- Medical Devices

- Disposable Incontinence Products Market

Disposable Incontinence Products Market Size, Share, and Growth Forecast, 2026 - 2033

Disposable Incontinence Products Market by Product Type (Protective Garments, Urine Bags, Urinary Catheters), Application (Chronic Kidney Failure, BPH, Other), End-user (Hospitals & Clinics), and Regional Analysis for 2026 - 2033

Disposable Incontinence Products Market Size and Trends Analysis

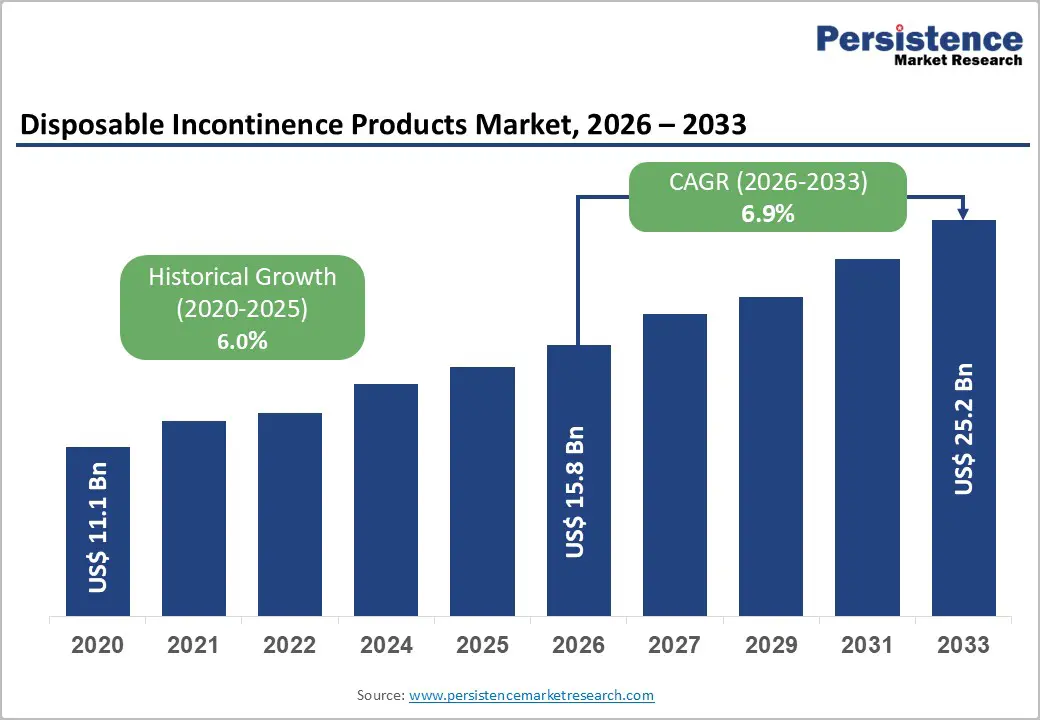

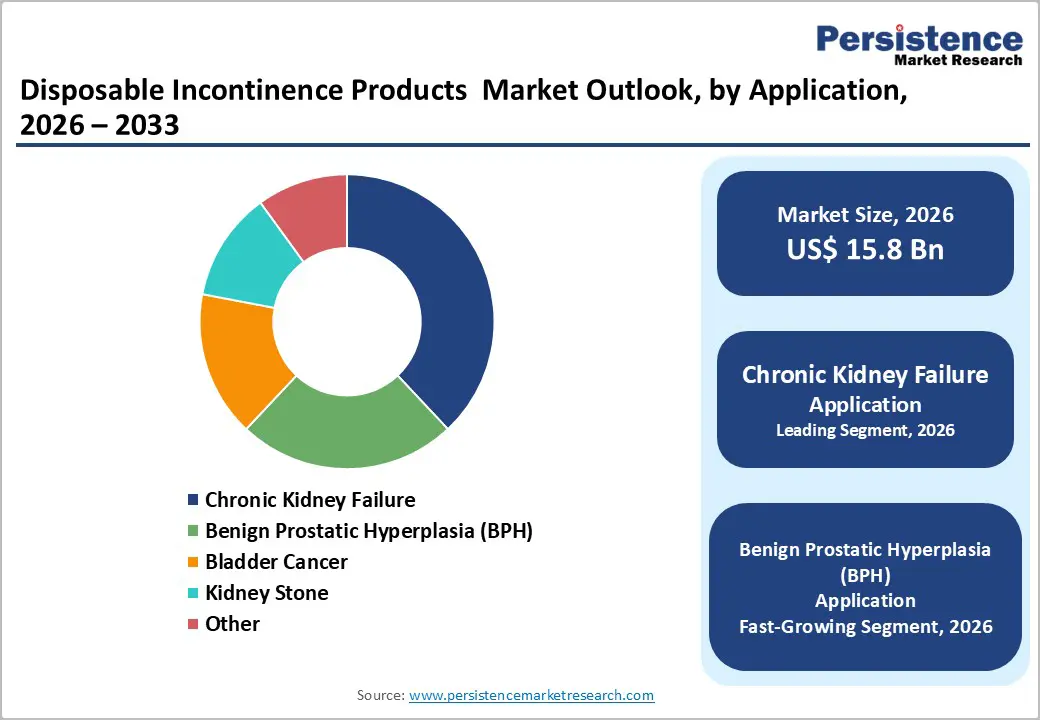

The global disposable incontinence products market size is likely to be valued at US$15.8 billion in 2026, and is expected to reach US$25.2 billion by 2033, growing at a CAGR of 6.9% during the forecast period from 2026 to 2033., driven by the rising prevalence of urinary and fecal incontinence, a condition that affects approximately 420 million people globally, according to the World Health Organization.

Disposable incontinence products include a broad range of single-use absorbent and medical care solutions designed to support incontinence management. These products include adult diapers, pull-up pants, pads, liners, guards, urine collection bags, and both indwelling and intermittent urinary catheters used across homecare and clinical settings.

Key Industry Highlights:

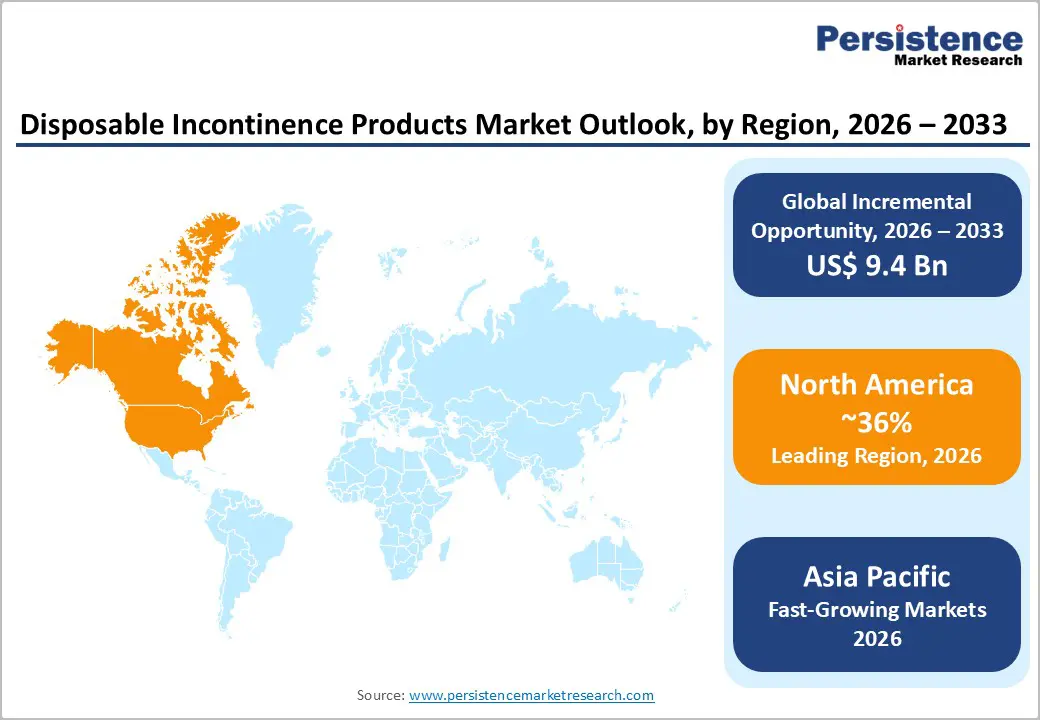

- Dominant Region: North America is expected to dominate, with approximately 36% share in 2026, due to strong reimbursement systems, advanced distribution networks, and high consumer awareness.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing disposable incontinence products market, due to aging populations, rising hygiene awareness, expanding healthcare infrastructure, and increasing disposable incomes.

- Leading Product Type: Protective garments are expected to dominate, holding 52% share in 2026, due to their wide usage across patients with mild to severe urinary incontinence.

- Dominant End-use Industry: Chronic kidney failure is expected to dominate the application segment with over 38% of share in 2026, due to the high prevalence of urinary incontinence and bladder dysfunction among patients with chronic kidney disease and dialysis treatment.

DRO Analysis

Driver - Rapidly Aging Global Population and Rising Incontinence Prevalence

The rapidly aging global population and rising prevalence of urinary and fecal incontinence are the major factors driving market growth. As life expectancy increases worldwide, the proportion of elderly individuals is expanding significantly, particularly in developed regions such as Japan, Germany, and Italy. Aging is strongly associated with weakened bladder and pelvic floor muscles, chronic illnesses, reduced mobility, and neurological disorders, all of which contribute to higher incontinence incidence.

Increasing cases of obesity, diabetes, post-surgical complications, and urinary tract disorders among adults are further expanding the patient population requiring daily incontinence management solutions. Growing awareness regarding personal hygiene, rising acceptance of incontinence care products, and expanding elderly care infrastructure are also accelerating market demand globally.

Restraint - Social Stigma and Low Awareness Suppressing Product Adoption

Despite the high clinical prevalence of urinary incontinence, social stigma remains a major demand suppressor in both developed and emerging markets. Many individuals experiencing urinary incontinence avoid seeking medical consultation due to embarrassment, discomfort, and social perception concerns. This delayed help-seeking behavior slows product adoption, limits market penetration across addressable patient groups, and concentrates product usage primarily among severe-stage patients who can no longer manage symptoms through behavioral or pharmacological treatments.

In emerging regions such as India, Southeast Asia, and Sub-Saharan Africa, awareness of disposable incontinence products remains limited among both consumers and healthcare professionals. Many patients continue using improvised cloth-based alternatives instead of clinically designed disposable products, reducing the overall market demand. Leading manufacturers such as Essity, through its TENA “LastTaboo” initiative, and Kimberly-Clark, through the Depend “ComeBackStrong” campaign, are actively working to reduce stigma and improve awareness.

Opportunity - Product Premiumization and Skin Health Innovation

A significant commercial opportunity exists in premiumizing the disposable incontinence products portfolio through skin health integration, enhanced user comfort, and functional differentiation. Incontinence-associated dermatitis (IAD) affects an estimated 5-15% of hospitalized patients using incontinence products, according to the International Skin Care Nursing Group (ISNG), representing both a clinical burden and a product innovation mandate. Next-generation protective garments incorporating pH-buffering skin barrier agents, aloe-infused inner liners, breathable back sheets with moisture-wicking channels, and antimicrobial surface treatments command meaningfully higher retail and institutional pricing while addressing a genuine clinical unmet need.

Premium product categories, including discreet underwear-style pull-ups for active adults, gender-specific fit designs, and specialty athletic incontinence guards, are expanding the addressable consumer demographic to include younger, active adults experiencing stress incontinence. The premium incontinence segment is estimated to deliver 15-20% higher gross margins relative to commodity protective garments, making it an attractive value-creation lever for incumbents.

Category-wise Analysis

Product Type Insights

Protective garments are expected to dominate the segment, commanding approximately 52% of the total revenue in 2026. This dominance reflects the category’s applicability across the broadest patient population, from community-dwelling adults with mild to moderate urinary incontinence to institutionalized patients with severe functional impairment. Kimberly-Clark offers Depend® Real Fit® protective underwear designed for adults with mild to heavy urinary incontinence, providing discreet, underwear-like protection for both active community-dwelling users and patients requiring long-term continence care.

Urinary catheters represent the fastest-growing product segment, driven by rising prevalence of neurogenic bladder conditions, expanded clinical indication for intermittent self-catheterization (ISC) as a gold-standard management protocol for spinal cord injury and multiple sclerosis patients, and growing physician preference for ISC over long-term indwelling catheter use to reduce catheter-associated urinary tract infection (CAUTI) rates. Coloplast offers the SpeediCath® intermittent catheter range, which is widely used for intermittent self-catheterization (ISC) in patients with spinal cord injury and multiple sclerosis.

Application Insights

Chronic kidney failure is anticipated to dominate, contributing approximately 38% of the global revenue in 2026. Patients with chronic kidney disease (CKD), particularly those on hemodialysis or peritoneal dialysis, frequently experience urinary incontinence and reduced bladder function due to the systemic effects of renal failure on neurological and musculoskeletal systems. Fresenius Medical Care provides dialysis and renal care solutions for chronic kidney disease patients, who commonly experience bladder dysfunction and urinary incontinence during long-term treatment.

Benign prostatic hyperplasia (BPH) is expected to be the fastest-growing application segment, driven by the rapid expansion of the global male aging population and the growing diagnosis and treatment rate for lower urinary tract symptoms (LUTS). Over 50% of men aged 60-69 and up to 90% of men over 80 experience BPH symptoms, yet treatment and incontinence product adoption rates remain below the clinical prevalence curve, representing a significant underpenetration opportunity. Boston Scientific offers the Rezum™ Water Vapor Therapy system for treating benign prostatic hyperplasia (BPH) and lower urinary tract symptoms (LUTS) in aging male patients.

End-user Insights

Hospitals & clinics are expected to dominate, accounting for approximately 45% of global revenue in 2026. Within institutional settings, urinary catheters and urine collection bags constitute the highest per-unit value products, with hospital group purchasing organizations (GPOs) such as Premier, Vizient, and Provista channeling significant volume procurement through negotiated supplier contracts. Vizient partners with Becton Dickinson to supply urinary catheters and urine collection systems to hospitals through group purchasing contracts.

Homecare settings represent the fastest-growing end-user segment. The structural shift toward home-based care delivery, aging-in-place preferences among elderly patients, and the expansion of reimbursement coverage for home health services are converging to drive rapid volume growth in the homecare channel. Convatec provides continence care and catheter products for home-based urinary management among elderly and chronically ill patients.

Regional Insights

North America Disposable Incontinence Products Market Trends

North America is projected to dominate the market, holding approximately 36% of the total revenue in 2026, with the U.S. accounting for over 85% of the regional demand. The U.S. market is underpinned by a combination of strong reimbursement coverage, Medicare Part B reimburses urinary catheters and drainage bags for eligible beneficiaries, while Medicaid covers incontinence supplies in many state programs, a well-established retail pharmacy and e-commerce distribution infrastructure, and high consumer awareness, driven by sustained brand marketing by Kimberly-Clark and Essity.

U.S. Disposable Incontinence Products Market Insights

The U.S. market is also at the forefront of clinical catheter innovation, driven by CAUTI prevention mandates embedded in CMS hospital reimbursement policy. Hospitals are transitioning from traditional Foley catheters toward antimicrobial-coated and silver-alloy impregnated designs, driving revenue mix shift toward higher-ASP clinical catheter products.

Canada Disposable Incontinence Products Market Insights

Canada, representing approximately 12-15% of the North America market value, shares similar demographic drivers, an aging population, universal healthcare coverage, and provincial health authority procurement frameworks. Canadian provincial drug formularies and provincial home care programs increasingly include disposable incontinence supplies, supporting homecare segment growth.

Europe Disposable Incontinence Products Market Trends

The Europe disposable incontinence products market is supported by well-established healthcare systems, broad national insurance coverage for continence care products, and an aging population across the region. Germany represents the largest market in Europe, driven by its median population age of over 46 years and a highly developed long-term care infrastructure. The country’s Pflegeversicherung (long-term care insurance) program reimburses incontinence products for both nursing home residents and homecare patients, supporting stable, reimbursement-driven market demand.

U.K. Disposable Incontinence Products Market Trends

The U.K. market is characterized by NHS procurement frameworks that drive volume purchasing of standardized incontinence products through NHS Supply Chain, alongside a growing retail and online direct-to-consumer segment. Post-Brexit regulatory alignment with MDR (Medical Device Regulation) equivalents creates a distinct compliance landscape that international suppliers must navigate.

Germany Disposable Incontinence Products Market Trends

Germany is the dominant European market, with a population median age exceeding 46 years and a robust long-term care infrastructure Germany’s Pflegeversicherung (long-term care insurance) system funds incontinence product provision for nursing home and homecare patients, creating a reimbursement-backed volume market.

Asia Pacific Disposable Incontinence Products Market Trends

Asia Pacific market is likely to be the fastest-growing region, driven by converging forces: rapidly aging demographics (Japan, China, South Korea, and Australia), expanding middle-class consumer populations with rising hygiene standards and disposable income, growing healthcare infrastructure in emerging economies, and progressively improving awareness and de-stigmatization of incontinence management.

Japan Disposable Incontinence Products Market Trends

Japan is projected to remain the world’s most aged major economy and represents the most mature incontinence products market in the region, with per-capita product usage nearing levels observed in Western countries. The domestic market is led by major Japanese manufacturers such as Unicharm through its Lifree brand, and Daio Paper, both of which offer technologically advanced, ultra-thin, and highly absorbent products designed to meet consumer preferences for discretion, comfort, and skin protection.

China Disposable Incontinence Products Market Trends

China represents the region’s single largest volume opportunity, with an elderly population exceeding 280 million and rapidly expanding institutional care capacity under the government’s “Healthy China 2030” initiative. Chinese domestic incontinence product manufacturers are gaining share in the mid-market segment, while international brands (TENA, Depend, and Unicharm) maintain premium tier positions through retail and e-commerce channels.

Competitive Landscape

The global disposable incontinence products market is characterized by a moderately consolidated competitive landscape across two distinct tiers: consumer-oriented absorbent garment manufacturers and clinical-use urological device suppliers. In the consumer segment, Kimberly-Clark Corporation, Essity AB, and Unicharm Corporation dominate globally, collectively accounting for an estimated 45-50% of the absorbent garment category. These players compete on brand equity, product innovation, distribution scale, and sustainability credentials.

In the clinical urological device segment encompassing urinary catheters and urine bags, the competitive landscape is anchored by dedicated medical device companies, including Coloplast A/S, Becton Dickinson, Hollister Incorporated, B. Braun Melsungen, Teleflex Incorporated, and ConvaTec Group. These players compete on clinical differentiation, GPO contract coverage, clinical evidence generation, and reimbursement support services.

Key Industry Developments:

- In June 2025, Kimberly-Clark sold a majority stake in its international tissue unit to Suzano for USD 3.4 billion while retaining 49% ownership, freeing capital to focus on core personal-care categories, including incontinence products.

- In February 2025, the European Union enacted the Packaging and Packaging Waste Regulation that requires all packaging to be recyclable by 2030 and sets a 5% plastic-reduction target by 2030, compelling disposable incontinence product makers to redesign material choices.

Companies Covered in Disposable Incontinence Products Market

- Kimberly-Clark

- Essity

- Unicharm

- Coloplast

- Becton Dickinson

- Hollister

- B. Braun

- Teleflex

- ConvaTec

- Medline Industries

Frequently Asked Questions

The global disposable incontinence products market is projected to reach US$15.8 billion in 2026.

The primary drivers are the rapid global aging demographic, rising prevalence of chronic kidney failure, BPH, and other urological conditions, and the accelerating shift toward homecare-based continence management.

The disposable incontinence products market is poised to witness a CAGR of 6.9% from 2026 to 2033.

Key opportunities include the premiumization of protective garments with skin health and sustainability features commanding higher margins, the rapid growth of the homecare catheter segment as self-catheterization protocols expand, and the vast underpenetrated demand in emerging markets, particularly India and Southeast Asia where per-capita incontinence product consumption remains well below clinical prevalence levels.

Key players include Kimberly-Clark Corporation, Essity AB, Unicharm Corporation, Coloplast A/S, Becton Dickinson and Company, Hollister Incorporated, B. Braun Melsungen AG, Teleflex Inc., ConvaTec Group PLC, and Medline Industries LP.