- Medical Devices

- Orthopedic Trauma Devices Market

Orthopedic Trauma Devices Market Size, Share, and Growth Forecast 2026 – 2033

Orthopedic Trauma Devices Market by Product (Internal Fixators: Screws, Plates, Intramedullary Nails, Others; External Fixators: Unilateral Fixators, Circular Fixators, Hybrid Fixators), End-user (Hospitals, Orthopedic and Trauma Centers, Ambulatory Surgical Centers), and Regional Analysis, 2026–2033

Orthopedic Trauma Devices Market Size and Share Analysis

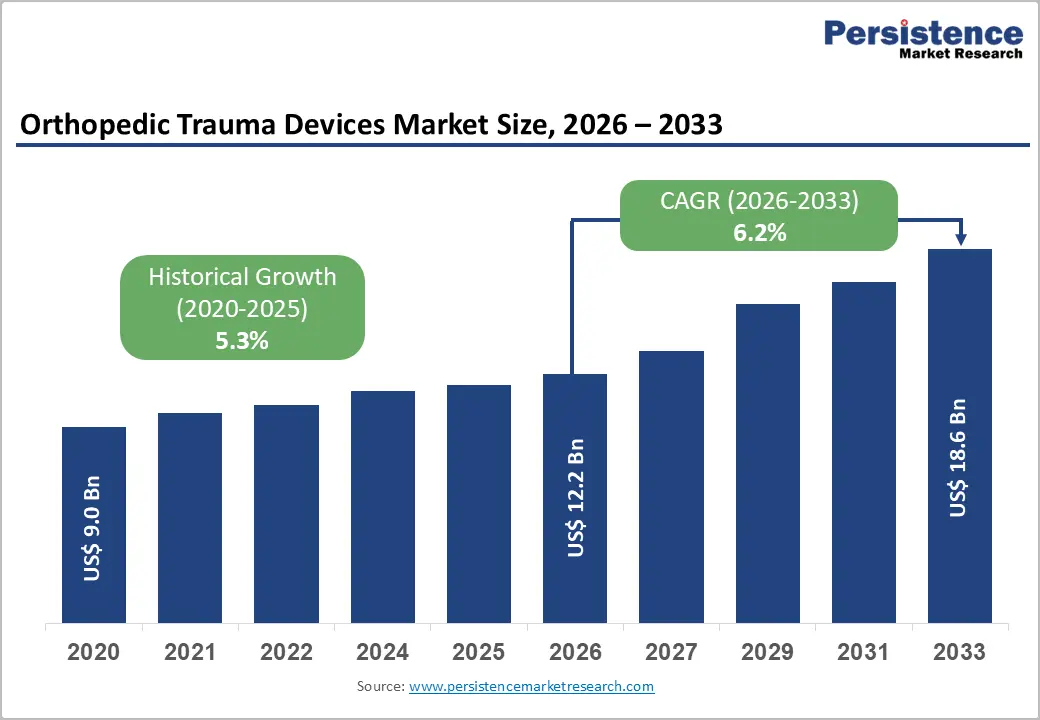

The global orthopedic trauma devices market size is expected to be valued at US$ 12.2 billion in 2026 and projected to reach US$ 18.6 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033. This growth is primarily propelled by a global surge in road traffic accidents, sports-related injuries, and osteoporotic fractures among the aging population. According to the World Health Organization (WHO), road traffic injuries affect approximately 1.19 million people annually, generating persistent clinical demand for fixation devices. Concurrently, the rising prevalence of osteoporosis affecting over 200 million individuals globally per the International Osteoporosis Foundation (IOF) and accelerating adoption of minimally invasive surgical techniques are reinforcing market expansion across both developed and emerging healthcare systems.

Key Industry Highlights:

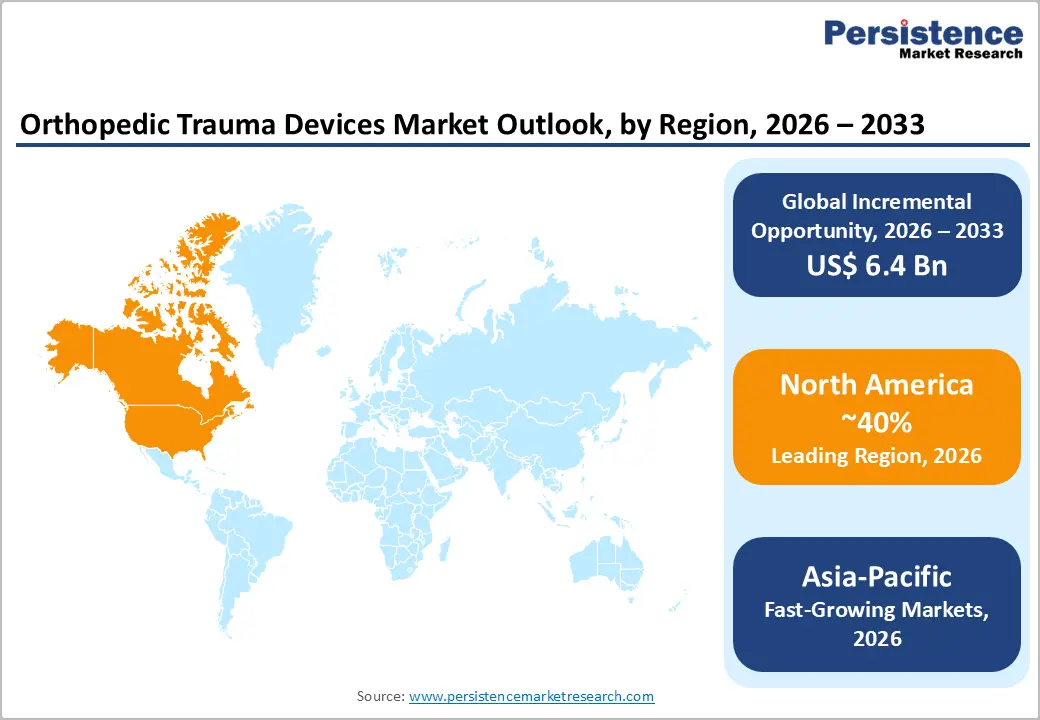

- Leading Region: North America leads the global Orthopedic Trauma Devices market with approximately 40% share in 2025, supported by high trauma incidence, 6.3 million annual fractures, advanced surgical infrastructure, and favorable Medicare/Medicaid reimbursement frameworks.

- Fastest Growing Region: Asia Pacific is the fastest growing region, driven by rapid motorization, Healthy China 2030 investments, India's expanding private hospital network, and Japan's large osteoporotic fracture burden in an aging population exceeding 29% over age 65.

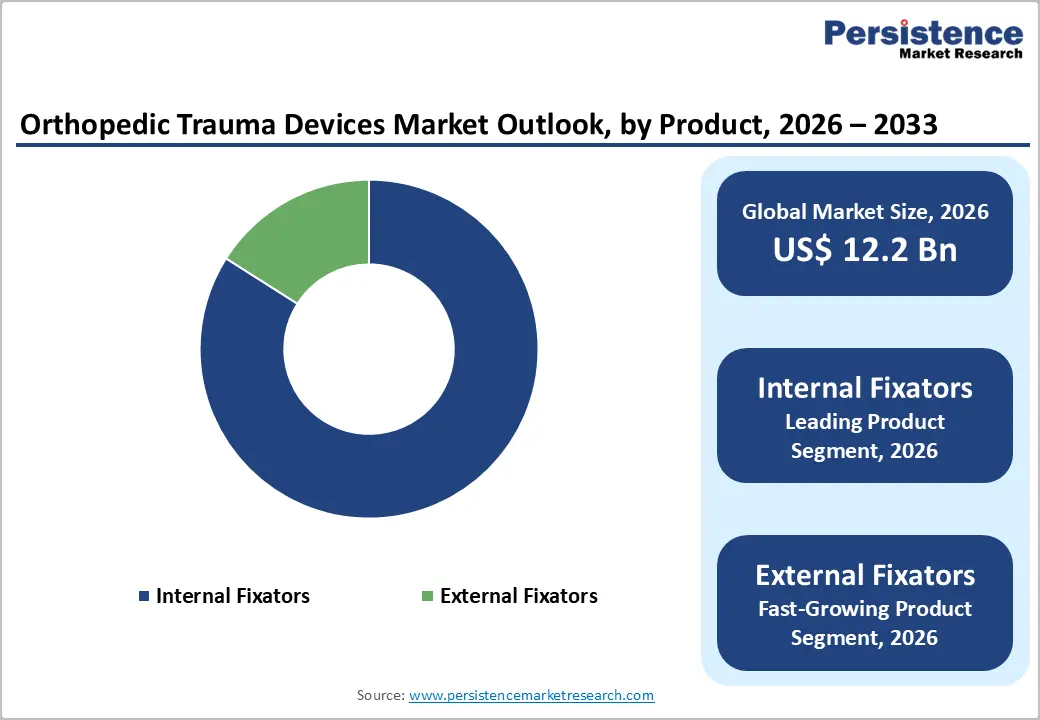

- Dominant Segment: Internal Fixators dominate the Product category with approximately 84% market share in 2025, led by intramedullary nails and locking plates as the gold-standard treatment for over 90% of long-bone diaphyseal fractures globally.

- Fastest Growing Segment: External Fixators represent the fastest growing product segment, driven by expanding use in polytrauma damage control protocols, open fractures, and limb lengthening procedures, particularly in emerging markets with growing trauma surgery volumes.

- Key Opportunity: Bioresorbable and biodegradable fixation implants offer transformational commercial potential, eliminating secondary removal surgeries, supported by FDA Breakthrough Device pathways and expanding clinical evidence validating magnesium-alloy screw performance.

Market Dynamics

Drivers - Rising Incidence of Traumatic Injuries and Road Traffic Accidents

The escalating global burden of trauma injuries represents the most fundamental demand driver for orthopedic fixation devices. The WHO's Global Status Report on Road Safety estimates that road traffic crashes cause over 1.19 million deaths annually and injure tens of millions more, a substantial proportion of whom require surgical bone fixation.

In the United States alone, the Centers for Disease Control and Prevention (CDC) reports nearly 3 million nonfatal traumatic injuries annually requiring emergency orthopedic intervention. Additionally, rapid urbanization and increased motorization in developing nations are amplifying trauma incidence in the Asia Pacific and Latin America, creating a geographically expanding addressable market for internal and external fixation devices.

Restraints - Stringent Regulatory Approval Processes and Lengthy Clearance Timelines

The orthopedic trauma device sector faces rigorous regulatory oversight from agencies including the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA). The transition to the EU Medical Device Regulation (MDR 2017/745) significantly extended approval timelines and increased compliance costs, with many manufacturers reporting certification delays exceeding 18–24 months. These prolonged timelines delay revenue generation for new product introductions, disproportionately impacting small and mid-sized device companies and constraining the pace of product innovation reaching clinical practice.

Opportunities - Accelerating Adoption of Bioresorbable and Biodegradable Fixation Implants

Bioresorbable orthopedic implants represent one of the most compelling next-generation opportunities in the trauma devices space. Unlike conventional metallic fixators, biodegradable implants fabricated from materials such as poly-lactic acid (PLA) and magnesium alloys gradually resorb within the body, eliminating the need for secondary removal surgeries and associated complications. A 2023 study published in the journal Biomaterials demonstrated that magnesium-based bone screws achieved equivalent mechanical performance to titanium in distal radius fractures while enabling natural bone remodeling.

The FDA's Breakthrough Device Designation program has fast-tracked several biodegradable fixation devices, reducing development timelines. As clinical evidence expands and manufacturing costs decline, bioresorbable implants are poised to capture a meaningful and growing share of the pediatric and upper-extremity trauma device segments globally.

Category-wise Analysis

Product Insights

The Internal Fixators segment is the undisputed leader within the Product category, commanding approximately 84% of the global Orthopedic Trauma Devices market share in 2025. This dominance reflects the clinical primacy of internal fixation as the gold-standard surgical approach for most closed fractures across the appendicular skeleton. Within this segment, locking plates and intramedullary nails drive the highest procedure volumes, particularly for femoral, tibial, and humeral fractures. According to the American Academy of Orthopaedic Surgeons (AAOS), intramedullary nailing is the preferred technique for over 90% of long-bone diaphyseal fractures, given its biomechanical advantages and faster patient mobilization outcomes. The segment benefits from continuous product innovation including anatomically contoured locking plates and titanium alloy nails with advanced interlocking mechanisms.

End-user Insights

Hospitals represent the dominant end-user segment, accounting for approximately 62% of the Orthopedic Trauma Devices market share in 2025. This dominance is rooted in hospitals' comprehensive trauma management infrastructure, including advanced imaging (CT, MRI, fluoroscopy), dedicated operating theaters, intensive care units, and multidisciplinary trauma teams, which is essential for managing complex polytrauma cases that constitute a significant share of fixation device utilization.

Level I and II trauma centers designated by the American College of Surgeons (ACS) handle the highest acuity fracture cases requiring premium implant systems. Furthermore, hospitals' ability to handle emergency, high-complexity cases and their established procurement relationships with major device companies reinforce their market leadership, even as ASC volume grows for less complex outpatient procedures.

Regional Insights

North America Orthopedic Trauma Devices Market Trends and Insights

North America dominates the orthopedic trauma devices market due to a very high incidence of fractures, advanced trauma infrastructure, and strong surgical adoption rates. The region benefits from one of the world’s largest elderly populations, where falls are a leading cause of injury. According to CDC-based national datasets, the U.S. records 7+ million orthopedic injury hospital encounters annually, with over 1.1 million emergency orthopedic surgeries.

High healthcare expenditure and widespread insurance coverage support the rapid adoption of internal fixation devices. The region also has 1,000+ Level I trauma centers, ensuring strong procedural volume and device utilization. This mature ecosystem makes North America the global demand leader.

U.S. Orthopedic Trauma Devices Market Trends and Insights

The U.S. is the largest contributor and is expected to reach ~US$ 5.0 Bn by 2026 within the trauma devices segment. The CDC reports that 1 in 4 older adults experiences a fall annually, significantly driving fracture-related surgeries. Hip fractures alone exceed 300,000 cases per year, most requiring surgical fixation. High adoption of minimally invasive internal fixation and robotic-assisted orthopedic surgery further strengthens device demand. The presence of major players like J&J and Stryker ensures continuous innovation and procedural penetration across hospitals and trauma centers.

Canada Orthopedic Trauma Devices Market Trends and Insights

Canada shows steady growth driven by aging demographics and provincial healthcare systems. It records hundreds of thousands of fracture-related admissions annually, with hip fractures being a major burden among elderly populations. Public healthcare coverage ensures universal access to trauma surgery, supporting consistent demand for implants. However, a lower population size compared to the U.S. limits its absolute market contribution.

Europe Orthopedic Trauma Devices Market Trends and Insights

Europe is a highly important orthopedic trauma market due to strong public healthcare systems, high fracture incidence, and aging demographics. Eurostat-linked demographic data show that the EU population aged 65+ is projected to reach 30% by 2050, significantly increasing fragility fractures. The region reports 7+ million fracture cases annually, with hip fractures alone exceeding 620,000 cases per year, a major driver of trauma implant demand. Europe also has strong regulatory frameworks and R&D funding (e.g., EU health research programs), supporting innovation in fixation devices and biomaterials. High adoption of internal fixation systems (~65% of surgeries) further strengthens its market position.

Germany Orthopedic Trauma Devices Market Trends and Insights

Germany is expected to reach ~US$ 2.2–2.5 Bn by 2026, making it the largest orthopedic trauma market in Europe. It has one of the highest surgical rates for fracture management, supported by universal insurance coverage and advanced hospital infrastructure. Germany also reports a high incidence of osteoporosis-related fractures due to its aging population. Strong presence of orthopedic manufacturers and early adoption of locking plates and intramedullary nails further reinforce demand.

France Orthopedic Trauma Devices Market Trends and Insights

France is a major contributor with increasing trauma case volumes, especially among elderly populations. Public healthcare ensures high access to surgical fixation procedures. Road traffic injuries and sports-related fractures also contribute significantly to orthopedic trauma demand.

Asia Pacific Orthopedic Trauma Devices Market Trends and Insights

Asia Pacific is the fast-growing market, driven by rising trauma burden, expanding healthcare infrastructure, and improving surgical access. According to global burden datasets (GBD/road injury studies), the region records 20+ million fracture cases annually, with 4+ million requiring surgical intervention. Rapid urbanization and motorization have increased road traffic accidents, a major cause of orthopedic trauma. Countries like China and India are investing heavily in healthcare capacity expansion and trauma systems. Government schemes such as India’s Ayushman Bharat and China’s hospital modernization programs are improving access to orthopedic surgeries, accelerating device adoption.

China Orthopedic Trauma Devices Market Trends and Insights

China is expected to reach ~US$3.3 billion by 2026, driven by high trauma incidence and large population base. It performs 1.2+ million orthopedic trauma surgeries annually, supported by expanding tertiary hospitals. Rapid industrialization and road accidents contribute significantly to fracture burden. Government healthcare reforms and rising insurance penetration are improving access to advanced fixation devices, including minimally invasive implants.

India Orthopedic Trauma Devices Market Trends and Insights

India is the fast-growing market due to increasing road accidents and expanding healthcare access. It reports 800,000+ orthopedic trauma surgeries annually, with rising penetration of private hospitals and trauma centers. Government initiatives are expanding insurance coverage and orthopedic infrastructure. Increasing awareness of surgical fixation over conservative treatment is accelerating the adoption of internal fixation devices.

Competitive Landscape

The orthopedic trauma devices market is moderately consolidated, with a handful of global players, including Johnson & Johnson (DePuy Synthes), Stryker Corporation, Zimmer Biomet, and Smith & Nephew collectively commanding a majority of global revenues. Key competitive differentiators include breadth of implant portfolios, surgeon education programs, and OR workflow integration. Companies are investing heavily in robotic-assisted surgical platforms, smart implant technologies with sensor integration, and biodegradable fixation materials. Regional players in Asia, particularly in China and India, are intensifying competition in the mid-tier segment through competitive pricing and government tender participation.

Key Developments

- February, 2026: Zimmer Biomet had released new clinical and performance data and highlighted its key innovations at the American Academy of Orthopaedic Surgeons (AAOS) Annual Meeting. The company showcased advancements across its orthopedic portfolio, including trauma, joint reconstruction, and robotic-assisted surgical solutions.

- October, 2025: Johnson & Johnson had announced its intent to separate its Orthopaedics business into a standalone entity. The move was aimed at sharpening strategic focus, improving operational agility, and allowing both businesses to pursue more targeted growth opportunities.

Global Orthopedic Trauma Devices Market – Key Insights

|

Key Insights |

Details |

|

Historical Market Value (2020) |

US$ 9.0 Billion |

|

Projected Market Value (2026) |

US$ 12.2 Billion |

|

Projected Market Value (2033) |

US$ 18.6 Billion |

|

CAGR (2026-2033) |

6.2% |

|

Leading Region |

North America, 40% share |

|

Dominant Product |

Internal Fixators, 84% share |

|

Top-ranking End User |

Hospitals, 70% share |

|

Incremental Opportunity |

US$ 6.4 billion |

Companies Covered in Orthopedic Trauma Devices Market

- Johnson & Johnson Services, Inc.

- Zimmer Biomet Holdings, Inc.

- Stryker Corporation

- Smith & Nephew

- B. Braun Melsungen AG

- Wright Medical Group N.V.

- Orthofix International N.V.

- Integra LifeSciences

- Citieffe S.R.L.

- Acumed

- Others

Frequently Asked Questions

The global orthopedic trauma devices market is valued at approximately US$ 12.2 billion in 2026

Rising fractures, aging population, road accidents, sports injuries, osteoporosis prevalence, and minimally invasive surgical adoption.

North America is the leading region with approximately 40% global market share in 2025, underpinned by approximately 6.3 million annual fractures in the U.S. (CDC), advanced trauma center infrastructure, and comprehensive Medicare/Medicaid reimbursement for orthopedic procedures.

Expanding emerging markets, minimally invasive fixation systems, bioabsorbable implants, and robotics-assisted trauma surgeries.

Johnson & Johnson Services, Inc., Zimmer Biomet Holdings, Inc., Stryker Corporation, Smith & Nephew B. Braun Melsungen AG, Wright Medical Group N.V.