clinic care to continuous home-based monitoring.

This trend is reinforced by the increasing use of digital devices and wearables for cardiovascular, diabetes, and respiratory management, as well as by growing patient preference for virtual care pathways following the COVID-19 pandemic. In parallel, regulators such as CMS continue to refine RPM billing codes and flexibilities, creating stronger financial incentives for providers and health systems to scale remote monitoring programs.

Key Market Highlights

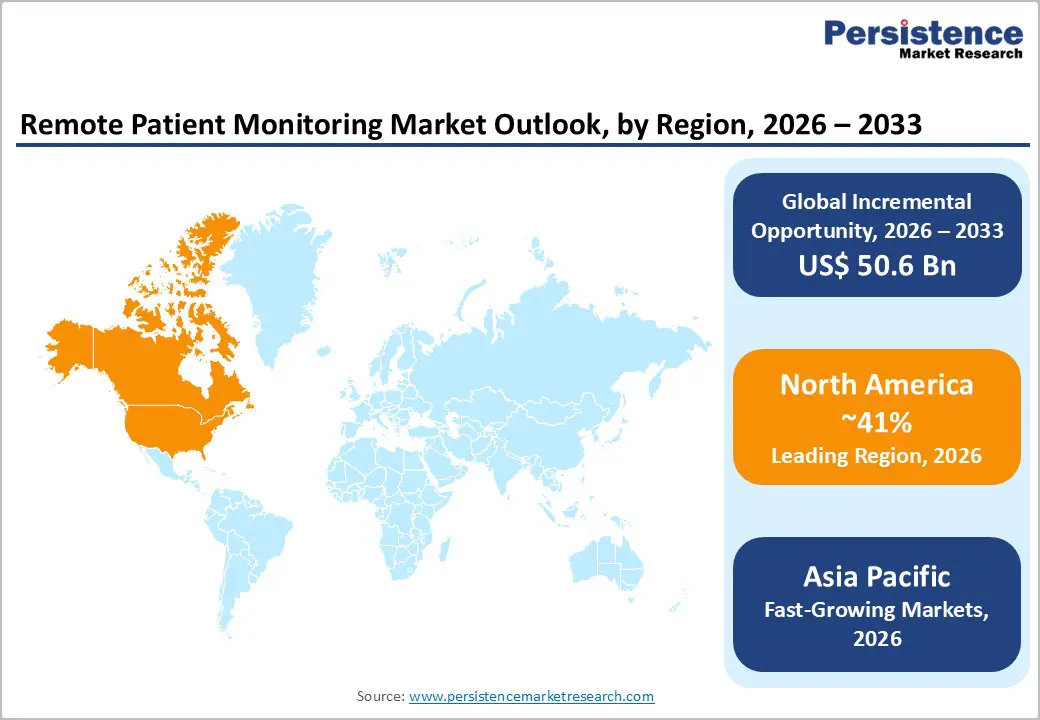

- North America is expected to remain the leading region for remote patient monitoring, driven by high chronic disease prevalence, robust digital infrastructure, and supportive CMS reimbursement frameworks that encourage large-scale provider adoption and enterprise RPM deployments.

- Asia Pacific is projected to be the fastest-growing region, benefiting from large populations, rising healthcare digitization, telemedicine policies, and cost-efficient device manufacturing ecosystems in countries such as China, India, and Japan.

- In the component category, devices/hardware hold a dominant share due to the widespread deployment of connected blood pressure monitors, glucometers, pulse oximeters, and wearables that provide continuous data streams essential to RPM programs.

- Software platforms are expected to be the fastest-growing component segment, as providers demand interoperable dashboards, AI-driven analytics, care coordination tools, and automated alert systems to efficiently manage expanding RPM patient cohorts.

- A key market opportunity is to scale AI-enabled RPM solutions for chronic disease and post-acute hospital-at-home models, helping health systems reduce readmissions, improve outcomes, and shift more care from hospitals to patients’ homes.

| Key Insights | Details |

|---|---|

|

Remote Patient Monitoring Market Size (2026E) |

US$ 67.3 billion |

|

Market Value Forecast (2033F) |

US$ 117.9 billion |

|

Projected Growth CAGR (2026-2033) |

8.3% |

|

Historical Market Growth (2020-2025) |

7.6% |

Market Dynamics

Drivers - Rising Burden of Chronic Diseases and Aging Population

A key growth driver for the remote patient monitoring market is the increasing global burden of chronic diseases combined with rapid population aging. Chronic conditions such as diabetes, cardiovascular diseases, chronic respiratory diseases, and cancer account for a substantial share of global morbidity and mortality, with cardiovascular diseases alone responsible for around 17.6 million deaths annually and diabetes directly linked to at least 5% of all deaths worldwide. RPM solutions enable continuous monitoring of vital signs, glucose levels, blood pressure, and other physiological parameters, thereby enabling clinicians to intervene earlier and prevent disease exacerbations. As more older adults prefer to remain at home while managing complex conditions, the adoption of RPM platforms increases, supporting home-based care models and reducing strain on hospitals and outpatient facilities.

Restraints - Data Integration, Interoperability, and Workflow Burden

One of the primary restraints for the RPM market is the challenge of integrating high-volume remote data into existing clinical workflows and health IT infrastructure. Many health systems struggle with interoperability among RPM platforms, electronic health records (EHRs), and analytics systems, resulting in fragmented data, alert fatigue, and increased documentation burden for clinicians. Without robust data standardization and automated triage tools, providers may find it difficult to scale RPM programs beyond small cohorts, limiting realized benefits despite strong interest and available technologies.

Digital Divide, Patient Engagement, and Privacy Concerns

Limited digital literacy, unequal broadband access, and concerns about data privacy and security also restrain wider RPM uptake, particularly among vulnerable populations. Older adults, low-income groups, and patients in rural or underserved areas may lack reliable internet connectivity, compatible devices, or confidence in using mobile apps and wearables for health monitoring. Additionally, worries about how health data are stored, shared, and monetized can make some patients and clinicians hesitant to fully embrace continuous remote monitoring solutions. Addressing these gaps through education, infrastructure investment, and clear privacy safeguards is essential to unlock the full potential of RPM.

Opportunity - Expansion of AI-Enabled RPM Platforms for Chronic Disease and Preventive Care

A significant opportunity lies in integrating artificial intelligence (AI), advanced analytics, and predictive modeling into RPM platforms for chronic disease management and preventive care. By applying machine learning algorithms to continuous data streams from wearables, implantable devices, and connected home sensors, providers can identify early signs of deterioration, personalize care plans, and prioritize high-risk patients for timely interventions. For example, studies have shown that RPM programs for heart failure and diabetes can reduce hospitalizations and improve outcomes when combined with proactive clinician review and patient coaching. As the global prevalence of type 2 diabetes and cardiovascular disease remains high, AI-enhanced RPM solutions targeting lifestyle modification, medication adherence, and risk factor control present substantial long-term growth prospects for technology vendors and healthcare organizations.

Scaling Hospital at Home and Post-Acute Care Models

Another major opportunity emerges from the accelerating shift towards hospital-at-home and post-acute care models, particularly in high-income countries seeking to free up hospital capacity and reduce costs. RPM technologies can safely support earlier discharge after surgery or acute exacerbations, enabling clinicians to track vital signs, symptom scores, and therapy adherence remotely while patients recover at home. Early evidence suggests that well-designed post-acute RPM programs can lower readmission rates, reduce emergency department visits, and improve patient satisfaction compared to traditional facility-based care. As payers and regulators explore alternative payment models and bundled payments for episodes of care, vendors that can integrate RPM devices, software, and services into scalable hospital-at-home offerings are likely to tap into a rapidly growing revenue pool across multiple therapeutic areas.

Category-wise Analysis

Component Insights

Within the component category, devices / hardware are expected to remain the leading segment, accounting for around 38% of the remote patient monitoring market in 2025. This dominance is supported by the rapid proliferation of connected blood pressure cuffs, glucometers, pulse oximeters, weight scales, cardiac implants, and wearables that form the foundational data-capture layer for RPM programs. Global shipments of health and wellness wearable devices alone are projected to reach approximately 440 million units by 2024, underscoring the scale of hardware penetration in consumer and clinical settings. As more devices obtain regulatory clearance and integrate wireless connectivity and cloud capabilities, hardware investments by providers, payers, and patients will continue to account for a substantial share of overall RPM spending, even as software and service components grow faster.

Application Insights

In the application category, chronic disease management is expected to be the leading segment, accounting for the largest share in 2025. Chronic conditions such as diabetes, hypertension, heart failure, chronic obstructive pulmonary disease (COPD), and arrhythmias require continuous or frequent monitoring to prevent complications and avoid costly acute episodes. RPM programs designed around disease-specific protocols, including daily weight tracking for heart failure patients or continuous glucose monitoring for diabetes, have demonstrated improved control and reduced hospitalizations in multiple studies. Given the rising prevalence of these conditions worldwide and the push towards value-based care, healthcare systems are prioritizing investment in chronic disease RPM pathways, making this application area the central pillar of market demand.

End-user Insights

Among end users, hospitals & clinics are expected to hold the leading share of the global remote patient monitoring market in 2025, ahead of home healthcare agencies and ambulatory care centers. Large health systems and integrated delivery networks often spearhead RPM programs because they have the necessary clinical staff, IT infrastructure, and reimbursement relationships to implement and scale remote monitoring initiatives. Many hospital-based providers have expanded RPM offerings beyond cardiology and endocrinology to include perioperative monitoring, high-risk pregnancy, oncology symptom tracking, and transitional care after discharge. As hospitals increasingly adopt enterprise-wide digital health strategies and link RPM programs to population health management and readmission reduction initiatives, their role as primary purchasers and coordinators of RPM solutions is expected to remain strong.

Regional Insights

North America Remote Patient Monitoring Market Trends and Insights

North America, led by the United States, is expected to remain the leading regional market for remote patient monitoring, with a market share of about 41% in 2025. The region benefits from high penetration of digital health technologies, strong broadband and smartphone adoption, and a large burden of chronic diseases, which creates substantial demand for continuous monitoring. U.S. policy actions have been particularly supportive: CMS has expanded telehealth and RPM coverage, introduced multiple CPT codes, and demonstrated reimbursement flexibility to encourage adoption of remote care in Medicare and Medicaid populations.

The innovation ecosystem in North America is also highly dynamic, with medical device manufacturers, health IT companies, and digital health startups collaborating on integrated RPM platforms across cardiology, metabolic disorders, respiratory care, and mental health. In recent years, large retailers and technology firms have entered the home-based care and RPM space, signaling confidence in long-term growth and helping health systems scale remote care infrastructure. These developments, coupled with increasing patient acceptance of telehealth rising from about 11% usage before the pandemic to roughly 46% during it, provide a strong foundation for sustained RPM expansion in the region.

Asia Pacific Remote Patient Monitoring Market Trends and Insights

The Asia-Pacific region is poised to be the fastest-growing market for remote patient monitoring, supported by large and rapidly aging populations, accelerating urbanization, and a rising burden of chronic diseases. Countries such as China, Japan, India, and members of the ASEAN bloc are investing heavily in digital health infrastructure, smartphone connectivity, and 4G/5G networks, which enable scalable RPM deployment at comparatively lower cost than in earlier-mover regions. The International Diabetes Federation and other organizations have highlighted the sharp growth in diabetes and cardiovascular risk factors across Asia, increasing the need for remote tools to manage glucose, blood pressure, and lifestyle interventions outside hospitals.

Competitive Landscape

The remote patient monitoring market is moderately fragmented, with a mix of global medical technology leaders, health IT vendors, and specialized digital health companies competing and partnering across devices, software, and services. Large incumbents emphasize integrated solutions that combine connected hardware, cloud platforms, analytics, and clinical services, while smaller innovators focus on niche indications, AI algorithms, or user-centric app experiences. Key strategic themes include expanding reimbursable RPM programs with health systems, securing regulatory clearances for new devices and algorithms, pursuing data-driven partnerships with payers, and exploring hybrid business models that blend subscription software, per-patient service fees, and outcomes-based contracts.

Key Developments:

- In February 2026, Assam took a significant step toward AI-enabled public healthcare by installing a contactless, AI-based remote patient monitoring system at Gauhati Medical College and Hospital. The system was deployed in a step-down ICU ward within the newly inaugurated medical college complex.

Companies Covered in Remote Patient Monitoring Market

- Philips Healthcare, Medtronic

- GE Healthcare

- Abbott Laboratories

- Boston Scientific Corporation

- Dexcom

- ResMed

- Masimo

- Omron Healthcare

- AliveCor

- Teladoc Health

- Vivify Health

- BioTelemetry

- iRhythm Technologies

- Honeywell Life Care Solutions

- Tunstall Healthcare

Frequently Asked Questions

The global remote patient monitoring market size is expected to reach about US$ 67.3 billion in 2026, reflecting strong adoption of connected devices, platforms, and services across major healthcare systems worldwide.

A major demand driver is the rising prevalence of chronic diseases and aging populations, which increases the need for continuous home‑based monitoring to prevent complications and reduce hospitalizations.

North America currently leads the global market, supported by robust digital infrastructure, high chronic disease burden, and favorable CMS and payer reimbursement frameworks for telehealth and RPM services.

A key opportunity is the expansion of AI-enabled RPM solutions for chronic disease management and hospital-at-home models, which can improve outcomes while lowering readmissions and overall care costs.

Leading players include Philips Healthcare, Medtronic, GE Healthcare, Abbott Laboratories, Boston Scientific Corporation, Dexcom, ResMed, Masimo, Omron Healthcare, AliveCor, Teladoc Health, Vivify Health, BioTelemetry, iRhythm Technologies, Honeywell Life Care Solutions, and Tunstall Healthcare.