- Biotechnology

- Next Generation Antibody Therapeutics Market

Next Generation Antibody Therapeutics Market Size, Share, Growth, and Regional Forecast, 2025 to 2032

Next Generation Antibody Therapeutics Market by Technology (Antibody-drug Conjugates (ADCs), Bispecific Antibodies, Multispecific Antibodies, Nanobodies, Others), Therapeutic Area, End-user and Regional Analysis from 2025 to 2032

Next Generation Antibody Therapeutics Market Share and Trends Analysis

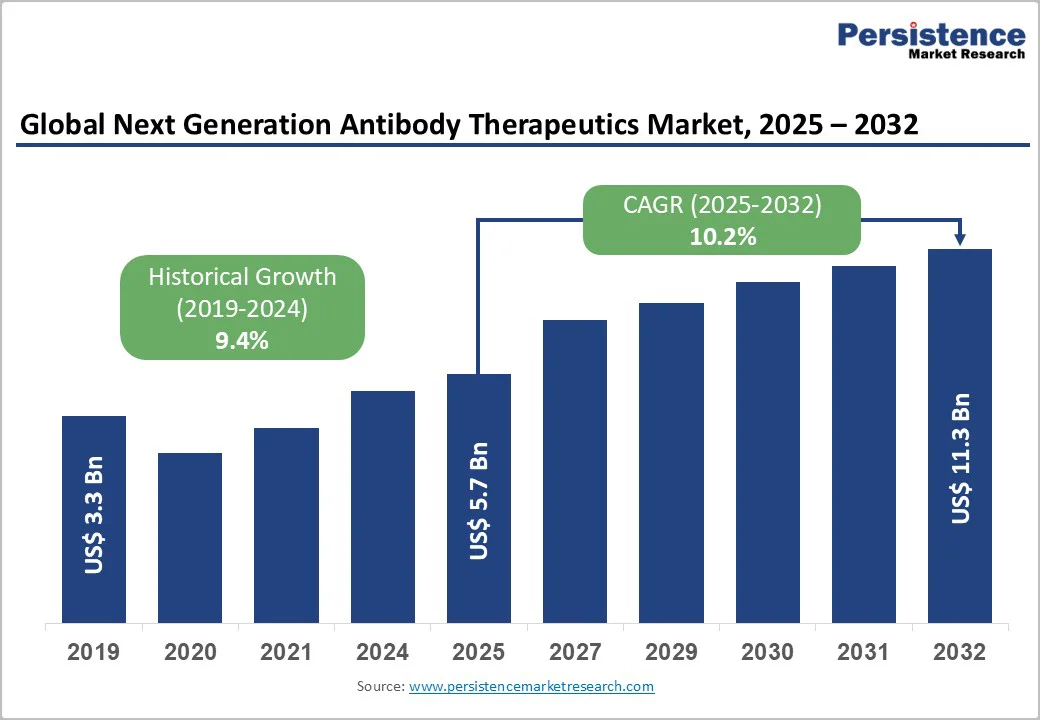

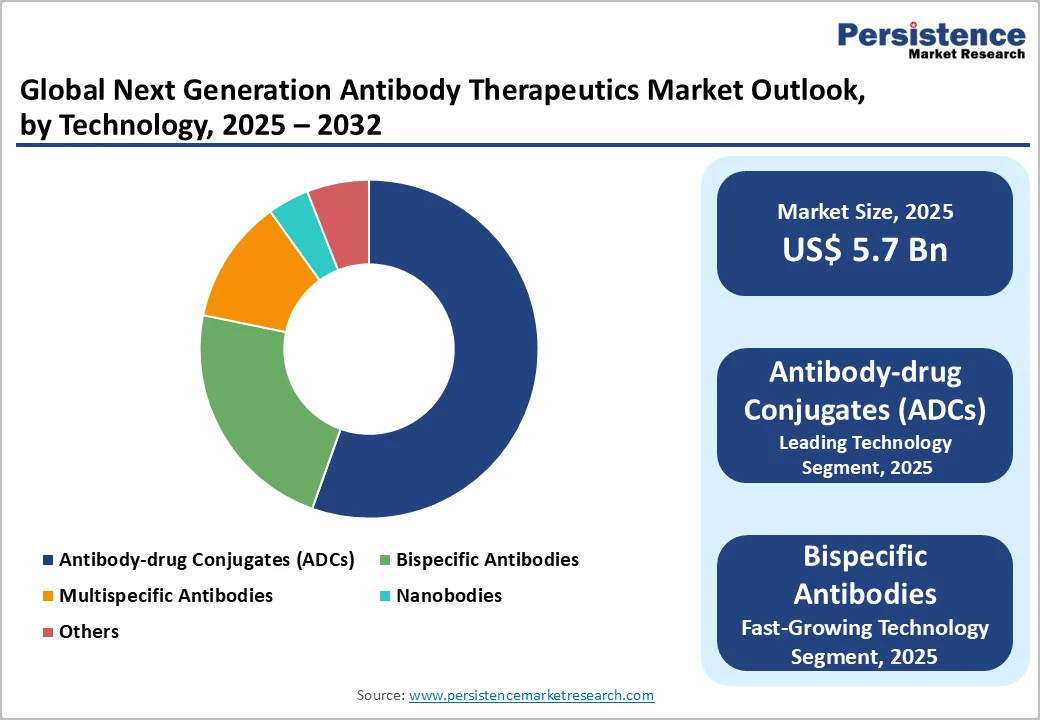

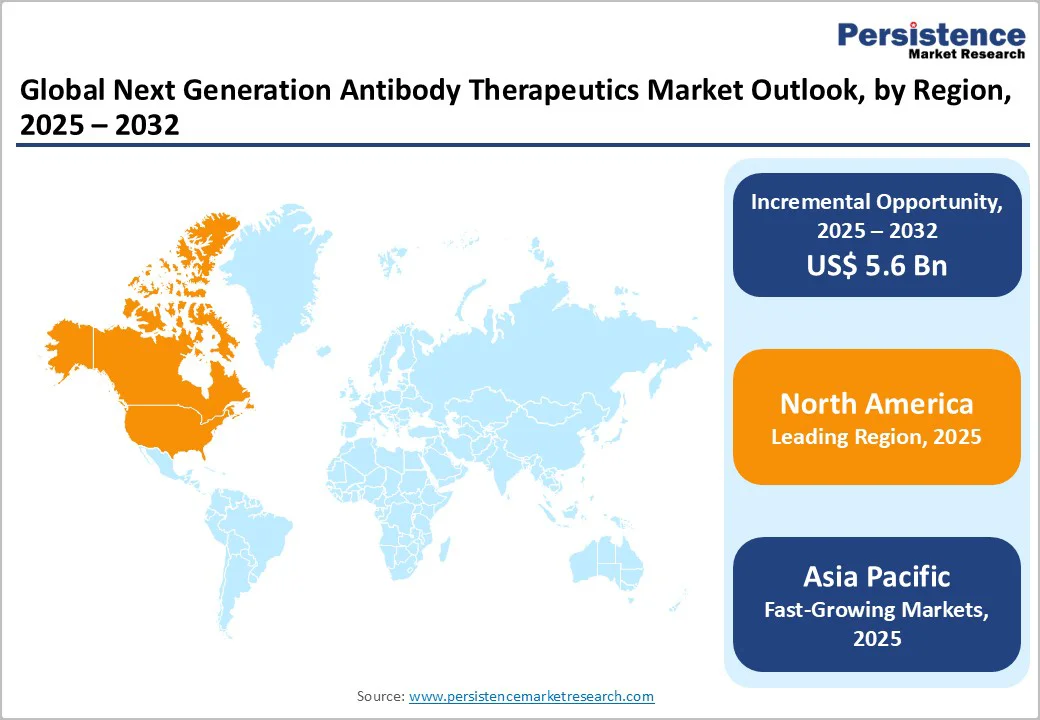

The global next-generation antibody therapeutics market size is valued at US$5.7 billion in 2025 and is projected to reach US$11.3 billion, growing at a CAGR of 10.2% between 2025 and 2032.

Biopharmaceuticals have transformed modern medicine, with antibodies representing a key segment, accounting for nearly 40% of therapeutics used clinically and non-clinically. The success of monoclonal antibodies has paved the way for next-generation antibody therapeutics, including bispecifics, antibody-drug conjugates, and polyspecific formats, designed to enhance specificity, potency, and safety.

These innovations address limitations of traditional antibodies, such as limited targetable proteins, poor tissue accessibility, and resistance mechanisms.

Key Industry Highlights

- Antibody-drug conjugates (ADCs) dominate globally, capturing nearly 38% of the revenue share in 2025, driven by targeted delivery to tumor cells, improved efficacy, reduced toxicity, and growing adoption in oncology.

- Oncology is the primary therapeutic area with ~64.3% market share, driven by rising cancer prevalence and unmet treatment needs.

- Bispecific antibodies are the fastest-growing segment, offering dual-targeting capabilities that enhance specificity, potency, and enable novel therapeutic approaches.

- North America leads the market with 48.8% share, supported by innovation, regulatory support, and a strong clinical pipeline.

- Europe benefits from regulatory harmonization through EMA, promoting the adoption of ADCs, bispecifics, and other antibody therapies across member states.

- Asia Pacific is rapidly expanding, driven by Japan and India’s growing biotech ecosystems, regulatory reforms, and emerging startups.

- Collaborations and partnerships dominate, accelerating development pipelines, enhancing technological capabilities, and expanding treatment options globally.

- Technological innovations in antibody engineering, including polyspecific and modular formats, drive faster discovery and broader therapeutic applications.

- Regulatory support and policy reforms in key regions facilitate market access, accelerate clinical adoption, and encourage investment in novel antibodies.

| Key Insights | Details |

|---|---|

| Global Next Generation Antibody Therapeutics Market Size (2025E) | US$ 5.7 Bn |

| Market Value Forecast (2032F) | US$11.3 Bn |

| Projected Growth (CAGR 2025 to 2032) | 10.2% |

| Historical Market Growth (CAGR 2019 to 2024) | 9.4% |

Market Dynamics

Driver - Expanding Impact of Next-Generation Antibody Therapeutics Across Challenging Disease Areas

Therapeutic antibodies have emerged as a dominant class of drugs, transforming treatment across oncology, autoimmune, and infectious diseases. Advances in antibody engineering, including novel scaffolds, modular formats, and optimized discovery platforms, are driving next-generation therapeutics with enhanced specificity, potency, and broader disease coverage.

Companies like Numab pioneer multispecific antibodies to target complex disease mechanisms, while Nona Biosciences and Kodiak Sciences collaborate to develop ophthalmic-focused next-generation antibodies. Similarly, Abilita Therapeutics’ EMP™ platform targets previously undruggable membrane proteins, with collaborations advancing oncology and pain therapeutics into clinical pipelines.

These innovations accelerate development timelines, overcome traditional therapeutic limitations, and expand treatment impact in previously inaccessible disease areas. Collectively, next-generation antibody therapeutics are a key driver of improved patient access, clinical outcomes, and growth in the global antibody therapeutics market.

Restraints - Engineering Challenges and Cost Implications in Next-Generation Antibody Design

The design of next-generation antibodies involves intricate engineering to optimize stability, binding specificity, and effector functions. Achieving the desired structural and functional attributes often requires iterative cycles of molecular modeling, mutagenesis, and extensive preclinical testing.

These processes are resource-intensive, demanding sophisticated platforms, skilled personnel, and high-quality materials, which collectively drive up development and manufacturing costs. Such complexities can slow the pace of innovation, increase time-to-market, and limit the affordability and accessibility of next-generation antibody therapeutics, especially in cost-sensitive regions.

Production and Operational Complexities in Antibody Therapeutics

Next-generation antibody therapeutics require highly controlled, large-scale biomanufacturing processes to ensure product consistency, purity, and efficacy. Advanced production platforms, specialized facilities, and stringent quality control measures contribute to substantial capital expenditures (CAPEX) and operational expenditures (OPEX).

Additionally, scaling complex antibody formats such as bispecifics or multispecifics further increases costs. These financial demands can limit the number of manufacturers able to enter the market, slow commercialization, and restrict patient access, particularly in emerging regions, thereby making rising manufacturing costs a significant restraint on the growth of the global antibody therapeutics market.

Opportunity - AI-Enabled Antibody Engineering: Unlocking Next-Generation Therapeutics Market Potential

Advances in antibody engineering, powered by AI and machine learning, are revolutionizing next-generation antibody therapeutics. While traditional methods such as immunization, B-cell screening, and synthetic library generation have contributed to ~80 FDA-approved antibodies, they face inherent limitations, including epitope bias and limited sequence diversity.

AI-driven platforms can address these gaps by analyzing vast datasets, predicting high-affinity candidates, and enabling epitope-specific design for greater precision and efficacy.

Companies like BigHat Biosciences integrate AI and wet-lab cycles to optimize antibodies rapidly, while Talem Therapeutics leverages computational design for unique antibody assets. Similarly, DesertSci applies AI-enhanced workflows to accelerate therapeutic discovery.

Together, modular engineering approaches, novel scaffolds, and machine learning create opportunities to compress discovery timelines, overcome traditional bottlenecks, and expand the therapeutic reach of antibodies into challenging disease areas.

Addressing Unmet Cancer Care Needs Through Policy Support and Antibody Innovation

The global cancer burden continues to rise, with over 20 million new cases and nearly 10 million deaths in 2022, with an estimation to reach over 35 million by 2050. This highlights the urgent need for effective, targeted therapies. Next-generation antibody therapeutics, including bispecific antibodies and antibody-drug conjugates, offer precise tumor targeting while minimizing damage to healthy tissue, addressing critical gaps in treatment.

Emerging markets, particularly in Asia and Africa, are expanding healthcare infrastructure and improving access to advanced therapies. Concurrently, supportive regulatory reforms and enhanced reimbursement frameworks are facilitating faster approvals and broader adoption. Together, these factors create significant opportunities to meet unmet patient needs, expand access, and strengthen the impact of next-generation antibody therapeutics globally.

Category-wise Analysis

Technology Insights

The Antibody-Drug Conjugates (ADCs) segment is expected to dominate the global market with nearly 38% revenue share in 2025. ADCs combine the targeting precision of monoclonal antibodies with potent cytotoxic agents, enabling selective delivery of drugs directly to tumor cells while sparing healthy tissue. This targeted approach improves treatment efficacy and safety profiles, making them highly attractive for oncologists and patients.

Strong clinical success across multiple cancer types, ongoing pipeline development, and increasing regulatory approvals further drive adoption. Additionally, advancements in linker technologies and payload optimization are expanding ADC applicability, solidifying their position as a leading therapeutic modality.

Additionally, Bispecific Antibodies are experiencing rapid growth due to their ability to simultaneously target two distinct antigens, enhancing therapeutic efficacy, improving immune engagement, and expanding treatment options across oncology and autoimmune diseases.

Therapeutic Area Insights

The oncology segment is projected to remain the primary therapeutic area, capturing approximately 64.3% of the market by the end of 2025. Cancer continues to represent a major global health burden, with rising incidence and mortality rates fueling urgent demand for effective therapies.

Next-generation antibody therapeutics are increasingly being adopted for their precision, reduced side effects, and ability to address previously untreatable tumor types. High investment in oncology research, regulatory incentives, and growing awareness among healthcare providers are driving robust growth in this segment, reinforcing oncology as a key driver of market expansion.

The autoimmune/inflammatory segment is projected to experience the strongest growth trajectory, driven by the rising prevalence of disorders such as rheumatoid arthritis, psoriasis, and inflammatory bowel disease. Targeted next-generation antibodies are increasingly adopted in this area for their ability to precisely modulate immune responses, offering improved safety and efficacy profiles, which is accelerating market expansion.

Regional Insights

North America Next Generation Antibody Therapeutics Market Trends

The North America Next Generation Antibody Therapeutics Market is expanding rapidly and is projected to account for 48.8% of the global market share by 2025, with the U.S. leading this expansion.

The robust innovation ecosystem, a supportive regulatory framework, and substantial investment in biotechnology drive the regional market. Advancements in antibody engineering technologies coupled with growing investments in biotechnology directed toward research and development of next-generation therapeutics reflect strong confidence in the sector.

The FDA’s expedited approval pathways and clear regulatory guidelines facilitate rapid clinical adoption, while the competitive landscape is shaped by established pharmaceutical giants and emerging biotech firms fostering innovation.

Notably, collaborations such as Regeneron Pharmaceuticals’ $326 million agreement with the U.S. Biomedical Advanced Research and Development Authority (BARDA) in 2023, to develop next-generation monoclonal antibodies against SARS-CoV-2 highlight North America’s strategic focus on public health preparedness, rapid development, and regulatory-aligned commercialization.

These combined factors reinforce North America as a pivotal region for antibody therapeutics, driving innovation, market growth, and expanded patient access across oncology, autoimmune, and infectious disease segments.

Europe Next Generation Antibody Therapeutics Market Trends

Europe holds a strategic position in the global market, driven by a strong focus on innovation, clinical adoption, and regulatory harmonization.

The European Medicines Agency (EMA) provides a centralized framework that ensures consistent quality, safety, and efficacy standards across member states, facilitating the approval and commercialization of advanced therapies such as bispecific antibodies, antibody-drug conjugates (ADCs), and other antibody treatments.

The region is witnessing growing emphasis on precision medicine, the integration of AI-driven discovery platforms, and collaborative research initiatives that enhance the development of next-generation therapeutics.

Events such as the upcoming PEGS Summit Europe in November 2025 are expected to spotlight breakthroughs in antibody engineering, bispecific Abs, ADCs, CAR therapies, and AI-enhanced discovery, fostering knowledge exchange and partnerships among leading researchers, clinicians, and biopharma innovators.

Rising prevalence of complex diseases and the adoption of novel therapeutic modalities further accelerate market growth, while regulatory alignment ensures smoother clinical translation. Together, these factors position Europe as a hub for innovation, collaboration, and adoption of cutting-edge antibody therapeutics, reinforcing its role in shaping the future of the global market.

Asia Pacific Next Generation Antibody Therapeutics Market Trends

Asia Pacific is experiencing rapid growth in the next-generation antibody therapeutics market, driven by advancements in biotechnology, increasing healthcare demands, and supportive regulatory environments.

Japan is a key contributor, supported by a mature regulatory system that enables streamlined approval and adoption of innovative therapies.

The Manufacturing Technology Association of Biologics (MAB)-comprising companies, universities, and research institutions- has been actively engaged in manufacturing technologies, high-performance cell lines, and quality control methods, for next-generation antibody drugs that conform to global standards. Thereby, enhancing Japan’s capabilities in producing innovative antibodies and reinforcing its leadership in the global biopharmaceutical industry.

India is emerging as a biotechnology hub, with numerous startups and research collaborations advancing antibody-based therapeutics. For example, Avammune Therapeutics in Bengaluru raised funding in 2025 to accelerate development of novel therapeutics, while partnerships between academic institutions such as the University of Hyderabad and companies such as Krismo Biosciences are fostering next-generation therapy research targeting infectious and chronic diseases.

The region also benefits from platforms like the Antibody Engineering & Therapeutics Asia 2025 conference, scheduled for November 2025, which will highlight breakthroughs in antibody engineering, bispecifics, ADCs, CAR therapies, and AI-driven discovery, facilitating collaboration between researchers and biopharma innovators.

Together, these developments reflect APAC’s dynamic ecosystem, emphasizing innovation, collaborative research, and regulatory support, positioning the region as a significant contributor to the global advancement of next-generation antibody therapeutics.

Competitive Landscape

The next-generation antibody therapeutics market is highly dynamic and moderately fragmented, characterized by extensive collaborations, strategic partnerships, and continuous innovation in antibody engineering, bispecifics, and ADCs.

Rapid technological advancements, preclinical pipeline expansion, and cross-sector collaborations drive competitive differentiation, fostering accelerated development and diversified treatment options across oncology, immunology, and infectious diseases.

Key Industry Developments:

- Seromyx announced its participation in the upcoming Antibody Engineering & Therapeutics conference in December 2025, presenting its advances in antibody discovery, engineering, and functional profiling to accelerate next-generation antibody therapeutics across oncology, immunology, and infectious diseases.

- In July 2025, Akari Therapeutics advanced research on its novel ADC payload PH1, highlighting its unique mechanism to selectively target cancers while demonstrating potential for improved safety and efficacy compared to conventional ADC technologies.

- In July 2025, Eli Lilly and BigHat Biosciences entered an AI-driven antibody discovery collaboration to design next-generation therapeutic antibodies, combining Lilly’s development expertise with BigHat’s machine-learning platform to accelerate precision biologics development.

- In April 2025, Harbour BioMed and AstraZeneca announced a global strategic collaboration to discover and develop next-generation therapeutic antibodies using Harbour’s transgenic Harbour Mice® platform, aiming to enhance innovation and expand treatment options across multiple disease areas.

- In April 2025, Nona Biosciences and Atossa Therapeutics announced a research collaboration leveraging Nona’s Harbour Mice® platform to develop fully human monoclonal antibodies, aiming to accelerate next-generation antibody therapies for breast cancer.

Companies Covered in Next Generation Antibody Therapeutics Market

- AbbVie Inc.

- AstraZeneca

- NBE-Therapeutics AG (Behringer Ingelheim)

- Antibody Therapeutics Inc. (JHBP company)

- Sino Biological, Inc.

- Genmab A/S

- abpro

- AbTherx, Inc

- Nona Biosciences

- Numab Therapeutics AG

- Zymeworks Inc.

- Radiance Biopharma Inc.

- Harbour BioMed

- Hummingbird Bioscience

- Regeneron Pharmaceuticals Inc.

- F-star Therapeutics Ltd.

- Biocytogen

- Akari Therapeutics

- Y-BIOLOGICS

- Alchemab Therapeutics

- Aganitha AI Inc.

- Eli Lilly and Company

- AAX Biotech

Frequently Asked Questions

The global next generation antibody therapeutics market is projected to be valued at US$ 5.7 Bn in 2025.

Technological innovations in antibody engineering, rising prevalence of cancer and autoimmune disorders, and strong clinical trial successes drive the global market.

The global market is poised to witness a CAGR of 10.2% between 2025 and 2032.

Key opportunities lie in AI-driven antibody discovery, expansion into neurodegenerative and rare diseases, and growing adoption of multi-specific and antibody-drug conjugate platforms.

Major players in the global are AbbVie Inc., AstraZeneca, Eli Lilly and Company, Sino Biological, Inc., Regeneron Pharmaceuticals Inc., NBE-Therapeutics AG (Behringer Ingelheim) and others.