- Home Appliances

- Domestic Heating Appliances Market

Domestic Heating Appliances Market Size, Share, and Growth Forecast 2026 - 2033

Domestic Heating Appliances Market by Product Type (Room Heating Appliances, Water Heating Appliances, Cooking Appliances, Others), by Energy Source (Electric, Gas, Oil, Renewable, Hybrid), by Technology (Manual, Programmable, Smart), by Installation Type (Portable/Standalone, Fixed/Wall‑mounted, Built‑in), End‑user (Residential, Commercial), and Regional Analysis, 2026 - 2033

Domestic Heating Appliances Market Size and Trend Analysis

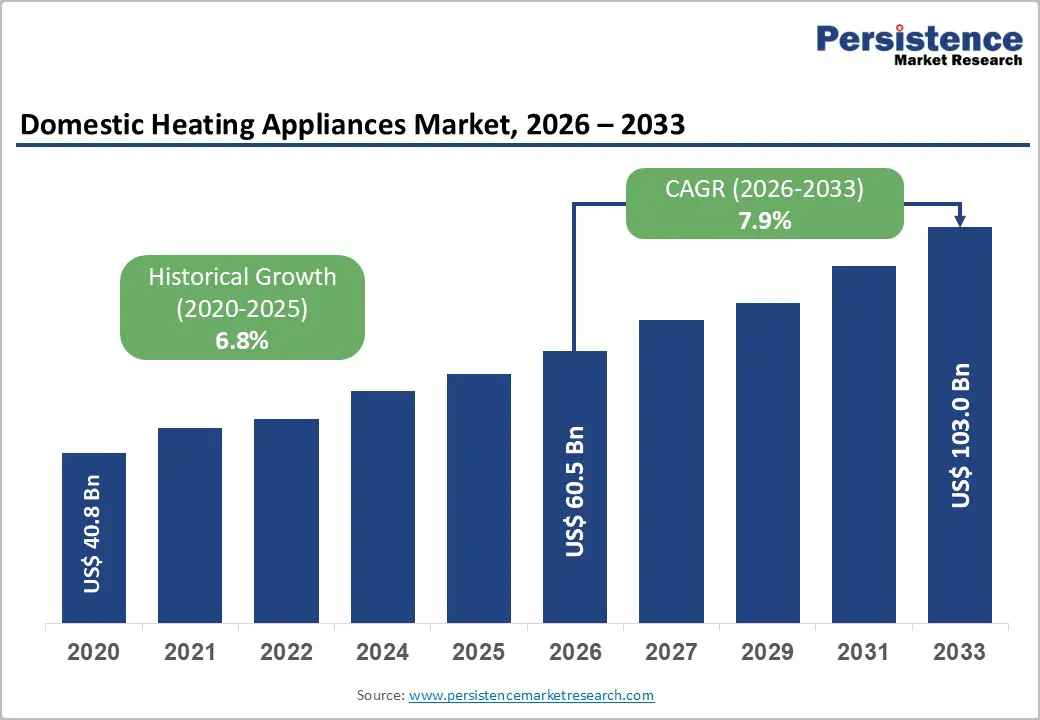

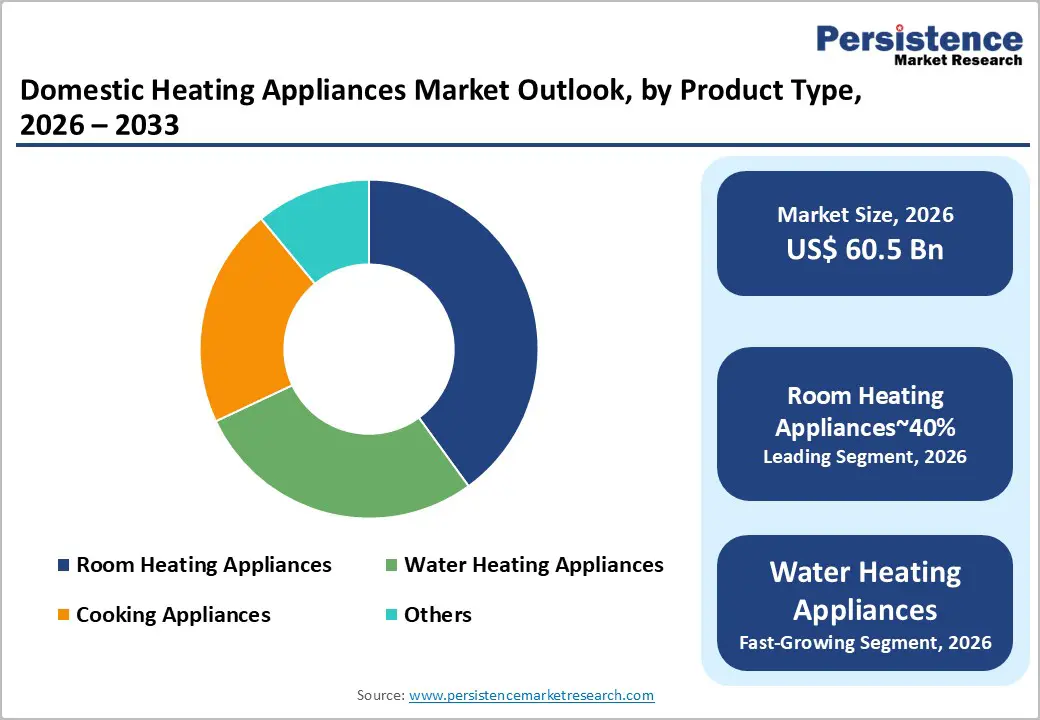

The global domestic heating appliances market size is likely to be valued at US$60.5 billion in 2026 and is expected to reach US$103.0 billion by 2033, growing at a CAGR of 7.9% during the forecast period from 2026 to 2033. This expansion is underpinned by rising urbanization, increasing homeownership rates, and a growing preference for energy-efficient, smart-enabled appliances across residential and commercial buildings.

Key Industry Highlights:

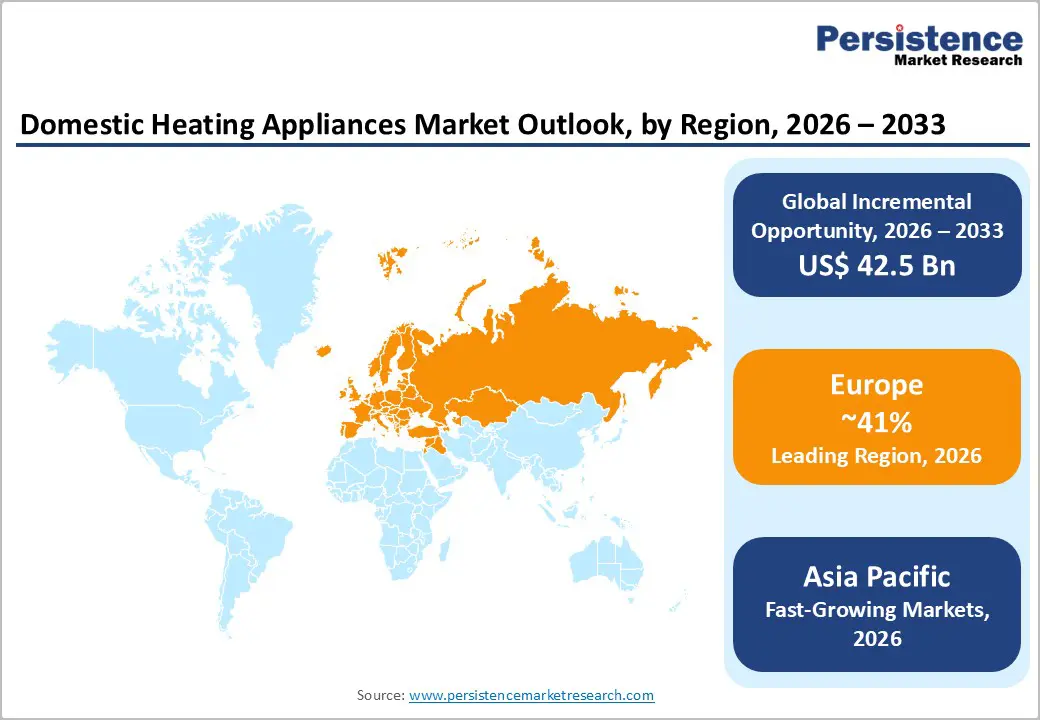

- Leading region: Europe dominates the Domestic Heating Appliances Market, with a 41% share, due to strict energy regulations.efficiency regulations, high adoption of smart heating systems, and strong policy support for low-carbon heating technologies.

- Fastest Growing Region: Asia Pacific is the fastest-growing region with a rising CAGR of 9.6%, driven by rapid urbanization, rising disposable incomes, and expanding housing construction in China, India, and ASEAN countries.

- Dominant Segment: The Electric segment within Energy Source is the dominant segment holding 45% share, supported by ease of installation, low maintenance, and compatibility with smart-home platforms and renewable electricity.

- Fastest Growing: The Smart segment within Technology is the fastest-growing with a rising CAGR of 8.7%, as consumers increasingly adopt IoT-enabled room heaters, water heaters, and thermostats that offer remote control and energy-usage analytics.

- Key Market Opportunity: Integration of renewable-compatible and smart heating solutions presents a major opportunity, particularly in markets with strong decarbonization policies and incentives for heat pumps, solar-assisted systems, and hybrid appliances.

| Key Insights | Details |

|---|---|

|

Domestic Heating Appliances Market Size (2026E) |

US$ 60.5 Billion |

|

Market Value Forecast (2033F) |

US$ 103.0 Billion |

|

Projected Growth CAGR (2026–2033) |

7.9% |

|

Historical Market Growth (2020–2025) |

6.8% |

Market Dynamics

Drivers - Urban housing expansion accelerates demand for modern domestic heating appliances across residential and commercial buildings

Rapid urbanization and rising homeownership are significantly increasing the number of residential and commercial buildings that require reliable domestic heating. Across many countries, reports from organizations such as the World Bank and OECD indicate that urban populations are growing faster than total population levels, leading to increased demand for modern housing equipped with room heating, water heating, and cooking systems. This shift is especially strong in the Asia Pacific and parts of Latin America, where large housing projects increasingly include electric and gas-based heating appliances as standard infrastructure.

As living standards improve, consumers are prioritizing indoor comfort, safety, and convenience, further boosting appliance adoption. The growing middle-class population is also more willing to invest in durable and efficient heating solutions. As a result, manufacturers such as Midea, Haier, and LG Electronics are benefiting from a larger installed base and rising replacement demand, supporting long-term market expansion.

Government efficiency standards and decarbonization policies are rapidly shifting demand toward smart, low-carbon heating technologies

Government regulations focused on energy efficiency and carbon reduction are strongly influencing purchasing decisions across the domestic heating appliances market. Policymakers are encouraging a shift toward high-efficiency boilers, heat pumps, smart thermostats, and renewable-compatible systems to reduce household energy consumption and emissions. In Europe, stricter Energy Performance of Buildings Directive (EPBD) requirements and the gradual phase-out of fossil-fuel-based heating in new buildings are accelerating the transition to electric and hybrid heating solutions.

Similar regulatory pressure exists in North America, where ENERGY STAR standards and updated building codes favor low-energy appliances. These policies are pushing manufacturers such as Carrier, Trane, and Lennox International Inc. to invest heavily in smart, low-carbon product portfolios. Over time, regulation-driven replacement of older systems is expected to remain a major driver of market growth.

Restraints - High upfront system costs and limited financing access continue to slow adoption of advanced heating solutions

The high initial cost of advanced domestic heating systems remains a major barrier to widespread adoption, particularly in emerging and price-sensitive markets. Technologies such as heat pumps, condensing boilers, and smart heating networks require significantly higher upfront investment than traditional electric heaters or conventional gas systems. Many households in developing regions lack access to affordable financing, subsidies, or low-interest loan programs, which limits their ability to upgrade to energy-efficient solutions.

As a result, consumers often continue using low-cost but inefficient appliances despite higher long-term energy expenses. This cost sensitivity slows the penetration of premium and technology-driven segments, including smart and renewable-integrated heating systems. For manufacturers focused on high-value products, slower adoption can restrict revenue growth and market expansion. Without stronger government incentives or financing support, affordability will remain a key challenge in unlocking full market potential.

Weak Power and Gas Infrastructure in Developing Regions Restricts Large-Scale Deployment Of Modern Heating Appliances

In several regions across Asia-Pacific, Latin America, and Africa, weak infrastructure continues to limit the adoption of modern domestic heating appliances. Unreliable electricity supply discourages households from investing in electric room heaters and water heaters, as frequent power outages reduce performance consistency and consumer trust. At the same time, underdeveloped gas distribution networks restrict the use of gas-fired heating systems, particularly in rural and semi-urban areas.

These infrastructure challenges force manufacturers to design alternative solutions, such as solar-assisted, hybrid, or low-power portable heaters to meet local conditions. While these adaptations help maintain market presence, they often result in lower margins and slower technology upgrades. Overall, limited grid stability and delays in fuel access impede the transition to high-efficiency and smart heating solutions, constraining market growth across developing regions.

Opportunities - Rising Smart Home Adoption Is Driving Strong Growth in IoT-enabled and AI-Controlled Heating Appliances

The growing adoption of smart home technologies is creating strong opportunities for IoT-enabled domestic heating appliances. Consumers increasingly prefer heating systems that allow remote temperature control through smartphones, automated scheduling, and real-time energy monitoring. These smart features improve comfort while helping households reduce electricity and gas expenses, making them attractive in both developed and urbanizing markets. Artificial intelligence and cloud-based platforms further enhance efficiency by learning user preferences and adjusting heating patterns automatically.

Major brands such as Samsung, Panasonic Corporation, and Mitsubishi Electric Corporation are actively expanding smart heating ecosystems that integrate with broader home automation platforms. Beyond hardware sales, connected appliances also generate additional revenue through software updates, maintenance services, and energy management subscriptions. As digital lifestyles continue to grow, smart heating solutions are expected to become a key differentiator and one of the fastest-expanding segments within the market.

Net-zero Targets and Renewable Incentives are Accelerating Demand for Low-Carbon and Hybrid Heating Systems

Global commitments to reduce carbon emissions are accelerating demand for renewable-integrated and low-carbon heating appliances. Technologies such as heat pumps, solar-assisted water heaters, and hybrid gas-electric systems are gaining strong momentum as governments promote cleaner household energy use. Countries including Germany, France, and the United Kingdom provide subsidies, tax credits, and installation incentives that make sustainable heating systems more affordable for consumers.

This policy support is driving the large-scale replacement of traditional oil and gas boilers in residential buildings. Manufacturers such as Glen Dimplex Group and Rinnai Corporation are rapidly expanding product portfolios focused on air-source and ground-source heat pumps to capture this growing demand. As energy prices fluctuate and climate regulations tighten, renewable-based heating is expected to shift from a niche solution to a mainstream choice, creating long-term growth opportunities across both new construction and retrofit markets.

Category-wise Analysis

Product Type Insights

Room heating appliances represent the largest product segment, accounting for approximately 40% of total market volume. This leadership is driven by widespread use of electric convectors, fan heaters, radiant heaters, and centralized heating systems across cold and temperate regions. Europe and North America show particularly strong demand due to long winters and high indoor comfort standards. In urban apartments and modern homes, compact and efficient room heaters are increasingly preferred for quick temperature control and space efficiency.

The growing popularity of smart room heaters with Wi-Fi connectivity, programmable schedules, and mobile app controls is further strengthening this segment. Consumers are attracted to these products for their ability to improve comfort while lowering energy bills. As households increasingly prioritize personalized climate control, room heating appliances are expected to maintain their dominant position while evolving toward more connected and energy-efficient designs.

Energy Source Insights

Electric heating appliances account for the largest share of the market, estimated at approximately 45%, owing to their ease of installation, low maintenance requirements, and broad availability across urban areas. Unlike gas systems, electric heaters do not require complex infrastructure, making them ideal for apartments, rented homes, and newly developed housing projects. Their compatibility with smart thermostats and home automation systems further boosts adoption among tech-savvy consumers. In addition, the growing share of renewable electricity from solar and wind sources is improving the environmental profile of electric heating solutions.

Many governments are encouraging electrification as part of long-term decarbonization strategies, supporting further market expansion. As power grid reliability improves in developing regions, electric appliances are expected to gain even stronger momentum. Overall, the advantages of convenience, flexibility, and sustainability continue to make electric heating the preferred energy source for households worldwide.

Technology Insights

Smart heating appliances are emerging as one of the fastest-growing technology segments, currently representing about 20% of the market but expanding rapidly. These systems use IoT connectivity, mobile applications, and cloud platforms to enable real-time temperature control, energy tracking, and automated adjustments based on user behavior. Smart devices also integrate with voice assistants such as Amazon Alexa and Google Assistant, creating seamless home comfort experiences.

Consumers value these features for improved convenience, reduced energy waste, and lower monthly utility costs. The segment is particularly strong in North America and Western Europe, where smart home adoption is already high. Leading companies such as Samsung, LG Electronics, and Honeywell International Inc. are continuously launching advanced connected heating solutions. As digital lifestyles grow globally, smart technology is expected to become a standard feature rather than a premium option across domestic heating appliances.

Installation Type Insights

Fixed and wall-mounted heating appliances hold a leading share of approximately 35%, reflecting growing preference for permanent and space-saving solutions in modern housing. Wall-mounted electric heaters, gas heaters, boilers, and water heaters are particularly common in urban apartments, where floor space is limited. These systems offer clean aesthetics, improved safety, and efficient heat distribution while blending easily with interior design layouts. In regions such as Europe and East Asia, building regulations and architectural trends increasingly favor concealed or semi-concealed installations for better space utilization. Wall-mounted systems also support higher-capacity heating compared to portable devices, making them suitable for long-term residential use. As urban living spaces become smaller and more design-focused, demand for compact fixed heating solutions is expected to continue rising. This trend supports steady growth for manufacturers specializing in modern built-in heating appliances.

End-user Insights

The residential sector dominates the domestic heating appliances market with an estimated share of nearly 70%, driven by rising home construction and expanding urban populations. New housing developments across Asia Pacific, Europe, and North America increasingly include modern room heaters, water heaters, and integrated heating systems as standard features. Higher disposable incomes and improved living standards are also encouraging households to upgrade from basic appliances to energy-efficient and smart solutions.

Aging populations in countries such as Japan and Germany are increasing demand for easy-to-operate, safe, and low-maintenance heating products. Homeowners are placing greater emphasis on indoor comfort, consistent heating, and long-term energy savings. Government housing programs and renovation incentives further support the adoption of residential appliances. Together, these factors ensure that residential users will remain the primary revenue driver for the market in the foreseeable future.

Regional Insights

North America Domestic Heating Appliances Market Trends

North America shows strong demand for high-efficiency furnaces, heat pumps, and smart heating systems, supported by robust energy-efficiency programs and strict performance standards. In the United States, agencies such as the Department of Energy and ENERGY STAR guide consumers toward low-energy appliances through labeling and regulatory requirements. These initiatives are accelerating the replacement of older heating systems with advanced, environmentally friendly technologies. The region also benefits from a well-developed smart home ecosystem that facilitates rapid adoption of connected thermostats and automated heating systems. Companies such as Carrier, Lennox International Inc., and Trane continue to introduce AI-driven climate-control products that enhance comfort while reducing energy consumption. Rising energy costs are further motivating homeowners to invest in efficient heating systems. Overall, innovation, regulation, and strong consumer awareness make North America a mature yet steadily growing market.

Europe Domestic Heating Appliances Market Trends

Europe remains one of the most policy-driven markets for domestic heating appliances, with a strong focus on sustainability and carbon reduction. Countries such as Germany, the United Kingdom, France, and Spain are actively promoting the adoption of heat pumps and energy-efficient heating systems through subsidies and regulatory mandates. The Energy Performance of Buildings Directive is accelerating the replacement of fossil-fuel boilers with electric and hybrid alternatives in both new and existing buildings.

Harmonized product standards and the EU Energy Label help consumers easily identify efficient appliances, encouraging informed purchasing decisions. Leading manufacturers such as Bosch, Glen Dimplex Group, and Rinnai Corporation are aligning product strategies with low-carbon goals. Retrofit projects in aging housing stock further support demand growth. As Europe continues its transition toward net-zero targets, the domestic heating appliances market is expected to remain highly active and innovation-driven.

Asia Pacific Domestic Heating Appliances Market Trends

Asia Pacific is experiencing rapid market expansion driven by urbanization, rising incomes, and large-scale residential construction. China and Japan serve as major manufacturing hubs, producing a wide range of electric heaters, gas water heaters, and heat-pump-based systems for domestic and global markets. In developing economies such as India and Southeast Asian countries, demand is shifting from basic electric heaters toward more efficient gas and hybrid solutions.

Government initiatives aimed at improving energy access, reducing emissions, and stabilizing power grids are further supporting the adoption of modern heating technologies. As middle-class populations grow, consumers are increasingly willing to invest in higher-quality and durable heating appliances. Seasonal temperature variations in parts of the region also contribute to increased room-heating demand. Overall, Asia Pacific is expected to remain the fastest-growing regional market over the coming decade.

Competitive Landscape

The global domestic heating appliances market is moderately consolidated, featuring a combination of global manufacturers, regional specialists, and component suppliers. Major players such as Midea, Haier Inc., LG Electronics, Samsung, Daikin Industries, Mitsubishi Electric Corporation, Panasonic Corporation, Carrier, Trane, Lennox International Inc., Honeywell International Inc., Glen Dimplex Group, Rinnai Corporation, and BSH Hausgeräte GmbH collectively hold a substantial share of global revenue. These companies dominate premium segments, including smart heating systems, heat pumps, and energy-efficient appliances.

Competitive strategies increasingly focus on geographic expansion, particularly in Asia Pacific and Latin America, where urban growth is strongest. Many firms are also investing in digital platforms, AI-based controls, and connected ecosystems to differentiate products. Strategic partnerships with technology providers and renewable energy companies are becoming common. Overall, innovation, sustainability, and smart features are shaping long-term competition across the market.

Key Developments:

- In January 2025: Carrier unveiled its latest air-to-water heat pump for residential and light-commercial use, featuring advanced energy-efficient performance and integrated smart controls. The system is designed to reduce energy use while delivering heating, cooling, and domestic hot water in a single unit.

- In September 2024: Midea broadened its electric room and water heating lineup across the Asia Pacific, introducing new energy-efficient models compliant with regional IEC and GB standards to better serve rapidly growing urban housing markets in the region.

- In March 2024: LG Electronics entered a strategic collaboration with a major European energy utility to pilot smart heating and water-heating systems for smart-city applications, focusing on demand-response optimization and enhanced energy efficiency in residential and mixed-use environments.

Companies Covered in Domestic Heating Appliances Market

- Honeywell International Inc.

- Midea

- Haier Inc.

- Hitachi Air Conditioning Company

- DAIKIN INDUSTRIES, Ltd.

- Glen Dimplex Group

- Trane

- Lennox International Inc.

- LG Electronics

- Mitsubishi Electric Corporation

- Panasonic Corporation

- Carrier

- Samsung

- Rinnai Corporation

- BSH Hausgeräte GmbH

- Bosch Thermotechnology (Robert Bosch GmbH)

- Vaillant Group

- NIBE Industrier AB

- A.O. Smith Corporation

- Noritz Corporation

Frequently Asked Questions

The domestic heating appliances market is projected to reach US$ 103.0 billion by 2033, growing at a CAGR of 7.9% from 2026 to 2033, driven by urbanization, energy‑efficiency regulations, and rising adoption of smart and renewable‑integrated systems.

Key demand drivers include rising urbanization, increasing homeownership, stricter energy‑efficiency regulations, and growing disposable incomes, which together boost demand for room heating, water heating, and cooking appliances across residential and commercial end‑uses.

The electric segment dominates the domestic heating appliances market by energy source, accounting for about 45% of the market due to ease of installation, low maintenance, and compatibility with smart‑home platforms and renewable electricity.

Europe leads the domestic heating appliances market, supported by stringent EU energy‑efficiency directives, strong policy incentives for low‑carbon heating, and high penetration of smart and heat‑pump‑based systems.

A key growth opportunity lies in renewable‑integrated and smart heating solutions, including heat pumps, solar‑assisted water heaters, and IoT‑enabled appliances, which align with global decarbonization goals and consumer demand for energy‑efficient comfort.